Good morning!

Today's Agenda is now complete - much more relaxing than yesterday's deluge!

UK CPI

UK inflation came in at an annual rate of 2.8% this morning, down from 3% in January and below the expected result of 2.9%. However, it’s too soon to get the bunting out as many important prices are expected to rise in the coming months: on top of household utility bills and council tax increases, we still haven’t seen the real-world effect of higher labour costs arising from the changes to national insurance contributions.

At 12:30, after PMQs, we’ll have the Spring Statement from Rachel Reeves, which is expected to include a range of welfare cuts.

At 13:30, the Office for Budget Responsibility will publish its economic outlook, and at 14:30 it will hold a press conference. So there will be no shortage of economic and political news to chew on today.

Companies Reporting

| Name (Mkt Cap) | RNS | Summary | Our view (Author) |

|---|---|---|---|

Ithaca Energy (LON:ITH) (£2.3bn) | Full Year Results | $200m divi, taking full-year total to $500m. Profit after tax $153m (LY: $293m), due mainly to lower gas prices. | AMBER/GREEN (Roland) Today’s results suggest to me that Ithaca is doing exactly what it’s meant to do – generating a lot of cash from established North Sea oil and gas fields. The dividend looks affordable and sustainable to me, at least in the near term. Beyond 2030 I’d argue the outlook is unclear, but with a potential 15% yield on offer, this may not matter right now. I can’t be fully positive on a business like this, but I can see plenty to like. |

Vistry (LON:VTY) (£2.1bn) | Full Year Results | Completions up 7% to 17,225, adj revenue up 7% to £4,329m. | AMBER (Roland) The company’s partnership model is being held back by funding uncertainty for housing providers following the Autumn Budget. This is expected to clear as the year progresses, leading Vistry to warn that profits will be H2 weighted. With debt levels still elevated and a backlog of unsold stock, I think there’s some risk of a further downgrade in 2025. However, the medium-term opportunity seems more encouraging and recent director buying also suggests some cause for optimism. |

Avon Technologies (LON:AVON) (£414m) | Trading Statement | Strong momentum in Q2, with growth driven by US DOD helmet orders and respirators/underwater rebreathers. | AMBER (Roland) [no section below] The ramp up of helmet volumes in the Team Wendy business is identified as “both a risk and an opportunity”. A large increase in production can sometimes be difficult to achieve while keeping costs and quality on track. It’s refreshing to see a company acknowledge this, but perhaps a little worrying also. It’s unfortunate that Avon is also in the midst of a substantial restructuring of Team Wendy, adding further complexity. Overall progress seems positive, but I don’t think the current valuation allows much room for error. On balance, I’m neutral. |

Kenmare Resources (LON:KMR) (£378m) | Full Year Results | 2025: on track for production guidance. Info being provided to potential takeover consortium. | |

Everplay (LON:EVPL) (£330m) | Full Year Results | Rev +5%, adj. EBITDA +46% (£43.5m). Cash £63m. Outlook: marginally ahead of exps. | |

Evoke (LON:EVOK) (£321m) | Full Year Results | SP down 13% Adj EBITDA “slightly ahead” of exps. Strong H2. Rev +3%, adj LBT of £28.8m. FY25 exps unch. | RED (Graham holds) Thinking about selling this as the timeline for the company to get its leverage multiple back to a reasonable level has been pushed back by a year. Adj. EBITDA numbers are impressive but the adjustments and exceptional items are truly enormous and even paying its interest bill looks difficult. |

LSL Property Services (LON:LSL) (£274m) | Full Year Results | Results “just above” consensus. Rev +20%, adj PBT +373% to £23m. YTD trading in line. | |

Luceco (LON:LUCE) (£240m) | Full Year Results | Revenue +16%, adj PBT +17.5% to £24.9m. Results “at upper end” of expectations. Strong momentum. Net debt of £69m gives a leverage multiple of 1.6x, within the target range of 1.0x - 2.0x. | GREEN (Graham) [no section below] This is a Super Stock and it's one that we've been positive on. I'm leaving our stance unchanged today with the company reporting continued market share gains in its markets - wiring accessories, EV charges, LED lighting and portable power. There is no hint of doubt in the outlook statement despite a "lacklustre" economic environment. I do note that statutory PBT (£18.9m) failed to grow due to higher acquisition-related costs, including amortisation. However, the cash flow statement is supportive with £35m of operating cash flow generated (previous year: £32m), and limited capex spending. A very large negative working capital movement - receivables up by £17m - should reverse in the current year. |

