Good morning!

There was some drama at the Federal Reserve yesterday, as outgoing chair Jay Powell indicated that he will be staying on as a member of the Board of Governors, for an indefinite period of time.

Powell has the right to stay until 2028, but was expected to stand down promptly as most outgoing chairs do.

His reason for staying? "Legal attacks on the Fed, which threaten our ability to conduct monetary policy without considering political factors."

The economic significance of the decision is that it delays President Trump's ability to appoint someone else to the Board with a greater propensity to cut rates. And so Powell continues to be a source of real frustration for the 47th president of the United States.

The Bank of England should provide a more tranquil source of monetary news today, with rates expected to be kept unchanged at midday, at 3.75%.

In overnight moves:

- The FTSE is expected to open lower again this morning, below 10,200

- With no progress towards a resolution of the conflict in the Middle East, Brent Crude has broken out to new highs at $114.

Companies Reporting

| Name (Mkt Cap) | RNS | Summary | Our view (Author) |

|---|---|---|---|

Rolls-Royce Holdings (LON:RR.) (£92.2bn | SR72) | “Further confidence in our guidance of £4.0bn-£4.2bn of underlying operating profit and £3.6bn-£3.8bn of free cash flow for 2026. We remain strongly positioned to deliver our mid-term targets…” | ||

Unilever (LON:ULVR) (£92.1bn | SR58) | Q1 underlying sales growth 3.8%. Full year outlook reconfirmed. Underlying sales growth to be at the bottom end of multi-year guidance range of 4% to 6%. | ||

Glencore (LON:GLEN) (£64.9bn | SR79) | Expecting input cost impacts (diesel/acid) to be more than offset by stronger commodity prices (copper/zinc/coal), to result in margin expansion. “...extrapolating our Q1 Marketing performance, would see this segment's full-year EBIT performance comfortably exceeding the top end of our long-term Adjusted EBIT guidance range of $2.3-3.5bn p.a.". | ||

Standard Chartered (LON:STAN) (£39.7bn | SR72) | Operating income $5.9bn, up 9%. ROTE 17.4%, up 260 basis points. 2026 guidance remains unchanged. | ||

United Utilities (LON:UU.). (£8.95bn | SR50) | Targeting regulatory returns of 10-11% in AMP8. Equity issue to raise £800m. | ||

Weir (LON:WEIR) (£7.18bn | SR47) | FY outlook: 2026 guidance reiterated. CEO stepping down after 10 years. New CEO has been hired internally. | ||

DCC (LON:DCC) (£5.02bn | SR95) | 5800p offer “fundamentally undervalues the Company and its future prospects”. | GREEN = (Mark) That PE firms have come sniffing backs up our previously positive view of this company. I’m not sure how the bidders thought that a 12% premium was ever going to be recommended by the board. There’s alway the chance they come back with something more punchy, but the gap looks insurmountable to me. However, the long-term attractions of the business remain. | |

Whitbread (LON:WTB) (£4bn | SR23) | Outcome of Business Review & Preliminary Results Announcement | Revenue +0%. Adjusted PBT +0% (£483m). Forward booked position is ahead of last year. “Our model is the right one”. New five-year plan. £275m of incremental adjusted PBT targeted from growth initiatives. ROCE to increase by 500 basis points. | |

Seplat Energy (LON:SEPL) (£3.43bn | SR93) | 2026 guidance reiterated. Production guidance of 135-155 kboepd. | ||

Persimmon (LON:PSN) (£3.3bn | SR80) | Trading in line. Early signs of increased inflation in the supply chain. “Assuming market conditions do not materially deteriorate, we anticipate delivering profit before tax in line with consensus.” | ||

Drax (LON:DRX) (£2.91bn | SR98) | Full year 2026 expectations for Adj. EBITDA in line with consensus estimates. | ||

Inchcape (LON:INCH) (£2.89bn | SR87) | Performance in-line with management expectations, FY 2026 guidance reiterated. | ||

Osb (LON:OSB) (£1.77bn | SR77) | “The Group delivered a resilient financial performance in the first quarter of 2026 and we continue to operate broadly in line with our 2026 guidance.” | ||

Hammerson (LON:HMSO) (£1.73bn | SR62) | CFO retires after 5 years. Will remain employed by the company for the next 12 months. Current Deputy CFO to become Interim CFO. | ||

