Hello again!

I'm sorry we had far more stories to cover than we could get around to today. Hopefully we'll get a chance to do some backlog work tomorrow.

Spreadsheet accompanying this report: link.

Companies Reporting

| Name (Mkt Cap) | RNS | Summary | Our view (Author) |

|---|---|---|---|

Tritax Big Box REIT (LON:BBOX) (£4.1bn | SR56) | An update on the planning application relating to its proposed data centre development at Manor Farm. BBOX now expects “practical completion” (PC) between October 2027 and March 2028 (previous expectation: PC between July and December 2027). | ||

Old Mutual (LON:OMU) (£3.0bn | SR90) | Group equity value per share increased by 2% to R19.80. IFRS profit increased by 10% to R8.4 billion. Total dividend 93 cents per share, up 8% year-on-year. Outlook: “the South African outlook has become more constructive, supported by the 2026 National Budget, which reaffirmed a commitment to fiscal discipline.” | ||

Primary Health Properties (LON:PHP) (£2.6bn | SR73) | Results include 4.5 months post-merger with Assura. EPRA net tangible assets down 4% to 99p as a result of shares issued in relation to the merger, and transaction costs. LTV 57%, temporarily above the targeted range 40% to 50%. | ||

Yellow Cake (LON:YCA) (£1.49bn | SR50) | On 16th March, YCA took delivery of 1,331,912 lb of U3O8 from JSC National Atomic Company Kazatomprom. | ||

Vistry (LON:VTY) (£1.24bn | SR88) | Appoints Rob Woodward CBE as Non-Executive Chair. | ||

Travis Perkins (LON:TPK) (£1.24bn | SR84) | Like-for-like revenue +0.3%, adjusted operating profit -12.5% (£133m). Statutory after tax loss £176m (previous year: £77m loss). “The trading environment since the start of the year has remained subdued and this reflects a continuation of the weak UK construction activity figures reported for the final quarter of 2025.” | ||

Trustpilot (LON:TRST) (£683m | SR40) | Bookings +18% at constant currency, PBT £14.1m (2024: £5.2m). Probability ahead of expectations. Net dollar retention rate 102%. Outlook: “Following another year of strong bookings growth in 2025, we expect high-teens revenue growth at constant currency in 2026. Alongside this revenue growth, we expect to deliver a 2-3ppts increase in our adjusted EBITDA margin.” | ||

Close Brothers (LON:CBG) (£538m | SR49) | “A resilient trading performance reflecting cost discipline, solid credit performance and a robust net interest margin.” Adjusted operating profit down 19% (£65.2m). Actual operating loss £65.2m (previous year: £102.2m). Outlook and guidance unchanged except for accelerated cost savings targets. | ||

Harworth (LON:HWG) (£561m | SR35) | Total accounting return 1.7% (2024: 9.1%). Operating profit £21.6m (2024: £74.6m). “Significant progress identifying data centre and power-enabled land portfolio within our land bank.” Refinanced and enlarged RCF to £275m. | ||

Wickes (LON:WIX) (£500m | SR85) | Revenue +5.9%. Adjusted PBT +14.4% (to £49.9m). Statutory PBT £48.7m (2024: £23.2m after non-cash impairment charge). Outlook: “...while outdoor project demand has been impacted by wet weather, we have experienced continued volume growth across indoor projects and D&I (Design & Installation)… we remain comfortable with consensus expectations for adjusted PBT in 2026.” | ||

Boku (LON:BOKU) (£482m | SR34) | Revenue +30%, adjusted EBITDA +36% ($41.3m), operating profit +205% ($18.9m). “As global e-commerce becomes increasingly dependent on a diverse range of payment methods, our role as a growth partner to global merchants around the world continues to deepen.” Medium term guidance unchanged. | ||

IP (LON:IPO) (£435m | SR37) | NAV per share up 13% to 110.4p. Target confirmed to deliver >£250m of exits between 2025 and end 2027. Total portfolio £908m. | ||

Mortgage Advice Bureau (Holdings) (LON:MAB1) (£315m | SR68) | Revenue +19.6%, adjusted PBT +13.3% (£36.3m). “2026 has started with good momentum, and the Group continues to trade in line with the Board's expectations.” | GREEN = (Graham) I see little reason to change my positive view as expressed in January. It’s a quality business and it’s not too expensive here, in my view. The share price has been discounted since January. Of course if we are being far too optimistic on the outlook for the mortgage market, then this is going to be a bad call. | |

Yu (LON:YU.). (£301m | SR98) | Revenue +8%, adj. EBITDA +4%, PBT +9% (£49m). Meter points supplied up 49% organically. Outlook: “Strong momentum from 2025 has continued into 2026 with record revenue, EBITDA and record cash balance in Q1, despite market uncertainty… Adjusted EBITDA and PBT in line with 2025, with growth of underlying profitability tempered by overhead investment to support future growth opportunity.” | ||

