Good morning!

We have a Fed interest rate decision this evening, where no change in rates is expected.

Its significance is that it's the last decision under outgoing Chair Jay Powell.

He will step down with rates stable in a 3.5-3.75% range, and with inflation at 3.3% - a two-year high - after oil prices spiked in March. Unemployment remains low at 4.3%.

No fireworks are expected this evening, and then next month we will enter the era of Kevin Warsh.

All done for today. Spreadsheet accompanying this report: link.

Companies Reporting

| Name (Mkt Cap) | RNS | Summary | Our view (Author) |

|---|---|---|---|

AstraZeneca (LON:AZN) (£216bn | SR75) | Q1 revenue up 13%. 2026 guidance is unchanged. | ||

GSK (LON:GSK) (£82bn | SR94) | Q1 revenue up 2%, 2026 guidance unchanged. | ||

Lloyds Banking (LON:LLOY) (£58bn | SR76) | Pre-tax profit up 33% to £2bn, 2026 guidance unchanged. | ||

HALEON (LON:HLN) (£31bn | SR59) | Q1 organic revenue up 2.2%, 2026 guidance unchanged. | ||

Prudential (LON:PRU) (£28m | SR47) | Q1 new business profit up 10% to $686m. “We remain confident in delivering double‑digit growth across our key financial metrics in 2026 and achieving our 2027 financial objectives." | ||

St Jamess Place (LON:STJ) (£6.5bn | SR65) | Q1 net inflows of £1.53bn, 31 March 2026 AUM of £216.9bn. | ||

Melrose Industries (LON:MRO) (£6.1bn | SR39) | Q1 revenue up 11% with improved profitability. 2026 guidance remains unchanged, assuming no further impact from Middle East conflict. | ||

Glanbia (LON:GLB) (£3.7bn | SR92) | Q1 revenue up 5.4%, FY 2026 adjusted EPS expected to be at the upper end of medium-term guidance of 7% to 11% constant currency. | ||

Frasers (LON:FRAS) (£2.9bn | SR88) | Acquired two major UK retail destinations with a combined annual footfall of almost 7.8m visitors and 420k sq ft of space. | ||

Primary Health Properties (LON:PHP) (£2.4bn | SR60) | Good progress with Assura integration, with LTV below 50% and £9m of annualised cost synergies. Also progressing with establishing a new vehicle for the private hospital portfolio. Progressive dividend policy remains unchanged. | ||

Jet2 (LON:JET2) (£2.0bn | SR57) | FY26 results to be in line with market expectations, with operating profit between £435m and £440m. Load factor in Q1 FY27 has been in line with the prior year. Later bookings mean visibility for the peak summer season is currently limited. | BLACK (AMBER/GREEN ↓) (Roland) I’m reluctant to downgrade our view of this business at all, but I feel I have no choice given that today’s profit warning has reduced FY27 earnings forecasts by a third. This is particularly frustrating as there was no commentary on profit expectations in the trading update – only investors with access to today’s broker note are likely to realise the scale of the downgrade. The main issue seems to be limited visibility on summer bookings. Travellers are leaving it late to book and there’s a risk some will opt for a staycation. While Jet2’s fuel position is well hedged, shortages remain a risk, as do longer-dated price rises. On balance, I think Jet2 remains an excellent business that’s too cheap. However, today’s downgrade suggests near-term disruption could now be more severe than previously expected, so I’m moderating our view slightly to reflect the greater risks involved. | |

RHI Magnesita NV (LON:RHIM) (£1.27bn | SR73) | Full-year guidance reconfirmed: adjusted EBITA of approximately €435 million on a constant currency basis (approximately €400 million including foreign exchange headwinds). | ||

Breedon (LON:BREE) (£1.06bn | SR61) | Q1 revenue rose by 5%, or 2% LFL with trading in line with expectations. | ||

Elementis (LON:ELM) (£856m | SR56) | Q1 revenue up 2%, with improved profit and margins. Full year expectations unchanged. | ||

Oakley Capital Investments (LON:OCI) (£791m | SR68) | NAV per share of 758p, with a total NAV return per share of 2.7% (+20p) during the period. Total shareholder return of -18% amid wider market sell-off. | ||

Aston Martin Lagonda Global Holdings (LON:AML) (£404m | SR32) | Q1 2026 in line with guidance, with revenue up 16% and operating loss reduced to £(8.9)m. Full year guidance unchanged. | RED = (Graham) [no section below] The only thing consistent about this stock is its ongoing losses. Adjusted EBIT of minus £56.9m in Q1 continues the trend here. Net debt rises to £1.46 billion (Dec 2025: £1.38 billion), several multiples of the market cap. The positives are that ASP has increased, leading to a higher gross margin on higher revenues, and the outlook statement guides for "material improvement" in financial performance this year. However, the damage has already been done in terms of the balance sheet and so I would continue to avoid this. | |

