Morning!

The FTSE finished down by 1.2% yesterday as the conflict continued to develop across the Middle East. It closed at 10,780.

This morning, as of 7am, futures are trading as follows:

- FTSE futures down 0.6% at 10,680 (update at 8.20am: now down 1.4% at 10,600).

- S&P 500 futures down 0.9%

- US crude oil up another dollar at $73

- GBP/USD closed at 134.8 on Friday before the conflict began, and is currently at 133.5.

Market update

11.30am update: the FTSE has continued to slip and is now down by 2.5%. A day for those with strong constitutions!

On a day like today, I always zoom out and remind myself of the bigger picture. Year-to-date, the FTSE is still up by over 5%. So I am still very much of the view that this is a "blip" from a long-term perspective, although of course all bets are off if military activity becomes more intense and drags in more participants.

The key for investors is always to find a strategy that aligns with your risk appetite (and other personal constraints). I tend to be fully invested, although as it happens I do have some dry powder at the moment. And I'm in no rush to spend it! When markets are scared, having even a small amount of dry powder can be a source of comfort - in my case, I might set some targets below the market where I will pick up shares, if sentiment continues to weaken.

Today's report is complete. Spreadsheet accompanying this report: link.

Companies Reporting

| Name (Mkt Cap) | RNS | Summary | Our View (Author) |

|---|---|---|---|

Smiths (LON:SMIN) (£8.5bn | SR70) | Smiths has agreed to acquire DRC Heat Transfer for £164m (10x adjusted EBITDA for the calendar year 2025). DRC revenues were £73m in calendar year 2025. | ||

Fresnillo (LON:FRES) (£30bn | SR80) | 27.6% increase in Adjusted Revenues to US$4.6 billion, 80.7% rise in EBITDA to US$2.8 billion. Outlook: silver production 42.0 to 46.5 moz, gold production 500 to 550 koz | ||

Intertek (LON:ITRK) (£7.3bn | SR69) | SP -15% Revenue +4.3%, adjusted operating profit +9.3% (cc), +5% (actual FX). Outlook: mid-single digit LFL revenue growth, margin progression, strong earnings growth and strong free cash flow. Reiterates medium term targets. | AMBER = (Roland - I hold) [no section below] Results from this quality assurance provider have fallen flat with investors today. One factor identified in newswire commentary is that like-for-like growth of 3.9% was below expectations of 4.4%. Looking closer, it seems that last year’s results were supported by its largest and highest-margin business, Consumer Products. This earned a 30% operating margin on sales of £983m and contributed almost half the group’s profits. Performance elsewhere was less inspiring, with profits falling in three of the remaining four divisions. The worst performer by far was Energy, where a 1.3% decline in LFL sales resulted in a 15% drop in operating profit. This division has significant exposure to the automotive sector and my impression is that this was the main issue, with “a temporary reduction of investments by some clients” as they respond to “a more challenging trading environment”. Overall quality metrics remained strong last year, with an operating margin of 15.8% (FY24: 15.7%) and a return on capital employed of 20.2% (FY24: 20.9%). I continue to see this as a high quality business with strong long-term prospects, but weakness in some markets is holding back overall results and near-term growth prospects seem relatively modest. I’m going to retain our neutral view today to reflect these concerns, but I intend to continue holding and might consider topping up if prices continue to fall. | |

IG group (LON:IGG) (£4.5bn | SR91) | Former Chief Operating Officer of Virgin Media is appointed Board Chair Designate. | ||

Aberdeen (LON:ABDN) (£4.1bn | SR89) | Adjusted operating profit +4%, AUMA +9%, net flows minus £3.9bn. “We have entered 2026 with momentum and remain firmly focused on delivering our 2026 Group targets.” | AMBER/GREEN ↓ (Graham) The shares are now trading at around 14x forecast earnings and I'm inclined to think that they are fairly valued here. This is unfortunately the rather boring result that we can often get when we look at larger companies. But not always: at 11x earnings last year, I was willing to stick my neck out and suggest that the stock was undervalued. At the current valuation, considering the persistent flow weakness in the Adviser business and the fairly average flow performance overall, I think it makes sense to moderate my stance and go back to AMBER/GREEN. Interactive Investor is now standing out clearly as the most profitable and highest-quality division. | |