Ashtead Technology Holdings (LON:AT.) (£296m | SR49) | Revenue +21%, adjusted EBITA +17.5% (£59.1m), PBT +14.3% (£41.2m). Outlook: Trading in the first two months of 2026 has been in line with management's expectations. We are closely monitoring the current situation in the Middle East which has created volatility in oil and gas markets and project execution timing uncertainty in the region… the Board remains confident in delivering further progress in 2026. | AMBER/GREEN = (Roland) [no section below] In January I upgraded my view on offshore oil and gas equipment rental business Ashtead to AMBER/GREEN. I think I can probably hold onto that view based on the strength of today’s results and unchanged outlook guidance. While organic revenue growth of 3% is unexciting, last year’s acquisitions appear to be making a positive contribution to revenue and have not diluted the group’s profitability. My sums show operating margin stable at 25% last year, with return on capital employed improving to 18% (2024: 15.4%). The main risk flagged up today is unsurprisingly the risk of “extended or wider disruption” in the Middle East. Ashtead says this has already created some “project execution timing uncertainty” in the region. There’s clearly a risk this could worsen, but the Middle East only contributed 6% of revenue and held 4% of assets last year, so I would guess any problems should be manageable if the energy sector remains buoyant elsewhere. Current consensus suggests further modest growth in 2026. With Ashtead shares trading on eight times forecast earnings, my view remains broadly positive. | |

Property Franchise (LON:TPFG) (£263m | SR55) | Revenue +25%, or 9% growth on a pro-forma basis. 51% of revenue was from recurring sources. Adjusted PBT +39% (£31m). Outlook: “Well positioned to navigate anticipated market conditions in 2026, including the impact of evolving government legislation.” | GREEN ↑ (Graham) I think I’m going to stick my neck out and upgrade this to GREEN on the basis that 1) the market cap is lower than it was the last time I checked, and 2) the profit outlook has improved. The P/E multiple on 2026 earnings is currently 10.3x. Not a bad entry point, perhaps, for those of who are long-term fans of the business? | |

Essentra (LON:ESNT) (£257m | SR35) | Revenue down 0.1%, but up 2.5% at constant currencies. Adjusted operating profit down 20.2% (£32m). FY25 in line with expectations. Trading-to-date in the new financial year provides confidence in achieving the Board's expectations for 2026. | ||

Gore Street Energy Storage Fund (LON:GSF) (£245m | SR N/A) | Commits to distributions of 7p per share annually, payable quarterly. Will be funded through operating cash flows and asset sales. Expects to generate £25m from disposals in FY27 and £75m in FY28. Also plans to add c.100MWh of capacity in each of FY27 and FY28 | ||

Science (LON:SAG) (£229m | SR92) | Revenue flat, adj operating profit up 7% to £23.1m. Operating results augmented by pre-tax gain of £24.1m from corporate investment in Ricardo, giving total pre-tax profit of £41.5m. Outlook: revenue growth may be constrained in the current geopolitical environment, but the Board retains a positive outlook. | ||

Empire Metals (LON:EEE) (£213m | SR17) | Diamond core drill programme completed at Thomas Prospect for 745m, “very high-grade TiO2 intervals identified near surface”. | ||

SThree (LON:STEM) (£212m | SR97) | Net fees down 8% YoY, a significant improvement on the prior-year rate of decline. Stabilisation supported by “ongoing growth in the USA and Japan”. Contractor order book down 7% to £152m, providing visibility of around five months’ net fees. Outlook: FY26 expected to be in line with previously announced c.£10m pre-tax profit guidance. | ||

Fintel (LON:FNTL) (£198m | SR38) | Revenue up 10% with adj EPS up 3.8% to 13.7p, in line with expectations. Notes 10% growth in recurring revenue and “accelerated development of digital & AI enabled compliance tools”. Outlook: strong start to the new year, trading in line with the Board’s expectations. | ||

Zotefoams (LON:ZTF) (£183m | SR93) | Revenue up 7%, adj pre-tax profit up 39% to £21.2m. Adj EPS up 46% to 38p, ahead of consensus of c.32p. Outlook: demand patterns are becoming more balanced and volumes are expected to moderate from the “unusually high levels” of 2024 and 2026. Focus in 2026 is on execution and delivery. Confident that “medium-term prospects are in line with our stated ambitions”. Trading so far in 2026 has been in line with expectations. | AMBER/GREEN = (Roland) Checking the accounts shows that the EPS beat here is purely due to the recognition of deferred tax assets last year. Looking at pre-tax profit tells us that operating performance was in line with expectations. I am impressed with evidence of improved profitability and strong cash generation. The only thing I’d highlight is that today’s outlook guidance indicates exceptional footwear demand from 2024/25 is now expected to normalise. In my view, this comment leaves some scope for interpretation. Growth elsewhere in the business is expected to offset any weakness in footwear, but I am not sure how confident we can be at this stage. Nevertheless, I remain impressed with execution and progress here and am happy to maintain our broadly positive view based on today’s results. | |

Midwich (LON:MIDW) (£165m | SR72) | Revenue down 1.5%, adj pre-tax profit down 22% to £30.5m. Adj EPS down 17% to 22.37p. Net debt to EBITDA ratio of 2.17x (FY24: 2.0x). Full-year dividend reduced to 5.25p (FY24: 13.0p). Outlook: working assumption is that there will be little improvement in 2026 | BLACK? Roland: I wonder if this outlook commentary may indicate a possible cut to FY26 guidance. We don’t have access to any updated broker notes this morning but previous consensus was for a c.10% rise in earnings in 2026. | |

Fonix (LON:FNX) (£153m | SR58) | Revenue up 7.1%, adj pre-tax profit up 2.6% to £8.0m. Adj EPS unchanged at 6.2p. Rollout in Portugal is progressing well. The company has begun a pilot with a major broadcaster in a third European market and has also started expansion into a fourth European market. Outlook: confident in the Group’s strategy and expect to deliver “long-term value for shareholders in line with market expectations”. | ||