Aptitude Software (LON:APTD) (£151m) | Full Year Results | ARR +2% to £52.1m but rev -6% to £70.0m. Op profit +8% to £5.7m. Flat outlook for FY25. | |

Trufin (LON:TRU) (£84m) | Full Year Results | Rev +203% to £55m, adj PBT £0.9m (‘23: £6.6m loss). YTD rev +145%, “excellent start to 2025”. | |

Anpario (LON:ANP) (£83m) | Results delayed, FY update | Audit delay to results, due by 2/4. Exp 2024 rev +23% to £38.2m, adj EBITDA +55% to £7m. Net cash. | |

Virgin Wines UK (LON:VINO) (£27m) | Interim Results | SP down 8% "Resilient" H1: revenue flat at £34m, PBT up 20% to £1.3m. Strong Xmas performance and 10% reduction in cost to serve customers. H2 has started positively; outlook in line. Net cash £17m. New CFO. New growth targets include annualised revenues of >£100m by the end of 2029 (FY25 forecast: £61m) with an EBITDA margin of 7% (FY25 forecast: 3.5%). It also announces plans to buy back up to 15% of its shares. | AMBER (Graham) [no section below] I have mixed feelings about this. The company does have the cash to pay for the buyback announced today but I prefer to see buybacks for stocks that are objectively trading at bargain levels and I'm not sure that's the case here. Forecasts out to FY27 suggest that the company will be barely profitable in the years ahead and even if it might be able to earn £7m of EBITDA in five or six years, I'm not sure that's worth significantly more than the current market cap today. So I'm not convinced that these shares are cheap and therefore I'm not convinced that the buyback is the best use of cash. |

Frontier IP (LON:FIPP) (£17m) | Interim Results | Pre-tax loss of £1.6m, NAVps of 67.6p. £3.3m placing. “Significant” progress across portfolio. |

Backlog

Mission (LON:TMG)

Down 14% this week to 23.1p (£21m) - Final Results - Graham - AMBER/RED

Roland covered a big disposal by this marketing communications group in January.

Yesterday it had full-year results which confirmed that trading in the new year is in line with expectations.

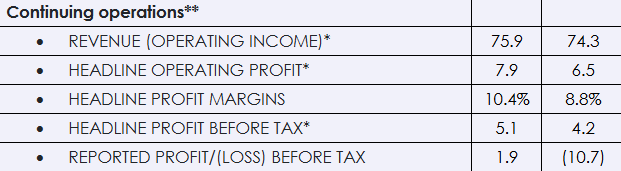

Let’s focus on 2024’s results for continuing operations, which exclude the business sold in January (“April Six”).

The left-hand column is 2024, the right-hand column is 2023 (£millions):

The disposal of April Six produced an upfront payment of £10.5m, along with a future earn-out of up to £4.2m.

Unfortunately the cash flow statement shows that it wasn’t a “clean” £10.5m that was received. There was over £2m of cash lost from subsidiaries disposed of, and there was over £2m in disposal costs. So the company only achieved a £6.2m cash inflow.

With operations producing limited cash, the end result for the year in terms of net bank debt was a reduction from £15.4m to £9.4m. Hopefully the earn-out from April Six will help to reduce this further - that payment is scheduled for June 2025.

Missions also owes £4.7m in connection with its own prior acquisitions, some of which can be settled with shares instead of cash.

The balance sheet has zero tangible net worth but this is at least an improvement on last year.

Dividend: dividends are paused for now. The Board expects to return to paying dividends in 2026.

Graham’s view

I’m happy to upgrade my stance to neutral, although I still don’t have much conviction here. The company needs another solid year now to reduce net bank debt further and get into a more comfortable position. The good news is that it is trading cheaply against forecast earnings; Canaccord Genuity put out a forecast for adj. PBT of £6.5m in January.

Do watch out, though: earnings forecasts are shaky and subject to further downgrades:

Today’s “Going Concern” statement by the directors doesn’t fill me with confidence either, talking about what the company might do if it runs into trouble with covenants in a downturn - headcount reduction would be on the cards.

So I don’t view this as a sleep-sound investment by any means but at a £20m market cap and with a slimmed-down group structure for 2025, perhaps prospects are reasonable from here.