Lancashire Holdings (LON:LRE) (£1.39bn | SR71) | Gross written premiums down 6.1%. “Excluding the impact of reinstatement premiums related to the California wildfires, the underlying reduction in gross premiums written was just 1.2%.” “..we maintain our expectation of a stable top-line, and a high teens RoE for 2026.” | ||

Sigmaroc (LON:SRC) (£1.39bn | SR92) | Q1 profitability ahead of 2025, and in line with expectations. Outlook for 2026 unchanged. | ||

Ceres Power Holdings (LON:CWR) (£1.21bn | SR25) | Infrastructure partnership signed between Delta Electronics and Centrica to serve the data centre market and energy intensive industries, launching with Solid Oxide Fuel Cells for off-grid energy generation. Delta is one of Ceres' manufacturing licensees. | ||

Metro Bank Holdings (LON:MTRO) (£933m | SR70) | Continued growth in underlying and statutory profit, reaffirming all guidance. | ||

MONY (LON:MONY) (£917m | SR83) | Management expectations for the full year remain unchanged. | GREEN ↑ (Graham) | |

Renew Holdings (LON:RNWH) (£704m | SR88) | £13m acquisition (£10m upfront, £3m defcon). Edwards Diving Services is a provider of specialist marine and civil engineering services to the water industry. | ||

International Personal Finance (LON:IPF) (£545m | SR88) | Aiming to complete acquisition by BasePoint by the end of Q2 2026. | PINK | |

Alfa Financial Software Holdings (LON:ALFA) (£457m | SR39) | Revenue up 3%. Trading in line with expectations. | ||

NCC (LON:NCC) (£335m | SR55) | Revenue up 5% on a constant current basis. FY26 Group Adjusted EBITDA is expected to be in line with the Board's expectations. | ||

Caledonia Mining (LON:CMCL) (£324m | SR85) | As part of the succession plan, the Chairman has notified the Board of his intention to step down. A current independent NED has offered to become the new Chairman. | ||

Property Franchise (LON:TPFG) (£321m | SR86) | Buys 25% interest in Meridian, the parent of Legal & General Surveying Services Limited, for £2.5m. | ||

Franchise Brands (LON:FRAN) (£266m | SR64) | System sales +4%. “...well positioned for a full-year performance within the current range of analysts' forecasts”. | ||

Eco (Atlantic) Oil & Gas (LON:ECO) (£221m | SR32) | “The JHI acquisition is progressing well with this important milestone of the interim court order. The next step, expected within two weeks, is to receive JHI's final shareholders' approval…” | ||

ASA International (LON:ASAI) (£215m | SR75) | The momentum seen in 2025 has continued into 2026. Portfolio 25% ahead year-on-year. Winding down operations in India ahead of full deconsolidation. | GREEN = (Graham - I hold) No reason to change my positive stance here. The portfolio has shrunk since December but this appears to be normal seasonality. Loan quality as measured by Portfolio at Risk remains within a normal range. With a P/E multiple of only 4x and strong year-on-year growth, I'm excited about the prospects here. | |

Vertu Motors (LON:VTU) (£201m | SR93) | Cyber attack insurance claim agreed at £3.9 million. £0.5 million deductible applies, resulting in net recovery of £3.4 million. This means an additional £2.4m to be received (£1m already paid). As a result, FY26 adjusted profit before tax to be ahead of the current market consensus. | ||

Evoke (LON:EVOK) (£185m | SR67) | Revenue +2%. Adjusted EBITDA +14%. Adjusted profit after tax £5.7m. Reported loss £549m. Q1 revenue in line. Discussions with Bally's Intralot S.A. remain ongoing re: possible offer at 50p per share. No forward looking financial guidance provided due to ongoing strategic review. | PINK (Graham holds) | |

Kore Potash (LON:KP2) (£184m | SR18) | Kola Project has seen continued progress in the quarter. Formal Sale Process: a potential buyer remains engaged and continues its due diligence. | PINK | |

KEFI Gold and Copper (LON:KEFI) (£176m | SR25) | GMCO’s Jibal Qutman Gold Project has been finalising its Definitive Feasibility Study. DFS currently under third party review. Kefi has assigned nil book value to its 13% interest in GMCO, but this “does not diminish the significance of the Company's involvement in the project.” Historically, KEFI has invested $13m into GMCO. | ||

GreenX Metals (LON:GRX) (£136m | SR10) | Tannenberg Copper Project (Geramany): GreenX is progressing with an integrated program to support future JORC Code reporting. Eleonore North Project (Greenland): Outcropping gold and high-grade antimony mineralisation now confirmed at the Noa Prospect within the project. Poland: preparing for enforcement activities of the Energy Charter Treaty Award. | ||