Atlantic Lithium (LON:ALL) (£106m | SR16) | Secured access to funding for up to $16.4m (£12.2m). This comprises an $11m investment from a group of Ghanaian pension funds through a subscription to new shares at 14.6p + “milestone-linked warrants”, plus a £4m share placing under the company’s agreement with Long State Investments. | ||

Strategic Minerals (LON:SML) (£105m | SR41) | New contract for infill drilling at Redmoor tungsten project. Fully funded through £4m placing announced in January. | ||

Eagle Eye Solutions (LON:EYE) (£96m | SR42) | Revenue up 16% to £22.4m, recurring revenue up 24% to £19.1m. Adj EBITDA down 28% to £4.3m. Confident in delivering FY26 results in line with recently increased expectations. | ||

Pebble (LON:PEBB) (£73m | SR95) | Revenue down 0.5% with pre-tax profit down 14.8% to £6.9m. Adj EPS down 16.6% to 3.86p, in line with expectations. Launches £5m share buyback. Panmure Liberum: FY26E adj EPS cut by 14% to 4.0p, FY27E adj EPS raised by 8% to 5.4p, to reflect increased investment in Facilisgroup in FY26. | BLACK | |

Intercede (LON:IGP) (£58m | SR40) | Expect to deliver recurring revenue growth in FY26 (y/e 31 March), but full-year revenue is expected to be 8-9% below current expectations of £18.7m, with adj EBITDA to be 15-18% below expectations of £4.6m. Company blames procurement delays, particularly in the US, and purchasing deferrals relating to geopolitical uncertainty, including the Middle East. Outlook: FY27 revenue target of £21m is unchanged. | BLACK (AMBER/RED) = (Roland) [no section below] In October, Mark flagged up the “higher-than-usual H2 weighting” that would be required for this digital identity specialist to meet full-year forecasts. Today we have confirmation that this ambition proved unachievable, with big cuts to both revenue and EBITDA guidance for the year ending 31 March. Management says that sales are delayed, not lost, and that order intake momentum improved in H2. However, Intercede has a track record of inconsistent growth. While the company is in the process of shifting to a subscription model, it’s still quite dependent on high-margin but lumpy licence sales. Given the significant shortfall in FY26 revenue and the reasons for it, I am not sure how much confidence we can have in revenue guidance for FY27 at this stage. Intercede shares are still trading on 16x FY26E earnings after this morning’s drop, so are not obviously cheap given the uncertain growth outlook. I’m going to maintain Mark’s cautious view following today’s profit warning. | |

Volvere (LON:VLE) (£56m | SR98) | Net assets up by 15% to £19.80 per share, net cash up by 19% to £33.22m. Revenue from continuing operations (Shire Foods) up 7% to £52.7m, pre-tax profit up 6% to £6.75m. Saw some pressure from cost inflation in H2, but continuing to invest in production capability and productivity. No change to long-term strategy, strong balance sheet allows business to “respond quickly”. | AMBER/GREEN = (Graham) I’m staying AMBER/GREEN on this as although I do think it’s undervalued, I also think that the logical next step for it is to return surplus cash to shareholders - which it's probably not going to do. | |

STV (LON:STVG) (£50m | SR36) | Revenue down 6%, with total advertising revenue down 10%. Studios revenue down 1%. Adj operating profit down 44% to £11.6m. No final dividend proposed. Management, targeting £8m of cost savings in FY26, notes that STV Player “achieved highest ever consumption, up 9% to 75m hours” in 2025. | ||

Water Intelligence (LON:WATR) (£45m | SR89) | Revenue up 9%, with adj pre-tax profit up 9% to $9.2m. Leverage of 1.17x EBITDA at year end. “The Group's competitive strategy of Preventive Maintenance is gaining traction.” | BLACK | |

Virgin Wines UK (LON:VINO) (£27m | SR86) | Revenue up 2%, outperforming wider drinks market (-11%), demonstrating market share gains. Pre-tax loss of £0.4m (H1 25: £1.3m profit) due to investment in growth. Net cash of £10.6m. Outlook: planning extra £550k of marketing spend this year, resulting in an increase in the expected loss for y/e 30 June 26. Cavendish: FY26E adj EPS reduced to -2.0p (prev. -0.79p). | BLACK | |

Abingdon Health (LON:ABDX) (£21m | SR19) | Revenue up 45% to £4.5m, adj EBITDA loss of £1.7m due to investment in overhead base to support expansion. Cash of £3.7m at 31 Dec 25 following net proceeds of £3.2m from placing. H2 FY26 is expected to be EBITDA and operating cash flow positive. FY26 revenue guidance unchanged at £12.6m. | ||

Thor Energy (LON:THR) (£11m | SR14) | Core objectives achieved: increased coverage of Phase-1 low coverage areas and added density in high focus exploration articles, with results confirming Phase-1 outcomes. Improved acquisition and sampling processes. Preliminary analysis of data is underway. | ||

Shearwater (LON:SWG) (£10m | SR41) | Revenue +31% vs the equivalent prior period (Jul-Dec 25) and +24% vs reported FY25 interim results. Adj EBITDA of £0.0m and reported H1 loss of £0.4m. Outlook: strong pipeline with H2 contract wins already secured. Remains confident of delivery of FY results in line with expectations. | ||

Litigation Capital Management (LON:LIT) (£10m | SR21) | An Australian Court has delivered a finding against LCM’s funded party. LCM had funded the case with A$1.4m. ATE insurance is in place to protect against adverse costs risk. LCM is reviewing the judgement and assessing potential next steps. |

Graham's Section

Volvere (LON:VLE)

Down 2% to £25 (£55m) - Trading Update and Notice of Final Results - Graham - AMBER/GREEN

(At the time of writing, Graham has a long position in VLE.)

