Good morning!

A close shave for me this morning, with two profit warnings, but luckily I managed to dodge both of them (having ditched both shares from my portfolio a few weeks ago). Although the challenge for today is to resist the temptation to catch the falling knives, as that is usually (but not always) a mistake.

Pressure Technologies (LON:PRES)

Share price: 191p (down 29% today)

No. shares: 14.4m

Market Cap: £27.5m

Profit warning - I am not surprised that this engineering group, which is heavily reliant on the oil & gas sector, has put out another profit warning. Indeed worrying about this prospect was what drove me to sell out on the last bounce up 2-3 weeks ago. With constant bad news from the sector, it was difficult to imagine how this company would be immune.

The trouble is, that there are a lot of trend-following market participants at the moment, who look for favourable chart patterns, buy shares which exhibit them, so their buying results in a share rising, which itself pulls in more momentum buyers. This is problematic, because (especially in small caps), the chart patterns can often be completely divorced from the fundamentals of the company, as has been the case here.

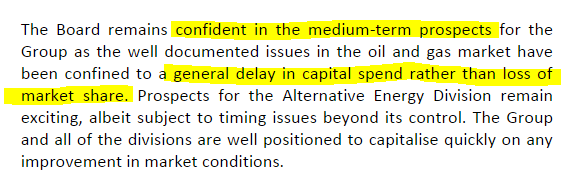

Anyway, PRES notes a further deterioration in market conditions, and the upshot is a significant profit warning for both this year (ending 27 Sep 2015) and next year:

Outlook - it's difficult to draw any conclusions from this, other than feeling generally soothed if one is a long-term holder, that things should improve at some unknown point in the future:

Valuation - this is almost impossible, due to inadequate information. EPS forecasts for this year have already come down from about 50p to 31.2p. That's now gone out of the window as well. It sounds like the company will at least remain profitable, but with business slowing down, next year could see a further deterioration (as the early part of this year was positive, but probably won't be next year).

There are no indications on a possible range of profit outcomes for this year (why not? Surely the company could have said we expect profit to be between £x and £y, which is best practice when issuing a profit warning, and at least demonstrates that management have control over the situation & know what's going on).

So unfortunately, today's statement from PRES translated into terms I understand, says to me that, we're letting you know things are going to be bad, but we're not sure how bad. Accordingly, I don't see how it's possible to value the company right now, it would just be a question of having a punt, and hoping for the best.

Balance Sheet - if you can't value a company on earnings, then the balance sheet is a good fallback. Also crucially, are they going to run out of cash? Things look alright in that regard here. The last reported balance sheet shows a healthy current ratio of 2.01, and with business slowing then I imagine working capital will be reducing, thus throwing off cash as debtors and inventories contract.

The company had net cash of £5.8m when last reported, but has subsequently spent £3.4m on freehold property, I don't see any issues with solvency here, so the group should be able to weather the current storm.

Although it seems a bit of a missed opportunity to have failed to update the market today on the group's cash/debt position. Not doing so just adds further uncertainty to the mix.

Note that PRES very wisely did a Placing at 575p in Mar 2014, to finance an acquisition, and provide an additional £6m working capital. Sensible management fix the roof when the sun is shining, although I think an element of luck was involved here too, in that they did their fundraising a few months before the price of oil collapsed.

My opinion - today's profit warning is the second this year, and may not be the last. That said, the shares have gone down a great deal, and at some point will probably be a good long term investment. My main worry is that, being a UK based group, a long period of depressed oil prices might see the North Sea oil producers shut down production permanently. If that happens, then it could be impossible for PRES to recover to previous levels of profitability.

So bottom line, I really don't know how to value this share, and think it's probably safest to keep away from it now. Although looking at the two year chart, the drop has been so extreme, that it is tempting to have a dabble in readiness for the next bounce.

UPDATE: I've now seen some revised broker forecasts for PRES, and it's grim. Current year EPS is now 14.36p, and next year 17.38p, plus a cut in the dividend is expected.

With so much uncertainty, and the trend being very much against them, I wouldn't want to hang my hat on these numbers even. So it looks to me as if a very cautious approach to valuation is best. Maybe 6 times current year forecast, so a share price of just 86p, is the sort of level where I'd be tempted to buy - less than half the current share price.