Atlantic Lithium (LON:ALL) (£130m | SR27) | Ratification of the Mining Lease in respect of the Company's flagship Ewoyaa Lithium Project. Advanced discussions relating to Project funding and continue its progress towards a Project Final Investment Decision. Cash A$13.9m. | ||

SIG (LON:SHI) (£91m | SR54) | LFL revenue -5%. “Pricing pressure remains elevated, and year over year pricing was flat in the quarter, despite modest inflation on input costs as expected.” Outlook: Trading starting to improve in March with LFL decline 2-3%, continues to anticipate softness in FY26, and increasing H2 weighting. | ||

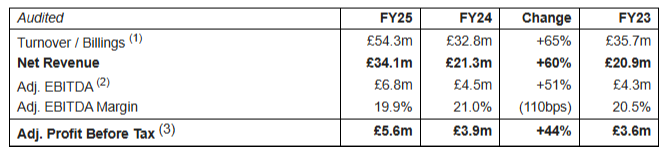

Brave Bison (LON:BBSN) (£82.5m | SR38) | Net revenue +60% to £34.1m, Adj. PBT +44% to £5.6m, EPS +15% to 6.9p. Net Cash £4.3m (FY24: £7.5m) all ahead of recently upgraded consensus expectations. Outlook: expects net revenue and Adj. EBITDA to exceed current consensus expectations for FY26 | AMBER/GREEN = (Mark) As with many marketing companies, things look less rosy once you look below the veneer of the headlines. With no organic growth figures given, and the number of acquisitions it is very hard to work out the underlying performance. Operating cash flow figures suggest this is not as cheap as the headlines. However, there is certainly trading momentum behind the company with a 15% upgrade to adj. EPS just four months into the year, suggesting that there could well be more upgrades to come. Balancing these factors, I am happy to keep our moderately positive view. | |

Synthomer (LON:SYNT) (£82.1m | SR40) | Revenue -9.9% to £1.74bn, Adj. EBITDA - 4.6% to £136.5m, U/L EBIT -22% to £37.6m. Net Debt £575m (FY24: £597m). Outlook: Significantly improved CCS and stable AS performances offsetting a slower start for HPPM in Q1 2026. Expect robust period-on-period volume and margin progress in Q2 2026 . CFO intention to step down. Iain Torrens will take up the role of CFO from 15 May 2026 on an interim basis. | ||

First Tin (LON:1SN) (£70.4m | SR43) | Measured Resources increased by 7,000t tin (15.8%) to 39.2Mt @ 0.13% Sn (51,200t tin). Indicated Resources increased by 4,400t tin (10.5%) to 46.5Mt @ 0.10% Sn (46,400t tin) | ||

Aura Energy (LON:AURA) (£66.8m | SR7) | Aura's technical team confirmed two successful methodologies for dewatering of production from the Tiris Project. | ||

Iofina (LON:IOF) (£62.4m | SR84) | Revenue +22% to $66.5m, Adj. EBITDA +56% to $11.8m, PBT +75% to $8.4m. Net Cash $5.2m (FY24: $2.9m). Anticipates H1 2026 crystalline iodine production to be in the region of 385MT, previously upgraded from 325MT-355MT. | ||

IG Design (LON:IGR) (£55.1m | SR66) | SP +27% FY2026 results are expected to be ahead of market consensus with revenue of $$292m and adj. Op Profit of $12.8m. Cash significantly exceeded expectations with year-end net cash of c$72 million. Glenart S.A., a South African manufacturer within the Group's "Celebrate" category, acquired for £5.3m (£3.4m up front). Glenart FY26 revenue £4m, EBITDA £1m. | AMBER/GREEN = (Mark) The rise this morning largely reflects the increase in broker forecasts, meaning this trades on roughly the same multiple as before. However, this doesn’t make them particularly cheap on earnings. There is a material net cash beat, though, and the big question for valuation is how much of that cash is genuinely surplus to requirements, given the huge working capital swings during the year. Today’s bolt-on acquisition suggests they are more confident of their financial position than they have been in the recent past. In terms of pure valuation, so much depends on excess cash, something I have no idea, so I am neutral on valuation. However, given that this is now the second upgrade in a row I think we should remain relatively generous in our view. | |

Ariana Resources (LON:AAU) (£50.5m | SR44) | 31-hole reverse-circulation drilling programme completed for 5,659m, targeting resource expansion at the Dokwe Gold Project. Incl. 4m at 16.9g/t from 69m. 4,533 ounces of gold and 10,305 ounces of silver were produced from the Zenit Mining Operations in Türkiye. | ||