It’s very important for readers to understand that I’m conflicted when it comes to this stock.

I’ve been invested here for 10 years, and it has grown to become an extraordinarily large part of my single-stock portfolio (currently 32%).

Indeed, it would be even higher - 36% - if I hadn’t started selling it this year.

My main reason for selling is that this level of concentration is not something I’m comfortable with. It’s a nice problem to have (when a successful investment becomes a very large part of your portfolio), but it’s a problem nonetheless.

So I am currently selling Volvere. I haven’t made the final decision in terms of how much of it I’m going to sell, but I am gradually reducing my position.

Now you know that I’m conflicted, let’s get into this trading update.

Volvere plc (AIM: VLE), the growth and turnaround investment company, is pleased to provide the following trading update for the financial year ended 31 December 2025.

Brief background for anyone who is new to the story: Volvere was managed for many years by the Lander brothers, until Jonathan Lander passed away in 2023. His brother Nick, also a co-founder of the company, continues to manage the business.

While in theory this is an investment vehicle that should invest in multiple businesses, it is currently concentrated in the food sector with a single operating business - Shire Foods, based in Leamington Spa. They have been “making delicious British pies for over 50 years”, and are major suppliers into discount supermarkets.

Therefore, Volvere these days is a strange hybrid between an investment vehicle (which dutifully reports its NAV to shareholders as a key metric) but which in reality is just one business plus a large pile of cash.

The cash pile is strangely large - it really ought to have been invested by now, but management have preferred not to invest it until they find a truly high-conviction opportunity.

Needless to say, this is a rare attitude.

And I shouldn’t complain too loudly about the cash drag: if management weren’t so cautious, then I would never have allowed this to become such a large percentage of my portfolio in the first place. And their long-term record has been excellent, despite their caution.

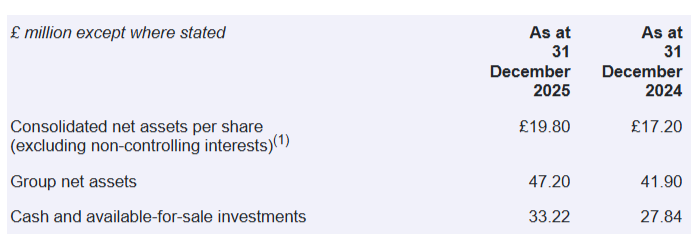

NAV per share was 116p in 2006, had grown to 583p by 2016, and has now reached 1980p as of December 2025.

One feature that has aided the growth of NAV is that they take the Berkshire Hathaway approach of buying back stock rather than paying dividends (disclosure: I’m long BRK.B too).

Today’s main figures:

So that’s 15% year-on-year growth in net assets per share.

The current share price is a 26% premium to NAV per share.

However, NAV per share is not really the right way to value Volvere at the moment. As noted above, it’s less of a fund and more of an operating business. And we don’t value most operating businesses purely on NAV.

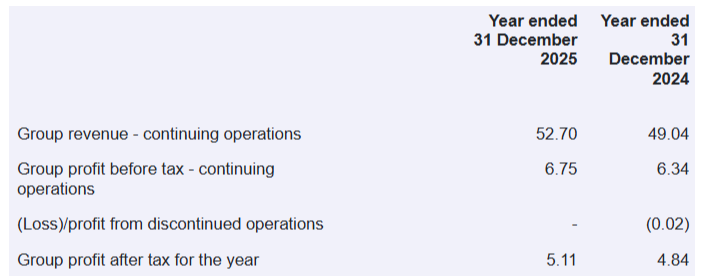

Which brings us to profitability:

“Continuing operations” refers to Shire Foods.

Trading performance at Shire Foods was broadly satisfactory. Shire's underlying profit before tax, intra-group interest and management charges was £6.31 million (2024: £6.17 million), stated before a one-off credit relating to provisions considered no longer required of £0.40 million (2024: £nil), giving an overall result of £6.71 million.

Volvere itself owns 80% of Shire Foods, with the other 20% very helpfully incentivising Shire’s managers.

Therefore when it comes to valuing VLE, I’m going to adjust the £6.3m profit figure down to £5m, excluding the slice not owned by Volvere itself.

Outlook:

I also note the reference to the 2025 performance as “broadly satisfactory”, which in practice means “slightly disappointing”.

The outlook is also a bit mixed, which makes sense in the current circumstances:

We started to feel the impact in the second half of 2025 of increasing raw material and distribution costs. Although this has continued in 2026, we are continuing to invest in our production capability, with a focus on increasing productivity, as well as increasing prices. Whilst underlying profitability in 2025 was marginally lower than we would have liked, we think it represents a good performance in the market in which we operate.

A continuing high oil price is likely to impact Shire's supply chain and we are monitoring it closely. Our available-for-sale investment has fallen in value since the year end, reflecting geo-political events and market volatility, but remains significantly ahead of our purchase cost. Notwithstanding the current uncertainty in terms of cost inflation and the potential impact of inflationary pressures on consumers, we remain committed to our long-term strategy for Shire through a focus on innovation, quality and efficiency.

The “available for sale investment” is, I understand, an investment in a liquid UK stock (probably a financial stock?) that was identified by Jonathan Lander a number of years ago, and continues to be held to this day.

Graham’s view

We’ve been AMBER/GREEN on this: see comments by Roland in September and myself last May, with the market cap being just below £50m in both cases.

I’m inclined to leave that stance unchanged today.

