Good morning!

1.30pm: almost a clean sweep today, happy with that! See you next time.

Companies Reporting

| Name (Mkt Cap) | RNS | Summary | Our view (Author) |

|---|---|---|---|

HSBC Holdings (LON:HSBA) (£160.2bn) | Final Results | PBT $32.3bn includes one-off gains. Extends its “mid-teens” ROTE target from 2025 to 2027. | |

Glencore (LON:GLEN) (£43.0bn) | Preliminary Results | Adj EBIT -33% at $6.9bn, mainly due to lower coal prices. $0.10 per share divi, $1.0bn buyback. | |

BAE Systems (LON:BA.) (£40.2bn) | Final Results | Rev +14% to £28.3bn, adj EPS +10% to 68.5p. Order intake -10% but order b’log +11.5% at £77.8bn. | AMBER (Roland) Solid results from BAE and a useful 10% dividend increase. However, the valuation remains elevated by historic standards and I feel the shares are largely up with events, so I’m taking a neutral view. |

Jet2 (LON:JET2) (£3.4bn) | TU | On prevailing trends, FY March 2025 PBT £560-570m. FY 2026: profit margins under pressure. | GREEN (Roland) |

Conduit Holdings (LON:CRE) (£719m) | Preliminary Results | GWP +24.8% to $1.16bn, ROE of 12.7% in “high catastrophe year”. Divi held. Exps for cont’d growth. | GREEN (Graham) I'm upgrading our stance as I'm very impressed by performance in 2024. The 2025 estimates incorporate high losses from the California wildfires but still suggest that ROE will be over 10%. In a better year, ROE will hopefully be back around 20%. And the shares are trading at a meaningful discount to their tangible net asset value. |

Beeks Financial Cloud (LON:BKS) (£217m) | TU | H1 is in line, adj. PBT +31% to £1.8m. Confident that results for FY25 will be in line. | AMBER (Graham) Nasdaq and Mexican Stock Exchange deals should boost H2 revenue. Needed as only 40% of the full-year revenue forecast has been generated in H1. Valuation doesn’t make sense to me so I’m neutral. |

Keystone Law (LON:KEYS) (£163m) | TU | FY25 rev & adj PBT to be “slightly ahead” of market exps due to Interest rates and new hires. | AMBER/GREEN (Graham) [no section below] I’m happy to leave Roland’s stance from Sep 2024 unchanged with KEYS on track to slightly beat expectations (revs £94m, adj. PBT £11.9m). There is “broad based client demand” and recruitment is “buoyant”. The share price has cooled down since September, putting it on a more affordable valuation with PER <20x. So it could be worth a fresh look. |

Tracsis (LON:TRCS) (£109m) | Contract Win | Chosen to implement “Tap Converter” system for UK PAYG rail fares. Revenue from 2026. | AMBER (Roland) |

Oxford Metrics (LON:OMG) (£70m) | AGM Statement | Trading so far in 2025 is in line with mgt exps. Order book “healthy”, markerless dev on track. | AMBER/GREEN (Roland) [no section below] |

One Health (OFEX:OHGR) (£22m) | Capital Raising & Proposed Admission to AIM | £7m placing and £1m open offer/retail offer. Proposes to leave Aquis and join AIM in March. | AMBER (Graham) This is still on Aquis but if all goes well, it will be on AIM next month. The Non-Exec Chair is a major shareholder and the remaining free float is likely to remain small and illiquid. I'll start off neutral as I wait to see how the company gets on with its plans to build its first owned surgical hub. |

Graham's Section

Beeks Financial Cloud (LON:BKS)

Down 6% to 302.2p (£203m) - Trading Update - Graham - AMBER

It’s always noteworthy when there’s a disconnect between the sentiment in a trading update and the sentiment in the share price’s response.

Today’s trading update is in line and management are “confident in achieving results for FY25 in line with its expectations”.

And yet the share price is down 6%.