RS (LON:RS1) (£3.3bn | SR90) | Acquires BPX Group, a UK and Ireland-based specialist distributor of industrial automation and control, for £27m plus £3m earn-out. | ||

Inchcape (LON:INCH) (£3.1bn | SR97) | Volumes +3%, 1% organic revenue growth. Adjusted PBT +3% at constant FX. Outlook: organic volume growth towards lower end of 3% - 5% medium-term guidance range, with H2-weighting. | ||

RIT Capital Partners (LON:RCP) (£3.0bn | SR N/A) | 13.5% NAV per share total return for the year, 16.9% share price return. Share price discount to NAV of -22.3% at 31 December 2025. | ||

International Workplace (LON:IWG) (£2.1bn | SR38) | Revenue +4%, adjusted EBITDA +6%, operating profit +0.7% ($143m). 2026 has started as expected. Pricing and revenue trends are positive; revenue growth expected to be at least 4%, as previously communicated. | ||

Greggs (LON:GRG) (£1.61bn | SR63) | Sales +6.8%, underlying PBT down 9.4%. Outlook: Full year guidance unchanged. Profits to be “at a similar underlying level to 2025, with any year-on-year improvement contingent on a recovery in the consumer backdrop”. | AMBER = (Roland) [no section below] Today’s results are in line with expectations and leave guidance for the year ahead unchanged. I think this is a solid performance in the circumstances. However, profitability has come under pressure from rising costs and softer consumer spending. Operating margin dropped to 8.6% in 2025, while ROCE fell to 16.2%. The equivalent figures in 2024 were 10.4% and 20.7%. Management notes that restoring ROCE to its target level of 20% is a key focus. Fortunately, my impression is that spending on growth remains disciplined and logical, with capex now having peaked. The shares also look reasonably priced at current levels, with a P/E of 12 and forecast dividend yield of 4.3%. The only catch is that earnings are expected to be flat this year, with only a modest return to growth in 2027. As Graham commented in October, there’s clearly a risk this business has gone ex-growth. With a flat outlook for the year ahead and customer base whose spending power is constrained, I think the valuation may be fair. I’m going to retain our neutral view for a little longer. | |

Keller (LON:KLR) (£1.40bn | SR93) | Revenue +3.4%, underlying operating profit +2.6% (£218.2m). “The Group enters the new financial year with a high quality order book, healthy tendering activity, strong balance sheet and a clear strategic direction.” | AMBER/GREEN = (Roland) A strong set of results and strengthened balance sheet are used to justify a more generous dividend policy, a new buyback and potential M&A. The new CEO appears quite relaxed about moving the business back into a net debt position and is confident the group’s improved operational performance and profitability are sustainable. I also have a positive view on the long-term outlook for this global market leader, but I would note that the order book is slightly lower than one year ago. My analysis also suggests that underlying growth – excluding some one-time benefits – was minimal last year. On balance, I think this is a good business in good health, but the shares aren’t as cheap as they were and I think it’s reasonable to assume that cyclical headwinds and project losses have the potential to recur in the future. I’m leaving my previous broadly positive view unchanged today. | |

| Kier (LON:KIE) (£1.04bn | SR92) | Results for the period ended 31 December 2025 | Revenue +2.6%, adjusted operating profit +6.6%. Order book +5% to £11.6bn, reflecting ”customers' continued confidence in the Group's breadth of chosen, robust, sectors, as well as its ability to pivot to new areas”. 94% of FY26 revenue and 78% of FY27 revenue secured. | |

Morgan Advanced Materials (LON:MGAM) (£646m | SR72) | Adjusted revenue down 3.3% (organic, constant currency basis). Adjusted operating profit down 18% (£99m). Actual operating profit down 54% (£45m). “A resilient performance against a backdrop of challenging markets.” Outlook: “Demand in our end-markets has broadly stabilised and our outlook for 2026 is in-line with current market expectations.” | ||

Johnson Service (LON:JSG) (£544m | SR55) | Revenue +4.3%, adjusted operating profit +16% (£72.5m). Outlook: “Notwithstanding the current economic uncertainty, particularly the impact of significantly increased labour and premises costs on some of our end customers, the Board expects to deliver another year of growth.” | ||

