Good morning,

There are two reports today, this one from me, and an additional report from Graham - here - he's running a bit late today, due to a late flight last night. So his report won't be finished until later this afternoon.

Today I shall be reporting on;

- Joules - Xmas trading update

- ShoeZone - preliminary results

Graham will be reporting on;

- McBride

- Sigma Capital

- Foxtons

Yesterday's report - I had a late surge, and added loads more companies to it, in the evening. So I reported on a total of 11 companies. Here is the link to review that report.

Thanks for all the reader comments - these are an increasingly valuable part of the whole thing. I very much welcome intelligent, interesting reader comments. Feel free to disagree with me too - well-argued bear points are particularly welcome.

"Market expectations" clarity in RNSs

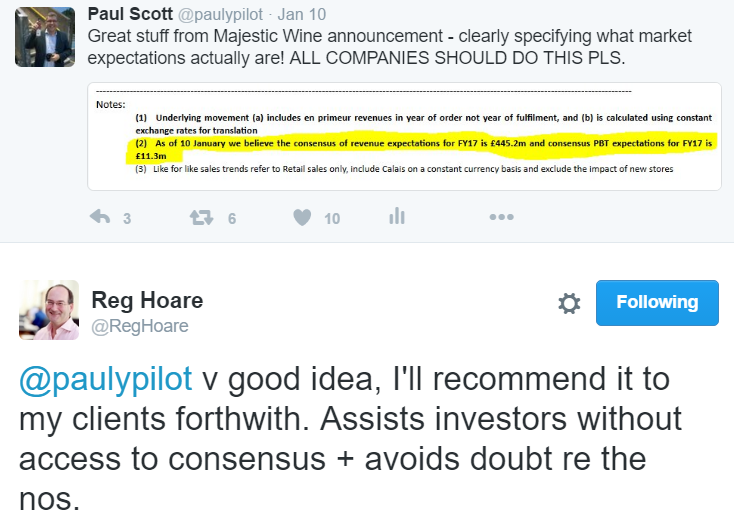

Before I get started on the companies, a quick hat tip (see Tweets below) to Reg Hoare of MHP Communications. Reg is one of my favourite PR people, as he's very responsive to private investors, and recognises our importance in creating liquidity & setting share prices.

Why do I talk to PR people at all, you may ask? Well, despite being much maligned, they're actually very helpful, I find. They give me access to companies that I wish to speak to & meet. They often email me broker notes on results day, and presentation slides which the Instis are given. Also they are sometimes receptive to grumbles I have about the wording of RNSs, etc. So my aim is to improve things for everyone, where possible, by giving useful feedback to the PR companies. Lots of them read my reports too!

For these reasons I'm happy to have a co-operative relationship with quite a few PR firms. I resist their charms when they try to change my views on companies, unless they present reliable facts & figures to support their argument. In those cases, I try to keep an open-mind & am willing to change my mind if the facts suggest that is the correct thing to do.

Also they all now know that it's a waste of time to try to get me interested in blue sky, or jam tomorrow shares!

Going back to Reg, he responded positively to my suggestion yesterday that all companies should clearly state in their trading updates the specific figure for market expectations.

Majestic Wine (LON:WINE) did that in their RNS yesterday, and it's so helpful, top marks to them & their advisers.

I'm pushing to ask all companies to follow suit. Anyway, this was my Tweet, and Reg's response;

Isn't that great?! Well done Reg. On this issue, I will be bending the ears of other PR people, and brokers, and in fact anyone who will listen! It's such a quick & easy fix, to make life easier for investors. There is no downside, or risk. If we have clarity, we're more likely to buy a share too, so it makes sense to improve trading updates for the end users.

Shoe Zone (LON:SHOE)

Share price: 182.5p (unchanged today)

No. shares: 50.0m

Market cap: £91.3m

(at the time of writing, I hold a long position in this share)

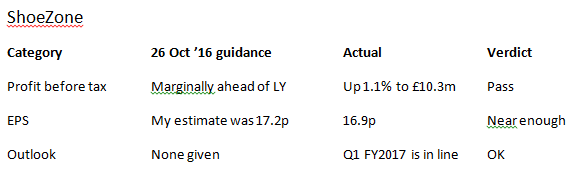

Results 52 wks ended 1 Oct 2016 - the figures for this discount shoe retailer were pre-announced in a trading update, which I reported on here, on 25 Oct 2016. So I'll now compare that trading update with the actual figures today.

(NB. the table below is my personal notes, created by me, it's not from the RNS)

Please bear in mind that my estimate of 17.2p EPS above was not from the company, it's just what I deduced from the trading update in Oct 2016, and broker notes.