When this happens, I expect to find some big earnings multiples to reflect high expectations having been baked in, and that’s the case here:

On the numbers more specifically, we have:

H1 revenues +22% to £15.8m

Underlying PBT +31% to £1.8m

Net cash of £6.6m is unchanged since June 2024. An additional £1.2m was received in early January.

On the expansion of the service, we have:

Strong Exchange Cloud momentum has continued. In addition to the approval of the contract with one of the largest exchanges globally, the Group was pleased to secure a further extension to the Johannesburg Stock Exchange contract and, post-period end, a major new win with Grupo Bolsa Mexicana de Valores, the second-largest exchange in Latin America.

The deal with Grupo BMV (the Mexican Stock Exchange) was separately announced in a late afternoon RNS yesterday.

Estimates

Thanks to broker Canaccord for their continued coverage. They note that H1 revenues are covering 40% of full-year forecasts, where in previous years the company generated 45% of full-year revenues in H1. They see “additional growth drivers kick in in 2H25”.

EPS estimates are unchanged vs. where they were in January when Roland had a look: 7.7p in FY June 2025, and 9.5p in FY June 2026.

At the latest share price this puts the stock an a forward PER of 32x, using FY June 2026 numbers.

Graham’s view

It’s not easy for me to have conviction in BKS hitting its full-year forecasts, as this requires 50% revenue growth in H2 vs. H1, which would represent a sharp acceleration vs. the year-on-year revenue growth announced today.

However, the new partnership with NASDAQ is live with customers on-boarded “at the end of February” (according to the January update), so this will boost H2 revenues.

The deal with Grupo BMV will see revenues recognised “at the point of the solution’s delivery” and “further underpins the Board’s FY25 expectation”, according to yesterday’s RNS.

So the company and its broker continue to argue that BKS will pull off this revenue acceleration..

I’ve never properly understood the investment thesis here. It seems to me that BKS is a data centre company that’s operating in an attractive niche (financial markets and exchanges). I can understand why it might deserve an above-average valuation, but at a market cap of £200m it’s trading at 5x forward sales (assuming it hits forecasts), 5x book value, and what seems to me eye-watering earnings multiples.

Investors must believe that very high margins and returns are achievable in future, to go with top-line growth.

But to me, data centres are a capex-heavy type of business with few barriers to entry, so I’d be surprised if BKS was able to earn above-average returns for very long.

I applaud the company’s growth to date but I’m afraid I don’t understand the valuation, so I’m neutral on this.

Conduit Holdings (LON:CRE)

Down 8% to 402p (£666m) - Preliminary Results - Graham - GREEN

CHL, the ultimate parent company of Conduit Re, a multi-line Bermuda-based reinsurance business, today presents its preliminary results for the year ended 31 December 2024.

We don’t cover the insurance sector very often in this report. Let’s take a look at what is happening here, with the shares down 8% on the back of these full-year results.

The top line is strong, with gross written premiums up 24.5% and reinsurance revenue up 28.5%.

However, the financial outcome from reinsurance was poor with a “reinsurance service result” of only $131.6m (last year: $183.6m).

Similarly, CRE’s “comprehensive income”, the net result of all of its operations, was only $125.6m (last year: $190.8m).

Return on equity falls to just 12.7% (last year: 22%).

Combined ratio (measure of profitability for an insurance company, excludes investment income): there are two measures given for this, and they both increase. This is a bad thing as anything above 100% indicates unprofitable insurance operations. The less forgiving measure rises from 81.9% to 97.1%.

Investments generated $66m even with a return of just 4%.

Tangible net assets per share increase from $6.25 to $6.70.

CRE’s 402p share price is equivalent to $5.06, so it is trading at a 24% discount to net tangible assets.

CEO comment: 2024 was a “high catastrophe year”. There were two major hurricanes in Florida.