Management's commentary could be seen as a profit warning, if we took a very harsh view. But the forward guidance given is ultimately rather vague, and the miss against expectations for the 2025 result is only “marginal” (“...2025 was marginally lower than we would have liked.”)

Furthermore, I think that modest expectations are already baked into the valuation here.

Let’s do a quick review of the valuation.

Cash and available for sale investments at year-end: £33m.

Let’s reduce this to £32m as the available for sale investment has reduced in value since year-end.

Market cap £55m

That leaves an enterprise value of about £22m.

That £22m figure is the value being given to Shire Foods on an ex-cash basis. Shire does use a little borrowing, but it also has valuable freehold properties and owned equipment. The interim results showed PPE of £7.8m.

Given that Volvere has been consistently profitable for years and continues to perform pretty well despite tough circumstances, I do think the enterprise value of £22m is on the low side. As I said above, I think that Volvere’s share of 2025 pre-tax profits is around £5m. After-tax, that's £3.8m. For a reputable food manufacturing business with freehold property, does it really make sense that it should trade on an implied P/E multiple of about 6x? I think that's pretty cheap, personally (but then I would say that!).

There are of course some risks, and I should try to name them:

Certain of Shire's customers (i.e. one or two supermarket groups) are likely to be responsible for very large percentages of Shire’s revenues, so there is customer concentration risk.

In general it’s difficult for manufacturers to earn sustainably high ROCE and high margins. In 2025, profit growth could not keep pace with revenue growth. So while profits have been on a pleasing upward trend, it would be wrong to assume that this is going to continue indefinitely, or to get too ambitious when it comes to the valuation that a buyer might place on it.

And I think the really big risk is what Volvere might do with its cash pile.

I’ve said before that I would be fine with Volvere selling off Shire (at a reasonable valuation) and returning all funds to shareholders. That remains my view today.

However, the company appears very unlikely to do that. They are far more likely to make a new investment:

We continue to review potential investments and would expect an increase in distressed businesses, particularly if cost inflation becomes evident and interest rates are accordingly held or increased. The Group's strong balance sheet means we are able to respond quickly to anything of interest should it arise.

It will be fascinating to see what new investment they might make. It has been many years since their last one - I think the last time was in 2020.

I do take comfort from the fact that they have spent so long waiting for the next investment. I can only presume that when they do eventually take a swing, it will be at a “fat pitch” - a situation where it’s almost impossible to lose money, due to asset backing, and with considerable upside if it works out. But of course, no investment is entirely without risk.

I’m staying AMBER/GREEN on this as although I do think it’s undervalued, I also think that the logical next step for it is to return surplus cash to shareholders - which it's probably not going to do.

Property Franchise (LON:TPFG)

Up 5.5% to 434.6p (£277m) - Final Results - Graham - GREEN ↑

The Property Franchise Group PLC, the UK's largest multi-brand property franchisor, is pleased to announce its Final Results for the year ended 31 December 2025 ("FY25").

The merger with Belvoir occurred on 7th March 2024, which means that most of the growth numbers in today’s report aren’t very meaningful (e.g. revenue +25%, EBITDA +49%).

The company doesn’t helpfully let know that that like-for-like (or “pro-forma”) growth was 9%.

51% of revenue is from “recurring revenue sources”, down from 52% last year.

This reflects softness in the rental market:

Managed portfolio of 149,000 properties (2024: 153,000), reflecting landlord caution ahead of the Renters' Rights Act and a more measured pace of portfolio acquisitions

Net debt finished the year at the very modest level of £2.3m, which is effectively zero for a business that has just earned an adjusted PBT of £31m.

Full year dividend is 22p, up from 18p the prior year.

Outlook:

Focused on delivering further revenue synergies arising from the Group's increased scale and platform capabilities

Well positioned to navigate anticipated market conditions in 2026, including the impact of evolving government legislation

CEO comment:

2025 was characterised by strong organic growth and solid operational progress across all three divisions, delivering profitability ahead of expectations. The scale and capability built through last year's acquisitions materially strengthened our strategic position and underpin the continued development of our platform model, enabling us to deliver enhanced value to franchisees, licensees and advisers.

Estimates

With thanks to Cavendish, the new PBT forecasts are as follows:

2025 actual result is £30.8m, <1% ahead of forecast.

2026 forecast £31m, upgraded by 3.6%

2027 forecast £36.3m, upgraded by 5.9%

Revenue forecasts have been upgraded by 5%-6%.

Graham’s view

It seems that the merger with Belvoir has worked out as expected and as hoped for, with the much larger group continuing to perform well.

I’ve long been a fan of this one, due to the high-returning franchise model.

The merger does affect these ROE calculations. I calculate 2025 ROE as 12.7%, which is still good, but technically TPFG did earn higher ROE in the past as a standalone entity, before the all-share merger.

But the enlarged, diversified group is an attractive investment idea, in my book.

I was moderately positive on TPFG in December, noting that top line growth was modest and the PEG ratio was 1.5x (i.e. it was expensively priced against forecast growth).

The PEG ratio has gotten worse since then, but that doesn’t take into account the latest forecast changes.

I think I’m going to stick my neck out and upgrade this to GREEN on the basis that 1) the market cap is lower than it was the last time I checked, and 2) the profit outlook has improved.

The P/E multiple on 2026 earnings is currently 10.3x. Not a bad entry point, perhaps, for those of who are long-term fans of the business?

