Good morning from Paul & Graham!

Weekend podcast - the latest edition, I recorded on Saturday. You can add this to your podcast platform, by putting in the URL. A listener suggested this, and it works on Google Podcasts, and should on others. This one was a bit too long, rather rambling, apologies, I'll try to stick to 30 mins total in future. If you're short of time, then skip the first 18.25 minutes, to get into the individual companies part.

Agenda -

Paul's Section:

Seraphine (LON:BUMP) (I hold) - another profit warning, this is the 4th since it listed a year ago! However, I think the disappointments are already in the price, with it having joined the 90% club (down 90% since listing) in just a year, along with a lot of other opportunistic, over-priced floats in 2021. However, the business looks potentially very interesting to me - a long-established niche brand selling high margin, own-designed maternity wear. The experienced new CFO has a lot to sort out (including inventories being far too high), but a positive going concern note suggests the risk of a discounted placing may not be as high as I feared. Risky still, but if the turnaround works, then this could have multibagger potential I reckon. Although it has to be said, I do get quite a lot of these wrong, because nobody can predict the future, and riskier shares are just that - risky.

Belvoir (LON:BLV) - we're given an in line update today for H1. Everything looks fine. This is a really nice little group, well-run, and making acquisitions which are adding value. It's still reasonably priced too. Thumbs up from me.

Graham's Section:

Flowtech Fluidpower (LON:FLO) (£77m) - this H1 trading update says that performance is in line with expectations, but the broker says that strong gross margins are offsetting a weaker revenue performance, and the EPS estimates for this year and next year are cut by mid single digits. This company tends to be a solid performer: it now needs to work on reducing its debt, which has risen significantly in the post-Covid environment as the company battles with difficult supply chains by increasing its inventory pile. Looks fairly valued at current levels.

Correction - Trackwise Designs (LON:TWD) (£14m) - Just a quick note to say that last Thursday’s SCVR (now amended) had a typo: the “severe but plausible” downside scenario in which the company experienced a financial shortfall was outlined by its outgoing CFO Mark Hodgkins, and not by its CEO. Happy to clear that up.

Journeo (LON:JNEO) (£10m) (+2.6%) [no section below] - this previously traded as 21st Century Technology Plc (C21). For many years it enjoyed very little financial success, but it did report small profits in both 2020 and 2021. The company provides both products and services to the transport sector.

Today’s H1 update shows revenue growth of 23% and orders up 36%. Full-year results are still expected in line with expectations, and include a new £0.9m follow-on contract signed with a vehicle operator at Heathrow airport. Brokers are expecting profits of £0.9m this year (EPS 10.4p), on revenues of £18m.

The company has access to a £2.75m invoice discounting facility, and is forecast to finish the year with a modest net debt position. The major risks here are likely to do with customer concentration and lumpy earnings, given the small size of the company. These risks may be priced in at current levels, if you have confidence in the continuation of positive business momentum and can see expectations for 17p EPS being hit next year.

XP Power (LON:XPP) (£565m) - H1 was very difficult for this manufacturer of power products. The company suffered from component shortages, lockdown in China, port disruption, the general inflationary pressures, and even lost a jury trial in the United States (potentially very costly). Net debt has increased significantly and the company has reported a meaningful operating loss for H1, after everything that went wrong. More positively, customer demand appears to be resilient and when supply chains work properly, the company’s revenue performance should improve. Short-term outcomes are unpredictable but I still view this as a decent-quality company trading at a price that is depressed by some (hopefully) temporary factors.

Explanatory notes -

A quick reminder that we don’t recommend any stocks. We aim to review trading updates & results of the day and offer our opinions on them as possible candidates for further research if they interest you. Our opinions will sometimes turn out to be right, and sometimes wrong, because it's anybody's guess what direction market sentiment will take & nobody can predict the future with certainty. We are analysing the company fundamentals, not trying to predict market sentiment.

We stick to companies that have issued news on the day, with market caps up to about £700m. We avoid the smallest, and most speculative companies, and also avoid a few specialist sectors (e.g. natural resources, pharma/biotech).

A key assumption is that readers DYOR (do your own research), and make your own investment decisions. Reader comments are welcomed - please be civil, rational, and include the company name/ticker, otherwise people won't necessarily know what company you are referring to.