While the business is still exhibiting substantial growth, we now have a demonstrated platform, generating profitable returns even in high industry loss years. Our results also illustrate the continued and growing cost efficiency of our business model and an increasing contribution to profitability from investment returns as our asset base grows. The Company is well capitalised and we expect to continue to build on these achievements as the business grows and matures.

Outlook

There has been “continued strong growth at January renewals”. The company says that pricing remains attractive but “risk-adjusted” rates are down by 3%.

However, the California wildfires started in January and “are likely one of the costliest insured catastrophes in history”. The expected hit to CRE is $100 - 140m.

But it should be easier to sell insurance in the months and years ahead:

We expect the recent events to support favourable underwriting conditions during upcoming renewal periods and we expect to see opportunities to grow our book and deploy capacity at favourable rates

The Exec Chairman sums things up nicely:

On our IPO four years ago we set out with a target of delivering mid-teens ROEs and gross premiums written of $0.9 billion in year four. Our premium in 2024 was $1.16 billion which is 30% above our IPO target, in addition we achieved a 12.7% ROE in a high industry loss year following on from a 22.0% ROE in 2023. We can be proud of what this business has achieved and, with a strong capital base and a robust, efficient platform that is still in its growth phase, I am very excited for the future."

Estimates

Panmure Liberum have cut their 2025 EPS estimate by 31% after taking into account the expected losses from the California wildfires (from 137.8 cents to 95.2 cents). 2026 also gets a trim, from 148.4 cents to 139.9 cents.

Importantly, they suggest that c. $45m of the loss would be in the annual loss budget. So if the hit from the wildfires is $100 - 140m, and there are no other major catastrophes, the unexpected hit would be a more modest $55 - 95m.

The 8% fall in the share price today may reflect disappointment in the size of the potential exposure to the wildfires, and the lingering uncertainty over CRE’s exposure.

Graham’s view

I see that Roland was AMBER/GREEN in November.

The main uncertainty in the short-term is obviously the wildfire impact, with a very wide range of possible losses.

2025 has started very badly in terms of catastrophes, and of course it can always get worse.

However, what I’m seeing is a relative newcomer that has already generated excellent (20%+) ROE in a good year (2023), and acceptable (10%+) ROE in a bad year (2024)

The new Panmure analysis suggests ROE of 14.2% in 2025, rising to 19.2% in 2026.

I do see a downside risk to the 2025 ROE estimate, but hopefully it will stay over 10%.

Then perhaps 2026 might be a good year with few natural catastrophes. Investment returns might also improve perhaps? Although that's tricky to predict as it depends on interest rates and on CRE's appetite to hold risk assets. It seems to have a very conservative investment profile currently.

I’m going to take a positive stance on this because it’s trading a material discount to NAV and I think it has achieved a lot in terms of proving its ability to get a good performance even in a year with high losses. It does have a shorter track record than other names in the insurance industry and that does increase the risk associated with this view. But I like what I’m seeing here: a discounted price for a high-performing insurer.

The share price has reached a level not seen since late 2022:

One Health (OFEX:OHGR)

Down 5% to 199p (£20m) - Capital Raising and Proposed Admission to AIM - Graham - AMBER

We’ve never covered this one before, as it’s on the Aquis Exchange and we generally don’t cover stocks listed there.

However, that’s about to change for One Health Group.

The company provides NHS-funded medical procedures in various hospitals and clinics. Its website describes itself as follows:

We are a team of Consultant Surgeons and Healthcare managers working with the NHS to provide faster, local and expert care in Orthopaedics, Spinal, General Surgery and Gynaecology.

Historic financials suggest that it’s both profitable and growing:

Today, the company announces plans to raise £7m in a placing, broken up as follows. The numbers are provisional:

£5.2m of new shares to help fund “the construction and delivery of One Health’s first owned surgical hub through to operation”

£1.2m sale of existing shares by the employee benefit trust (EBT)

£0.6m sale of existing shares by the Non-Exec Chair and the company’s Chief Medial Officer.

N.B. The Non-Exec Chair currently has a 57% interest in the company, but should drop below 50% after this.

