Good morning. Paul & Graham are here today.

Agenda -

Paul's Section:

Hotel Chocolat (LON:HOTC) 134p (unch.) (£184m) - confirms today that its Japanese JV has entered court protection to restructure. Hence a c.£30m hit to HOTC - as indicated 9 days ago in a bombshell announcement, so today is really just confirmation. I question how management allocated capital so badly - spending about £1m per shop in Japan, for just 20% ownership of the JV? Despite crashing by about 80% this year, HOTC shares still don't look cheap yet, given it's now really just a UK business, and faces plunging profits in 2023 from cost headwinds.

Headlam (LON:HEAD) 307p (down 1%) (£257m) - a surprisingly good trading update, with self-help measures absorbing costs & reduced volumes, to still report increased profit in H1, and in line with expectations for FY 12/2022. Very good balance sheet, although cash is down a lot, partly due to generous shareholder distributions. A very nice value share, thumbs up from me.

Ince (LON:INCE) 5.6p (down 53%) (£5m) [No section below] - this one continues to be a disaster, we’ve been warning against it here for years, due to a diabolical balance sheet, with all sorts of nasties in it - e.g. large deferred consideration, excessive debtors, bank debt, and deeply negative NTAV.

INCE did a deeply discounted fundraise once before, and it’s now announced another one! 5p placing, a 58% discount. I wouldn’t pay anything for INCE equity personally. Although occasionally things like this can be speculative multibaggers, but a more likely outcome seems to me that it gets taken private for tuppence, or goes bust. It’s amazing to think these are lawyers & financial experts, yet are utterly incompetent at managing their own finances (although to be fair, the same accusation could be levelled at me! LOL!). INCE equity is therefore uninvestable at any price, in my view. For gamblers only - you never know, occasionally these things do pay out, although not often in bear markets. At least the risk of insolvency might have reduced somewhat, given this latest emergency fundraising.

Epwin (LON:EPWN) 76p (down 1%) (£110m) [No section below] - A solid H1 trading update. Trading has “moderated slightly” in June & July, but it “remains confident of achieving expectations in 2022”. H1 revenues up 13%, mainly due to price rises - good that it can pass on cost inflation. Managing OK with supply chain issues. Modest net debt of £7.3m, 03.x EBITDA. Tons of headroom (£65m) on bank facilities. Last balance sheet (at Dec 2021) was OK, at c.£20m NTAV, worsened by net lease liabilities. Overall - looks reasonable, although I’d be worried it might see business turn down once current shortages & premium prices for building products normalise, possibly? Generous divis, with a 6% yield, twice covered - not to be sniffed at, if that’s sustainable.

Virgin Wines UK (LON:VINO) 67p (down 8%) (£37m) [No section below] - FY 6/2022 results. Revenue down 6% on last year, to £69m, as the pandemic boost wore off. Although still up 63% on a pre-pandemic basis. Plenty of cash. EBITDA £6.3m, which Liberum converts into £5.3m PBT, and EPS of 7.5p = PER of 8.9 - starting to look attractive value (at a third of IPO price!). Forecast balance sheet is OK, and has about £11m NTAV. My view - I was expecting to dismiss this, but actually it’s now looking sensibly priced, for quite a decent, profitable small business. Lots more detail in the RNS. Worth a closer look, to put it on the possible buys list for later, I think. I don’t see any rush to get involved here.

Forterra (LON:FORT) 296p (up 2%) (£646m) [No section below] - very good interim results from this brick maker. I like the strong profit margins too. Positive outlook, FY 12/2022 profits to be “slightly ahead” of expectations. I like the balance sheet - dominated by huge fixed assets, but all bought & paid for, with no net debt (net cash actually, at £24.1m). Decent divi yield of 4.7%. Looks a very nice value share, if you think strong demand is likely to continue. High StockRank of 92. Thumbs up from me.

Fintel (LON:FNTL) 200p (down 1%) (£207m) [No section below] - a trading update for H1 of FY 12/2022. “Core” numbers strip out the effect of disposals - H1 revenue up 9% to £27.1m, adj EBITDA up 5% to £8.7m. Zeus (many thanks!) forecasts FY 12/2022 EBITDA of £19.0m, which is 12.0p adj dil EPS. So a PER of 16.7 - looks a bit pricey in a bear market. Although much revenue is recurring. Last balance sheet at Dec 2021 looks thin, with negative NTAV of £(8.1)m. Although plenty of liquidity now, with cash of £7.6m, an undrawn RCF of £45m at June 2022. Small divis. My view - looks a decent business, with nice recurring revenues. A bit pricey for me though, in current market conditions.