3-year chart:

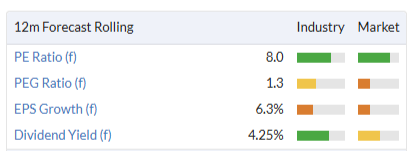

Mortgage Advice Bureau (Holdings) (LON:MAB1)

Up 9% to 592p (£343m) - Final Results - Graham - GREEN =

Mortgage Advice Bureau (Holdings) plc (AIM: MAB1), a leading technology-driven UK property finance service, is pleased to announce its final results for the year ended 31 December 2025.

This is another business with a “franchise” model.

It has been a fixture on my annual watchlist, and thankfully the business is doing well.

2025 highlights:

Revenue +19.6%

Adj. PBT +13.3% (£36.3m)

Adjusted diluted EPS +13.5%

EPS minus 5.8%

And an important line:

2026 has started with good momentum, and the Group continues to trade in line with the Board's expectations

The first and last lines of the CEO comment:

"2025 was another year of strong performance for MAB, keeping us firmly on track to deliver our five-year growth plan.

In my view, MAB has become uniquely positioned in the intermediary and mortgage sectors as a result of executing a very deliberate strategy to build a specialist network with customer acquisition at the heart of the model….

Through continued organic growth, disciplined acquisitions and the increasing use of technology, data and AI, we believe MAB is well positioned not just to participate in the mortgage market, but to shape where it goes next."

Market trends

A big reason I’ve stayed positive on MAB1 for several years is that I’ve been waiting for the business to show what it can do in a booming mortgage market.

While 2025 was perhaps not “booming”, it did enjoy a significant strengthening against the prior year.

From the CEO overview today, some observations on the mortgage market:

Total lending up 19%

Refinancing lending up 17%

Purchase lending up 21%

2024 was really quite weak in hindsight. And I’m inclined to think that the mortgage market can continue to expand in 2026, as rates continue their gradual downward path.

While the volatile situation in the Middle East could yet influence matters, at the moment all of these forecasts are plausible:

UK Finance forecasts modest 3% growth in total mortgage lending in 2026, comprising purchase growth of 2%, remortgage growth of 7% and Product Transfer growth of 2%. IMLA adopts a more optimistic view, forecasting total lending growth of 8% in 2026, with purchase and remortgage activity each increasing by 11% and Product Transfers by 4%.

MAB1’s medium-term targets

This is what the company is working towards:

The Board's medium-term targets, announced in 2025 and presented at our Capital Markets Day, comprise:

· Doubling revenue from 2024 levels

· Adjusted PBT margin of greater than 15%

· Adjusted cash conversion of greater than 100%

· Doubling market share in new mortgage lending

2025 didn’t see any progress in PBT margin or market share of new mortgage lending, but it did see good revenue growth and excellent cash conversion. So it’s a bit of a mixed bag when it comes to progress against these targets.

I don’t see any harm in management working towards these targets, even if they ultimately fall short of them.

Balance sheet: there’s no tangible asset backing here, I’m afraid.

Graham’s view

I see little reason to change my positive view as expressed in January. It’s a quality business and it’s not too expensive here, in my view. The share price has been discounted since January.

Of course if we are being far too optimistic on the outlook for the mortgage market, then this is going to be a bad call.

Roland's Section

Zotefoams (LON:ZTF)

Up 3.5% at 388p (£191m) - Preliminary Results - Roland - AMBER/GREEN =

Today’s full year results from this “world leader in high-performance foams” look healthy to me, with pre-tax profit in line with broker estimates.

I’ve been positive on this business for a while, noting how the changes put in place by CEO Ronan Cox are leading to improved profitability and a stronger commercial focus. Today’s figures confirm this process remains underway, with improved margins and returns on capital:

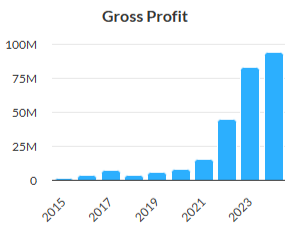

Revenue up 7.2% to £158.2m

Gross profit up 14.8% to £52.9m

Gross margin up 2% to 33%

Adjusted operating margin up 2.2% to 14.4%

Adjusted pre-tax profit up 39% to £21.2m (in line with consensus)

Adjusted EPS up 46% to 38.0p (vs consensus of 32p)

Return on capital employed up 2.2% to 13.9%

EPS beat? Today’s adjusted EPS figure is comfortably ahead of forecasts, but this seems to be due mainly to the recognition of deferred tax assets during the year. This also explains why pre-tax profit is in line, so I would be inclined to see underlying business performance here as in line with expectations.

Clean profits: I don’t have any major concerns about the adjustments used here – the difference between reported and adjusted figures was fairly small this year. The main difference was that reported figures last year were hit by £15m of closure costs for the MuCell (ReZorce) packaging business. This is now in the rear-view mirror and I would say today’s accounts are quite clean.

Cash flow & Balance sheet: net debt rose by 31% to £31.5m last year on a covenant basis, putting a slight dent in my thesis about debt reduction.

However, a closer look shows that this was due to the financing of the acquisition of Overseas Konstellation Company S.A. (OKC) in November for €36m, including €27.6m of cash upfront.

Stripping out this deal, my sums suggest that Zotefoams converted net profit of £22.6m into free cash flow of £19.2m last year – a respectable performance.

In this context, I don’t have any concerns about debt levels or leverage here.

Trading commentary: this is where it gets a little more interesting (my bold):

This performance was underpinned by robust demand across key end‑markets, most notably the continued strength of our Consumer & Lifestyle activities, particularly athletic footwear, alongside solid progress in Transport & Smart Technologies.