So this looks OK. A bit more detail;

- Gross margin - excellent, at 62.0% (LY 61.5%) - can this be maintained though, as forex cost pressures mount? In narrative, company reassures that GM can "broadly" be maintained.

- Online sales up 11% (should be more). I can't find a figure for total, or what proportion of grand total, so assume it's not particularly high.

- Growth in international sales online - encouraging, but need figures on this to assess important.

- Short leases - this is a key competitive advantage, which I like very much. Average length is only 2.6 years. This means company has flexibility to relocate, and take advantage of "trend of falling rents".

- Business rates - company says it will be a net beneficiary from the recent revaluation - good news.

- Balance sheet - very solid, with plenty of cash. Although note pension deficit has risen significantly and £0.6m annual cost is going to rise.

- Family-controlled, so a takeover bid is very unlikely, unless they want to sell out. If they do, then it would have to be at a decent premium.

- Dividends - very generous - 6.8p final, plus 8.0p special divis are in the pipeline.

- Cash generation - very good, and anything above £11m is paid out to shareholders, a terrific discipline (similar to Somero Enterprises Inc (LON:SOM) yesterday)

- Current trading - in line with expectations. They're up against soft comps though, as last year's H1 was poor.

My opinion - I like it a lot. However, it's a mature business, so where's the growth going to come from? In current market conditions, I doubt there is much upside on this share price - the market isn't interested in mature retailing businesses right now - it wants fast growing ones.

That said, the income from divis here is smashing.

I've dipped my toe in, with a small purchase this morning. My intention is to research it in more depth, and think about it more, before deciding whether to buy any more. I doubt this will become a significant holding for me, it's more a dabble, and to generate a bit of dividend income.

Based on the bullet points above, I think Shoe Zone should be able to cope with more depressed retail conditions in 2017 far better than many others. That's mainly due to its variable (and reducing) costs on shop leases, and an apparent ability to maintain margins. I like that it's a really entrepreneurial business, run by a family who clearly know what they're doing, and are experienced.

That said, I don't see much excitement being likely with this share, and it could even drift down, in current market conditions. I would buy more if it dropped significantly.

EDIT: I forgot to mention, FinnCap has put out a rather downbeat note today, saying it's going to reduce its forecasts. Another broker has put out forecasts which show negligible profit growth over the next 2 years.

Therefore I think we should work on the basis that profit is likely to be flat, or maybe down a little in the short to medium term. I think they're perhaps being a little too negative. Sure, SHOE is subject to the same wage cost pressures as everyone else. However, it has mitigated cost increases from the forex issue, so it says, and is also able to manage down its rent+rates costs, unlike most other retailers.

So to my mind, this company is more likely to weather any storm in weaker consumer confidence, than most other retailers.

Joules (LON:JOUL)

Share price: 226p (up 3.2% today)

No. shares: 87.5m

Market cap: £197.8m

Christmas trading update - what a useless update this is! It doesn't give us the two key bits of information that we need - namely LFL sales growth, and profit versus market expectations.

So we now have to guess whether they are deliberately withholding inconvenient figures, whether the office junior was left in charge of writing & publishing the RNS, or even that they may not actually have accurate data to report?

Instead the company says this;

Joules delivered a strong performance over the Christmas period with total retail sales* up 22.8% against the comparable period last year.

Retail gross margin rate, over the same period, is expected to be marginally ahead of the prior year. This outcome reflects continued strong growth across both the Store and E-commerce channels.

Also, they don't tell us the split between how retail & ecommerce sales performed.

So all we have to go on, is that management tell us everything went well over Xmas.

My opinion - this looks quite a nice growth stock. Although the net margin isn't quite as high as I would expect. Also, it has a very established "preppy" design for its products. Being so niche increases the risk that this look could go out of fashion.

The shares look a bit pricey to me, but so is everything that is growing organically, and with an online element.

If you like growth stocks though, this one is worth a look, in my view.

Right, got to dash - I'm off to IG's office, to record my quarterly "Small cap wrap" with Jeremy Naylor. All good fun, and it makes me really focus on which are my best stocks - a useful exercise.

Best wishes, Paul.

(usual disclaimers apply)

See what our investor community has to say

Enjoying the free article? Unlock access to all subscriber comments and dive deeper into discussions from our experienced community of private investors. Don't miss out on valuable insights. Start your free trial today!

Start your free trialWe require a payment card to verify your account, but you can cancel anytime with a single click and won’t be charged.