Maybe that's too pessimistic, but this share is starting to look like an "all bets are off" type of situation, at least when it comes to estimating its profitability. If there's a major recovery in the price of oil, then this company would be a nice, leveraged bet on that - although oil producers would probably be a better idea for a rapid recovery.

The group may need to do a restructuring, to shed a lot of costs, if there is no end in sight to the current situation. That would mean exceptional costs, but could then open the door to improved profits in future.

It's all looking a bit of a can of worms right now, I'm steering clear of this one, as it could go a lot lower than the current price of 191p, I suspect.

SCISYS (LON:SSY)

Share price: 60p (down 27% today)

No. shares: 29.0m

Market Cap: £17.4m

(at the time of writing, I hold a small number of shares in this company)

Profit warning - this is an interesting company, which provides bespoke software for mainly public sector organisations, such as the European Space Agency, broadcasters, as well as CRM systems for car industry. They've got fingers in lots of pies, and hence long-term income streams, and strategic importance to big organisations is something that should be capable of commercial exploitation, in my view.

The key sentence in today's profit warning says:

Trouble is again, it's not quantified. So how much is substantial? We don't know, and will have to wait for revised broker forecasts. I do wish companies would quantify the extent of the profit miss in their RNSs. It's incredibly frustrating to be left in the dark, until the company has spoken to the house broker, given them the full story, and only then do shareholders find out what's going on - if you can get hold of the broker notes of course, which many private investors find difficult.

Companies can, and should inform the market of the likely range of profit outcomes for the year. Even if it's a wide range, due to uncertainty, it's always better that the market is given as much information as possible.

So what has caused the profit warning? Some blame is put on Euro weakness, since translation of profits from the European subsidiaries will translate into a lower sterling result. Fair enough, that's to be expected.

The main issue though is more worrying, and to me indicates an alarming lack of financial control;

Surely this is basic stuff? Errors of this nature simply should not be allowed to occur. There should be a process to ensure this kind of mistake cannot happen, and that there are contingency amounts built into contracts to allow for cost over-runs. If I had any significant shareholding here, I'd be livid. As it is, thankfully I only have a tiny rump of shares left in my pension, which I'd forgotten about.

Bank covenants - normally when a company says it's likely to breach its bank covenants, then it's time to run for cover, as the situation can get very ugly. Although in recent years banks have been very lenient.

However, this is a good example of why I like freehold property so much. Banks are happy to lend against freeholds as security, even if a business is trading badly. It's the best type of security, as it cannot be moved or misappropriated (since the bank will usually take a fixed charge against the property, which means that, even if the company goes bust, the bank will own the property, and can sell it to clear the borrowings secured against it).

Checking note 15 of the last Annual Report, Scisys had £7.6m in freeholds, which are in the books at cost. I believe the company has owned the freeholds for some time, so current market value is likely to be above cost. Therefore its gross borrowings of about £4-5m, which are in any case offset by cash for part of the year, look safe.

My opinion - the comments from the Chairman make it clear that he is not impressed with this profit warning. I agree, and hope that the relevant employees responsible for this major cock-up are now (at the very least) on a final warning. He says that it's an isolated incident.

I'm tempted to buy a few more for my long-term portfolio, but it's been such a difficult share to deal in before, due to extreme lack of liquidity, maybe that's not such a good idea. There is also the worry that, as Jon Moulton pointed out at last year's LVIC, that in his experience, problems are always worse then management at first reveal. Hence it usually makes sense to steer clear until the dust has settled.

Furthermore, even after today's sharp fall in share price, the dividend yield is not enough to get me excited. The divi might even be cut, if the problem contract issues get worse? On balance then, I'll hold fire on topping up for the time being. There's always the chance that a big holder will throw in the towel, and trash the share price in order to exit - that can be the only way to exit from a very illiquid share sometimes. So I'll keep my powder dry for that possibility, and if it doesn't happen, not a problem.

As a more general point, this situation illustrates clearly why I'm worried about small cap valuations at the moment. Many small caps are priced to perfection, yet lots of things go wrong at smaller companies - since they are more dependent on individual clients, contracts, products, and people.

