Good morning!

In overnight trading, the FTSE is up 0.7% and the S&P is up 1.6%, as a US federal court has just blocked Trump's tariff plans. The Court of International Trade says that the US Congress has exclusive authority to regulate international trade, not the President.

Trump has filed an appeal, and I note that the Republican Party does currently control Congress. Even so, this appears to be a very large spanner in the tariff agenda.

1.50pm: we've run out of time for today, thanks everyone.

Today's agenda is complete.

Companies Reporting

| Name (Mkt Cap) | RNS | Summary | Our view (Author) |

|---|---|---|---|

Auto Trader (LON:AUTO) (£7.90bn) | Revenue +5%, op profit +8% (£377m). 2026 outlook: retailer rev growth to improve to 5-7%. | ||

Harbourvest Global Private Equity (LON:HVPE) (£1.78bn) | NAV per share return +7.3%, share price +19.2%. Discount to NAV falls from 42% to 35%. | GREEN (Graham) I don't see what the "catch" is - to my eyes it's a reputable, well-diversified investment trust with historical performance of c. 10% annually, currently trading at a very large discount to NAV. | |

Capital Gearing Trust (LON:CGT) (£846m) | NAV return 4.1%, share price +3.6% vs. CPI +2.6%. Discount to NAV 2.8%. Defensively positioned. Paid £194.5m to repurchase shares during the financial year. It also plans to pay a 102p final dividend, due to higher interest income from investments. Outlook: the company should remain “a relatively safe haven for your money as we aim to limit drawdowns and yet keep pace with inflation”. | AMBER/GREEN (Graham) [no section below] This is another very reputable trust although far less ambitious than others: it aims merely to preserve wealth by beating inflation. It has successfully done this in FY March 2025 and has also kept its discount under tight control by buying back a very large percentage of its shares. I view this trust as a solid choice for investors seeking a lower-risk holding. | |

Cohort (LON:CHRT) (£724m) | FY April 2025: strong growth in revenue and profit, in line with exps. Outlook: unchanged. | ||

Resolute Mining (LON:RSG) (£617m) | Media reports permits possibly being revoked. Company seeking information and clarification. | ||

Atalaya Mining Copper SA (LON:ATYM) (£581m) | Copper production 14.3kt. Cash cost well below FY25 guidance. CEO v. optimistic for year ahead. | ||

Hollywood Bowl (LON:BOWL) (£500m) | SP down 8% LfL rev +2.1%. Warm, dry weather a recent headwind. FY EBITDA to fall within range of forecasts. | ||

Rockhopper Exploration (LON:RKH) (£353m) | $79.8m from arbitration case (risk of annulment). Sea Lion in Falklands seeks bank financing. | Graham [no section below] Two points stand out. 1) it is very late to publish Dec 2024 results. 2) the company acknowledges that it will likely need more equity funding if Sea Lion is to go ahead. | |

Home Reit (LON:HOME) (£301m) | Managed wind down strategy continues to progress. Possible legal issues. | (Graham) [no section below] N.B. Shares remain suspended long-term as the company has been unable to publish timely accounts. Results for FY August 2023 were published in January 2025! | |

Filtronic (LON:FTC) (£274m) | Order valued at £0.8m to supply modules for airborne radar application in H2 of next year. | (Graham) [no section below] Is it really necessary to publish an RNS for a contract of this size? | |

Serabi Gold (LON:SRB) (£116m) | Gold production +11.2% to 10,013oz. EPS +140% to 11.58c. AISC $1636/oz down 12%. Net cash balance $20.9m. | AMBER/GREEN (Mark) | |

Software Circle (LON:SFT) (£116m) | FY 3/25: Rev +13% to £18.3m. Organic revenue down 7%. Operating EBITDA +22% organic, added £1.1m through acquisition to give £4.8m. Operating cash flow per share 0.5p (FY24: 0.6p). | AMBER/RED (Mark) [no section below] | |