Discoverie (LON:DSCV) 738p (up 8%) (£705m) [No section below] - A good Q1 (Apr-Jun) trading update, with strong organic revenue growth of 17%, with another 10% on top from acquisitions. Profits are ahead of expectations. Record order book (up 40% organically in a year) at June 2022, but expected to “begin to normalise” as the year progresses - have customers been building up inventories maybe? Margins resilient. Chip shortages have improved, but “remain tight”. Sri Lanka is 6% of group production - OK so far, but contingency plans made. Acquisition is on track. “Well positioned” overall. My quick view - looks a good business, performing well. Priced accordingly at a PER of c.20.

Graham's Section:

Aptitude Software (LON:APTD) (£198m) - The full-year outlook is unchanged at this enterprise software group. Organic growth is reported at 10%, and total growth is much higher after an important acquisition completed late last year. The company has an impressive cash balance but the overall balance sheet strength is limited. Operationally the company appears to be performing well with good momentum. Valuation remains a niggle for me but I can’t deny that much of the air has already come out of this stock.

Restore (LON:RST) (£613m) (+0.9%) [no section below] - this is a group of five support services businesses. Jack last covered it here. Today’s half-year results show 32% revenue growth, of which 19% is organic and 13% relates to acquisitions. I suspect that these results still include an element of recovery from the Covid-induced downturn. Adjusted PBT increases by 36% to £21.2m and the company includes a helpful bridge to show how this was achieved: price increases mostly offset cost increases, and there was a huge bounce in activity levels compared to last year. Net debt is now over £100m and more acquisitions are coming in the pipeline. I agree with the StockRanks which argue that there’s limited value on offer here (PER 16x) but potentially this is compensated for by a lower risk profile than most small-caps.

SRT Marine Systems (LON:SRT) (£51m) (-4.5%) [no section below] - this is a company with a long track record of promising investors the world, and delivering very little. It describes itself as “the global leader in maritime surveillance, security, management and safety products and integrated systems”. Revenues and cash flow are lumpy and unpredictable, as large contracts are negotiated in far-flung parts of the globe.

Today’s results show a £6m loss on £8m of revenues. The poor performance necessitated an equity placing during the year. But it’s not all bad: there’s a £600m “validated sales pipeline” (?), and the long-standing CEO says he has “started to see strong demand return for our products… which I expect to be reflected in next years (sic) financial results”. Plus ça change.

Trackwise Designs (LON:TWD) (£15m) (-10%) [no section below] - this company releases its 2021 results very late: the delay was previously blamed on “the cumulative impact of Covid-19, including related staffing absences”. The results show revenues up 32% to £8m and a small adjusted operating loss (excluding share-based payments and new facility set-up costs).

Balance sheet - the 2021 Auditor’s Report will include a Going Concern warning. TWD already raised £7m in early 2022, but the net debt position still rose to nearly £8 million by the end of June. The outgoing CFO Mark Hodgkins, says that in a “severe but plausible downside scenario”, in which it failed to secure the facilities it is currently negotiating, the company would face a fresh shortfall of £6.8m.

Profit warning - revenue from TWD’s most important customer has been “delayed” and brokers have this morning slashed their FY 2022 revenue forecast by 53% to £10.5m. They forecast year-end net debt of £14.5m, which looks very dangerous to me in these circumstances. I consider this stock uninvestable.

[Paul adds: Thanks for this Graham! I was warming to TWD as a speculative punt, but your update today has put me off. Looks more risky than I suspected when I looked at it here in June. Interesting new products, but I'd like to see more secure finances before investing here.

EDIT: Also note there is an InvestorMeetCompany webinar which is available as a recording, which I watched over the weekend. Management say the audit disclosures were required, but that they believe they can plug the funding gap mainly with new borrowing facilities which are in negotiation, e.g. for HP on capex, (£4.4m), a £1.9m trade finance loan, and £1.4m from improved payment terms from their nickel supplier from 2023)]

Explanatory notes -

A quick reminder that we don’t recommend any stocks. We aim to review trading updates & results of the day and offer our opinions on them as possible candidates for further research if they interest you. Our opinions will sometimes turn out to be right, and sometimes wrong, because it's anybody's guess what direction market sentiment will take & nobody can predict the future with certainty. We are analysing the company fundamentals, not trying to predict market sentiment.