Blencowe Resources (LON:BRES) (£39.6m | SR12) | Batch completes the remaining shallow results ahead of a maiden Beehive JORC Resource and a wider Orom-Cross JORC Resource upgrade. Includes 22.2m at 7.73% total graphitic carbon. | ||

Zenith Energy (LON:ZEN) (£37.9m | SR42) | Progressing the spin-out of its Italian uranium exploration business into Reveille Resources on Acquis. Zenith and Ajax have each agreed to invest an initial £200,000 in Reveille, each securing a 25% interest in the issued share capital. | ||

Ferro-Alloy Resources (LON:FAR) (£34.4m | SR10) | Revenue -4% to $4.53m, Net Loss $8.42m (FY24: $9.43m). Cash 31 Mar: $2.16m following placing. | ||

Predator Oil & Gas Holdings (LON:PRD) (£33.2m | SR18) | Revenue £0.94m, Operating Loss £2.99m (FY24: £2.06m Loss). Cash £1.52m (FY24: £3.81m). | ||

Amigo Resources (LON:AMGO) (£32.7m | SR81) | Successfully completed a phased exploration programme across the Project area. Multi-element geochemical analysis has identified anomalous gold responses across the Project area. | ||

Novacyt SA (LON:NCYT) (£22.6m | SR39) | Revenue +2% to £20.0m slightly ahead of expectations. U/L revenue +4%. LBITDA £7.8m. exceeding market expectations. Cash £19.1m (FY24: £30.5m). | ||

Harena Rare Earths (LON:HREE) (£20.5m | SR14) | Interim CFO, Jack Allardyce becomes Chief Financial Officer with immediate effect. | ||

Chesterfield Special Cylinders Holdings (LON:CSC) (£20.1m | SR75) | H1 trading broadly in line with management expectations at £6.4m revenue and LBITDA £0.8m. Delays mean that FY revenue & EBITDA in line with last year at £16.6m & £0.8m, respectively, slightly behind expectations. | BLACK (AMBER/RED =) (Mark) This profits warning, while relatively minor, reinforces why I remain mostly negative. There is little asset backing and the investment case relies on believing long-term future forecasts for a company that keeps missing in the near-term. | |

Eenergy (LON:EAAS) (£19.2m | SR37) |

Revenue -16% to £19m after accounting change. Adj. EBITDA £2.2m (FY24: LBITDA £0.7m), Cash £0.9m (2024: £2.3m), Net Debt incl. Leases £1.3m (FY24: £2.9m). | ||

Celsius Resources (LON:CLA) (£15.4m | SR17) | Completed A$9.3m equity raising, delivery of DFS, strategic planning around underground mine development. | ||

Prospex Energy (LON:PXEN) (£14.1m | SR19) | Quarterly Net production +4% to 2,686.9kscm, Quarterly net revenue +36% to €1.155m. | ||

Kelso group (LON:KLSO) (£13.7m | SR37) | NAV declined 4% to 2.3p/share from 2.4p. 2026: NAV +13% to 2.6p. | ||

Cizzle Biotechnology Holdings (LON:CIZ) (£10.9m | SR14) | Operating Loss £753k (FY24: £2.166m loss). “The outlook for 2026 is encouraging.” |

Graham's Section

MONY (LON:MONY)

Unch. at 176.45p (£919m) - AGM Statement - Graham - GREEN ↑

This is the owner of MoneySuperMarket and various other brands including Quidco..

We’ve been broadly positive on it (e.g. Roland in February).

Growth has been very modest (2%) and there are concerns about AI disruption, but this is arguably reflected in a cheap rating:

Turning to today’s statement: the main takeaway is that full year guidance is unchanged:

MONY Group has delivered good growth in revenue[1], supported by the strength in breadth of the Group's established portfolio of products and brands.

Checking footnote [1], I find:

Revenue is presented on a like-for-like basis, excluding Ice Travel Group (ITG) Travel revenue following the Group's move to a minority position as of 1 December 2025. On a statutory basis, including 2025 ITG revenue for the same period the position is flat.

In other words: like-for-like revenue is growing. But total revenue isn’t growing, due to the change in the position at Ice Travel Group (ITG).

Background on ITG:

ITG owns icelolly.com and travelsupermarket.com.