Central Asia Metals (LON:CAML) (£427m | SR97) | Mineral Resource at 31 December 2025 estimated at 20.5 million tonnes at an average grade of 2.2% zinc and 3.9% lead. Revised mine life, along with other assumptions, is expected to result in an impairment charge of up to $120 million to the carrying value of Sasa. No change to dividend policy. “Does not in any way affect the Group’s cash generation”. | BLACK? | |

Custodian Property Income Reit (LON:CREI) (£423m | SR72) | Strategic Majority-Share Acquisition of £8.5m Family Property Portfolio | Purchases Scorpion Properties Limited for £8.5m. “Another highly complementary portfolio which comprises five single-let industrial properties with 100% occupancy.” | |

Origin Enterprises (LON:OGN) (£397m | SR99) | H1 revenue up 5.1% to €852.6m, with underlying volume growth of 1.4%. Op profit up 2.4% to €17.4m. Expect H2 weighted profit, as in previous years. Outlook: will issue FY26 guidance in June as significant levels of spring volumes are still to be delivered. | ||

NCC (LON:NCC) (£388m | SR55) | Sale of Escode business for £309m remains on track with completion expected “no earlier” than 30 April 2026. FY26 adj EBITDA is expected to be in line with expectations. | ||

Mears (LON:MER) (£293m | SR90) | Sale of Morrison Facilities Services Limited for £18.0m in cash. This business was focused on healthcare and education and generated a pre-tax profit of £2.8m in 2025. | ||

Reach (LON:RCH) (£219m | SR78) | SP -12%, market cap £189m Revenue down 3.7% to £518.4m, adj operating profit up 2.4% to £104.7m. Adj EPS up 5.9% to 26.8p. 2026 outlook: on track to meet expectations. | AMBER ↓ (Graham) Despite the large drop in the share price today, this is still trading around the level it was trading at in January when I expressed a fully positive view on it (though it looks like I left us officially on AMBER/GREEN, as my co-writers have been more sceptical of it). Today's full-year results confirm a modest revenue decline, as expected, and adjusted operating profits have held up very well at £104.7m. This is badly soured, however, by a statutory operating loss of £160m, as the company took a £223m impairment charge. I always think it's bad news when losses or impairment charges exceed a company's market cap, and that is the case here. The impairment has been applied broadly to "goodwill, publishing rights and titles, internally generated intangibles, property, plant and equipment and right-of-use assets". Balance sheet equity reduces from £637m to £526m, and tangible equity remains negative (£526m of total equity with £679m of intangibles). It's not all bad news: the pension deficit appears to be under control, with £57m of contributions expected in 2026, and the funding deficit in the schemes expected to be removed by 2028, as before. While I don't think all that much has changed here - and importantly, the outlook statement for 2026 is in line - I must acknowledge that the massive impairment charge for 2025 does concern me. I need to put greater importance on the fact that the balance sheet has negative tangible equity, and allow for a higher probability of future impairments, which could send it further into negative equity. On that basis I'll retreat to a neutral stance here for the time being. At a P/E multiple of 3x the risks might be priced in. But in my experience, it's right to be cautious on stocks where annual losses and/or impairment charges are as large as the market cap. | |

EKF Diagnostics Holdings (LON:EKF) (£111m | SR76) | 3yr purchasing agreement with Blood Centers of America to provide pricing for the DiaSpect hand-held hemaglobin analyzer and associated consumables and software. | ||

Shield Therapeutics (LON:STX) (£104m | SR36) | ACCRUFeR has been accepted in China for the treatment of adults with iron deficiency following a successful Phase 3 trial. | ||

Gaming Realms (LON:GMR) (£92m | SR42) | Current £6m buyback nearly complete, has been extended by a further £5m to reflect net cash position of £16m. Due to poor liquidity, has agreed with broker that buybacks will be allowed to exceed 25% of average daily volume, while remaining below 50%. | ||

Kodal Minerals (LON:KOD) (£85m | SR33) | Started arbitration proceedings relating to a claim by Kodal Mining UK Limited (in which Kodal is a 49% shareholder) for indemnification in respect of a US$15m payment made to the Government of Mali. | ||

