Good morning! I added a few more sections to yesterday's report late last night, so here is the link for that report.

I'm looking forward to Mello Bloomberg tonight, so hope to see some of you there. Let's hope we don't get too merry, and sign up for a Bloomberg terminal, or it could turn out to be an unexpectedly expensive evening!

Portmeirion (LON:PMP)

Share price: 895p

No. shares: 10.7m

Market Cap: £95.8m

(at the time of writing I hold a long position in this share)

Preliminary results - for the year ended 31 Dec 2014. Reported EPS is 57.6p (up 8.2%), which has come in a little ahead of broker consensus of 56.0p.

Revenue growth in the three key markets (USA, UK, and S.Korea) looks pedestrian, but growth in RoW looks more encouraging - up 25%. Also note that online sales are small, at only £2.0m, but growing strongly (up 70%), which is encouraging.

Dividends - up 10.4% to 26.5p for the year. That gives a yield of just under 3.0% - which may not sound exciting, but the divi has been going up by c.10% every year since 2008, so assuming that continues, this should be a decent income stock - something that is heavily emphasised in the narrative to today's statement.

Balance Sheet - excellent, as always. The freehold HQ site is included within fixed assets, which is always welcome. The current ratio is wonderful, at 4.0, although note that inventories are rather high. The company doesn't duck this issue, and 'fesses up in the narrative that stock control was not good enough, and is an area they need to focus more on.

Pension deficit - has gone up to £4.2m. A cash outgoing of £0.8m p.a. is required to keep this under control - unwelcome, but not a deal breaker, in my view.

Outlook - sounds positive - sales are up in the first two months of 2015. Acquisitions are mentioned as a possibility.

My opinion - this is one of my favourite companies, and it has performed very well in recent years. However, the price looks about right now, and given a more relaxed rate of growth now, I've decided to top-slice my holding this morning, banking some profits to free up for other opportunities. Am happy to keep running the remainder of my position for the long term.

It looks as if this year the company might do c.60p EPS, so the PER of about 15 looks sensible to me - i.e. it's probably about the right price. The upside could come unexpectedly though, as the company could be worth more to an acquirer perhaps?

Northamber (LON:NAR)

Share price: 43p

No. shares: 27.5m

Market Cap: £11.8m

Interim results for the half year to 31 Dec 2014 are out today. Although turnover has risen 18%, the company remains loss-making - it is an IT products distributor.

I'm having a few technical gremlins this morning, so this section of the report just vanished, hence I'm having to recreate it. The balance sheet remains quite strong, although net cash fell sharply at the year end, but the company says it recovered in early 2015.

My opinion - the way I look at things, this company needs to either diversify into more profitable areas, or shut down. There's no logic at all to continuing trading at a loss. Otherwise shareholders might be forgiven for complaining that it's probably just a lifestyle business for the Directors. There is a small divi, but that can't continue forever, unless the company makes some profits. This is one example of where a strong balance sheet is perhaps allowing management to continue with an illogical, uncommercial business operation, cocooned from reality by a cash pile and generally solid balance sheet.

Cambridge Cognition Holdings (LON:COG)

Share price: 86.5p

No. shares: 16.9m

Market Cap: £14.6m

(at the time of writing, I hold a long position in this share)

Final results for the year ended 31 Dec 2014 have come in well ahead of forecast. FinnCap were forecasting an adjusted loss before tax of £0.9m, but the result is much better, at a loss of £0.2m. Turnover was up 40% against prior year, to £5.8m. So it's starting to look like a proper business, rather than blue sky. It's worth noting too that the trend improved throughout the year, with H2 being modestly profitable.

It's a very interesting product, which tests people for cognitive function, which can even be used to an iPad. It therefore enables GPs to quickly & easily test for early stage dementia, and thus relieves pressure on specialist clinics from the "worried well", who can be tested and reassured that they are fine, at the GP level.

I took an interest in the shares when they began winning contracts from drug development companies (to test the impact on mental capability) of new drugs. Clinical trials are now about two thirds of turnover.