MONY was the majority shareholder of ITG until it sold a chunk of its stake back to ITG, at a loss, becoming a 49.9% shareholder instead. This means that ITG’s revenues are removed from MONY’s income statement (but its P&L shows up elsewhere).

MONY Trading Year-to-date

Most divisions are doing boringly fine:

Insure “performed well”

Money “delivered solid performance”

Home Services is “encouraging”

The difficult piece is Quidco: “Cashback performance remains impacted by economic uncertainty affecting UK corporate marketing budgets and consumers.”

Strategy: they continue to attempt to convert users from occasional visitors into long-term members.

Following the launch of SuperSaveClub (SSC) in late 2023, we have grown membership consistently and sustainably, and are pleased to report that SSC has now reached almost 2.4 million members. This loyal, engaged member base has a higher customer lifetime value.

SSC was reported to have 2.1 million members at the full-year results, so I would say that is very decent growth in four months.

MoneySuperMarket now has a ChatGPT app: a new route-to-market. So is AI a threat or an opportunity? It “lets people compare car insurance, broadband and banking deals through simple, conversational questions instead of forms.”

Buyback: £25m buyback is ongoing.

Outlook: in line with consensus, with an H2 weighting “as previously indicated”.

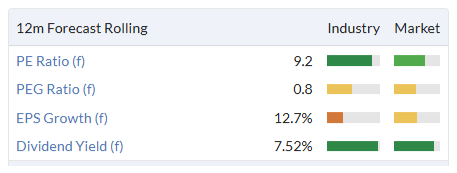

Market expectations are for EBITDA of £145.2m, with a range of £140.0m to £148.3m. The StockReport shows an EPS forecast of 18.6p.

Graham’s view

I used to be a shareholder of Gocompare (now owned by Future). I mention that just to provide context that I do really like this sector. MONY is the type of stock I’d like to own.

It’s a Contrarian-style stock, which is basically my favourite type of stock: high quality, and potentially offering value, but unloved at the moment:

The 3-year chart tells a story:

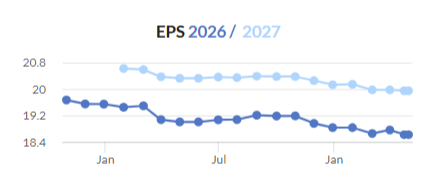

And I acknowledge that earnings forecasts have been on the slide:

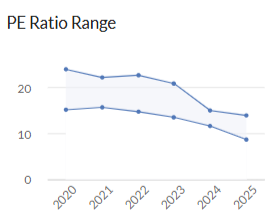

But has the market overcompensated? The P/E multiple is depressed by historic standards, implying a great deal of pessimism:

Let’s do a quick comparison with Gocompare.

Future paid £594m for it in 2020.

The previous year, in 2019, GoCompare had generated revenues of £152m. Its operating profits were volatile, halving to £20m from £37.5m.

But in simple terms, Future paid nearly 4x trailing revenues for GoCompare.

Given what’s happened to Future over the years, someone might argue that they were probably overpaying for deals.

But the point stands that they paid a trailing price/sales multiple of nearly 4x.

MONY is only trading at a P/S multiple of 2x.

If we depress the EBIT multiple as much as possible by using the £37.5m figure (GoCompare’s operating profit in 2018) instead of the £20m figure (GoCompare’s operating profit in 2019), then the trailing EBIT multiple was 16x.

I calculate that MONY’s trailing EBIT multiple is currently 8x.

There are reasonable counter-arguments. Things have changed since 2020. AI is a threat. Growth is hard to come by. The business models will have to constantly adapt to keep up with the times.

Even so, I can’t help noticing that MONY is trading at half the valuation at which GoCompare was taken over.

This might be a little foolhardy, and it definitely reflects my own biases in favour of this sector (online platforms), but I’m going to upgrade our stance on this to GREEN.

ASA International (LON:ASAI)

Unch. at 214.85p (£215m) - Q1 2026 Business Update - Graham - GREEN =

(At the time of writing, Graham has a long position in ASAI.)

We had full-year results from microfinance provider ASAI recently, and they are back again with a Q1 update.

Loan portfolio $583m, up 25% year-on-year.

Year-on-year growth was 33% at the full-year results; it has actually shrunk since Dec 2025: this reflects “usual seasonal repayment patterns after the holiday period”.

Client base up 12% year-on-year to 2.7 million, and up 1% in Q1.

However, these figures exclude the business in India, which is being wound down. Including India, client numbers fell 2%.