Aurrigo International (LON:AURR) (£78m | SR36) | Aurrigo has obtained the licence to support its partners in the roll-out and implementation of its autonomous technologies to support the deployment of autonomous ground service equipment at East Midlands Airport. | ||

PCI- PAL (LON:PCIP) (£41m | SR47) | H1 revenue +7% to £11.3m, ARR +21% to £20.3m. Adj EBITDA -79% to £0.2m reflecting “increased investment being made in line with the strategy outlined in July 2025”. Outlook: strong momentum continued into H2. | ||

Synectics (LON:SNX) (£40m | SR80) | FY25 revenue +22% to £68.1m, adj EPS +29% to 28.0p (ahead of exps). FY26 outlook: revenue expected to be 10% below FY25 levels with mid-single digit EBITDA margins (vs. 12.5% in FY25). Expect a return to double-digit growth in FY27. | BLACK (AMBER/RED ↓) (Roland) Last year’s performance was strong, but it seems much of this was driven by a large (£12m) one-off contract in Asia. The company seems to have little confidence in being able to replace this in FY26 or even FY27. My sums suggest adjusted earnings could fall by 50%+ this year as the business retrenches and CEO Amanda Larnder focuses on modernising its products and delivery and improving sales and marketing processes. Although the £14m net cash position provides a robust safety net, my sums suggest a cash-adjusted FY26E P/E of 10. That seems high enough to me at this point, given the group’s modest profitability and cautious outlook. I think it’s fair to take a moderately-negative view until there’s some evidence of a return to growth. | |

Headlam (LON:HEAD) (£34m | SR34) | Rob Barclay appointed CEO Designate from 9 March and will assume the role on 27 April when the interim exec chair will return to a non-executive role. Richard Jones will join as Interim CFO from 12 March and will join the board in due course. | ||

Cyanconnode Holdings (LON:CYAN) (£29m | SR12) | Received a further non-binding proposal from Esyasoft for a possible all-cash offer of £37.5m (10.44p per share). This represents a 44% premium to the last undisturbed price of 7.25p on 2 Feb 26. This offer is at a level the Board would recommend to shareholders. | PINK | |

Insig Ai (LON:INSG) (£19m | SR1) | New contract with existing client to use Insig AI’s Generative Intelligence Engine. Purchased enterprise licence for £60k and entered into revenue share agreement. Client will also provide Insig AI with access to its own client base for direct sales. |

Graham's Section

Aberdeen (LON:ABDN)

Down 8% to 204.4p (£3.8bn) - Final Results - Graham - AMBER/GREEN ↓

There has been a sharp fall in the Aberdeen share price this morning, not helped by a >2% fall in the FTSE.

Aberdeen itself has not been in the FTSE 100 index since 2023, but I think it should have a strong chance of readmission to the flagship index at the next revision.

Today’s headlines are positive:

Very strong performance in interactive investor as we build the UK's leading Wealth & Investments group

Transformation savings target exceeded, delivering a simpler, more efficient business

Committed to Group FY 2026 targets, with clear opportunities to drive sustainable, profitable growth

And the headline financial KPIs are fine, with modest growth in the adjusted profit measures:

Net flows

Due to Aberdeen’s size and complexity, net flows are a little trickier to understand as compared with other fund managers.

I think the correct overall number to focus on is net flows excluding liquidity, which excludes the flow of client cash and cash equivalents. This will be short-term, low-margin business.

Overall net outflows for the year were £3.9bn (previous year: outflow of £1.1bn).

Excluding liquidity movements, however, there has been a year-on-year improvement: net outflows are only £1.7bn (previous year: £6.1bn outflow).

In the context of total AUMA of £556bn, these net outflow figures do not seem terribly concerning at first glance.

But let’s now drill into Aberdeen’s three major divisions: Interactive iInvestor, “Advisor”, and “Investments”.

interactive investor (ii)

This is probably the highest-quality division at Aberdeen: a visible consumer brand supported by predictable, recurring revenues. Results here are excellent:

Net operating revenue +19% (within this, trading revenue grew by a remarkable 44%).