Paul's Section:

Seraphine (LON:BUMP) (I hold)

27.25p (pre market open)

Market cap £14m

Seraphine Group plc, the international digitally-led maternity and nursing wear brand, today issues its maiden Final Results for the 12 months ended 3 April 2022 (the "Period" or "FY22"), against the backdrop of an extremely challenging year for the retail sector.

I’ll call this FY 3/2022, as it only just crosses into April by 3 days.

Key points (on an initial skim read. I need to go through it all again in more detail, when time permits) -

Very high gross margin of 63.2% (although down from even higher 65.9% last year)

High average basket value of £135 (up 6.5%) - it has pricing power.

Low cost of acquiring new customers, CAC of £16 (but since risen to £25.40, see outlook section)

Long-established niche in maternity wear, with limited competition, due to specialised fit, and limited market size - larger companies have tried this niche too, but often bow out, once they realise volumes are too low, and range of sizes is so extensive. Leaving the business for BUMP instead.

Logistics problems, especially with customer returns internationally - too slow (see poor TrustPilot reviews mention this as main problem) - mgt is aware, and working on solving this (I raised this issue in a call with the CEO a while ago).

Operates globally from single distribution centre in Belgium (Europe is largest market).

New CFO, ex FCCN & Asos, Lee Williams - who I see as a safe, experienced pair of hands, and he must see potential at BUMP, otherwise why join? But lots of things need sorting, this was a big weakness previously.

Adj EBIT £2.2m (down from £5.6m) - so still profitable, and adjustments are reasonable I think, given that FY 3/2022 figures include IPO costs and adjustments re high finance charges under previous private equity ownership. Clean numbers should look better in future.

3 profit warnings since floating, make that 4 now!

Shares floated at 295p, now in -90% club! Disappointing float, but is there value here now? It's a full listing, not AIM.

FY 3/2022 numbers -

Revenues of £44.0m, in line with guidance of £44.1m given on 5 May 2022, and is up an impressive 29% vs LY (last year) - in a sector where many online fashion businesses are struggling to report any growth.

Adj EBITDA of £2.6m (down 59% on £6.2m LY) - this is below guidance, which was “not less than £3m” - a bit disappointing, but not a disaster. “Final audit adjustments” are blamed. I can live with this, as the new CFO Lee Williams has only recently joined, and the former CFO was clearly out of his depth, so I would expect some odds & ends to get picked up under a new, more experienced CFO.

Statutory loss is massive, at £(33.9)m, mainly due to exceptional write-offs of intangible assets of £27.9m, and IPO costs of £3.5m. Bear in mind that this financial year includes the first few months when it was under private equity ownership, then floated on the main market in July 2021. So that distorts things like finance costs, which will be much lower in future.

There’s no getting away from the fact that this was a disastrous, over-priced IPO. One of many in 2021, as companies/brokers took advantage of the pandemic online boom, to stitch up fund managers with over-priced floats, passed off as structurally growing. However, the wreckage may contain some bargain nuggets of gold, and I think this could be one of them, possibly. But that’s dependent on a proper turnaround, and there are still headwinds facing the business - e.g. supply chain, logistics, higher marketing costs. These should be fixable issues, over time.

