Good morning! What an interesting day yesterday, I saw five company presentations in total, and briefly comment as follows;

Pennant International (LON:PEN) - Met the CEO, Chris Snook, and had a quick whizz through what the company does (simulation software & equipment). Looks an interesting & reasonably priced company.

IMImobile (LON:IMO) - A recently floated company. I met the CEO, Jay Patel, and was very impressed with him - very much the type of CEO I like to back. It's not a sector I understand (complicated software to allow companies to communicate better with clients' mobile phones), and the valuation doesn't jump out at me as being value, but it's certainly a company I shall do some more research on, to better understand its prospects.

The following 3 companies presented at last night's EDIF;

Benchmark Holdings (LON:BMK) - a very interesting-sounding company, but I haven't got the slightest clue how to assess the company's prospects, nor how to value it. So it's in the too difficult/speculative tray for me.

Staffline (LON:STAF) - the shares have been a spectacular success, but my judgment on this share is completely tainted by the fact that I bought cheaply in 2012, but sold far too early. Hence I'm not interested in revisiting it after it's gone up so much. Probably fully valued for now, but still has impressive growth aspirations. I've got nagging ethical concerns about companies which facilitate a large section of the population living on low wages. We need to get back to companies giving people proper jobs, full time, on decent wages, not an army of agency workers being subsidised by the taxpayer (through working tax credits & housing benefit).

Manx Telecom (LON:MANX) - niche telecoms company that has been passed around by various owners, before ending up with its own recent IPO. The near-6% dividend yield is the (only?) attraction here. For me that's nullified by the pension deficit, too much debt (always the case with companies sold on by Private Equity), and that it operates in a regulated sector (telecoms).

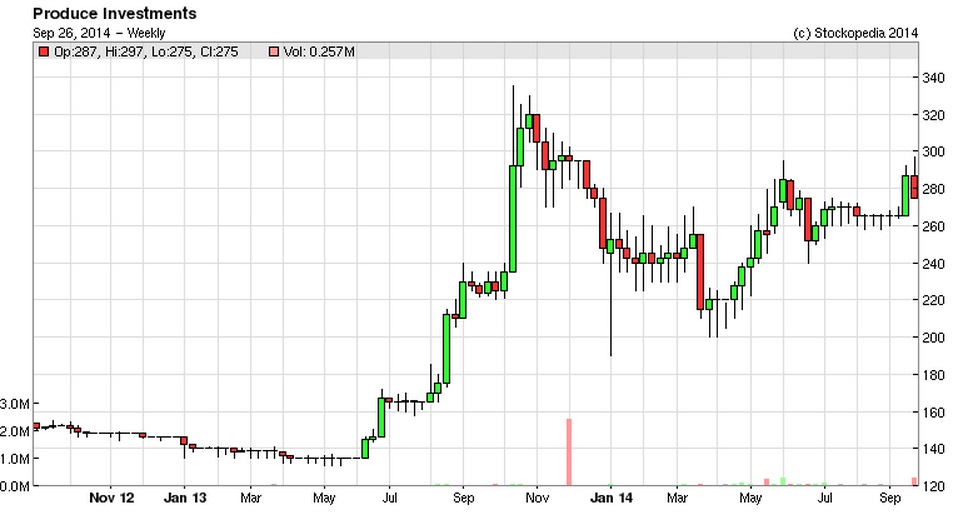

Produce Investments (LON:PIL)

Share price: 285p

No. shares: 26.5m

Market Cap: £75.5m

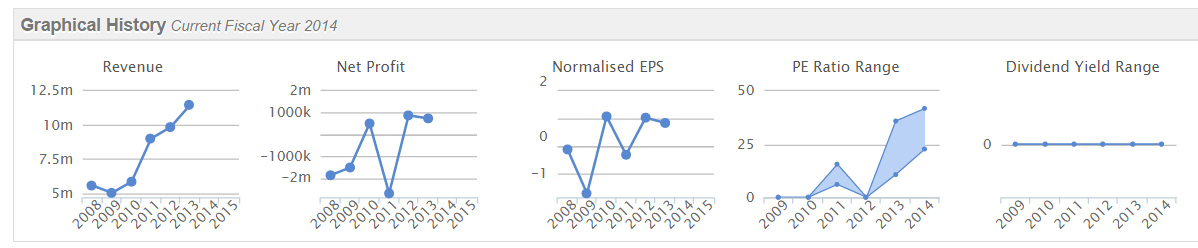

This company is worth a look - it's a potato grower and distributor. The shares have come up on my value filters a few times, and I did a quick review flagging the value here on 16 May 2014.