Adjusted operating profit +34% to £155m.

Net inflows £7.3bn, and AUMA up by 26% to £97.5bn. Gross inflows were nearly double the value of gross outflows (“redemptions”).

ii has generated over 50% of the group’s total adjusted operating profit for 2025 (£155m out of £305m total, before central costs).

Advisor division

The IFA-facing division had a less profitable year, due to “previously announced strategic repricing”.

Net operating revenue fell 13.5% to £205m, and expenses rose by £8m to £119m. The result: adjusted operating profit was squeezed by 32% to just £86m (previous year: £126m).

Net flows were minus £2.2bn but positive market movements allowed AUMU to rise by £5bn to £80bn.

Objectively it’s a poor year-on-year progression, but it’s framed as being strategically necessary.

There is also what amounts to a profit warning in here:

Revenue in FY 2026 to reflect strategic repricing, with total revenue margin forecast to be 25-26bps. Expenses also expected to reflect end of third-party outsourcing discount.

While we have made good progress in turning around our flows, we now expect to return to positive net flows in 2026, with £1bn net inflow target to be delivered in 2027.

This £1bn net inflow target was originally supposed to be delivered in 2026, and has therefore been pushed back by a year. The target for the current year is now simply to get back to some degree of positivity.

Investments division

This is the conventional fund management division that we can compare with other listed fund managers.

Excluding “liquidity” (cash outflows of £2.1bn), the “Institutional & Retail Wealth” arm of this division achieved net inflows of £0.1bn, which I view as a solid result in the circumstances. I do not expect to see inflows at mainstream fund managers these days. In that context, a breakeven result is perfectly acceptable.

The other arm of this division, “Insurance Partners”, saw net outflows of nearly £7bn (again, excluding liquidity).

All told, therefore, the Investment Division saw net outflows of nearly £7bn excluding liquidity.

Including liquidity, net outflows were even higher at £9bn.

But a rising financial tide lifts all boats, and AUM rose by £20bn despite these outflows, to £390bn.

As for profitability:

Operating revenue down 7% (“impacted by changes in asset mix”)

Operating profit up 5% (“with focus on operational efficiency, partly offset by lower revenue”).

In the end, adjusted operating profit rose by £3m to £64m. This remains the least profitable division within Aberdeen, but it is still more profitable in its own right than many other fund managers we cover in this report.

Outlook

Despite the warning re: inflows in the Advisor division, they remain confident in their existing FY26 targets and in the outlook for the years ahead:

We are confident in the outlook for the business and in the FY 2026 Group targets of adjusted operating profit of at least £300m and net capital generation of c.£300m.

Once our net capital generation target has been met, we are targeting net capital generation to grow on average 5-10% per annum over the medium term, absent any major market irregularities.

CEO comment: after describing the overall group as being “in much better shape” compared to last year, and seeing “significant opportunities for future growth” in iInteractive iInvestor, he acknowledges the challenge in the Adviser business:

"As expected, last year's strategic repricing impacted profitability in Adviser. However, we have made progress, with net outflows almost halving year on year, and improved client service. We still have more to do, and our focus remains on returning to growth as quickly as possible….

"We have entered 2026 with momentum and remain firmly focused on delivering our 2026 Group targets and sustainable growth beyond this."

Graham’s view

I’ve been quite positive on this one, giving it a GREEN in October and before that in April last year.

That doesn’t look very clever on a day when the share price falls 8%+, but I originally gave it the green light when the share price was 148p and the P/E multiple was 12x, which I think looks reasonable in hindsight.

The difficulty now is that the valuation demands a little more from the company:

One way to approach it might be to think in terms of each division’s share of profits: iInteractive iInvestor is responsible for 51%, Advisor for 28%, and Investments for 21%.

For example, we could value interactive investor at 16x earnings (comparable to AJ Bell (LON:AJB)), Advisor at 12x (an average multiple to reflect the delay in achieving its net inflow target) and the Investments division also at 12x (more expensive than POLR, less expensive than JUP). You can fill in your own numbers with whatever you think is appropriate.

Blending these sample P/E multiples together, I end up with a group P/E multiple for Aberdeen of 14x.