Premier Miton (LON:PMI) (£105m) | AUM £10.2bn (30 Sep 24: £10.7bn). Adj. PBT down 5% to £5.4m. Interim dividend maintained at 3p. Cash £31.2m. Outlook: “...well positioned to secure positive net inflows including from the newer markets we are targeting.” | AMBER/GREEN (Mark) | |

Watkin Jones (LON:WJG) (£91.8m) | SP down 9% Rev. down 26% to £129.2m. Op profit down 90% to £0.4m. Net cash ex-IFRS 16 £73.4m (HY24: £44.0m). Outlook: pipeline targeted in H2 25 to enable delivery of full year performance in line with current market expectations. | AMBER/GREEN (Graham) Sticking with a moderately positive stance which is a little speculative. However, this is a Super Stock with a strong balance sheet (assuming that building safety provisions don't grow much bigger from current levels) and modest profitability, and I still think it has the potential for a strong recovery as the macro environment changes. | |

Braemar (LON:BMS) (£84m) | Rev -7% to £141.9m, u/l EPS down 15% to 31.3p. Net debt of £2.5m at year end now net cash after working capital timing. Outlook: order book flat, FY26 u/l op profit now expected to be in the range of £13-14m, below expectations. Dividend cut from 13p to 7p, difference used for £2m buyback in the short term. |

BLACK (AMBER/RED) (Mark) | |

Zephyr Energy (LON:ZPHR) (£80.9m) | Estimated total range of 0.827 to 1.24 million barrels of oil equivalent ("boe") for the State 36-2R well. Williston project: Q1 production averaged 756 boepd, net to Zephy, down on Q4 due to temporary downtime. Assessing US$30m of sourced drilling opportunities funded through the new US$100 million strategic partnership. | ||

Churchill China (LON:CHH) (£69.8m) | “Hospitality markets remain under pressure…strongly placed for recovery with appropriate stock levels…continue to win new installation business across all our markets, albeit at lower volumes, and see strong replacement orders at good margins.” | AMBER/GREEN (Mark) [no section below] | |

Journeo (LON:JNEO) (£49m) | £4.2m PO from Alstom to enhance safety, security & operational efficiency on CrossCountry's Voyager fleets. Commenced design & initial equipment supply. Majority of revenue in FY26 & FY27. Additional £0.4m SaaS revenue per year for 5 years. | GREEN (Mark) [no section below] | |

Asiamet Resources (LON:ARS) (£25.3m) | 2024 Annual Report & $2.5m Placing | Updated project mining feasibility plan. $5.5m net loss, similar to previous year. $2.3m cash, bolstered by $2.5m placing to connected parties announced today. |

Graham's Section

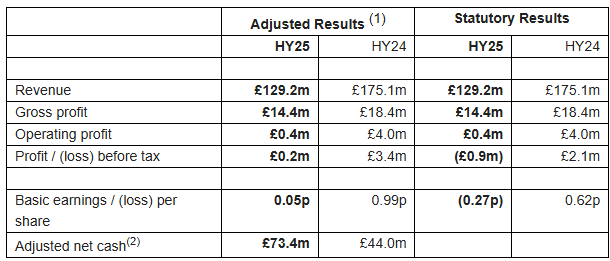

Watkin Jones (LON:WJG)

Down 9% to 32.7p (£84m) - Half-Year Results - Graham - AMBER/GREEN

These are interim results to March 2025, which the company says are in line.

The major exceptional item is £1.1m relating to the building safety provision. Apart from that, the results are pretty clean, although of course a breakeven result is hardly going to be all that satisfactory for investors.

They describe the profit result as follows:

Operating profit of £0.4m (HY24: £4.0 million) achieved as a result of strong construction delivery, with gross margins in line with previous guidance against a backdrop of continuing limited transactional liquidity in the market

As I noted in January, the business model of forward funding for build-to-rent construction has been badly affected by higher rates, and this situation has still not improved.

However, the Watkin Jones share price has not been doing so badly this year. It was 24p when I covered it in January, and was near current levels when I looked at its in-line trading update earlier this month.

That will of course be cold comfort to long-term investors here:

Turning back to today’s interim results, I note that the net cash balance has improved to £73.4m, covering the vast majority of the market cap.