Graham's Section

Evoke (LON:EVOK)

Down 13% to 62.4p (£317m) - Full Year Results - Graham - RED

At the time of publication, Graham has a long position in EVOK.

This starts off promisingly (my emphasis added):

FY2024 Adjusted EBITDA slightly ahead of top end of guidance range with strong second half of the year

Significant transformation of the business showing results; no change to FY25 expectations

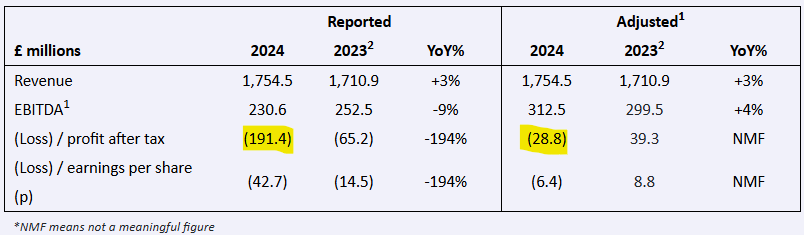

The company notes that it achieved an adj. EBITDA of £197m in the second half (vs. only £115m in H1).

The guidance range for adj. EBITDA was £300-310m. This was itself on upgrade on prior expectations, and Evoke has now beaten it.

Unfortunately there is an actual after-tax loss and an adjusted after-tax loss for the year. If only we could eat EBITDA:

There are a huge array of exceptional items and adjustments. We’ll get into them shortly.

Current trading / outlook

Probably one of the main reasons for the share price decline today is that Q1 revenue growth is at a “low single digit”, below the 5-9% full-year target.

Reasons (or excuses!) given include:

Short term impact of additional safer gambling measures in the UK Online business (introduced at the end of Q4).

Elevated marketing and promotional activity in the prior year

Operator favourable sports results in Q4, racing cancellations in January

Despite very modest revenue growth, Q1 adj. EBITDA is up by £18-28m vs. Q1 2024. I’m a little surprised the range given is so wide, as Q1 is about to finish.

The result is that over the last twelve months, adj. EBITDA is now c. £330 - 340m.

The market evidently doesn’t believe them, but they insist that full-year expectations are unchanged:

No change to FY25 expectations and the Board reiterates its confidence in achieving FY25 targets of 5-9% revenue growth and Adjusted EBITDA margin of at least 20%

Net debt

The leverage multiple remains uncomfortably high at 5.7x although this is down from 6.4x six months ago.

The company’s guidance is for this to get below 5x by the end of 2025, and the medium-term target is for this to get below 3.5x in 2027.

The company previously targeted for leverage to get below 3.5x by the end of 2026, not 2027 (and the 2026 deadline isn’t even mentioned today!). But they say that the reason for the new deadline is “primarily to allow for the additional time needed to build out world class capabilities, alongside the further exceptional costs and capex required to execute such a significant transformation in the business”.

CEO comment excerpt:

I was delighted to see the results of our transformation start to materialise during the year, with the business returning to revenue growth in Q3 for the first time in almost three years, in turn delivering a step change in profitability as a result of our increasingly efficient operating model. Whilst a transformation of this scale is never easy, I am pleased with the strong progress we made during the year..

2025 is shaping up to be another exciting year for evoke. While Q1 revenue growth is expected to be low single digit, we remain highly confident in our full year expectations of 5-9% growth in addition to driving further margin expansion as a result of our more efficient operating model.

Adjustments

With so much talk of adjusted EBITDA, it’s important to interrogate this number and see how meaningful it really is.

So, how does the company get from an adj. EBITDA of £312.5m to an actual pre-tax loss of £169m? That’s a gap of over £480m!

(And the previous year was just as bad, with £300m of adj. EBITDA turning into an actual pre-tax loss of £130m!)

For 2024, we have:

Depreciation and amortisation of £122m

Net finance expense £178m

Exceptional items £80m (previous year: £53m)

Adjustments £100m (previous year: £89m)

I can accept that it costs money to save money, but the scale of these exceptional items scares me.

As amortisation (which is a non-cash charge) is a very large part of the adjustments, I’ll also check the cash flow statement to see if that helps to calm my nerves.

Indeed, net cash generated from operating activities is encouraging at £226m (previous year: £151m). But in the “investing” section of the cash flow statement, I see that the company spent about £90m on capitalised software development. So the real cash flow generation by the business is somewhere south of £140m (before net finance expense).