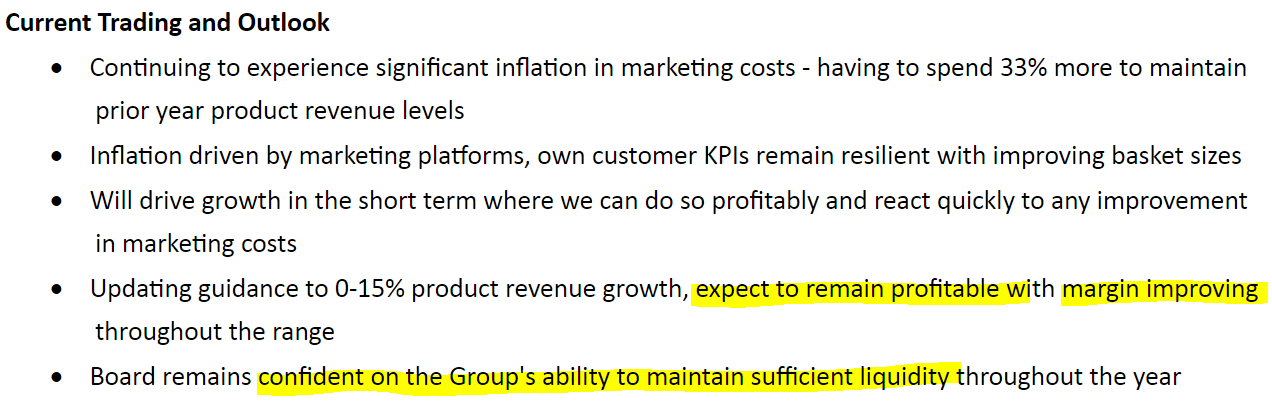

Outlook - previous guidance (from May 2022) was for revenue growth of 10-20% in FY 3/2023, and EBITDA margin of 8-9%.

Today’s guidance lowers revenue growth to 0-15% (sensible, given macro conditions), with the EBITDA guidance replaced with “expect to remain profitable”.

The final bullet point below is key, in that it reassures me no placing is imminent. I think this share could do well, if mgt avoid a dilutive fundraising. Note it is dependent on a £6m facility from HSBC.

.

There’s more detail given in another outlook section -

Customer acquisition (CAC) has now risen to £25.40 (up 60% on LY), but this isn’t too bad considering average order size is £135 - should still be profitable from first customer order.

Q1 revenues - below LY Q1, but improving trend (June 2022 flat vs LY).

Customer returns - increased marginally in Q1 (no figure given), but offset by increased basket sizes. BUMP can afford customer returns, due to high margins, and high basket size, whereas fast fashion, low priced competitors struggle. BUMP sees free returns as all part of their service.

Management is focused on driving efficiencies and setting a strong base for profitable growth once the challenging external conditions subside. The recent reinforcement of the management team and the resilience seen in customer KPIs once exposed to the brand provides reassurance on the underlying strength of our proposition. We remain confident in the medium-term opportunities for the business.

[Paul: my bolding]

Marketing - interesting that digital marketing has become expensive, so BUMP is “redeploying budget to traditional marketing channels and partnerships” - this could have wider read-across - i.e. have Google & Facebook cooked the golden goose, by price gouging too much?

BUMP says it won’t chase short-term growth by increasing marketing spend.

Liquidity - this is key for me, as the main risk is a discounted placing being necessary. At least that doesn’t sound imminent -

The Board is confident on the Group's ability to maintain sufficient liquidity throughout the year.

Cash was £2.8m at 3 April 2022 year end, but £3.0m (half the HSBC facility) drawn down, so £0.2m net debt - looks OK. The going concern note says that £5m was drawn down in total more recently.

Going Concern note - very interesting to read, with lots of useful information in it. Although I think someone should have edited the wording, as in places it doesn’t really make sense.

The pleasing thing is, and bear in mind the auditors sign off on these things, BUMP should remain in compliance with its bank covenants, even in a severe but plausible downside scenario - thus making a placing less of a risk -

The Directors believe, after careful consideration of forecasted cash flows and expected trading performance that the Group will have sufficient cash to meets its liabilities as they fall due, no covenant breaches are also forecasted. The Directors have therefore concluded that it is appropriate to adopt the going concern basis for the preparation of these consolidated financial statements.

Balance Sheet - a big rise in inventories jumps out at me, with the commentary saying that was due to stocking-up to prevent supply chain problems. Even so, £14.7m inventories is a huge amount for the size of business.

At the reported 63% gross margin, those inventories (stated at cost, remember) equate to £39.7m revenues - compared with FY 3/2022 actual revenues of £44.0m! So it’s holding almost a year’s worth of product in stock - that’s insanely high. Retailers should be holding about 6-8 weeks inventories.

Even in current circumstances, I wouldn’t expect to see more than about 3 months inventories. So nearly a year’s inventories held at 3 April 2022 is way, way too high. Even allowing for the fact that BUMP has a lot of continuity ranges, that sell continuously. It’s less exposed to fashion trends than brands. Remember BUMP is serving a niche, of maternity & baby wear, not general fashion.