However, this cash balance is stated before the building safety provision, which now stands at £45m (including the value of promised client contributions towards remedial works, called “reimbursement assets”).

After taking the building safety provision into account, perhaps a more realistic net cash figure would be £28m.

Outlook:

Whilst the external market backdrop remains challenging, we continue to focus on the factors within our control…

The “total secured pipeline” of £1.1bn sounds promising but that figure is not yet contractually secured and I presume subject to the difficult problem of how to finance it.

CEO comment (emphasis added):

"We continue to actively market and engage with investors on our development opportunities which are attracting interest, supported by the attractive fundamentals of the PBSA and BTR sectors in which we operate. Whilst transactional activity remains slow and subject to a continuing volatile market backdrop, we are focussed on ensuring that the Group remains in the best position to exploit opportunities as conditions improve."

Balance sheet: low borrowings and tangible equity of £122m.

Estimates: Progressive had declined to issue 2025 forecasts, until today. It has now at last published forecasts for FY Sep 2025, and these are:

Revenue -12% to £317m

Adj. PBT £5.3m (FY 2024: £9.2m)

No dividend.

Graham’s view

These results have been met with a poor reception by the market.

The economic backdrop is clearly not helping yet, with deals not being funded as they were before, and the company only able to promise that it will return to strength when conditions allow.

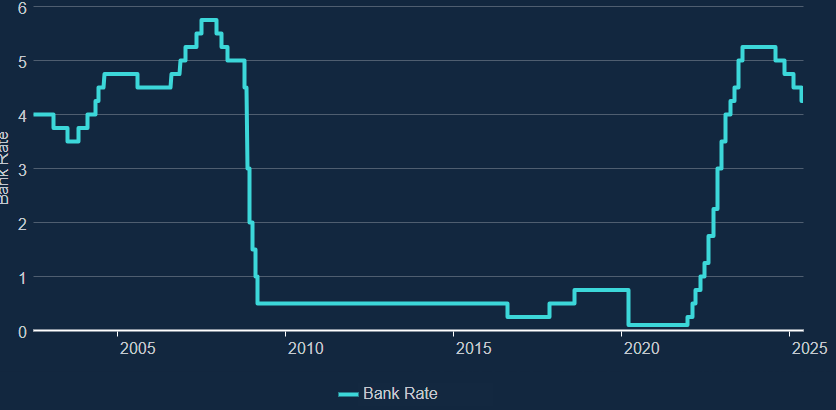

A reminder of the interest rate path we’ve been on:

On top of that, the forecasts from Progressive, while affirming the company’s promise that the current H2 period will be much stronger than H1, don’t yet give any indication as to performance in FY 2026 (the financial year that starts in just over four months!).

So there is still an enormous amount of uncertainty, and in the meanwhile the company is not yet performing as it did historically. Any recovery could be years away.

And yet despite this, I’m still inclined to think that my AMBER/GREEN stance is justified.

Firstly, in StockRank terms, this is a Super Stock:

Secondly, I have no balance sheet concerns, aside from the risk of future building safety provisions (admittedly I’m not sure how to judge the seriousness of this risk). But as things stand, the company has plenty of available cash to fund remedial works, has headroom on its facilities, and tangible equity in excess of its market cap.

Thirdly, the company remains modestly profitable. I concede that for H1, we are required to ignore the impact of safety provisions in order to create a small adjusted profit. But for the year as a whole, I hope to see a small unadjusted profit.

In a circumstance where revenues have fallen by more than a quarter over five years, with the interest rate environment having completely changed, I think that’s noteworthy.

Looking ahead, interest rates seem likely to continue falling, even if they do so gradually.

Overall, therefore, I think a moderately positive stance continues to make good sense here. If conditions don’t improve then hopefully the company’s tangible backing will help to support the valuation. But if conditions do improve, then perhaps in a couple of years this turnaround could get quite exciting. It's a little speculative, but I like the risk:reward.