The company also plans to raise £1m through the combination of an open offer (to existing shareholders) and a retail offer (for both existing and new shareholders).

So in total the company is raising about £6m of new money, with perhaps also about £2m in sales of existing shares.

Given the market cap last night was only £22m, this is a hugely significant development for OHGR. Plus, when it’s on AIM, people like us may start studying it in more detail!

It’s expecting to list on AIM on 20th March.

Graham’s view

While I tend to bring scepticism to new IPOs, I have a totally different attitude to companies switching from Aquis to AIM (or from AIM to the LSE).

AHGR has been on Aquis since 2022 so it already has a track record as a public company for a few years.

I’ll start off neutral on it and see if they can put the funds raised to good use.

Please bear in mind that the Non-Exec Chair will still hold a large share of the company even after this transaction, so the free float is likely to remain very small and illiquid for now.

Roland's Section

Jet2 (LON:JET2)

Down 10% to 1,407p (£3.0bn) - Trading Update - Roland - GREEN

the Board expects to report a Group profit before foreign exchange revaluation and taxation for the year ending 31 March 2025 of between £560m and £570m, an 8% to 10% increase on the prior year.

Holiday operator and budget airline Jet2 is a favourite with many subscribers here at Stocko – and with good reason. This is a very well-run business whose shares have five-bagged over the last decade, despite the disruption from Covid-19.

The StockRanks continue to rate Jet2 highly as well, underlining its fundamental appeal:

Keelan took a broader look at Jet2 in The Week Ahead on Friday. Let’s see what fresh news is on offer in today’s update.

Updated guidance: Jet2’s half-year results in November included guidance for pre-tax profit to exceed consensus expectations, which were then pegged at £541m.

Today the company has confirmed it expects to report adjusted PBT of between £560m and £570m for the year ending 31 March 2025.

This represents an increase of 8%-10% from the prior year, but I don’t think it’s an upgrade. With thanks to broker Canaccord Genuity, updated estimates this morning are broadly unchanged:

FY25E adj PBT: £563.6m (previously £563.9m);

FY25E EPS: up 1% to 191.5p (previously 189.7p).

In my view, this is effectively an in line update. This may account for this morning’s share price drop. Perhaps investors were hoping for another ahead announcement.

Trading commentary: Jet2 does not seem to be facing any serious new problems, but there are some ongoing headwinds, mostly reflecting external conditions:

However, we also recognise the current macro-economic conditions and the many demands placed on consumer discretionary incomes, which combined with the later booking profile and cost headwinds detailed, may mean profit margins in the year ahead come under some pressure.

A number of points stand out to me from the commentary:

The company makes several mentions of a later booking profile - people are leaving holiday planning later than usual;

Winter 24/25 capacity is 14% higher than the prior year, at 5.1m seats - Jet2 is expanding;

Season to date booked average load factor is down 2.2%, but this is partly due to Easter timing and the ramp up of new bases at Luton and Bournemouth. Excluding this, load factor is flat despite increased capacity – so more people are booking with Jet2;

The company recently awarded a 3% pay rise from April 2025 - looking after the workforce;

Jet2 is moving from Boeing to Airbus A321neo aircraft and is seeing the expected benefits from this change, but a number of scheduled deliveries have been delayed, leading to additional costs;

Cost inflation in large areas including hotels and aircraft maintenance is expected to exceed the headline CPI rate;

Changes to employer taxes will add £25m to FY costs, while the mandated use of 2% of Sustainable Aviation Fuel (SAF) will add £20m of incremental costs.

Roland’s view

Like many airlines and travel businesses, Jet2 trades on a low P/E multiple. Looking under the bonnet, I’d argue that the price to book ratio of 1.9 is also attractive.

Jet2’s NAV of £1.8bn is backed by tangible assets and net cash and the group has recently been generating a 30% return on equity. Based on this, buying shares at 1.9x book value implies a return on cost of equity of around 16%.