Ecora Royalties (LON:ECOR) (£342m | SR72) | Q1 portfolio contribution up 105% vs Q1 2025, supported by base metals portfolio +152%. | ||

Puretech Health (LON:PRTC) (£316m | SR60) | Final Results & Voluntary Delisting of Nasdaq Depositary Shares | Cash and short-term investments of $277.1m at 31 Dec 25 and $248.1m at 31 March 2026. Operational runway “at least through the end of 2028”, inclusive of participation in expected Founded Entity fundraisings. | |

Altyngold (LON:ALTN) (£312m | SR90) | Revenue up 82% to $175.4m with after-tax profit of $62m (2024: $26.4m). 2026 outlook: production target of 50k oz gold and ore processing capacity of 1Mtpa. | ||

Halfords (LON:HFD) (£293m | SR82) | Strong trading with FY26 profit expected around the upper end of expectations (consensus range: £36m to £41.2m). FY27 Outlook: comfortable with consensus expectations for underlying PBT of £42m to £48.6m. | AMBER/GREEN = (Roland) Today’s year-end update provides a further nudge higher for FY26 expectations and reiterates guidance for further profit growth this year. CEO Henry Birch appears to be doing a solid job, but the long-term decline in profitability, high cost base and slim margins mean I don’t have the conviction to upgrade our view to be fully positive. A forward P/E of around 10 seems about right to me, so I’m leaving our previous moderately positive view unchanged today. | |

Sylvania Platinum (LON:SLP) (£251m | SR94) | Declared 22,853 4E PGM oz in Q3, exceeding targets. Likely to achieve or exceed the upper end of the previously increased PGM production guidance of 90,000 to 93,000 4E PGM ounces, announced in Q2 FY2026. | ||

Helical (LON:HLCL) (£227m | SR43) | Exchanged contracts for a further 10k sq ft of fitted space at The Bower, with a further 22k sq ft under offer. This would take occupancy at The Bower to 96.6%. | ||

Falcon Oil & Gas (LON:FOG) (£183m | SR29) | The definitive agreement entered into between Falcon and Tamboran Resources is progressing and is expected to close in the second quarter of 2026. 2025 loss $2.6m. Cash of $1.3 million. | ||

Warpaint London (LON:W7L) (£151m | SR61) | Revenue +3%, adjusted EBITDA -15% (£21.3m), PBT -24% (£18.1m). The difficult trading conditions experienced in 2025 continued in Q1 2026. Sales in the first four months of £26.1m vs. £32.6m last year. | BLACK (AMBER/RED =) (Roland) | |

Galantas Gold (LON:GAL) (£178m | SR25) | Canadian dollars: net loss $8.5m (2024: $1.5m). Cash balance £13.3m. | ||

Keystone Law (LON:KEYS) (£151m | SR60) | 2026 results marginally ahead of market expectations. “The Board remains confident that Keystone will continue to deliver strong, sustainable growth and expects adjusted PBT to be ahead of current market expectations for 2027.” | GREEN ↑ (Graham) | |

Mincon (LON:MCON) (£129m | SR91) | SP +2% The Group has successfully carried forward the positive momentum from 2025 into the first quarter of 2026. No change to forecasts at ShoreCap. EPS forecast 3.9 euro cents in 2026, then 4.8 euro cents in 2027. | GREEN ↑ (Graham) [no section below] Congrats to shareholders here who have seen a big jump in the share price since I covered it last. A strong construction sector in North America, combined with a global mining boom, have changed the market’s perception of what this drilling equipment company is worth. The company itself has helped out by beating FY25 Dec 2025 forecasts with its results last month. Adj. PBT came in at £7.4m, vs. £5.6m forecast by ShoreCap. However, I note that FY26 forecasts haven’t budged. As with Keystone, I’m a little concerned about valuation at this level, with a PER of about 18x.However, I won’t fight the momentum - this is a company I always thought had the potential to come good, and it’s enjoying a nice recovery now after a tough few years. | |

Mercia Asset Management (LON:MERC) (£125m | SR59) | Warwick Acoustics Limited, one of MERC’s direct portfolio companies, is supplying components for an automotive electrostatic audio system. The "SV Electrostatic Sound" system was announced today by Range Rover. MERC directly owns 30.7% of Warwick Acoustics. | GREEN = (Graham) [no section below] | |