Harbourvest Global Private Equity (LON:HVPE)

Up 1% to £24.50 (£1.8bn) - Annual Financial Report - Graham - GREEN

I’ve taken an interest in investment trusts recently - or more specifically, private equity investment trusts. As a result, I’ve invested in Pantheon International (LON:PIN) and I’m also considering an investment in Harbourvest Global Private Equity (LON:HVPE), the FTSE-250 trust managed by HarbourVest Partners

My reasons for having an interest in the sector are:

Easy diversification away from the S&P 500 where I have some concerns around the lack of diversification and possible overvaluation.

The focus on capital gains rather than dividends suits my mindset and tax situation.

Trusts in general are trading at interesting discounts to NAV.

My most successful investments personally have been in two private equity vehicles (Volvere (LON:VLE) and Berkshire Hathaway (NYQ:BRK.B) ).

HarbourVest Global Private Equity has popped up on my radar as I noticed it was well-diversified along with having various other features I’m looking for in private equity trusts.

Today’s results for FY January 2025 show that the trust generated a return of 7.3% for the year, in dollar terms.

The share price rose 19%, which narrowed its discount to NAV from 42% to 35%.

But let’s calculate an up-to-date figure for this.

NAV for 30th April has been estimated at $55.54. At the latest cable exchange rate, that’s £41.20.

Based on today’s £24.50 share price, the trust is now trading at a 40.5% discount. So most of the narrowing that was achieved during FY January 2025 has currently been reversed.

The trust is actively buying back its own shares at this level; $106m was spent on this in FY25.

Outlook

The Chair strikes an optimistic tone for the outlook:

We remain optimistic as we navigate 2025. Greater clarity and a more measured tone around global trade policy could support a gradual return to stability in the coming months, supporting the much-needed recovery in the IPO and M&A markets, and we would expect this to be accompanied by a stronger alignment of buyer and seller expectations - a key catalyst for unlocking value in the sector. Your Investment Manager also shares this positive outlook and is encouraged by potential IPOs in the venture space, which bodes well for HVPE given its exposure to this segment.

Note that a recovery in the IPO market wouldn’t just benefit the likes of Cavendish (LON:CAV) and other banks/brokers. These private equity trusts would be major beneficiaries as it would give them an avenue through which to sell their holdings at attractive levels.

Later, on the subject of recent market turbulence relating to tariffs, which has caused some corporate transactions to be postponed, he says:

While the effect on HVPE may be a lower overall quantum of distributions from our investments in 2025 than originally anticipated before the tariffs shock, we remain confident that HVPE's high quality, diversified global portfolio ensures it is very well placed to capitalise on the many exciting opportunities that the improving conditions in private markets will present.

Graham’s view

I’m AMBER/GREEN on trusts in general but I’m GREEN on Pantheon International (LON:PIN) (in which I have a long position) and I’m also strongly considering an investment in HVPE, so I think it’s only right that I’m GREEN on this one, too.

I just don’t see what the “catch” is - to my eyes this is a reputable, well-diversified investment trust with historical performance of c. 10% annually, currently trading at a very large discount to NAV. What’s not to like?

There will be a continuation vote in July 2026, so if shareholders decide to shut it down and try to get their money back, they’ll have the opportunity to do so. But personally I know I’d want to vote for its continuation!

Mark's Section

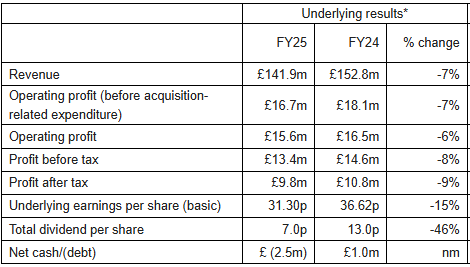

Braemar (LON:BMS)

Down 6% to 240p - Final Results & Share Buyback - Mark - BLACK/AMBER/RED

When Roland last reviewed Braemar, it was following the profits warning in their FY25 Trading Update. This was what they said at the time:

FY25 revenue guidance: “in the region of £141m” (previous consensus £152m)

FY25 underlying operating profit: c.£16.5m (previously £17.5m)

Here’s the actual results:

That’s a slight improvement on what they were guiding, with the updated numbers from Edison in March showing £141.1m in revenue and £15.4m in underlying operating profit. (It seems Edison don’t agree that acquisition-related expenditure should be excluded. Something I agree with, given the repeated acquisitions and that this is a people business where acquisitions often involve golden hellos paid to attract teams of brokers to join.)