Consumer & Lifestyle + Nike: frustratingly, Zotefoams has switched its segmental reporting to provide a geographic split, rather than reporting by business unit.

Today’s results do include a very minimal reporting by vertical:

Sadly, the company no longer seems to disclose how much revenue is coming from its largest single customer (Nike). This disclosure was included in the 2025 interim results, but seems to have been removed from today’s full-year results. This is poor practice in my opinion, given how material this customer is to the profitability of the group.

Based on the commentary today, it seems reasonable to assume a similar contribution from Nike in H2, so I would guess this customer may have generated around half of Zotefoams’ revenue last year, or c.£75m.

It’s worth remembering that while this level of concentration is a risk, it’s also an opportunity. I believe the company’s current exclusive contract with Nike runs to 2029. Lower production costs from Zotefoams’ new facilities in Vietnam may mean that its high-performance foams can be used in cheaper shoes than previously, creating an opportunity for volume growth.

Transport Smart Technologies: growth in North America was said to be driven by “strong growth” in this business, with “robust orders in automotive and transit applications” plus some improvement in construction demand towards the end of the year.

Outlook

I have to admit that in my view, today’s outlook statement leaves some scope for interpretation.

On the face of it, guidance from CEO Ronan Cox is in line with expectations:

We have entered 2026 with good momentum. Trading in the early part of the year has been in line with our expectations, supported by continued demand in Transport & Smart Technologies and improving order books across several markets.

However, there’s also a more ambiguous statement on demand from Consumer & Lifestyle customers:

As anticipated, demand patterns across our markets are becoming more balanced following a period of exceptional growth in Consumer & Lifestyle. In footwear, we expect volumes to moderate from the unusually high levels experienced in 2024 and 2025 as customers normalise inventory positions which is an expected transition, and our operating plans reflect this shift.

Finally, Mr Cox ends with a comment that “medium term prospects are in line with our stated ambitions”. As Mark has observed in the past, a focus on the medium-term outlook can sometimes mean the near-term outlook is less certain.

I don’t have access to any updated broker forecasts yet, but the benign share price reaction today suggests to me that brokers covering Zotefoams have left FY26 forecasts unchanged. According to the StockReport, this suggests a more moderate rate of growth this year when

FY25 actual adj EPS: 38.0p

FY26E adj EPS: 39.5p

To remove the distortion caused by last year’s tax situation, I think it’s also useful to compare forecast revenue and pre-tax profit for FY26 – these estimates are courtesy of Singer Capital’s February note:

2025 actual | 2026E | |

Revenue | £158.5 | £191.4m (+21% vs FY25) |

Adjusted pre-tax profit | £21.2m | £27.2m (+28% vs FY25) |

The underlying thesis is that growth in other parts of the business, such as transportation, will offset any softness in consumer footwear. The higher growth rate for profit vs revenue tells me Singer’s analysts expect a further improvement in operating margins in 2026.

These 2026 forecasts leave Zotefoams trading on around 10x FY26 forecast earnings, with a 2% dividend yield.

Roland’s view

Improving profitability and strong cash generation paint a healthy picture here. I only really have two niggles:

I think it’s fair to apply a cautious earnings multiple to any business that may be depending on a single customer for half its sales.

I think there’s still some risk that normalised volumes in footwear could hit overall performance this year.

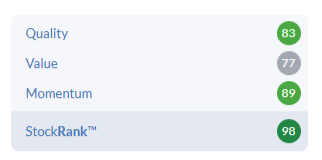

Despite this, I’m impressed by progress since the current CEO took charge and am comfortable maintaining my AMBER/GREEN view today, in line with the stock’s High Flyer styling and strong StockRank:

Yu (LON:YU.)

Down 4% at 1,706p (£288m) - Final Results for the year ended 31 December 2025 - Roland - AMBER/GREEN =

Yü Group PLC (AIM; YU.), the independent supplier of gas and electricity, and meter asset owner and installer of smart meters, to the UK corporate sector announces its final audited results for the year to 31 December 2025.

This small-cap utility business has been a three-bagger over the last three years – but after a rapid run up, these highly-ranked shares have remained rangebound over the last two years.

Today’s results have prompted broker upgrades but have seen the share price fall. Is this picture about to change?

2025 results highlights

If I was feeling picky, I might observe that Yu’s management has chosen to use a slightly confusing mix of percentage changes and absolute changes when reporting its financial and operating metrics. This makes rapid comparisons of growth rates more difficult.

To improve clarity, I have only used percentages in the list below:

Revenue up 8% to £700m

Gross profit up 7% to £100m

Adj EBITDA up 4% to £51m

Pre-tax profit up 9% to £49m

Adjusted earnings up 3% to 216p

Dividend up 12% to 67p per share, giving a 4% yield

Net cash up 19% to £95.6m

Despite my nitpicking, I don’t think there’s much to dislike here. Revenue growth in this business is influenced by commodity prices, but the group’s operating margin was stable at 6% last year, while return on capital employed remained stable (and impressive) at 41%.

One point worth noting was that more stable energy markets (until recently) resulted in more competitive energy pricing in 2025. As a result, Yu’s gross margin fell by 1% to 14% last year. I imagine there’s a chance this could reverse if Yu is large and skilled enough to successfully handle the current volatility in energy markets.