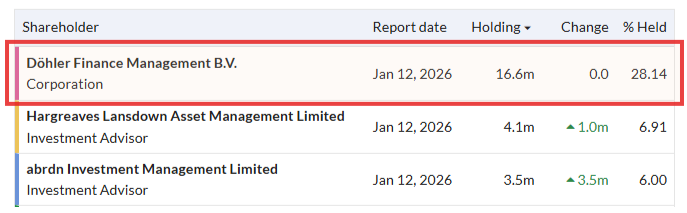

Treatt (LON:TET) (£121m | SR52) | Half Year Results & Recommended cash acquisition of Treatt plc | Recommended cash offer from Döhler Group SE for 305p per share, a 48% premium to yesterday’s closing price. | TAKEOVER (Graham) |

Roadside Real Estate (LON:ROAD) (£111m | SR24) | £14 million proceeds from the put option with CGV now expected to be received by the end of May 2026. The acquisition of DAR will complete shortly after receipt of the funds. The acquisition of HOCH remains on track to complete by 31 May 2026. | ||

Berkeley Energia (LON:BKY) (£102m | SR15) | Continued to advance its ongoing exploration initiative targeting critical minerals in Spain at its Conchas project. Berkeley Exploration Limited remains committed to the Salamanca Project and continues to be open to a constructive dialogue with Spain re: permitting situation. | ||

Trifast (LON:TRI) (£90m | SR87) | FY26 underlying EBIT expected to be in line with market expectations. As a result of the closure of the Malaysian manufacturing operation and on-going conflicts in the Middle East, FY27 revenue will be reduced by c.£8.0m. | ||

Orosur Mining (LON:OMI) (£77m | SR14) | Columbia (Anza Project): completed its in-fill drilling program at Pepas and has declared a Maiden Resource Estimate of 219,000 ounces of gold. Cash balance $13.65m. 9-month net loss $6.6m. | ||

Pebble (LON:PEBB) (£77m | SR97) | FY 26 outlook remains in line with market expectations. | ||

Arrow Exploration (LON:AXL) (£64m | SR83) | Net income of $1.4 million including $7.6m impairment. Total oil and gas revenue $70.5m. 13% increase in annual average production to 4,012 boe/d. Arrow has a fully funded 2026 work program totaling $24 million targeting up to nine new wells in the Tapir block. | ||

Alternative Income REIT (LON:AIRE) (£60m | SR58) | NAV fell 0.1% from the previous quarter including the effect of 1.4p dividend. NAV total return 1.5%. Board remains confident in AIRE's ability as a standalone entity, to generate secure and predictable income returns, whilst maintaining capital value. | ||

Watkin Jones (LON:WJG) (£59m | SR59) | HY 2026 operating profits are expected to be at a similar level to HY 2025. “Whilst the adverse movement in the UK interest rate outlook since early March has created greater uncertainty with regards to future transactional liquidity conditions, the Group will continue to be agile in optimising its pipeline whilst continuing to diversify its revenue streams.” | ||

Chapel Down (LON:CDGP) (£54m | SR5) | Net sales revenue +19% (£19.4m), adjusted EBITDA (excluding fair value adjustment to biological produce) +25% to £3.7m. PBT £0.5m. Currently expects FY26 results to be in line with market expectations. | ||

Naked Wines (LON:WINE) (£49m | SR86) | FY26 performance is in line with previously communicated guidance. Will recognise £2-3m non-cash adjusted item relating to transition to new digital platform. Will provide guidance on FY27 with the audited FY26 results in the summer. | ||

Skillcast (LON:SKL) (£46m | SR48) | ARR +19% (£13.8m). EBITDA +200% (£1.5m). Cash in bank £12.7m. “Growth rates have moderated to around 15% due to slower decision-making as a result of the global uncertainty, particularly among larger clients… The Group remains confident of meeting EBITDA expectations through productivity improvements and continued operational leverage.” | ||

Sanderson Design (LON:SDG) (£46m | SR89) | Revenue down 1% (£99.5m). Adjusted underlying EPS +37.5% (5.39p). “...entered FY2027 with good momentum which has been maintained and current trading is in line with full year expectations.” | ||

Star Energy (LON:STAR) (£22m | SR91) | Net production averaged 1,886 boepd in 2025 with downtime driven by a number of discrete events which have now been resolved. Outlook: anticipate net production of c.2,000 boepd and operating costs of c.$44/boe. | ||

Vianet (LON:VNET) (£18m | SR77) | “A resilient financial performance”. Turnover £15.5m (FY25: £15.3m), adj. EBITDA £3.61m (FY25: £3.59m). Hires new CEO internally. Outgoing CEO returns to position as Chair. Enters the new financial year “with conviction”. | ||

Zoo Digital (LON:ZOO) (£12m | SR69) | Expects to report FY26 Adjusted EBITDA of at least $3.8 million in line with market expectations. | ||

Total Graphite (LON:TGR) (£11m | SR6) | Announces the successful proof of concept and ongoing development of its newly launched business trading in high value, downstream processed graphite materials. First step towards a fully vertically-integrated, commercial business model. | ||

Medpal AI (LON:MPAL) (£10m | SR1) | Acquires a second pharmacy facility to support the growth in its pharmacy operations through its subsidiary MedPal Limited. Total cash consideration £310k. |

Graham's Section

Treatt (LON:TET)

Up 45% at 299.5p (£177m) - Recommended Cash Acquisition - Graham - TAKEOVER

We have a recommended offer and this time it’s at 305p.