We stick to companies that have issued news on the day, with market caps up to about £700m. We avoid the smallest, and most speculative companies, and also avoid a few specialist sectors (e.g. natural resources, pharma/biotech).

A key assumption is that readers DYOR (do your own research), and make your own investment decisions. Reader comments are welcomed - please be civil, rational, and include the company name/ticker, otherwise people won't necessarily know what company you are referring to.

Paul’s Section:

Hotel Chocolat (LON:HOTC)

134p (pre market open)

Market cap £184m

Has gone into Court protection, whilst it tries to restructure & raise more capital.

HOTC’s exposure -

- Loan of £23m outstanding,

- Guarantees of up to £5.8m re leasing company loans.

My opinion - this is really just confirming what was said 9 days ago, which I covered here, when HOTC indicated a full impairment against the JV loans was necessary. The £5.8m loan guarantees in addition are new to me though.

There’s not really anything to add from today’s announcement. If anything, it might be a positive, to draw a line under a disastrous overseas expansion strategy. What I don’t understand, is how has HOTC managed to squander c.£30m on a JV that it says today is only 20% owned by HOTC (I had assumed it was a 50:50 venture), and yet which produced only £5m retail sales in H2 of calendar 2021. Even allowing for some impact from the pandemic, this seems a massive investment for 20% ownership of only 31 stores, about £1m each! How is that even possible? Management seem to have made extraordinarily bad capital allocation decisions. They’re not going anywhere though, with controlling combined shareholdings.

If you’re thinking about buying/holding this share, Roland’s recent article is a must-read.

Overall, my view is unchanged after today’s (predictable) update. Management have made some terrible mistakes, and I have to question their competence. But, they’ve built an impressive brand, and the UK operations seem to have good potential still.

The other thing to consider is the big cost headwinds, that have caused FY 6/2023 forecasts to be slashed. The consensus figure on Stockopedia of 8.9p EPS could come down, as one recent broker update I saw was just 5.6p. At that level of earnings, a share price in double digits would make more sense than the current 134p.

It’s tempting to have a nibble here, but there could well be disillusioned fund managers dumping their holdings, now the big growth dream of international domination has evaporated. I see that recent TR-1 forms have been disposals by abrdn, which has reduced from 7.1% to under 5%, so presumably they’ll still be selling in the market for a while.

I’m not convinced it has de-rated enough, and with no particularly compelling reason to buy, think I’ve persuaded myself to sit on the sidelines here for a while.

The good thing, is HOTC can absorb the hit from Japan failing, because it’s mainly a write-off of a balance sheet (non-cash) asset. The £5.8m loan guarantees would be cash outflows, but that’s affordable within existing resources. Hence risk of dilution from a placing, is close to zero, in my opinion, nothing to worry about there (assuming there's no more material bad news yet to come).

There is de-listing risk though, given management controlling shareholdings, and after the humiliation of screwing things up badly, they might decide to take the company private. I don't trust their judgement, so think I'm talking myself out of wanting to invest here. Let's see where the dust settles.

.

.

Headlam (LON:HEAD)

306p (down 1% at 08:46)

Market cap £257m

Headlam Group plc (LSE: HEAD), the leading floorcoverings distributor, is providing a Pre-Close Trading Update in respect of the first six months of the year to 30 June 2022 (the 'Period') ahead of announcing interim results on 6 September 2022.

Company headline - is a concise and accurate summary -

Improved profitability despite economic backdrop

My summary -

H1 revenue £323.8m down 1.9% on H1 LY (that’s OK, as the StockReport shows forecast revenues for FY 12/2022 are flat vs LY)

UK revenues down 2.9% (weakness in residential), with the small France/Holland division up 5.1%, partially offsetting UK weakness.

Underlying PBT improved, at £17.3m for H1 (up 3.6% on H1 LY)

Operational efficiency & cost control drove the profit increase.

Believed to have increased market share.

Prices increased, driven by manufacturers - helped to offset operational cost inflation. (This must mean volumes dropped more than the 1.9% drop in revenues, given that prices increased)

Outlook - strikes me as good, in the current tougher macro conditions -

Currently, the Company remains on track to meet market expectations4 for the year, although the marketplace will undeniably continue to present weakness on the residential side and operational cost inflation headwinds remain.