This is much lower than adj. EBITDA because, among other things, it doesn’t exclude this software development spending from the calculation.

The interest bill was then £160m+, so in summary I do not think that Evoke earned enough real cash flow to pay its interest bill in 2024.

Graham’s view

I’ve stubbornly held onto this for years. My main mistake was not selling when the disastrous William Hill acquisition occurred - that was a major oversight on my part. It fundamentally changed the company’s financial and risk profile, and also made it a much lower-quality business. I have no excuse for not selling when that occurred.

However, given that I failed to sell out when that happened, the question remains as to whether I should have sold subsequently, or if I should sell now.

I’ve been happy to hold onto it as 1) it’s a very small percentage of my single-stock portfolio (currently 2%), 2) I’ve always believed that it’s possible for the company to get its balance sheet under control, which would likely result in the shares multi-bagging from current levels, 3) I think the 888 brand is excellent and the other brands clearly have value too (William Hill, Mr Green and others).

In July 2023, Playtech were reportedly willing to buy the company for 156p per share, well in excess of double the current price.

Net debt is £1.8 billion so the enterprise value is around £2.1 billion.

If the company hits its 5% revenue target (the bottom of its guided range) and 20% EBITDA margin, that translates to c. £370m of EBITDA this year. That makes an EV/EBITDA multiple of less than 6x, which in theory offers reasonable value, if its solvent and its balance sheet can improve.

Net finance expense isn’t going anywhere, and I expect that capitalised software spending will remain high, too. But the company really needs its exceptional costs and other adjustments to settle down. We need much cleaner accounts than what the company is currently presenting.

I’ve been AMBER/RED on this but I think I’ll downgrade my stance to RED today, as I'm disappointed by delayed timeline to hit the target leverage multiple of <3.5x, and I don’t have faith that it will hit the target by its new deadline, either.

The rational decision might be for me to sell this and move on.

Roland's Section

Ithaca Energy (LON:ITH)

Up 8% to 154p (£2.5bn) - Full Year 2024 Results - Roland - AMBER/GREEN

Robust 2024 operational and financial performance at the top end of management guidance

Ithaca’s eye-catching double-digit dividend yield highlights the core focus of this business – to extract as much cash as possible from mature and proven North Sea oil and gas assets.

I’ll return to the dividend in a moment, but I think it’s worth taking a look at today’s results first. The numbers suggest to me that Ithaca is doing a reasonably good job at delivering on its remit.

However, these results do also highlight the reverse operating leverage effect caused by the reduction in gas prices over the last year. Note the reduction in cash flow and profit versus 2023:

Production: 80.2kboe/d, at upper end of guidance (75-81kboe/d)

Revenue: $1,982m (2023: $2,320m)

Net cash flow from operating activities: $853m (2023: $1,291m)

Profit after tax: $153.2m (2023: $292.6m)

Avg realised oil price after hedging: $82/bbl (2023: $82/bbl)

Avg realised gas price after hedging: $78/boe (2023: $111/boe)

The accounts are made more complicated by the acquisition of Italian major ENI’s UK assets. This deal was completed in October and is said to have reduced group average operating costs from $22/boe to $14/boe in Q4.

That supports a positive picture for cash generation in 2025 – Ithaca has hedged 71% of its expected gas production from 2025 to 2027 to lock in attractive (and predictable) pricing.

Leverage increased slightly last year to 0.45x (2023: 0.35x), with year-end net debt of $885m. However, the company has recently completed a $2.25bn refinancing to extend the maturity on its debt, reduce costs and provide more than $1bn of headroom. This could allow Ithaca to undertake further M&A, in its role as a regional consolidator.

This level of leverage looks safe enough to me at the moment, but it’s worth noting that oil and gas borrowing doesn’t come cheap, even for a large operator like Ithaca. The company’s new Senior Notes have an 8.125% coupon and interest charges totalled c.$95m last year.

Dividend: Ithaca has declared a third interim dividend of $200m dividend today, taking the total payout for the year to $500m.

My sums suggest last year’s $500m payout was not fully covered by free cash flow of just over $300m. However, I don’t think this should be an issue in 2025 given the benefit of the ENI assets – the company says that a full-year contribution in 2024 would have increased EBITDAX from $1,405m to $1,985m.