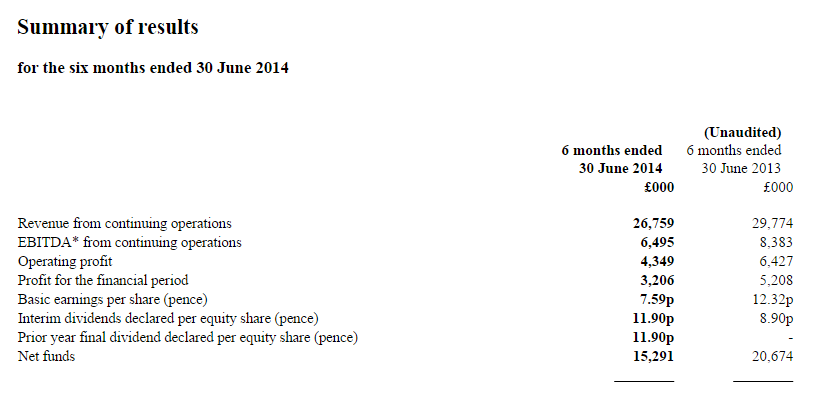

Final results for the 52 weeks ended 28 Jun 2014 have been published today, and look good. Revenue fell 6.9%, but that doesn't matter, it's profit that matters - and that was up 50.7% to £10.1m (taking the adjusted profit before tax). I'm happy with the adjustments, mainly relating to a £1.6m exceptional for the closure of a facility.

Valuation - adjusted EPS of 39.6p looks to be ahead of forecast (consensus is for 32.4p), although I'm wondering whether the broker consensus might be based on basic EPS? (which was lower, at 33.6p). This is always the problem with looking at broker consensus forecasts - you're not certain which EPS figure they are trying to forecast - basic, diluted, adjusted?

Anyway, whatever the case, the PER works out at a very low 7.2, dividing the 285p share price by adjusted EPS achieved of 39.6p. That's certainly a cheap PER for a stock that has just delivered strong results.

Dividends - the total payout for the year is 6.825p (up 25%), for a yield of 2.4% - so that's reasonable, but not spectacular.

Balance Sheet - net debt has risen to £24.5m, due to the acquisition of The Jersey Royal Co Ltd. The company presents its Balance Sheet in that annoying American way, where all the assets are listed first, then all the equity & liabilities. I hate that style of presentation - it makes no sense whatsoever to me, but some people seem to like it. So I'm just having to rejig the figures into the correct format that I can understand.

Net tangible assets are £31.4m.

The working capital position is sound, with current assets being 141% current liabilities, which passes my usual 120% minimum for most sectors.

Long term liabilities are a little high for my liking at £26.1m, being mostly bank debt and a pension deficit, so overall I'd say that the Balance Sheet is just about OK, but not quite as strong as I'd like. It could do with a bit more asset backing, to protect the company if there is a bad harvest one year.

Outlook - a bit of a mixed bag (or should that be sack?!) here;

Looking to the year ahead, although recognising we are only circa 30% of the way through harvesting, our best estimates for the current year's crop would indicate both reasonable yields and quality. As a result of this we would expect prices to come under pressure as supply is forecast to be higher than demand. The Group's procurement model which fixes an element of crop in advance but also has a proportion of crop linked to the free market enables the Group to take advantage of any such lowering of prices. We would also expect the retail environment to remain fiercely competitive as the market continues to evolve through increased competition from the Discounters, changing consumer shopping habits and more focus on reducing home waste, all of which impact market volume.

Whilst the market will continue to be challenging the Directors remain confident about the Group's prospects for the coming year...

My opinion - the shares look good value. Personally I cannot overcome my aversion to food producers, since they are likely to come under even more, unprecedented pricing pressure from the supermarkets. When you add in the uncertainty over weather & the possibility for some sort of natural disaster that could cause a profit warning if a crop is ruined, then maybe overall these shares could be seen as cheap, but fairly priced at the same time? It's not for me, but I can see the attractions of the low valuation.