Does being over-stocked matter? Yes, because the suppliers will want paying for it! Usually about 60 days after the product has been delivered. Note 20 shows that BUMP owed supplies £6.9m for stuff that has been invoiced, and £4.4m of accruals (usually stuff that has been received, but not yet invoiced). So I think BUMP needs to urgently reduce its inventories, to generate the cash to pay suppliers.

It’s clear that managing supply chain is one of BUMP’s weaknesses. So I hope the new CFO gets a grip on this area. I’d say much tighter internal controls are needed over stock ordering by the buyers, to prevent such a large inventories position building up again in future. Meanwhile they need to sell the excess inventories. There could be write-downs, and a lower gross margin, if slow-moving items need to be discounted to shift them. Hence expect plenty of half-price sales online.

NAV is £20.4m, less intangible assets of £23.1m, and deferred tax of £(5.7)m, gets me to adjusted NTAV of £3.0m - a tad weaker than I would like.

Being over-stocked, and dependent on HSBC facilities, is not ideal. But equally, I wouldn’t want to see dilution in a placing, with the shares this bombed out.

Unfortunately, it was not floated with a robust enough balance sheet.

Hence there is some risk here.

My opinion - there’s a decent business lurking here, in my view. Disappointing performance since listing has been due to a range of factors, but poor financial controls and management seem clear - now fixed with an experienced new CFO, who I think should be able to sort things out, and refocus the business. That’s the upside case, on a completely bombed out share price, with market cap of only £13m - could this be a multibagger from here? If they get performance back on track, then it’s possible.

Very high gross margins and high average transaction value, show that it operates in a lucrative niche. Orders are profitable from day 1, and there’s limited competition. Seraphine has been around a long time, and is well-known for its stylish, special fit maternity wear. Many influencers have worn its products, including pregnant royals.

A handful of flagship shops are operated mainly for brand & influencer purposes, to have a key physical presence - that’s fine, as long as they don’t lose money heavily.

Most sales are online, and it has 3 key markets - Europe, USA, and UK. To achieve good sales in all 3 is a key point which impresses me - that this is a potentially scaleable international business, which could excite investors again in a future bull market - just like it did at IPO last year.

We’re now up to 4 profit warnings since it listed, including today’s, hence the share price being on the floor. So this is not a high quality, strongly performing company at the moment. It’s more of a value, special situation, turnaround type of investment. So, speculative essentially, hence it won't appeal to everyone. Although note that renowned shrewd investor Christopher Mills has been building up a position recently, with Harwood Capital at 5.1%. The shareholder register is still dominated by the private equity form which floated it, with 42.7%. I don't know what their intentions are.

It seems to me the key concern now is excessive inventories, which need to be greatly reduced to generate cash. As Far Eastern supply chains seem to be beginning to ease, that should be possible over time.

There is some risk here, but this share could be a good recovery candidate in 2013. I hold. Sorry for spending so long on a micro cap, but it's a key personal holding, so I would be digging deep anyway, so it makes sense to share it here.

Dear oh dear -

.

Belvoir (LON:BLV)

235p (down 1%, at 10:25)

Market cap £88m

Belvoir Group PLC (AIM:BLV), a leading UK property franchise and financial services Group, provides the following update ahead of publishing its Half Year results on 5 September 2022.

H1 performance (6m to 30 June 2022) -

Revenue up 11% vs H1 LY (despite tough LY comparative as FOXT & WINK have also said recently)

The growth has mainly come from 2 acquisitions, of financial services advisory businesses, now up to 301 advisers (from 243, 6 months ago).

Core underlying revenues (fees to franchisees) was up 1%. Within that, lettings growth offset sales reduction.

Net debt is £3.1m, down £0.9m from a year ago, despite paying out £3.9m for acquisitions - I like this a lot, self-funding more acquisitions.

Overall trading is good -

Consequently, the Board confirms that the Group is performing well and is trading in line with management's expectations for the year ending December 2022.

There’s a webinar on IMC at 16:30 on results day, 5 Sept 2022. Management came across well on previous webinars I think - they strike me as down-to-earth, competent, unpretentious, and experienced - ideal really.