Outlook: production is expected to be 105-115 kboe/d in 2025. Operating costs are expected to be $770m to $850m, with capital expenditure of $750m to $850m, including the politically-sensitive Rosebank development.

The dividend target remains 30% of post-tax cash flow from operations and management expects this to support another $500m distribution. I estimate this equates to around 23.4p per share at current prices/FX, giving a potential 15% yield.

Management expect cash generation to remain strong over the next five years:

Strong cash flow generation over the next five years (2025 to 2029) with a potential for over $9bn of total pre-tax cash flow from operations from 2P Reserves at $80/bbl and 85p/therm.

Based on this, my rough sums suggest it could be possible for Ithaca to return more than 50% of its current market cap to shareholders as dividends by 2030.

Roland’s view

I’m not a sector expert and have only taken a brief look at today’s results. But I don’t see any obvious problems here. Ithaca’s focus on mature and proven assets means it’s highly cash generative and can plan capex to maximise future returns.

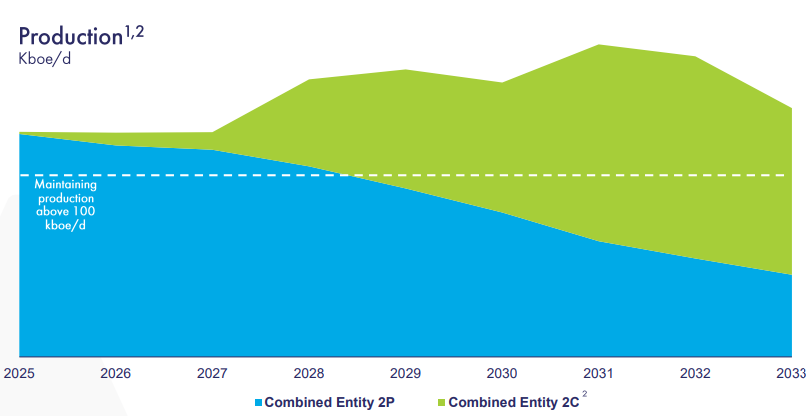

The ENI deal is expected to allow the company to maintain production above 100kboe/d until at least 2033. Ithaca believes it could be the largest producer in the UK North Sea by 2030:

In today’s presentation, the company says its assets support 17 years of production at current levels. However, this doesn’t necessarily mean Ithaca can remain as profitable and cash generative as it is today for the next 17 years.

Analysing the group’s assets is beyond my ability, but I think it’s fair to say that the energy market environment will inevitably evolve over the next 10-15 years.

It’s also possible that the $2.7bn of decommissioning liabilities reported on the 2024 balance sheet will become more onerous to deliver than they are at present – cash expenditure on decommissioning was only $94m last year.

On balance I can see plenty to like here on a near/medium-term view, with the caveat that this is a specialist business with a (potentially) finite lifespan.

Vistry (LON:VTY)

Down 6% to 608p (£2.0bn) - Full Year Results - Roland - AMBER

2024 was a challenging year for the Group resulting in a disappointing financial performance, despite strong growth in completions and revenue.

Now that the rocket fuel of ultra-cheap mortgages and Help to Buy has been removed from the market, most UK housebuilders have seen their profitability return to pretty average levels.

However, most of the companies we’ve looked at recently have at least managed to report improving order book trends. In contrast, Vistry’s order book stood at £4.4bn recently, lower than the £4.6bn seen in March 2024.

The company’s 2023 strategic shift to focus on partnership projects originally looked like a sensible move, reducing capital intensity and exposure to open market sales. But this strategy has now left the company waiting for new government funding to become available to its partners so that it can move forward.

Last year’s performance was also marred by a big cost overrun in its South Division and a further increase in fire safety remediation provisions. To make matters worse, the company appears to be struggling with slow-moving inventory in its former housebuilding business.

Today’s results are rightly described by CEO Greg Fitzgerald as disappointing and warn of a possible H2 weighting to this year’s results.

However, Fitzgerald is a very experienced housebuilder and spent £2.2m buying Vistry shares in October and November last year. Non-exec Usman Nabi also spent £11.1m on shares during the same period. This suggests to me that they have a reasonable degree of confidence in the company’s medium-term prospects.

Let’s take a look.