Portfolio at risk (due more than 30 days) rose to 2.0%. It was 1.8% in December 2025. It was 2.2% a year ago. This reading doesn’t worry me.

India wind-down progress:

As at 31 March 2026, India clients had reduced by 75% year-on-year to 38k, the branch network by 53% to 75, and Gross OLP by 76% year-on-year to USD 7.2m.

This wind-down “materially reduces exposure and simplifies the Group”.

I do wonder why the business doesn’t work in India. My impression is that Indian borrowers have access to many more lenders, which breaks the microfinance model (as it becomes necessary to understand a borrower's total indebtedness, not just their ability to repay the microfinance loan).

CEO comment:

Q1 2026 demonstrates the underlying strength and discipline of ASA International's platform. Across our continuing operating platform, we delivered solid portfolio performance alongside continued client growth across key markets, with particularly strong momentum in Pakistan and East Africa. Portfolio quality remains robust and among the best in the industry, reflecting the effectiveness of our risk management and long-standing client relationships.

Graham’s view

I’m pretty excited about this one. It’s only 2% of my portfolio and I’m open to the idea of adding to it over time. For previous coverage, check the archives - and my initial writeup back in January.

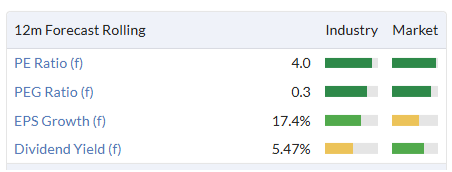

A reminder of the value metrics:

This can be a pretty dangerous sector, of course. I’ve invested in unusual lenders in the past, and am comfortable with the risks. I can well understand why others might wish to stay from a business lending to low-income individuals in far-flung parts of the world.

Mark's Section

Brave Bison (LON:BBSN)

Up 6% at 78p (£87m) - Final Results - Mark - AMBER/GREEN =

Some really strong headlines here:

These were said to be “all ahead of recently upgraded consensus expectations “ which is great to see. However, there is a certain amount of marketing gloss applied.

Acquisitions:

Not all this growth is organic and the company has made a number of acquisitions during the year. We’ve generally appreciated their deal-making on the DSMR, with many acquisitions requiring little capital up front. However, as far as I can see they don’t actually break out the organic growth figure, so it is hard to judge the underlying performance of the business.

Dilution:

The company conducted a £15.5m equity raise in the year to fund the acquisition of Mini-MBA. This means that the Adj. EPS, which is what equity holders actually care about, rises by a much more modest 15%.

The weighted average number of shares was 81.0m versus 64.5m the year before (adjusted for the share consolidation). Following the deal with System1’s founder to exchange shares, they now have 112.2m shares in issue.

Earnings in FY26 will obviously benefit from a full year of the acquired businesses. However, the shares in issue are now almost double the previous year, and will act as a drag on EPS growth.

Adjustments:

Being this acquisitive leaves a huge gap between adjusted and statutory figures:

While excluding these costs tends to be a market norm, I can’t help feeling this is a bit like asking to have your cake and eat it. For a company that makes a one-off acquisition it would seem fair to adjust these out, far less so for a business that made five in a single year.

Cash flow

Given all of this, perhaps the best measure to look at is the cash movement. Cash inflow from operating activities rose nicely from £1.6m to £3.2m for the year. However, the fully-diluted market cap is now 91.0m, meaning that this is trading at 29xOCF, not necessarily as cheap as the headline EPS figures suggest.

Outlook:

The good news is that they are upgrading the FY26 outlook:

The Board expects net revenue and Adj. EBITDA to exceed current consensus expectations for FY26. Net revenue in Q1 FY26 is expected to increase 58% year-on-year, an encouraging performance despite the conflict in the Middle East causing some clients to review spending.

They highlight the 18% organic growth in MiniMBA which shows that this was a good deal despite the dilution required. To upgrade this early in the year is a good sign and suggests that there could be more to come during the year.

Forecasts:

Unsurprisingly, Cavendish raise their estimates, saying:

We have lifted our revenue by 9% to £49m. This feeds through to a 9% upgrade in adj EBITDA to £10.3m. The upgrade to basic adj EPS is 15% to 8.1p, representing an impressive 17% YoY growth rate. This would be even higher at 24% YoY growth on an underlying basis if we stripped out the impact of the business starting to pay corporation tax.

This makes the shares look good value on a P/E of less than 10. However, I have to question how much heavy lifting the word “adjusted” will be doing. Cavendish are forecasting operating cash flow to be only around 14% of EBITDA, due to £8.1m of working capital outflow.