In response to the previous profits warning, Edison took 7.5% out of their FY25 revenue and operating profit numbers, but an even more severe 10% out of their FY26 estimates. It seems that that wasn’t aggressive enough, as today the company says they will miss those figures:

Underlying operating profit (before acquisition-related items) for FY26 is now expected to be in the range of £13 million to £14 million.

This mid-point of that is 9% below Edison’s previous £14.8m forecast, but it's probably worse than that as the company choose to exclude the acquisition-related items that tend to run in the £1-1.5m per annum range.

There isn’t an updated Edison note yet, but Canaccord have updated their figures and have reduced their adjusted operating profit figure to £13.5m from £15.8m. It appears that they are willing to overlook the acquisition costs in their figures. Their EPS estimate for 2026 is cut by 19% to 23.1p. However, they upgrade their 2028 estimates. Given the company doesn’t seem to be able to forecast the current year particularly accurately, I’d certainly take this with a pinch of salt!

The reasons given for the weakness make sense and are largely out of the company’s control:

Tanker rates are recovering from the lows in H2 although macro conditions remain weaker at the start to the year given increased geopolitical uncertainty and a weaker USD.

This is undoubtedly a cyclical business, but one where they never seem to deliver blow-out numbers in the good years:

I suspect the reason is that, as a people business, they have to pay bonuses to staff in good years, which reduces the returns to shareholders. Speaking of returns. Many investors were attracted to this company for the large and growing dividend payout:

However, this is also a victim of these results, being cut from a forecast of 14p to 7p. This is now only a 3.2% yield, so it won’t be making a home in income investors ’ portfolios anymore. This is the narrative around the cut:

Total dividends have grown by 160% from 5.0 pence per share in FY21 to 13.0 pence per share in FY24. Despite this, our share price has remained broadly unchanged. In short, our progressive dividend policy, despite the yield being increasingly attractive, has not generated increased equity value to shareholders.

Moaning that the dividend payout was not reflected in the share price sounds a bit like me complaining that my car keeps crashing, without reference to the actions of the driver. The difference is going to be made up by share buybacks in the short term:

…the Company will continue to pay a dividend in line with our updated Capital Allocation Framework, it will reduce the dividend to a level that the board believes remains attractive and will use surplus capital to purchase (and then cancel) its own Company shares. For this year, cash saved from a reduced dividend will support a share buyback programme of up to £2 million.

On 28th February, the company had £2.5m of net debt, but this has since moved to a net cash position due to the timing of working capital. With an RCF of £30m, it would seem that they could easily have afforded to pay the dividend, which was covered by even the reduced earnings. The cynic in me wonders if the capital freed is destined for further acquisitions, with costs they conveniently adjust out of their numbers, and paying bonuses!

Mark’s view

This further profits warning and the big dividend cut reinforce Roland’s AMBER/RED view of this cyclical people business, especially as the share price is at similar levels to before two large downgrades in EPS. All three of the QVM Ranks are likely to see big falls when these results are digested by the algorithms.

Serabi Gold (LON:SRB)