Jet2’s sizeable net cash balance (last reported at £2.3bn) also provides another benefit, now that interest rates have normalised. Net finance income was £68m in H1, adding almost 10% to operating profit.

The outlook for the next 6-12 months looks relatively flat and planned capex of £5.7bn over the next seven years may draw on the group’s cash reserves.

However, I don’t have any serious concerns about the longer-term prospects for this business and believe the shares remain reasonably valued. I’m going to maintain our GREEN view based on today’s update.

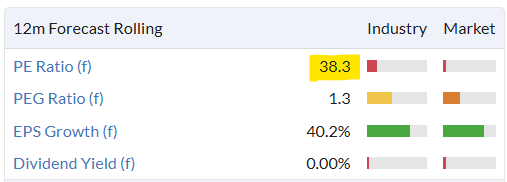

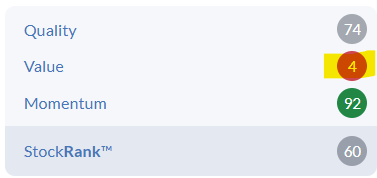

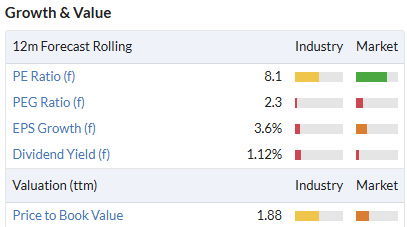

BAE Systems (LON:BA.)

Unch. at 1,336p (£40.0bn) - Final Results - Roland - AMBER

FTSE 100 defence group BAE Systems remains a widely-held stock among UK investors despite the appeal of the Mag 7 and US market.

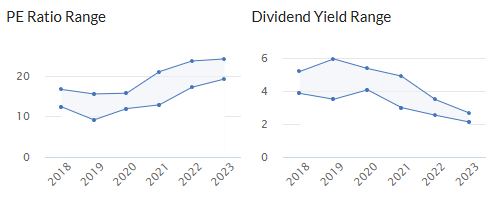

Events of recent years have stimulated growth and saw BAE end 2024 with a record order backlog of £77.8bn. This progress has encouraged investors to bid the stock up to a valuation that’s well above historic norms:

Today’s results have received a relatively cool reception but do not seem to flag up any serious concerns. Let’s take a look.

2024 results highlights: BAE’s headline figures show strong growth in most areas:

Sales (adjusted revenue) up 14% to £28,335m

Underlying EBIT up 14% to £3,015m

Underlying EPS up 10% to 68.5p

Order intake down 10.6% to £33.7bn

Order backlog up 11.5% to £77.8bn

Net debt exc leases: £4,945m (2023: £1,022m) - due to £4.4bn acquisition of Ball Aerospace

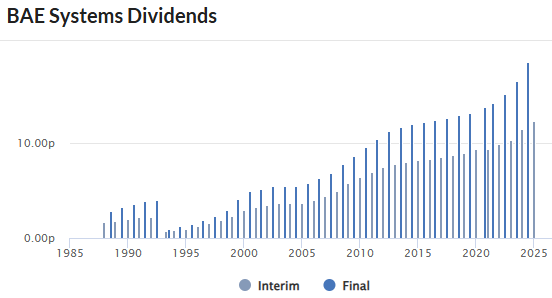

The full-year dividend has been lifted 10% to 33p per share, maintaining a 30-year track record:

My sums show this increased payout is comfortably covered by free cash flow of £2,505m (83p per share). BAE’s cash conversion is generally good in my experience and this FCF figure represents >100% conversion from reported net profit of £2,445m. A good performance.

The group’s dividend is a traditional attraction for investors, but the 2.5% yield is far less appealing than it used to be. To justify buying for income at this level I would argue that investors need a fairly strong view on growth.