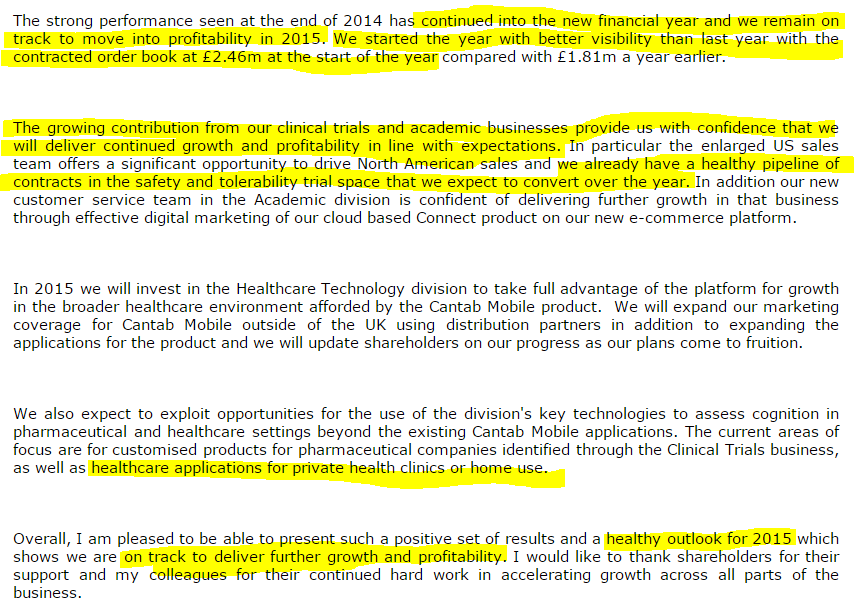

Outlook - a rather rambling update, but all sounds positive;

My opinion - I'm very pleased with these results & outlook. It's difficult to know how to value the company, but assuming there's more growth to come, and profitability should mean no further fundraisings/dilution, then the £14.6m market cap is a level I'm happy to run with. There are plenty of other far more fanciful things out there at far higher valuations! For once, this seems to be a blue sky share that is actually starting to deliver decent results.

Broker forecasts are for £0.3m adj profit this year, and £0.8m next year. With good momentum already happening, one hopes that there might be scope to beat those forecasts, as I imagine extra sales will be high margin.

I note from the chart that these shares still seem "off the radar", as no excitement seems to have taken hold as yet, despite the company delivering ahead of plan.

As you would expect for something this small, the shares are illiquid, and the bid/offer spread is horribly wide, so it's not a share to trade, but more a buy & hold type of investment.

Essenden (LON:ESS)

Share price: 67.4p

No. shares: 50.1m

Market Cap: £33.8m

(at the time of writing I have a long position in this share)

Preliminary results - for the 52 weeks to 28 Dec 2014.

These results look very good, continuing the recovery of this ten pin bolling centre operator. Adjusted EPS rose by two thirds to 5p, so the PER looks reasonable at 13.5, assuming that they can continue improving earnings.

Current trading - is positive, with +4.2% LFL sales growth for the first 10 weeks of this year. That should have a good impact on the bottom line, thanks to operational gearing.

Balance sheet - is tons better than it used to be, since the loans were converted into equity. There's still a bit of debt remaining, but at a reasonable level that doesn't threaten the business at all, in my view.

Corporate action? - it sounds as if the company is effectively up for sale now, which could provide some potential upside possibly?

My opinion - management have indeed performed an impressive turnaround here. Personally I don't mind whether they sell the business (if the price is right!) or continue going it alone - although if the latter, then they need to start paying a decent divi, as shareholders have not received any divis in recent years.

Regards, Paul.

(of the companies mentioned today, Paul has long positions in PMP, COG & ESS, and no short positions. A fund management company with which Paul is associated may also hold positions in companies mentioned)

See what our investor community has to say

Enjoying the free article? Unlock access to all subscriber comments and dive deeper into discussions from our experienced community of private investors. Don't miss out on valuable insights. Start your free trial today!

Start your free trialWe require a payment card to verify your account, but you can cancel anytime with a single click and won’t be charged.