Down 1% to 151p - 3m Interim Results to 31 March - Mark - AMBER/GREEN

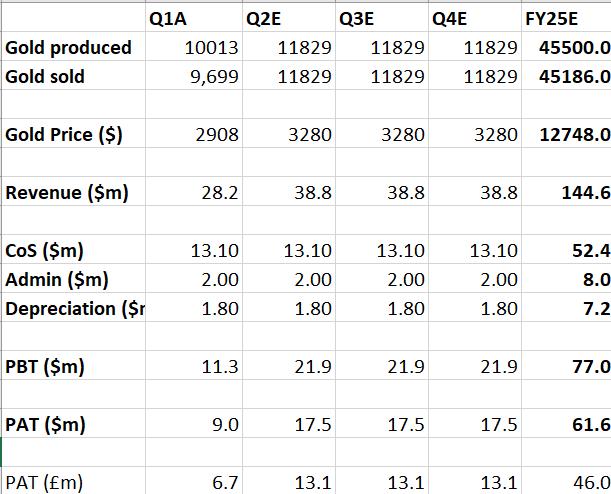

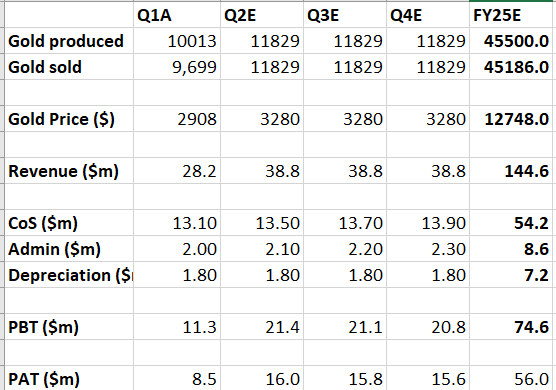

These are the Q1 results. Gold production is up 11.2% to 10,013oz but this was known following the Q1 production report. However, it is worth noting that this is below the run-rate required to reach the 44-47koz FY25 production guidance. The mid-point of that range would be 11,375oz/quarter. There’s not a lot of detail around how production should evolve over the next three quarters. All they say is that the production increase is driven by grade:

The Group delivered a strong start to 2025 with an 11% increase in production year-on-year, driven by significant grade improvements at both Palito (+32%) and Coringa (+8%).

However, we have previously had a Q1 Operational update that gave production details. At this stage, I think we can assume that they are on target for their production guidance. The financial side looks phenomenal with higher production leading to lower AISC:

All-In Sustaining Cost for the three-month period to March 2025 of $1,636 per ounce (Q1-2024: $1,859 per ounce).

This is despite a strengthening Real impacting margins. But the real driver of the more than doubling of EPS is the gold price:

Whilst the Company benefited from an improving gold price throughout the first quarter of 2025, the most material uplift occurred only in March, with the USD gold price rising to $2,996 and averaging $2,908 for the quarter, compared to a current spot price of approximately $3,300 per ounce. This contributed to a Q1 average gold price in Brazilian Real of BRL17,018. In Q1-2025, the average USD gold price increased by 18% in comparison to Q1-2024 ($2,908 in Q1-2025 vs $2,469 in Q1-2024).

The company had a roughly 20% tax rate for the quarter, so if this, plus costs stay similar, there is scope to beat the current forecasts. This is my simple maths:

Versus the StockReport numbers:

There is scope for some cost inflation and higher tax, and they will still beat expectations if the gold price remains around today’s price:

One of the big concerns I’ve had here in the past is that, like most gold miners, Serabi were going to put all the profits back into expanding production, until the gold price collapsed again in a few years. However, in their Q1 production report, they said:

In light of the excellent operational performance, strong prevailing gold price, cash position and anticipated cash growth ahead, the Company is currently assessing appropriate mechanisms to return capital to shareholders.

There’s no update on this today, but we wouldn’t necessarily expect this with Q1 results. Brokers now have a 13c FY25 dividend now forecast, although this declines in 2026 forecasts, suggesting that this may be paid as a special dividend.

Risks

The production uplift required in the remaining quarters of FY25 suggests there is work to do to hit production forecasts for the full year.

Most of the phenomenal results so far have been driven by the gold price. While the company have done well to keep costs flat in an inflationary environment, they have largely been passengers in these strong results. This means that they will remain passengers if the gold price falls significantly in the future.

When companies produce windfall profits as a result of commodity rises, there is always the risk of governments wanting a bigger slice of the windfall via increased taxation or other means.

Mark’s view

Despite the risks mentioned above, the valuation here remains compelling on a forward P/E likely somewhere between 2 and 3. It appears to me that there is scope for the company to still beat the current forecasts even with a minor production miss or higher cost inflation, as long as the gold price remains strong. The gold price can be hedged relatively cheaply by those who view this as a significant risk. With the company now flagging shareholder returns, the risk that management will waste the windfall profits reduces. Production increases in FY26 could further enhance returns. I see no reason to change the AMBER/GREEN view following today’s Q1 results.