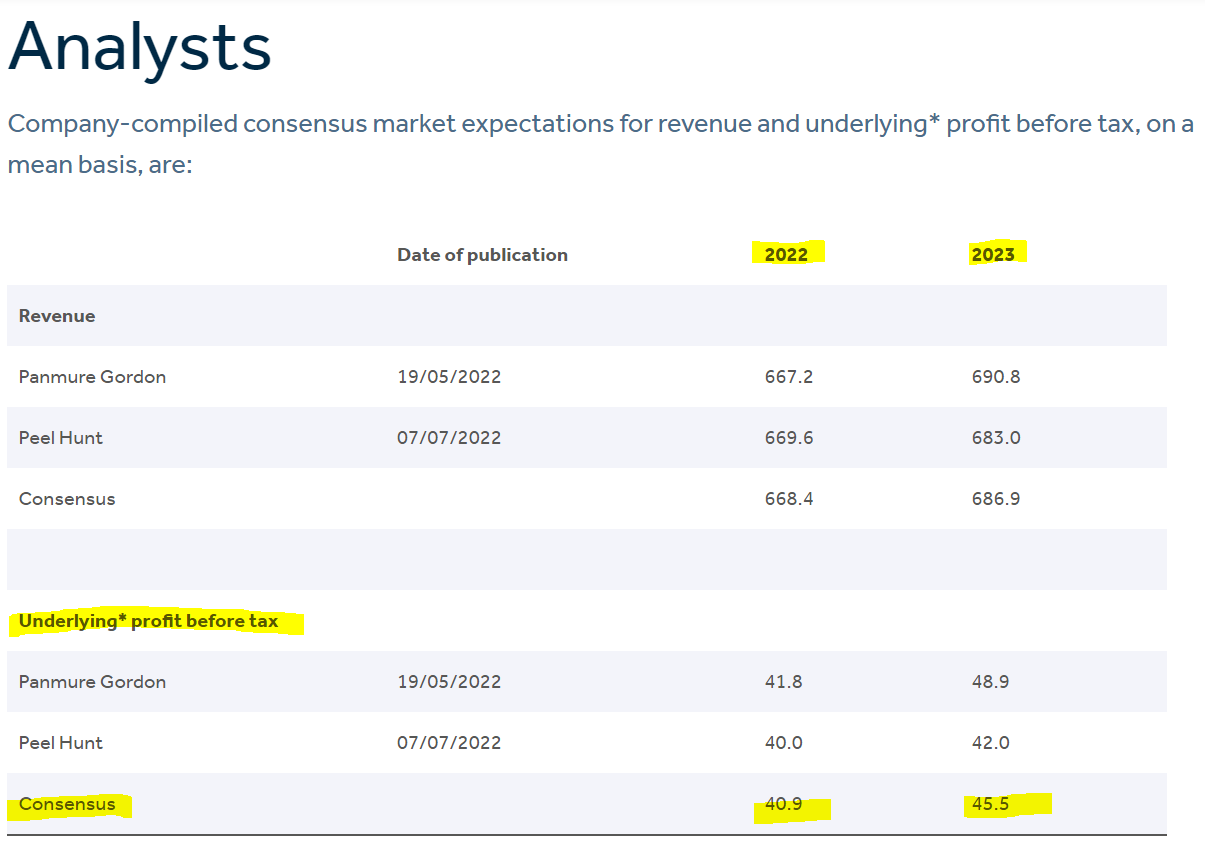

4Company-compiled consensus market expectations for revenue and underlying profit before tax, on a mean basis, are available on the Company's website at www.headlam.com.

This link is better, as it takes you to the actual page you need, instead of wasting time looking through the website trying to find it!

This is great info (copied below).

If HEAD can publish broker forecasts on its website, even for a shy one like Peel Hunt, why can’t everyone else? Maybe companies need to insist on being permitted to publish this info on their investor relations websites, when signing up with a new broker?

.

These numbers look consistent with the broker consensus figures on Stockopedia (which are different, because they’re post-tax, and EPS).

That means the current year PER is about 8.4, dropping to 8.0 next year. That seems cracking value to me. Maybe the market is worried that consumer food/energy squeeze might trigger an H2 profit warning? That’s possible I think, so some allowance probably should be factored in for weak macro.