Balance sheet:

On first look, the net cash of £4.3m is impressive. Although it is down from £7.5m the year before, this has been a year of great corporate activity.

However, looking into more detail, I can see why Cavendish forecasts a large working capital unwind. Trade payables look particularly elevated:

And there are ongoing acquisition liabilities:

The company is still forecast to have around £2m of net cash at the year end, but they could still owe £2.8m for past acquisitions if these continue to perform as expected. It looks like they will probably have to resort to more equity finance if they want to do any major deals in 2026

Mark’s view

As with many marketing companies, things look less rosy once you look below the veneer of the headlines. With no organic growth figures given, and the number of acquisitions it is very hard to work out the underlying performance. Using operating cash flow to cut through everything reveals a business that may be trading more expensively than the (heavily-adjusted) headlines may suggest.

However, there is certainly trading momentum behind the company with a 15% upgrade to adj. EPS just four months into the year, suggesting that there could well be more upgrades to come. If they do, they look like they will need to come from organic growth or bolt-ons as the balance sheet capacity for further major deals looks limited.

We rated this AMBER/GREEN at around the same share price in the past and I see little reason to change this, given today’s upgrades.

IG Design (LON:IGR)

Up 27% at 71p (£68m) - Trading Update and Acquisition of Glenart, S.A. - Mark - AMBER/GREEN =

This update has been well-received by the market today:

Following the positive trading update issued in February, the Group has continued to experience good trading momentum, and the Board is pleased to announce that FY2026 results are expected to be ahead of market consensus and Board expectations. The Group expects to report FY2026 revenues of c$292 million and adjusted operating profit of c$12.8 million, representing an adjusted operating margin of 4.4%, and delivering adjusted profit before tax of c$11.5 million.

Revenue is around 3% ahead of Canaccord’s previous estimate and the combination of higher revenue and better margins sees them raise adj. EBIT forecasts by 16% to $12.8m.

This isn’t just viewed as a one-off either, with FY27 & 28 revenue raised by 2.6% and 2.2% respectively. This is helped by an acquisition, also announced today.

Acquisition:

Glenart S.A. is a South African manufacturer within the Group's "Celebrate" category, with a particular strength in crackers, and is therefore highly complementary to the Group's existing operations. The business generates the majority of its revenues in South Africa, the UK and the USA, and operates across similar mass-market and trade channels to the Group. The Board considers the acquisition a bolt-on, strategically aligned and a compelling opportunity to expand the Group's geographical presence in a complementary product offering.

These are reasonable numbers, but perhaps doesn’t really move the needle:

For the year ended 28 February 2026, the business reported unaudited revenues of c£4 million, PBIT of c£0.8 million and EBITDA of c£1million, from a net asset base of c£2.7 million.

Forecasts:

If we assume similar trading performance going forward, then Canaccord is effectively upgrading the existing business by around £1m of EBITDA in FY27 and £0.2m in FY28.

The company gets a further benefit from better than anticipated cash flow. Canaccord say:

YE net cash of $72m is also significantly ahead of updated February guidance of c.$55m to $60m (CGe $58.0m), reflecting continued disciplined cash and WC management and the sale of a surplus UK warehouse for $4m. Ex the c.$35m DG Americas outflow, continuing operations generated over $20m of cash in FY26. As previously flagged an update on future capital allocation will be provided at the prelims.

This means PBT forecasts rise 21% for FY26 to $11.5m, 22% to $12.9m for FY27 and 11.9% for FY28.

Valuation:

Canaccord calculates that the company is on a forward EV/EBITDA of less than 2, which seems very cheap. However, this is not a great metric for this company. While it is undoubtedly good news that they report such a significant cash beat, they have a carefully chosen year-end where they typically report the highest cash balance of the year. As a seasonal supplier to retailers, they see big working capital swings during the year. Investors may recall that this is a business that almost went bust while reporting roughly $20m of net cash a few years back.

Since getting rid of their US business, which was 2/3rds of turnover for a nominal sum, the remaining European business has been transformed. However, Canaccord are still forecasting a decline in EPS from FY26 to FY27, and they are on 14.7x FY28 adjusted earnings after today’s rise. This is very expensive for this type of business.

However, they did pay dividends in 2021, and could well see a modest payout now affordable.