The size of this business means that it depends heavily on large, multi-year deals to keep the hopper filled. Fortunately there were a number of these last year:

Agreement to partner in the development of the next generation combat aircraft (GCAP)

Under AUKUS agreement, selected to deliver Australia’s new fleet of nuclear submarines

£4.6bn contract for Hunter Class frigates in Australia

£2.0bn of orders for combat vehicles produced by Hägglunds subsidiary

Multiple satellite launches for US Space Force and NASA

Plus very many smaller deals, including Typhoon orders totalling £1.1bn

Many of BAE’s large programmes are fairly lumpy and the order backlog remains at a record high. For these reasons, I’m not sure that last year’s 10% decline in order intake is a concern. However, a reduction in order intake could be a leading indicator that demand is stabilising, so is worth watching.

2025 Guidance: we don’t have access to broker notes for BAE, but fortunately the company does provide clear financial guidance:

Sales: increase by 7% to 9%;

Underlying EBIT: increase by 8% to 10%

Underlying EPS: increase by 8% to 10%

Free cash flow target: >£1.1bn (within 2025-27 cumulative target of >£5.5bn)

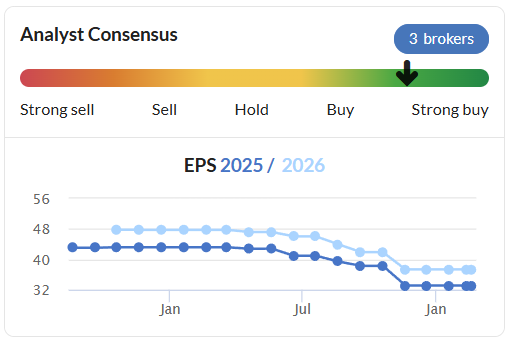

Taking the mid-point of this EPS estimate gives me a 2025 estimate for adjusted earnings of 74.7p per share. That’s slightly below the consensus figure of 75.2p shown in Stockopedia prior to today.

I’m not sure this is enough to constitute a downgrade, but it’s certainly not an upgrade. Let’s call it in line.

Roland’s view

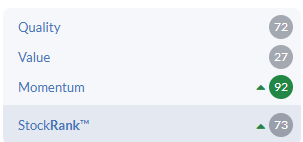

BAE’s fortunes and growth trajectory will remain unavoidably linked to geopolitical events and political decisions. I’m not going to speculate on these here but in broad terms, my view reflects that of Stockopedia’s algorithms. These now class this stock as a High Flyer, not something I’d have expected a few years ago:

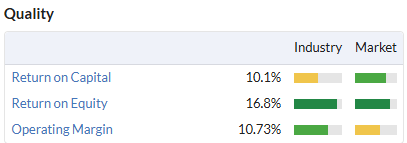

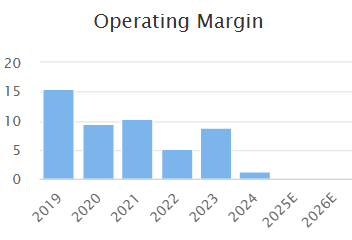

The company’s QualityRank of 72 is respectable, but I’m not sure this capital-intensive business really qualifies as a quality stock. Return on capital employed (ROCE) has typically only averaged around 10%, although cash generation is good.

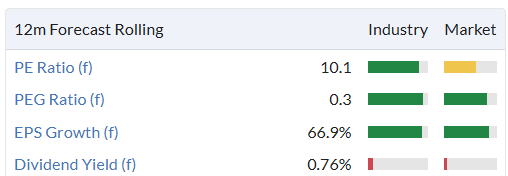

Looking at valuation, the shares now trade on a 2025 forecast P/E of 17.8, with a 2.6% dividend yield.

Personally, this is above the level I’d want to pay for this business. Although I think trading is likely to remain positive, my feeling is also that the re-rating triggered by the invasion of Ukraine in 2022 has probably completed.

This view is also reflected in BAE’s overall StockRank:

I think there’s scope for further progress, but I don’t feel comfortable guessing at external catalysts. I’m going to take a neutral view for now.