So if you're paying top whack for small caps (e.g. PERs of say 15 or more), then you've got no margin of safety for anything going wrong.

UPDATE: I've seen the revised forecasts from FinnCap today, and they've really taken an axe to things - for the current year forecast adjusted profit has been slashed from £3.3m to just £0.3m! That's far worse than I thought likely from the RNS.

I think this completely undermines any attractions about investing in this company, so I'm taking it off my watchlist now, and won't be averaging down.

Vianet (LON:VNET)

Share price: 99.5p

No. shares: 27.5m

Market Cap: £27.4m

Final results y/e 31 Mar 2015 - these results look better than I expected. It's not a company I follow closely any more, as progress was too slow, and I felt the growth potential was limited, and so I sold out a while ago to recycle the money into other more interesting opportunities. There's an opportunity cost to holding positions of course.

That said, I'm pleased that my original analysis has turned out to be reasonably alright, with the shares back up to where I originally took an interest several years ago, and of course with a generous 5.7p dividend each year, the overall return has been not too bad.

A few quick comments;

Positive

- Vending might be getting somewhere (at last!), with a £0.6m operating profit (up 60% vs LY)

- Fuel division losses eradicated - now at around breakeven

- Full year divis of 5.7p maintained for another year

Negative

- Core business, likely to continue declining - 900 net loss of sites this year

- Market Rent Option action by Govt puts serious question mark over viability of tenanted pubs

- No significant commercial progress in USA yet for iDraught

- Dividend payments look stretched, so a cut could happen in future

My opinion - overall I think the shares look fully priced at 99.5p. Management have done a good job in stemming the decline of the core business, and squeezing a better performance out of the very small, and marginal, other divisions.

I think at some point they will need to bite the bullet, and cut the dividend, which could pull away the main support for the share price, so a risk not to be ignored.

Overall, it's difficult to see much upside potential, based on how slow growth has been in the past. Threats to the core business remain, and it seems to me that pubs groups will increasingly move away from the tenanted model, to disposing of under-performing sites, and taking good sites in house (when arguably they don't need Brulines any more, as they have full control). Both trends are negative for Vianet, and almost all of its profit still comes from Brulines, So potentially quite risky, longer term, I would say.

I'd rather invest in companies where there is a tailwind from market conditions, not a headwind, as in this case.

VP (LON:VP.)

Share price: 718p (up 6.4% today)

No. shares: 40.2m

Market Cap: £288.6m

Final results y/e 31 Mar 2015 - these look excellent figures. Just a few brief comments, as I'm running out of time.

The key figures for me are that basic EPS (before amortisation) rose 30% to 54.5p. Therefore the PER is currently 13.2 times 2014/15 earnings, which seems fair to me. The outlook comments sound reasonable.

I don't have any Balance Sheet concerns - there is some debt, but it's to fund assets, so that's fine. Divis are up, to 16.5p for the full year, yielding 2.3% - not madly exciting, but shareholders are foregoing some income so that the company can continue expanding - so the reward should be greater earnings, and better divis in future.

My opinion - I like this company, and am kicking myself for not having bought the two dips in the last year. Same with Lavendon (LON:LVD) - I almost pushed the buy button on that a few months ago, but didn't, so have missed a big recovery there too.

My typing/mouse fingers are playing up now (I get RSI up my right arm, and it's flaring up now after 5 hours on the computer), so as usual now, I'll add some final comments on today's YouTube video, including a review of results from Wincanton (LON:WIN) and phone hacking at Trinity Mirror (LON:TNI), more comments on Zoopla, and a few other bits & bobs.

Regards, Paul.

(as mentioned above, Paul has a small long position in SSY, and no short positions. A fund management company with which Paul is associated may also hold positions in companies mentioned)

See what our investor community has to say

Enjoying the free article? Unlock access to all subscriber comments and dive deeper into discussions from our experienced community of private investors. Don't miss out on valuable insights. Start your free trial today!

Start your free trialWe require a payment card to verify your account, but you can cancel anytime with a single click and won’t be charged.