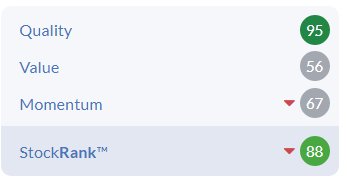

My opinion - we like Belvoir here at the SCVR. Experienced management are methodically building a bigger group, as you can see from the Stockopedia graphs below -

.

.

The share count has roughly doubled since 2016, but that’s taken into account in EPS calculations, so this shows the acquisitions have added value.

Some demand was pulled forward into 2021, hence the kink in the profits & EPS, but the long-term trend is very clear. This share has shrugged off the pandemic & cost of living squeeze. Rents are going up, so it should be inflation-protected too.

EDIT: Finncap has helpfully issued an update today, available direct or from Research Tree. No changes to forecasts, as I would expect, given it's an in line update. Looking at future years forecasts from Finncap, I think these look beatable. Hence very low risk of a profit warning, and more likely to be issuing ahead of expectations updates this year & next year, in my opinion. That's a key point right now, we have to avoid the banana skins by focusing on companies & business models that are set up to meet or beat expectations. There's also a useful graph in Finncap's note, showing the breakdown of activities. Financial Services revenues in particular stand out, as a big growth area for BLV that has flown under the radar a bit. End of edit.

I think if you want a well-managed, defensive share, at a reasonable price, BLV is well worth considering.

Stockopedia’s algorithms agree -

.

.

.

Graham's Section:

Flowtech Fluidpower (LON:FLO)

Share price: 125.25p (unchanged)

Market cap: £77m

This is a supplier of hydraulic and pneumatic components to industry, and a provider of related services. Additionally, it “designs, manufactures and installs bespoke solutions” for its customers.

This H1 trading update is in line with expectations. Key points:

- Like-for-like revenues +4.8% (total revenues +4%).

- Net debt increases to £19.7m at the end of H1, leaving headroom of £5.3m.

The headroom is obviously looking a bit tight, and management are keen to assuage concerns:

Given the supply chain related pressures encountered in late 2021, which have continued into this period, we decided to continue our investment in inventory, which increased by £11m in the 12-month period to 30 June 2022… we expect a degree of unwind of this position in the remainder of the year as we benefit from a more predictable supply chain environment.

Paul also noted that FLO’s debt was rising when he looked at this stock last August. The rise back then was also attributed to working capital needs.

Outlook - inflation and the macroeconomic environment are mentioned, but the tone here is positive. The company has invested in e-commerce (if you want to see its main UK customer-facing website, click here) and is looking forward to “attractive returns” from its “broader e-business agenda”.

Estimates - I’ve checked the latest broker note, and it says that actually the company’s H1 sales performance did not quite meet its expectations. However, it is thought that stronger margins have offset this. Overall, due to an accounting change and economic worries, it cuts EPS estimates for FY 2022 by 3.9% (to 10p) and for FY 2023 by 5.4% (to 11.1p)..

My view - this is not a stock that’s likely to ignite strong opinions either way. In recent years it has been a solid performer, except for the Covid-impacted 2020.

The present environment is tricky for it but perhaps FLO can come through it better than the average company - as a distributor, maybe it can pass on price rises to its customers without too much complaint?

Its industrial end-markets are difficult to judge, but revenue seems to be holding up OK, despite possibly missing prior expectations for this year.

The balance sheet is also worth mentioning - if supply chains don’t normalise as expected, there must be a possibility that action will be needed to improve headroom.

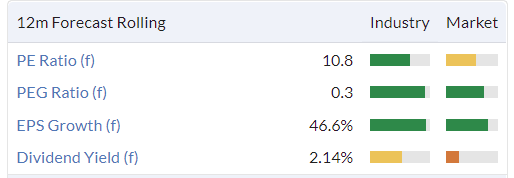

Overall, I don’t think this stock should be on a high PE rating and the market agrees, putting it on 11x next year’s EPS estimate.

See what our investor community has to say

Enjoying the free article? Unlock access to all subscriber comments and dive deeper into discussions from our experienced community of private investors. Don't miss out on valuable insights. Start your free trial today!

Start your free trialWe require a payment card to verify your account, but you can cancel anytime with a single click and won’t be charged.