Operational growth also remained strong, with good progress on of the key metrics reported by the company:

Meter points supplied up 49% to 131k

Equivalent volume of energy supplied up 14% to 2.5TWh

Market share up 0.8% to 3.5%

Contracted revenue for 2026 up 18% to £668m

Bad debt charge of 2.6% (2024: 2.1%)

Smart meter recurring revenue up 69% to £2.2m

These metrics seem to suggest that the company has added a larger number of smaller companies over the last year, with the number of meter points supplied rising much more quickly than total energy supplied.

One point worth noting is an increase in the bad debt charge to 2.6%, partially reversing the decline from 3.1% to 2.1% seen in 2024..

While this level of bad debt still looks manageable to me, Yu relies on large revenues to generate relatively low margins. This means that any increase in bad debt can have a significant impact on profit.

Looking at 2025 as an example, each 0.1% increase in bad debt as a proportion of revenue corresponded to around 1.4% of pre-tax profit (around £700k).

An increase in bad debt is unsurprising given the wider cost challenges facing some business sectors. However, I think bad debt rates remain a key risk to watch for as the company pursues continued growth. Any decline in the underlying credit quality of customers could become a serious concern if unchecked.

This could become a more serious risk if energy prices remain high. Business customers do not benefit from regulatory energy price caps, so those without fixed rates could soon start struggling with higher energy prices if the current situation in the Middle East doesn’t ease.

Market share opportunity: Yu says it acquired 11% of market switchers in the B2B market last year (2024: 7%), helping to lift market share in the B2B market to 3.5%.

Founder and CEO Bobby Kalar says that the addressable market for the company is 3.6m meter points, suggesting there’s still plenty of scope for growth.

Contracted revenue for the year ahead represents around 75% of revised revenue forecasts for 2026. This compares to a figure of around 80% one year ago, but visibility still seems good to me, given that some customers do not choose to contract their supply (i.e. fix prices) and pay variable rates instead.

Pleasingly, the company was recognised for the third consecutive year in the Sunday Times Top 100 Places to Work. While this isn’t a guarantee of a good investment, I think the odds of a good result are probably improved in businesses that treat their employees fairly.

UAE office: perhaps a little surprisingly, Yu’s CEO has also decided to spend more time in the UAE at the company’s newly opened offshore IT base:

[...] while we have achieved success domestically, I am pleased to have established a subsidiary 'hub of talent' and office presence in the UAE

Our UAE office represents an exciting new opportunity for us to deliver operational improvements and efficiencies through the development of robotic technology and AI automation that will accelerate our growth ambitions while positioning ourselves as the tech outlier and disruptor in the B2B energy space.

I am personally leading this strategy and, as such, I am spending more time in the UAE supported by my fantastic UK team, and I look forward to updating you on progress in due course.

Even without a Middle East war, I’m not sure I’d be encouraged by the news that the CEO is spending “more time in the UAE”.

I am not an expert on this sector, but I would have thought a more logical choice for an offshore IT base might be Eastern Europe or India. I am not sure I’d expect the development of such an office to be led on the ground by the CEO, either.

Outlook & New 3yr Strategy

So why are Yu shares falling today? It doesn’t seem to be due to today’s in-line results or to the valuation, which remains reasonable:

I suspect that one of the main reasons why the shares are down this morning is that Yu has launched an ambitious new three-year plan to double its market share:

“2026 kicks off the three-year plan to deliver at least 7% market share”.

A “self-funded incremental £9m+ planned opex investment” is planned for 2026 to “grasp the market opportunity”.

Yu’s operating costs were £37m last year, so a £9m increase represents a c.25% increase – a big commitment to growth. If the company doesn’t generate a commensurate increase in revenue and profit, then profits could fall in the short term as the company’s growth gears up.

Broker forecasts: two broker notes are available on Research Tree today offering revised forecasts in the light of today’s new growth plan.

The analysts’ revised revenue figures cover quite a wide range, but the expected direction of travel for earnings is quite clear:

Panmure Liberum: FY26E adj EPS: 215.1p (-5.7% vs 228.1p previously)

SP Angel FY26E adj EPS: 219.2p (-2% vs 223.6p previously)

The consensus estimate for 2026 earnings on the StockReport prior to today was 223p per share, so I suspect we’ll see this figure edge lower in the coming days.

Even so, these revised forecasts still leave Yu priced on a modest 8x forecast earnings – and both brokers expect a return to earnings growth from FY27.

Roland’s view

Today’s results look quite strong to me. Yu is continuing to expand and gain market share while maintaining a good level of profitability. Although bad debt charges rose last year, they remain within the group’s historical range and look manageable enough to me.

Whether now is a good time to launch an expensive new growth plan will remain to be seen. I wouldn’t rule out further success given the company’s track record:

However, such a large increase in spending is not without risk and I am slightly disconcerted by the CEO’s new enthusiasm for running a UK energy supplier while in the Middle East.

This isn’t enough to dent my broadly positive view on Yu, though, especially as Kalar continues to own more than 50% from Yu stock. He has a lot of skin in the game and I find it hard to imagine him abandoning the disciplined growth that’s brought the business this far.

The StockRanks remain positive about this business, with Super Stock styling.

More prosaically, a 4%+ dividend yield that’s covered three times by earnings suggests to me that the valuation remains reasonable and that the stock could have attractive income potential.

I’m leaving my previous AMBER/GREEN view unchanged today.

See what our investor community has to say

Enjoying the free article? Unlock access to all subscriber comments and dive deeper into discussions from our experienced community of private investors. Don't miss out on valuable insights. Start your free trial today!

Start your free trialWe require a payment card to verify your account, but you can cancel anytime with a single click and won’t be charged.