Tracsis (LON:TRCS)

Up 8% to 389p (£115m) - Contract for Tap Converter - Roland - AMBER

This technology group serves the UK rail sector and was previously a small-cap favourite, but it’s come off the boil badly in recent years:

Today’s contract win announcement suggests the tide might be turning, but is frustratingly short on financial detail, in my view.

Tap Converter Contract win: Tracsis says it has won a contract to provide a new payment system for rail ticketing:

Major contract win, through a competitive bid process, to provide the central smart ticketing technology platform enabling PAYG travel in urban areas across National Rail.

This appears to refer to a system where travellers will simply tap on and off trains using a card/phone and later be automatically billed the best possible fare:

Tracsis will utilise its existing technology to construct journeys from these taps calculating the best fare while automatically applying entitlements, concessions, discounts and fare caps. Once calculated, the system provides this fare information to the TOC to charge the passenger and submits settlement records to the rail industry's settlement engine.

Tracsis already appears to be a major player in this market in the UK. Six Train Operating Companies already use Tracsis smart ticketing systems:

Tracsis is currently the only provider of an accredited PAYG ticketing platform on the National Rail network outside London, and this contract significantly extends the potential reach of Tracsis' technology.

Financial impact: there’s a frustrating lack of financial guidance in today’s RNS, in my view.

The company says that development will start immediately, with deployment and transactional revenue expected from 2026. But no details are provided beyond this statement:

Once deployed, the contract delivers a guaranteed minimum annual operating fee with additional transaction revenues based on the volume of PAYG transactions processed.

It’s not clear to me whether companies using Tracsis’ existing PAYG technology will be expected to migrate to the system, or may choose not to.

Once the Tap Converter system is operational, Tracsis revenues will be based on the volume of transactions processed and this will be driven by future customer adoption rates and system usage.

It’s interesting to speculate on the total addressable market here. Tracsis’ current PAYG systems processed 2.25m journeys last year.

The company says that in total, there were 1.7bn rail journeys made last year. Of these, it estimates that 10% to 15% could be paid for using the Tap Converter system “in the medium term”.

This would seem to imply that more than >200m annual journeys, principally commuting, could pass through Tracsis’ new system eventually. That could be a 10-fold increase from current levels, but with no idea of the financial profile of the new system (versus the older ones), it’s hard to estimate what impact this might have.

Estimates: sadly there are no new broker notes available on Research Tree today.

The only explicit financial guidance from Tracsis today is that expectations for the year ending 31 July 2025 are unchanged.

Roland’s view

With no guidance on expected revenue from the new system and no broker notes, shareholders are in the dark about how to interpret today’s news.

It sounds positive to me and I think it’s reasonable to see this as a new growth driver for Tracsis. But I don’t see any way to estimate timescales or the likely contribution to earnings from this new system.

Tracsis is viewed as a Falling Star by Stocko’s algorithms and consensus estimates have drifted steadily lower over the last year:

Profitability has really suffered in recent years, too:

However, the company had net cash equivalent to more than 10% of the market cap at the end of July 2024, and the current forecast valuation doesn’t look too demanding to me:

I suppose the worst-case scenario I can see here is that the Tap Converter system will cannibalise Tracsis’ existing ticketing business and generate lower profit margins than current systems.

Assuming this does not happen, I think that current forecasts ought to be enough to provide a base for Tracsis shares, with today’s news perhaps forming a foundation for a modest return to growth.

It’s always risky to try and call the bottom for a Falling Star. I’d want to do more in-depth research before considering whether to invest in Tracsis. But I’m comfortable taking a neutral view here, perhaps with a view to upgrading when more detail becomes available. AMBER.

See what our investor community has to say

Enjoying the free article? Unlock access to all subscriber comments and dive deeper into discussions from our experienced community of private investors. Don't miss out on valuable insights. Start your free trial today!

Start your free trialWe require a payment card to verify your account, but you can cancel anytime with a single click and won’t be charged.