Last year, there were bids at 260p and 290p that were voted down.

Treatt’s major shareholder Döhler blocked the 290p bid, having built a stake that was large enough to prevent a “scheme of arrangement”:

Döhler today offers to take over the company itself, at 305.

This is a 48% premium to the prevailing share price.

However, I think it’s more interesting that it’s just a 5% premium to what Natara Global were willing to pay.

But Döhler and Treatt have a strong relationship:

The Döhler Group has a deep understanding of the Treatt Group's business, having worked closely with the Treatt Group over many years as a strategic supplier and customer, and these insights have allowed the Döhler Group to develop a differentiated perspective on the Company.

It’s also interesting to note what Döhler said back in September 2025, when it was building its stake (emphasis added):

Döhler views Treatt as a high-quality company and recognises its strong position in the natural extracts and flavours market. Döhler is supportive of the strategy outlined by Treatt and looks forward to building a constructive dialogue with the Döhler executive management team. Döhler intends to hold its shares in Treatt for investment purposes.

Döhler confirms that it is not considering an offer for Treatt.

How much has changed in seven months!

This is what they say today:

Whilst the Döhler Group remains supportive of the strategy outlined by Treatt and recognises the recent steps taken to stabilise the operating performance of the Company, it believes that public markets are unlikely to provide the necessary support to the Company to deliver its strategy due to the public markets' focus on short-term performance.

Döhler firmly believes that it would be the right partner to unlock the full extent of the Treatt Group's growth potential as its support and advanced distribution capabilities will provide the Company with the platform and flexibility to accelerate the execution of its long-term strategic agenda in a privately-owned setting.

Shareholder support: letters of intent to support the takeover have been received from shareholders holding 12% of Treatt. That might not seem like much, but the bid from Natara had even lower support - only 6.3%.

Half Year Results

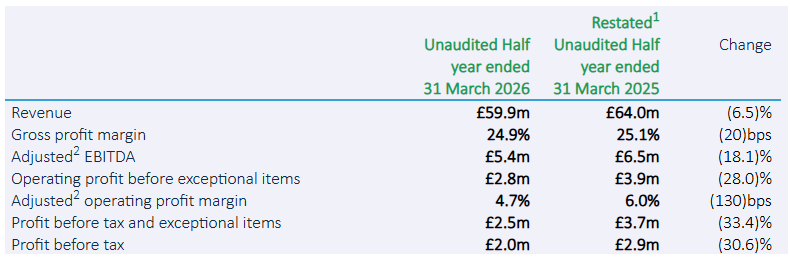

Today’s interim results are overshadowed by the takeover news, and they are pretty uninspiring.

“The reduction in profit was mainly due to lower sales, led by lower citrus sales and challenging market conditions in North America.”

Graham’s view

With the share price at nearly 300p this morning, and with a recommendation from the Board to support the majority shareholder, this deal must be considered very likely to go through.

Unfortunately, it’s been a lost decade for Treatt shareholders:

At least there has been a steady stream of dividends over this time period - I calculate about 60p since 2016. If shareholders had reinvested them in Treatt itself, or in something else that has performed better, they should have done ok.

But the profit result in 2025 was lower than what the company achieved in 2016, even before adjusting for inflation. It seems that competition did eventually catch up with the business, turning it from a solid investment into a fairly mediocre one.

Keystone Law (LON:KEYS)

Up 9% at 517.4p (£164m) - Final Results - Graham - GREEN ↑

Back in February, at the full-year trading update, I took a moderately positive stance on this listed law firm.

While I had a really positive impression of the business, I balked at the valuation.

The FTSE is lower by 4% since then, and the Keystone share price has underperformed it, falling by 11%:

That calculation is even after taking into account today’s ahead of expectations update.

So I think it’s reasonable to say that the valuation back then was indeed a little punchy.

But where do we go from here?

Here are today’s highlights for FY January 2026:

Revenue +17.9% (£115.2m)

Adj. PBT +20.6% (£15.3m)

61 new Principals added, bringing the total to 491.

These results are considered to be marginally ahead of expectations (revenue £114.3m, adj. PBT £15.1m).