I didn’t know this would happen in advance, but when I plug in today’s ABDN share price vs. the 2026 EPS forecast for the company, I get a forward P/E multiple of 14x, suggesting in other words that the shares are now fairly valued.

This is unfortunately the rather boring result that we can often get when we look at larger companies. But not always: at 11x earnings last year, I was willing to stick my neck out and suggest that the stock was undervalued.

At 14x earnings today, I think it makes sense to moderate my stance and go back to AMBER/GREEN.

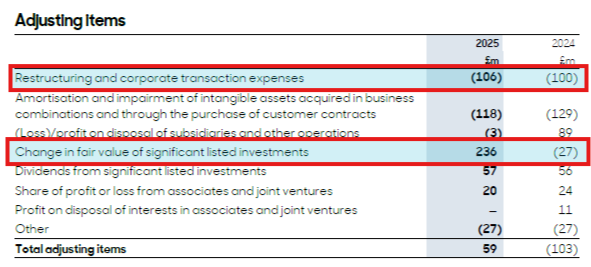

Before closing, I should also mention that today’s strong PBT numbers (£442m of statutory pre-tax profit) mask some very large restructuring charges that the company took.

Aberdeen has been taking very large “restructuring and corporate transaction expenses” each year. But this year, that was more than fully offset by gains from their shareholding in Standard Life, recorded as “change in fair value of significant listed investments”:

The net result is that PBT looks very strong for 2025, but I’m not entirely satisfied with how this was achieved - the results are far from what I’d consider “clean”.

Which only makes the downgrade to AMBER/GREEN all the more justified.

Roland's Section

Synectics (LON:SNX)

Down 15.6% at 188p (£33m) - Final Results and Strategic Update - Roland - BLACK (AMBER/RED ↓)

Synectics plc (AIM: SNX), a leader in advanced security and surveillance solutions, announces its audited final results for the year ended 30 November 2025 ("FY25").

When I saw that the title of this morning’s results included the words “Strategic Update”, I had a bad feeling. Sure enough, today’s results include a warning that revenue and profit will fall sharply in 2026 before (hopefully) rebounding from FY27 onwards.

Synectics’ share price has been trending lower for a full year now, so this appears to be a situation where the market has been anticipating a poor outlook. I’m happy to see that I downgraded my view to neutral in December after the company’s full-year update seemed to strike a mixed note.

Let’s take a look at the main points from today’s update.

FY25 results summary

The headline numbers for the year ended 30 November 2025 look pretty positive:

Revenue up 22% to £68.1m

Adjusted EBITDA up 36.1% to £8.5m

Operating margin: 7.8% (FY24: 7.6%)

Adjusted earnings per share up 29% to 28.0p

Cash of £14.1m with no bank debt (FY24: £9.6m)

Final dividend of 2.8p per share, giving a total dividend of 5.0p (+11% vs FY24)

Both of Synectics’ divisions appear to have had a good year:

Synectic Systems (revenue up 21% to £41.7m, op profit up 23.5% to £7.2m): trading was boosted by “a significant increase in revenue from the leisure and hospitality sector”, including a non-recurring “significant gaming deployment” in South-East Asia (casino surveillance systems). This contract contributed around £12m of revenue last year.

Ocular (revenue up 24% to £26.4m, op profit up 17% to £1.6m): growth in both on-vehicle and security markets. Following a strategy refresh in the second half of FY24, the focus has been on strengthening marketing and sales performance. This has increased the “qualified opportunity pipeline” by nearly 100%.

Order book: last year’s growth rate is expected to reverse in FY26 as the “significant gaming deployment” drops out of the numbers. The order book for the year ahead is down by more than 30% compared to FY24.

Solid order book at 30 November 2025 of £26.5 million (30 November 2024: £38.5 million). The change in order book from the prior year-end predominantly reflects the completion of a significant gaming contract.

Outlook

Management warns that FY26 will be a “transitional investment year”. Translated, this appears to mean there will be a shortage of new business compared to FY25:

Revenue in FY26 is expected to be around 10% lower than FY25 with growth offset by the absence of the significant one-off gaming contract (loss of £12m of revenues).

Investment to support long-term growth is expected to mean mid-single-digit EBITDA margins. For comparison, EBITDA margin was 12.5% in FY25.