Mark’s view

The rise this morning largely reflects the increase in broker forecasts, meaning this trades on roughly the same multiple as before. A 2028 P/E of 14.7 doesn’t exactly scream value for this type of business. However, net cash of $72m is 76% or the market cap, even after today’s rise. The big question is how much of that cash is genuinely surplus to requirements. If the answer is none of it and it is needed to fund the working capital cycles then the reality is that these assets are pretty much permanently unproductive based on current forecasts, and the shares are overvalued (unless there is a costless way of winding down the business.) If the reality is that say half that cash could be distributed (or spent on earnings enhancing acquisitions), then this is looking potentially undervalued.

The problem I have is that I simply have no idea what proportion could be excess to requirements in the new structure without NA. As such I would normally just rate this as AMBER; filed under “too hard”. However, given that this is now the second upgrade in a row I think we should remain relatively generous and keep the AMBER/GREEN view.

DCC (LON:DCC)

Down 2% at 5760p (£5.0bn) - Rejection of possible offer - Mark - GREEN =

Yesterday morning DCC’s shares were up 9.3% in response to an announcement that they had received a possible offer. Today we find out that the offer was rejected and I can see why:

The Proposal comprised 5,800 pence in cash per DCC share, and assumed no further distributions or dividends will be declared or paid from the date of the Proposal.

This is something like a 12% premium to the undisturbed price. Why would shareholders take the risk of an equity investment to sell out for a mere 12% premium?

I rarely look at companies of this size. However, my friend Jamie Ward presented it as his pick on the BASH at Mello Birmingham.

To my discredit, before looking at the business I thought it did marketing, as in media marketing. In reality it is an energy marketer, i.e. it owns Petrol Stations and similar!

I am probably doing Jamie’s argument a disservice but it boiled down to that between about 2009 and 2018 the company rolled up energy business and compounded EPS at mid-double digits percentage rate and the market rewarded it with a mid-teens P/E. Since then, the company has continued to grow but at a slightly slower rate, and the market reaction has seen a significant de-rating:

However, it remains very much the same business with a similar outlook.

That private equity acquirers recognise the long-term cash flow potential of the business is perhaps not surprising. That they thought that shareholders would roll over for a 12% premium does surprise me.

Mark’s view

That Private Equity have come sniffing reinforces why Roland had a GREEN view on this company, as these firms clearly see similar attractions. That the company only received a 12% premium offer (so far) is perhaps a reflection that this is already a sizable business, with modest net debt (leveraging a business is often a source of PE returns) and a reasonable (but not stand out) multiple in the current markets.

There’s alway the chance they come back with something more punchy, but the gap between the initial offer and what would be acceptable looks insurmountable to me. However, I can see the attraction for those with long-term investment horizons and PE interest backs that up, even if they haven’t been willing to pay up so far.

Chesterfield Special Cylinders Holdings (LON:CSC)

Down 13% at 45p (£18m) - FY26 Trading Update - Mark - BLACK (AMBER/RED =)

That the share price is down a double-digits percentage is perhaps not surprising in response to this update:

Overall, the Company now anticipates a full-year revenue and adjusted EBITDA performance at similar levels to the previous year (2025: revenue of £16.6 million, adjusted EBITDA of £0.8 million), slightly behind market expectations (adjusted EBITDA of £1.0 million).

Even here, there appears to be some hope built into these figures, as H1 shows an EBITDA loss, something that always makes us cautious on the DSMR:

Trading in the first half of the year was broadly in line with management expectations, and the Company expects to report a first-half revenue of £6.4 million (2025: £5.4 million) and an adjusted EBITDA* loss of £0.8 million after central costs (2025: loss £1.3 million).

What is surprising is that the share price has been so strong over the last six months:

Especially given the history of misses and downgrades:

Forecasts:

Can’t see any updated broker coverage this morning, so it seems unlikely that these delays to projects have suddenly led to a bumper FY27 forecast. As such, the rating seems high for a company with no asset backing.

Mark’s view

While the company may have rebuilt its finances by selling off their PMC division, it seems old habits die hard and the business continues in its tradition of missing forecasts. Even if it hits FY27 numbers it doesn’t look particularly cheap. Almost also the purported value is in contracts that deliver outside the forecast window. Too far away to have any confidence of profitable delivery, given its chequered history. This profits warning, while relatively minor, reinforces why I remain mostly negative. AMBER/RED

See what our investor community has to say

Enjoying the free article? Unlock access to all subscriber comments and dive deeper into discussions from our experienced community of private investors. Don't miss out on valuable insights. Start your free trial today!

Start your free trialWe require a payment card to verify your account, but you can cancel anytime with a single click and won’t be charged.