Net cash £9.7m

The focus on technology and AI persists:

Ongoing implementation and evaluation of IT infrastructure to drive real impact for our lawyers and the broader business

Rolled out several AI initiatives to enhance our offering to lawyers, including deploying secure, locked-down versions of ChatGPT and Claude and adopting the NetDocuments AI extension

Outlook is strong:

The Group has made a positive start to 2027 with client demand and recruitment activity remaining positive during Q1 2027

The Board remains confident that Keystone will continue to deliver strong, sustainable growth and expects adjusted PBT to be ahead of current market expectations for 2027

Estimates

According to the company, expectations for FY2027 are considered to be revenue £122.3m and adj PBT £15.1m.

That adj. PBT forecast is the same as the 2026 forecast, so I would have considered it a little disappointing if they had only managed to match that.

Panmure Liberum has a new revenue forecast of £123m, and adj. PBT forecast of £15.7m.

Balance sheet

There are net assets of £20.7m, mostly tangible (only £5m of intangible assets).

Net cash, as noted above is £9.7m.

The company points out that £11.6m was paid to shareholders in the form of dividends during the year. So effectively all of the company’s net profit got paid out to shareholders.

Graham’s view

The question for me today is whether I need to go fully GREEN on it.

Before getting into that, I’d just like to point out that the “real” PBT figure is £14.7m, not £15.3m. Share-based payments are running at about £800k p.a.

Assuming that holds true again in FY27, the £15.7m adjusted PBT forecast says to me that we could be looking at net income of about £11.2m (after share-based payments and tax).

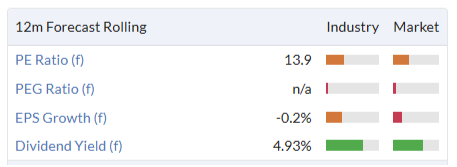

This gives me a P/E multiple of 14.5-15x, just a little higher than what’s on the StockReport:

As a value investor at heart, it’s not easy for me to get enthusiastic about a law firm trading at this level, no matter how well it’s performing.

The ValueRank is only 42:

To square the circle - reconciling my value instincts against a high-performing but possibly overvalued law firm - I’m going to go GREEN on this today.

However, that positive stance is going to come with a condition: if the stock price gets to 600p by the next time I cover this, and there haven’t been any further upgrades, I’ll be returning to a more conservative stance.

I think this respects the strong trading update today, while also being clear that I don’t see a massive amount of value on offer here!

Roland's Section

Warpaint London (LON:W7L)

Down 7% at 175p (£141m) - Results for the year ended 31 December 2025 - Roland - BLACK (AMBER/RED =)

This cosmetics business warned on 2025 profits in February and has now cut its guidance for 2026.

Mark’s concerns over trading visibility for 2026 have proved to be well founded. Today’s outlook reports “difficult trading conditions” in Q1 and guides for a heavier second-half weighting to profit than in previous years.

As a result, house broker Shore Capital has cut its 2026 EPS forecast by 8% this morning.

Let’s take a look.

FY25 results summary

Today’s top-line figures show revenue growth last year, but when the £11.8m contribution from the Brand Architekt acquisition in February 2025 is stripped out, sales fell sharply:

Revenue up 3% to £105.1m

Organic revenue down 8% to £93.3m

Adjusted EBITDA down 15% to £21.3m

Pre-tax profit down 24% to £18.1m

Adjusted EPS down 25% to 16.7p

Net cash up 102% to £16m

Dividend up 18% to 13.0p per share

Trading commentary: Warpaint says it experienced a “challenging trading environment across many of the Group’s markets”. The company’s products are sold at relatively low price points and its customers were affected by cost-of-living pressures last year (my emphasis):

While revenues were affected by subdued consumer confidence, underlying demand for the Group's brands remained encouraging. In several instances volumes increased year-on-year, with consumers increasingly favouring lower price points within the product range as they adjusted spending patterns in response to broader economic pressures.

A breakdown of trading by brand highlights broad-based weakness:

W7: total W7 sales fell by 2% to £63.9m, accounting for 61% of total revenue (2024: 64%).

W7 sales fell in all regions: UK -5%; EU -2%; US -25% due to tariff-related disruption.

Technic: sales fell by 15% to £25.3m, due partly to the closure of Bodycare.

White label manufacturing was also scaled back, with revenue falling by 63% to £1.6m.

Brand Architekts: sales of £11.8m, with an adjusted EBITDA contribution of £0.8m since acquisition on 12 February 2025. This represents a much lower profit margin than the remainder of the business, but BA was loss-making when acquired and is being improved. 2026 is expected to see further gains in profitability.

US tariffs: the company says tariffs disruption hit in April/May when retailers were looking to place Christmas orders. The situation is said to have improved since then, so perhaps we can see this as a one off issue?