I don’t have access to any updated forecasts for Synectics this morning, but I have used the guidance above to construct some FY26 estimates:

FY26E revenue of c.£61.3m

FY26E adj EBITDA margin of 4%-6%

FY26E adj EBITDA of £2.5-£3.7m (FY25: £8.5m)

Over the last two years, adjusted net profit has been 50%-60% of adjusted EBITDA. Assuming a similar result in FY26, I estimate FY26 adjusted EPS could be 10-11p – about 60% below FY25.

FY27: management strikes a more positive note for FY27, but note that this guidance still excludes the benefit of the non-recurring contract from FY25. This suggests to me that adjusted EBITDA in FY27 could still be significantly below last year’s £8.5m result.:

Double-digit revenue growth is expected in FY27, with EBITDA anticipated to exceed normalised FY25 levels once the impact of the non-recurring contract is excluded.

By FY28, the Group anticipates further acceleration of revenue growth and EBITDA margins as the strategic initiatives implemented in FY25 and FY26 create a robust platform for accelerating returns and sustainable growth

Strategic Update

Last year was CEO Amanda Larnder’s first year in the role. Today’s strategy comments suggest to me she has identified areas of underperformance and inefficiency in the business. Among the areas highlighted for change in FY26 are:

Simplifying the deployment of the Synergy software platform. The average installation time is expected to fall from 20 days to 4.5 days (!), benefiting “both margins and productivity”.

Re-engineering the COEX camera range to deliver “meaningful cost reductions in response to increased competitive pressure” while also updating the core product to support future requirements in the energy market.

Improving go-to-market strategy to develop a broader range of system integrators and technology providers, reducing demand on internal teams.

Improving sales and marketing efforts using data and consistent processes to identify opportunities: “In previous years, our commercial efforts have been too fragmented, with limited use of data, inconsistent sales processes, and underdeveloped customer targeting.”

Roland’s view

From time to time we see small companies that struggle to repeat large one-off contract wins. This sometimes results in disappointing performance for several years after. I don’t know if that will be the case here, but it certainly seems to be a risk.

In today’s guidance, management is already feeling the need to warn that next year’s results will still compare poorly to FY25. This suggests a low level of confidence in the company’s ability to win other large contracts. I’m not sure why this might be, but I would view this as a potential concern.

The strategic plans announced today seem logical enough to me. I would imagine they have the potential to improve margins and returns – a concern I’ve flagged in the past.

However, reading between the lines makes me wonder whether this business had become too complacent and whether some of its technology may have become dated.

For example, if Synectics can cut the deployment time for one of its core products by 75%, what needs to change to achieve this (and why hasn't it happened previously)? A potential saving of 15 days’ labour seems remarkable to me and suggests either great inefficiency or very dated configuration procedures.

In the absence of updated broker forecasts today, I am going to disregard the now-stale FY26 and FY27 estimates in Stockopedia and rely on my own. On this basis, I reckon the shares could be trading on a FY26E P/E of around 17.

However, net cash of £14m represents more than 40% of today’s £33m market cap. Stripping this out gives a cash-adjusted P/E of around 10x.

I can see that there could be some value and turnaround potential here, but I’m discouraged by today’s big downgrade and the changes that appear to be needed to support a return to growth.

In keeping with our normal approach, I’m going to cut my view by one notch to be mildly negative today while we wait for further updates on trading and profitability. AMBER/RED ↓

Keller (LON:KLR)

Up 6.6% at 2,132p (£1.49bn) - Preliminary Results - Roland - AMBER/GREEN =

This market-leading geotechnical contractor specialises in complex groundworks for large projects. Keller is one of the UK market’s few big risers today, up by 9% after a very strong set of results.

It seems this business may be another indirect beneficiary of the AI boom. – Keller shares have doubled over the last two years and management attributes much of today’s results to strong demand in North America from “large infrastructure projects and data centres”, which have helped to offset weakness in US residential markets.