Andrews Sykes (LON:ASY)

Share price: 292p

No. shares: 42.3m

Market Cap: £123.5m

I was delighted to see the share price here collapse by about 28% this morning, as I've been hoping that the market would give me a chance to buy back into this terrific company. So I picked up a little scrap of stock this morning at just over 276p.

It's very illiquid, due to a bizarre ownership structure, where the founders/Directors own about 90% of the company! That puts off a lot of people, but it doesn't deter me at all - the quality of the company far outweighs the ownership structure to me, and the major shareholders have never done anything to harm minority shareholders over many years, so I trust them.

Interim results for the six months to 30 Jun 2014 have been released today, and look disappointing, hence the sharp fall in share price. The company must have set a new record for the number of times they mention the weather in today's announcement! This happens quite often with this company, they have the odd bad year when usual weather patterns don't play out right - it's a pumps & air conditioning business. Although mention is also made of competitive pressures, which is a slight concern.

Here are the headline figures from today's results;

So not very good in comparison with H1 last year, for a variety of reasons.

Balance Sheet - is in excellent shape, with net cash of £15.3m, and overall just looks terrific.

Valuation - It looks like they may do 20-25p EPS for this year perhaps? So that puts the PER between 11.7 and 14.6. Considering the company's financial strength, high quality scores on ROCE, ROE, and operating margin, and its propensity to pay out chunky dividends, I think that's an attractive valuation in a bad year.

Outlook - this says to me that 2014 is going to be a disappointing, but not disastrous year. I can live with that:

Trading in the third quarter to date has been disappointing. Although in both the UK and Northern Europe warmer weather arrived earlier than last year, it was not sustained and did not reach the temperature peaks of 2013. Whilst both June and July were warm, August was disappointingly cool and wet thereby affecting the performance of our air conditioning hire business and this is continuing to have an impact into September.

Activity in the Middle East was, as expected, quiet in July due to Ramadan but the anticipated upturn in the last five months of the year has so far failed to materialise.

The weather for the final quarter of 2014 is currently an unknown factor and may significantly affect the outcome for the year. The board remains cautiously optimistic that the group will return a satisfactory performance for the remainder of 2014.

My opinion - one of my favourite companies is back in my portfolio, which is very pleasing. I think this is a smashing business, on a tuck away and forget forever type of basis. Although as usual, please DYOR, and I'm particularly interested in hearing any bearish views in the comments below - we need people to challenge our views, not to reinforce them!

Hopefully today has given me a good buying opportunity? The risk is that the company is having more serious competitive problems - after all it does make high profit margins, so perhaps that is being chipped away by competitors? I'll have to give this more thought - maybe my previous liking of the business is clouding my judgment?

Richoux (LON:RIC) - I've been keeping an eye on this tiny restaurant chain, in case there is roll-out potential. Interim results today look poor though, so no sign of there being any significant expansion potential here in my view.

As you can see from the Stockopedia graphics below, whilst turnover has been rising, it's still very small, and profitability doesn't seem to be establishing any trend, and looks to be down this year.

The Balance Sheet is sound, with net cash of £3.1m.

At 20p per share, the market cap is £18.4m, which is looking pretty generous in my view.

Note also that it has a very low StockRank of 10.

Filtronic (LON:FTC) - My scepticism about this company has proven correct, with another profit warning today. The key bit says;

While at this stage of the year it is too early to be clear about the second half outlook for Broadband, on the balance of probability management believes that for the year as a whole Broadband is likely to generate a result below current market expectations.

It's not clear to me whether there is a viable business here at all? Hence it is impossible to value.

That's all folks! Have a lovely weekend.

Regards, Paul.

(of the companies mentioned today, Paul has a long position in ASY, and no short positions)

See what our investor community has to say

Enjoying the free article? Unlock access to all subscriber comments and dive deeper into discussions from our experienced community of private investors. Don't miss out on valuable insights. Start your free trial today!

Start your free trialWe require a payment card to verify your account, but you can cancel anytime with a single click and won’t be charged.