As tariffs have stabilised, albeit at higher than historic levels, we continue to see significant opportunities in the US.

More broadly, today’s commentary highlights additional store placements in a number of major UK retailers last year:

In the second half of 2025, W7 was rolled out into an additional 140 Superdrug stores and launched accessories into 250 Boots stores, along with a Christmas gift offering going into 350 Boots stores for the first time. W7 also expanded its impulse offering into a further 150 Tesco stores.

Balance sheet, cash flow & profitability

The adjustments reported with today’s figures don’t cause me any serious concerns. Profitability and cash flow have generally been very strong in this business, so I’m more interested in understanding if this situation continued in last year’s more difficult conditions:

Operating margin: 18% (2024: 24%)

Return on Capital Employed: 21% (2024: 31%)

Free cash flow: £10.8m (c.100% conversion from adjusted net profit)

These figures show a decline in profitability last year, but they’re still high enough to score very well for quality.

Cash conversion was also excellent, when adjusted for the non-cash gain on bargain purchase relating to Brand Architekts. This kind of situation rarely arises, but suggests savvy buying by Warpaint founder and CEO Sam Bazini:

The gain on bargain purchase arose principally because, at the acquisition date, Brand Architekts was loss‑making and experiencing ongoing cash outflows, which adversely affected its valuation and resulted in the business being acquired at a price below the fair value of its identifiable net assets.

Net cash: Warpaint has no debt (except leases) and reported a year-end net cash position of £16m.

This figure is double the £8m reported at the end of last year, but checking the accounts shows that 2024 saw £8m of working capital outflows. Netting this out simply highlights the quality of cash generation here, in my view – although I would note that there’s clearly a lot of seasonality to the group’s cash position.

Today’s cash flow statement shows £242k of interest received in 2025, with 152k of interest paid. The commentary confirms that Warpaint has bank facilities available to help fund working capital movements. Reassuringly, these were reduced last year and were unused at the end of the year:

Accordingly, the Group maintains an £8.0 million invoice and stock finance facility (2024: £9.5 million), and a 'general purpose' £1.0 million facility (2024: £5.0 million); both facilities were reduced at the Company's request during 2025. At the year end, both facilities were unused and the balance outstanding was £nil (31 December 2024: £nil).

Given the group’s strong year-end net cash position, seasonal use of these facilities doesn’t worry me too much.

2026 outlook & updated forecasts

Today’s guidance flags up a number of potential positives for the year ahead:

“Significantly improved Christmas order received from Walmart”;

Expansion of European footprint with a capsule range of W7 products being launched in 2,200 Dirk Rossmann stores in Germany;

Recent acquisition of the Barry M brand for £1.4m provides further opportunities in the group’s core market segments.

However, Warpaint has seen a slow start to the year, with revenue for the four months to 30 April expected to be £26.1m. That’s 20% below the same period last year, when sales totalled £32.6m.

April has seen some “signs of recovery”, with sales expected to exceed those in April 2025. This suggests to me that Q1 must have been really quite bad.

Management hopes to be able to make up some of the Q1 shortfall with stronger trading later in the year (my emphasis):

Sales in 2026 are expected to be more second half weighted than prior years due to the timing of certain larger orders and planned customer rollouts from May 2026.

At this stage in the year, we have no way of knowing whether the H2 weighting will come good or not. But our experience is that these situations can increase the risk of a profit warning much later in the year.

Broker update: Warpaint London’s house broker Shore Capital is certainly taking a more cautious view and has cut its 2026 and 2027 forecasts today.

2026E

Revenue £108m (-10% vs £119.6m previously)

Adj EPS: 20.0p (-8% vs 21.7p previously)

2027E

Revenue: £113.3m (-10% vs £125.4m previously)

Adj EPS: 21.1p (-9% vs 23.3p previously)

Warpaint’s share price is down by 7% at the time of writing, broadly matching the reduction in EPS estimates today. That leaves the stock on a broadly unchanged forward valuation:

Roland’s view

Today’s downgrade marks the second profit warning this year for Warpaint London. The company appears to have had a poor start to the year and the reliance on an H2 weighting increases the risk of a further downgrade if hoped-for improvements don’t materialise.

We took a moderately negative view on this business following February’s warning (9/2) and the shares have continued to decline since then:

However, the StockRank has risen since then and the valuation of this business now seems quite modest to me, given the strong balance sheet, double-digit profitability and well-supported 6% dividend yield.

Out of respect for our rules I am going to maintain our AMBER/RED view today, but I also have some sympathy with the StockRanks’ Contrarian styling. I think this founder-led business could be worth watching at current levels for any sign of an improving outlook.