Premier Miton (LON:PMI)

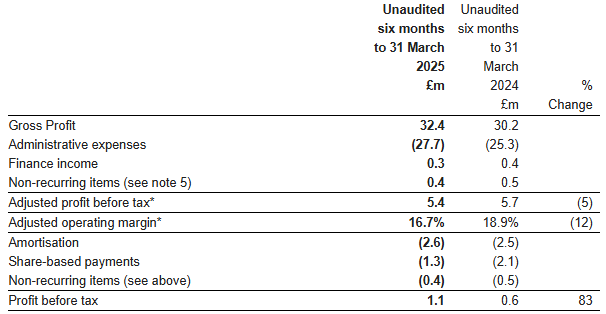

Down 1% to 63.6p - Half Year Results - Mark - AMBER/GREEN

The AUM of £10.2bn was known from the Q2 AUM update on 16th April. However, they provide a small update today with £10.4 billion closing AuM at 22 May 2025 meaning that they have started to recover. This is partly driven by performance where they say:

Whilst we do not generally place too much emphasis on short term performance numbers, it is pleasing to note that our managers have coped well during recent market volatility with 71% of our funds performing ahead of median to 30 April 2025, and approximately half in the first quartile.

Their gross profit is up due to their ability to charge performance fees on some funds:

Costs are also up, and it is worth noting that their non-recurring costs appear to recur, and there is a large share-based payment charge:

Like many asset managers, they are cutting costs to improve future profitability. Although the focus here appears to be on infrastructure, not just staff costs:

Operationally, we have completed the infrastructure review initiated in December 2024 and identified efficiencies expected to reduce our annual run-rate costs by approximately £3 million, or 6%. Importantly, these adjustments will not impact our ability to pursue growth opportunities or maintain service quality.

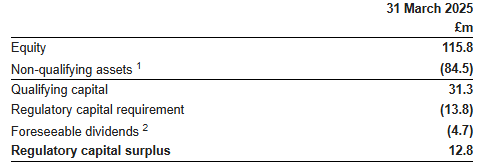

There is £31.2m of net cash on the balance sheet, although it is worth noting that a fair amount of that is taken up by regulatory capital:

Still, unlike Impax, they have managed to maintain their 3p per share dividend, which surely signals they aim to keep the 6p full-year dividend for a yield of around 9%. Their policy is:

The Group's dividend policy is unchanged and remains to target an annual ordinary dividend pay-out of approximately 50 to 65% of profit after tax, adjusted for non-recurring items, share-based payments and amortisation.

6p dividend would be uncovered by the 5.69p FY25 forecast EPS, so this does require a recovery in the medium term to be maintained. Cash flow didn’t cover the payment of the final dividend in H1, but this is partly due to the acquisition of Tellworth and timing on tax payments. Volatile global markets have taken their toll on the forecasts:

The 2.55p diluted adjusted earnings per share for the half year suggest that they need a better second half to hit these reduced forecasts. However, these results, along with the small rise in AUM, suggest they are on track.

Mark’s view

Given the 50% rise in share price off the April lows, and with the EPS consensus having fallen slightly since we last reviewed it on the DSMR, I think the short-term investment case is a little weaker. However, like almost all asset managers, there is scope to do much better in better market conditions. Premier Miton are helped in this endeavour by outperforming peers both in terms of AUM and fund performance. That they have started to charge performance fees again bodes well for the medium-term recovery. I think there is enough here to maintain the AMBER/GREEN view, although, personally, I have sold my small position into the recent rise as the recovery seemed a little too fast.

See what our investor community has to say

Enjoying the free article? Unlock access to all subscriber comments and dive deeper into discussions from our experienced community of private investors. Don't miss out on valuable insights. Start your free trial today!

Start your free trialWe require a payment card to verify your account, but you can cancel anytime with a single click and won’t be charged.