2025 results summary

Revenue up 3.4% to £3,087.3m (+5.9% constant currency)

Underlying pre-tax profit up 3.1% to £197.3m

Reported pre-tax profit up 1.4% to £186.4m

Free cash flow down -8.7% to £175.9m

Underlying earnings up by 5.7% to 211.3p per share (ahead of expectations of 208p)

Full-year dividend up 41.6% to 70.4p per share

Net cash of £59.7m, “for the first time in more than 25 years”

These are clearly good results, showcasing excellent cash conversion and a strengthened balance sheet. My number- crunching suggests profitability was stable last year, with very strong returns on capital:

Operating margin 6.7% (unchanged)

Return on Capital Employed (ROCE): 19.7% (2024: 19.8%)

Segmental results & order book: splitting out divisional results presents a slightly more nuanced picture than I was expecting:

North America (revenue up 5% to £1,815.7m, operating profit down 9.6% to £166.2m): growth at Moretrench and RECON plus project wins in US Foundations (infrastructure and data centres) helped to offset lower revenue from residential work at Suncoast. Performance also benefited from “some historic claims settlements”.

Europe & the Middle East (revenue up 4.1% to £873.4m, operating profit up “four-fold” to £38.8m): rapid profit growth here was due to the non-recurrence of project losses in 2024.

Asia-Pacific (revenue up 14.6% to £398.2m, operating profit up 14.6% to £30.6m): higher volumes at Austral and Keller Asia were partly offset by softer trading at Keller Australia. There was also some benefit from “project closure settlements” in Australia.

I have not researched Keller’s divisional operations in detail. But my overall impression is that underlying profit growth was minimal last year and benefited from some one-off factors.

This view is strengthened by a slight decline in Keller’s reported order book at the end of the year:

Total order book at 31 Dec 25: £1,541.7m (Dec 24: £1,610.0m)

Order book for contracts greater than one year: £559.7m (Dec 24: £578.3m)

Balance sheet & Capital Allocation

Keller has a new chief executive and a newly -improved balance sheet, with net cash for the first time in 25 years. Despite remaining “mindful of macroeconomic uncertainty”, CEO James Wroath has opted to return the business to a target net debt position through a programme of increased shareholder returns and potential M&A:

Target net debt to EBITDA ratio of 0.5x - 1.5x.

Intention to launch a further £100m share buyback.;

Dividend cover policy amended to 2.5x-3.5x underlyiing earnings (FY24: 4.0x cover).

Acquisitions: “We believe there is an opportunity to accelerate our strategic plans and further enhance our market positions through selective acquisitions.”

These measures are affordable as things currently stand. But if I was a shareholder, I would not be averse to the group maintaining a net cash position. As this year’s results show, even without leverage the business appears to be able to generate attractive returns on capital.

Outlook

With the demand for our services supported by favourable long-term structural growth drivers including infrastructure investment, population growth, energy transition, climate resilience and technology adoption, we remain confident that the Group is well placed to build on its momentum and deliver further progress in 2026 and in the years ahead.

Mr Wroath appears to have taken charge at a strong point in Keller’s history and sounds confident in the future, expressing the view that “our operational performance is sustainable”.

There is no comment on FY26 financial guidance but I think it’s fair to assume current forecasts will be maintained.

This leaves Keller trading on a FY26E P/E of around 10, with a 3.2% dividend yield.

Roland’s view

One year ago, I commented that “this should be a cyclical business, but the 30-year record of dividend growth suggests strong underlying demand, probably reflecting the group’s market leadership.”

Keller is a market leader and is able to execute some of the most complex and large-scale groundwork projects in the world. On the face of it, the current valuation remains modest for a business with strong quality metrics and a healthy balance sheet.

However, the valuation is a little stronger than it was a year ago and I think it could be naive to assume that this business will not suffer from cyclical downturns or large project losses again at some point in the future.

The StockRanks currently style the shares as a Super Stock and take a positive view, albeit with a declining ValueRank.

I’ll be interested to see how these figures are updated when today’s results are added to our databases but in the meantime I think it’s fair to maintain my previous AMBER/GREEN view here.

See what our investor community has to say

Enjoying the free article? Unlock access to all subscriber comments and dive deeper into discussions from our experienced community of private investors. Don't miss out on valuable insights. Start your free trial today!

Start your free trialWe require a payment card to verify your account, but you can cancel anytime with a single click and won’t be charged.