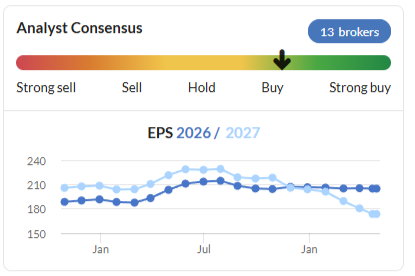

Jet2 (LON:JET2)

Up 1.7% at 1,085p (£2.08bn) - Trading Update - Roland - BLACK (AMBER/GREEN ↓)

Airlines and holiday operators are among the businesses with most immediate exposure to the surging price of jet fuel and the situation in the Middle East. So today’s profit warning from Jet2 is not surprising.

What is disappointing is that this cut to FY27 earnings forecasts has been slipped out through the company’s broker, without being disclosed in today’s FY26 trading update. While we have access to today’s broker note, many investors won’t, creating an uneven playing field.

With that said, let’s take a look at today’s update.

FY26 trading update

The first part of today’s update reiterates guidance for the year ended 31 March 2026:

Operating profit of between £435m and £440m, in line with current market expectations.

Year-end net cash of £2.0bn

Canaccord Genuity 2026E adj EPS estimate 226.4p (previously 222.2p)

What’s more interesting at this stage is the outlook for the current year.

FY27 trading update

Jet2 continues to expand and says capacity on sale for this summer is currently 7.7% higher than last year, at 19.9m seats.

Passengers booked to date are up by 6.2%, suggesting capacity uptake is running slightly behind availability.

Aircraft load factors (occupancy) for Q1 (April-June) are said to be in line with last year, but the company says events in the Middle East have caused “the booking profile [to] become increasingly close to departure”.

This means that visibility for the summer season is limited. There’s clearly a risk that staycations will surge and fewer people will opt to travel abroad.

Reassuringly, 87% of the airline’s summer jet fuel requirements have been hedged at an average price of $707 – around half the current market price of nearly $1,500/t.

Of course, price isn’t the only issue – shortages are a possibility if exports from the Strait of Hormuz remain restricted.

Outlook

The FY27 commentary in today’s update makes it clear that some weakness is possible in summer trading. But I am not sure a reasonable reader would assume a 32% cut to FY27 earnings forecasts.

This is the position put forwards by Jet2’s joint broker Canaccord Genuity today – many thanks for making this available on Research Tree:

FY27E adj EPS: 127.4p (-32% vs 187.7p previously)

FY28E adj EPS: 222.4p (+3% vs 216.9p previously)

Consensus estimates have already trended steadily lower this year, but these forecasts are likely to signify a further drop for FY27:

Today’s revised forecasts leaves Jet2 trading on a FY27E P/E of 8.5, falling to a P/E of 4.9 for FY28E.

Roland’s view

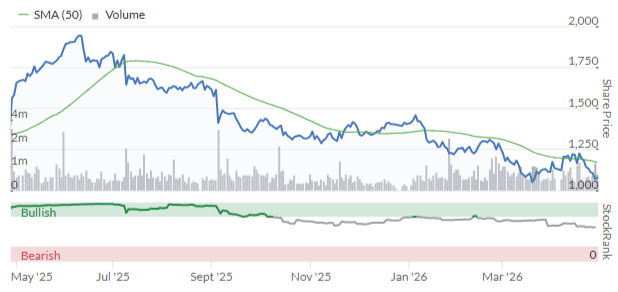

The market has remained unmoved by today’s news, perhaps because Jet2’s share price has already fallen by 44% from last year’s high of 1,945p:

I can certainly see the logic in arguing that Jet2’s strong balance sheet, proven strategy and modest valuation are enough to offset the expectation of a single bad year.

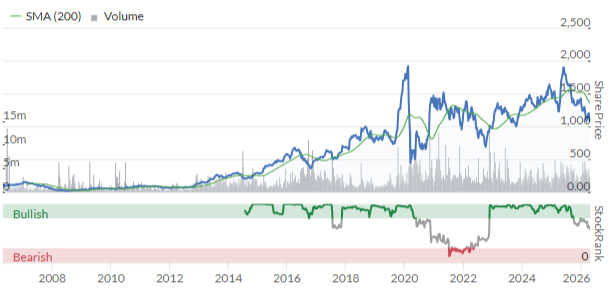

In my view, this business is well run and has an excellent record of generating long-term growth for shareholders. Even at current levels, Jet2’s share price has 10-bagged since 2006 – equivalent to a 12% annualised gain:

Too cheap? Right now, Jet2 shares are trading in line with their last-reported book value of 1,028p per share, despite a post-Covid average return on equity of nearly 30%. That’s very cheap, unless future profitability becomes permanently impaired – something I think is unlikely.

For chart watchers, the stock is also trading on a long-term trend line that was barely even broken during the Covid pandemic, when airlines shut down completely.