2024 results summary: the key numbers from these results are somewhat mixed and contain a lot of adjustments:

Completions up 7% to 17,225 units

Adjusted revenue up 7% to £4,329m (including JVs)

Adjusted pre-tax profit down 35% to £263.5m

Reported pre-tax profit down 64% to £104.9m

Adjusted earnings down 35% to 55.9p (in line with consensus)

No final dividend recommended

Last year’s shortfall in profits was primarily driven by the impact of cost issues in Vistry’s Southern Division. These ultimately had a £91.5m impact on FY24 profits.

In terms of adjustments, the main item was a further £115m building safety provision, taking the remaining total to £324m. This is a non-cash charge now, but will ultimately be unwound through cash expenditure on remediation (except where the company succeeds in reclaiming amounts from third parties).

Debt levels: year-end net debt doubled to £180.7m last year. The company had previously targeted a net cash position by the end of 2024 but says the shortfall is due to the drop in profits [caused by South Division] and “a build up of working capital and stock”.

To make matters worse, the average daily net debt position was much higher, at £698.1m (FY23: £586m). Full credit for Vistry for disclosing this, but this is a higher figure than I’d really want to see.

The problem partly seems to be an overhang of unsold stock from the group’s legacy housebuilding business. Cash generation is being prioritised this year and the company hopes to release c.£200m:

The housebuilding landbank release has been slower than anticipated reflecting more constrained market conditions than expected. Site by site strategies are being reviewed and options including bulk sales and discounting are under consideration to accelerate the roll-off and cash generation.

Partnership housing: overall demand from partners was said to be “reasonable” in 2024. 220 new agreements were signed with over 70 partners, including private rental landlords, a growing sector.

Partner sales actually increased last year:

Partner Funded units increased by 18% in FY24 to 12,633 (FY23: 10,722), demonstrating the resilience of the Partner Funded market. Our Partner Funded ASP increased to £236k (FY23: £222k), reflecting changes in mix.

The slowdown in Partnership housing appears to have taken place following the government’s Autumn Budget:

Whilst the additional £500m affordable housing grant announced with this budget, and the further £300m announced in February 2025 were positively received, ongoing uncertainty around the timing and quantum of future Government funding for affordable housing, led to subdued levels of partner demand in Q4 24 and Q1 25.

Outlook: overall volumes are expected to remain stable this year. The group’s current order book just about supports this view:

The Group's forward order book totals £4.4bn (14 March 2024: £4.6bn), with 65% (FY24: 65%) of forecast FY25 units secured.

Much will depend on whether demand for partnership homes improves as expected over the current year:

Following the Government's recent announcement of an additional £2bn of affordable housing funding to the existing affordable homes programme, we expect Partner Funded activity to step-up during the year, resulting in a greater H2 weighting of Partner Funded delivery for the Group in FY25. Overall, we are expecting our Partner Funded volumes in FY25 to be at a similar level to FY24, with strong momentum going into FY26.

Profits are expected to “make some progress in FY25”, but with more of an H2 weighting than usual. So perhaps there’s still some risk of a further downgrade to expectations:

Roland’s view

Looking further ahead, Vistry is targeting 5%-8% pa revenue growth and a 40% return on capital employed, supported by the capital-light nature of its partnership model.

This would represent a substantial improvement on last year’s adjusted ROCE of 14.6%, but it may not be impossible.

The one-off costs associated with the South Division shouldn’t repeat and management expects the group’s capital-intensive land bank to shrink, relative to construction volumes, in the future. This is because partnership projects are completed and pre-sold much more quickly than open market homes.

Vistry also expects a greater proportion of development on sites it controls (e.g. through JVs) but does not own – again, reducing capital intensity and potentially increasing ROCE.

However, last year’s performance was poor and left the group more heavily leveraged than I’d like to see. The H2 weighting to this year means that there’s a lack of clarity over the near-term outlook.

The forward P/E of 10 seems high enough to me at this point. While the balance sheet shows £2.0bn of tangible net assets (in line with the market cap), it’s worth noting that switching year-end net debt for average daily net debt could significantly reduce this tangible net asset figure.

I think there could be a medium-term opportunity here, but for now I’m most comfortable taking a neutral view. AMBER.

See what our investor community has to say

Enjoying the free article? Unlock access to all subscriber comments and dive deeper into discussions from our experienced community of private investors. Don't miss out on valuable insights. Start your free trial today!

Start your free trialWe require a payment card to verify your account, but you can cancel anytime with a single click and won’t be charged.