Unless the situation in the Middle East worsens significantly and prevents a FY28 recovery, I struggle to see too much downside from current levels.

For this reason I am only going to downgrade Graham’s previous GREEN view by one notch today, to AMBER/GREEN.

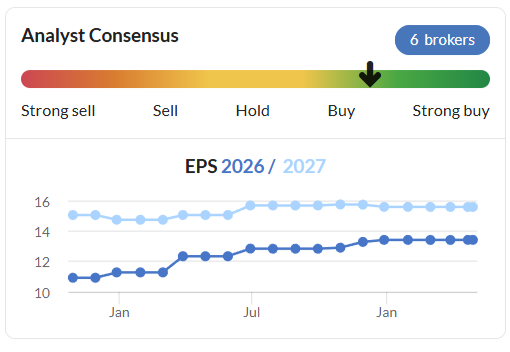

Halfords (LON:HFD)

Up 10% at 147p (£323=2m) - Trading update for the financial year to 3 April 2026 - Roland - AMBER/GREEN =

Halfords Group plc (“Halfords” or “the Group”), the UK’s leading provider of motoring and cycling products and services, is pleased to provide a strong trading update ahead of its FY26 results.

Today’s update from this well-known retailer is short but sweet, with two key pieces of information:

FY26 update (y/e 3 April): adjusted pre-tax profit for the FY26 financial year is expected to be “around the upper end of the consensus range of £36.0 to £41.2m”;

FY27 outlook: profits are expected to continue rising during the current year, despite the obvious headwinds – “we are currently comfortable with consensus expectations for FY27 underlying PBT of £42.0m to £48.6m”.

I think there are a few details worth noting from today’s commentary:

Like-for-like sales rose by 4.8% last year, with Motoring LFL +2.9% and Cycling LFL +6.4% – it seems the post-pandemic cycling slump may be easing;

Gross margins improved, while costs were “well managed”;

The “majority” of Halfords’ FY27 energy costs and currency requirements are hedged, as are most freight rates. This should reduce volatility as a result of the situation in the Middle East.

Roland’s view

Profit expectations for FY26 were upgraded multiple times. The end result was that consensus EPS estimates rose by 23% in 18 months. I think this reflects creditably on the group’s turnaround under CEO Henry Birch:

Today we have a final nudge higher for FY26, with profits expected to be at the upper end of guidance.

It’s too soon to know whether we will see a similar pattern of upgrades for FY27, but progress does seem encouraging, with Halfords controlling the things it can control and continuing to benefit from its scale and market share.

When Graham reviewed November’s interim results he took an AMBER/GREEN view. He noted Halfords’ slim profit margins and suggested a P/E of around 10x might be fair for this type of business.

I share this view. Even at an adjusted level, I think Halfords’ operating margin is only likely to be around 3% this year. Returns on capital are also low.

While the company seems to have done a good job offsetting higher minimum wage and National Insurance costs, its dependence on a 12,500+ workforce means these pressures may persist.

More broadly, I think the long-term record for this business suggests a relentless and only partly-successful struggle against rising costs and competitive pressures.

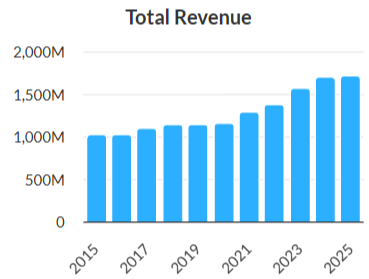

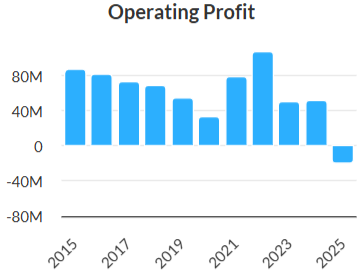

While revenue is 70% higher than 10 years ago…

… profits have generally trended lower, reflecting declining margins:

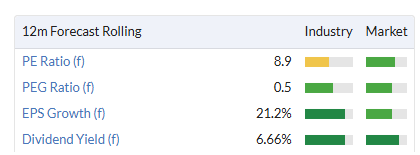

Today’s 10% share price gain means Halfords’ FY27E P/E has now risen to c.10x, in line with the valuation when we last covered the stock.

While the 7% dividend yield is covered and suggests some value is on offer, the group’s low profitability and exposure to the consumer economy mean that I’m going to leave our previous AMBER/GREEN view unchanged today.

See what our investor community has to say

Enjoying the free article? Unlock access to all subscriber comments and dive deeper into discussions from our experienced community of private investors. Don't miss out on valuable insights. Start your free trial today!

Start your free trialWe require a payment card to verify your account, but you can cancel anytime with a single click and won’t be charged.