The CEO says -

"We are pleased with our performance thus far in 2022, particularly given the economic backdrop.

Profitability has been improved, market share gains made, and our strategy is proving to provide a countermeasure and protection against a weaker underlying market.

We believe we are set fair especially for when headwinds ease."

Net cash/ Balance sheet - Net cash has dropped a lot, it was £53.7m at Dec 2021 year end. That has now dropped to only £6.0m at end June 2022. How come? £25.8m has been paid out to shareholders, including both last year’s final divi, plus a special divi, and it’s also doing daily buybacks too.

Other reasons given for cash falling - stocking up ahead of busier season & new product launches, and capex for expanding the trade counters side of the business.

I don’t think this is a worry, as HEAD is very soundly financed, with a lovely balance sheet. As the company points out today, it owns freehold property in the books (2020 valuation) at £110m - amazing really, for a £257m market cap company with no debt.

Hence shareholders here do not need to fear either solvency, or dilution, even if the economy deteriorates.

My opinion - the share price has fallen a lot, which is nothing to do with the company’s performance, which remains good.

This is an excellent value share, in my opinion. You’ve got the safety of a really strong balance sheet, no debt, loads of freeholds, and a twice-covered divi yield of 6% protecting you against inflation, and/or providing an income.

Sure, there’s a risk of an H2 profit warning if consumers switch off discretionary spending in the autumn, which is probably why the share price is on the floor. But it’s becoming more obvious by the day that Governments will have to take more decisive action to mitigate soaring energy costs later this year. Plus plenty of households have savings, and so can afford to replace carpets regardless.

The commercial sector declined during the pandemic, whilst residential did well. That’s probably reversing somewhat now.

HEAD has a really good business model - selling a wide range of large, bulky products, which customers couldn’t realistically stock themselves. So customers need HEAD, and the wide range & bulk buying power creates a barrier to entry for competitors. There's also a longer term opportunity to maybe even sell direct to consumers?

I wouldn’t normally be interested in buying this type of cyclical share in an economic downturn, but HEAD is doing a lot of self-help stuff, to make the business more efficient. Hence why it has been able to absorb a downturn in revenues, whilst still reporting increased profits. That protects profitability now, but also gives a springboard for future growth when the economy has calmed down, and inflation falling. Also, it's all about valuation - I think the share price has overshot on the downside, for investors taking a longer term view.

A solid thumbs up from me. I’ll be buying back into this share later this year. It’s tightly held, so surprisingly difficult to deal in.

It got irrationally cheap during the pandemic too, then recovered strongly. I imagine, at some unknown point, we're likely to see a repeat of that in future -

.

Graham’s Section:

Aptitude Software (LON:APTD)

- Share price: 345p (pre-market)

- Market cap: £198m

Looking deep into the archives, I previously thought that this enterprise software provider was overvalued at 544p.

It has been a bumpy ride for shareholders:

Today’s interim results benefit from an October 2021 acquisition that was described by Jack here.

Strip that out and the organic growth rate at Aptitude is around 10%. Which is perfectly good, but not enough on its own to justify a very high rating for the stock.

Aptitude tends to enjoys a high rating and this remains the case today, even after stock has deflated so much:

Some key points from the interims:

- Annual Recurring Revenue £49m (up 10% organically, at constant currencies)

- Total revenue for H1 2022: £36.1m, of which £24.4m was recurring in nature.

- Cash £23.6m, net cash £13.5m after subtracting financial liabilities.

- Balance sheet equity £59m, but negative net tangible asset value.

- Outlook for 2022 is in line with expectations.

The balance sheet doesn’t give any cushion in terms of NTAV and while the cash balance is impressive at nearly £24m, some of this may be required to help deliver £30m of deferred income (products paid for upfront by customers, and delivered over time - this is normal in software businesses). The company says H2 is seasonally stronger for cash.

While this balance sheet doesn’t worry me, I don’t think it offers much of a buffer and I wouldn’t say that it’s a positive factor when it comes to valuing the business as a whole. Aptitude used up its previous balance sheet strength to get the 2021 acquisition done.

Operational highlights - lots of positivity here. It’s not hard to imagine the value of Aptitude’s solutions in the subscription-based world we live in. So hopefully the company can keep going on this positive trajectory. I also note Aptitude’s launch of Fynapse, its new finance management platform for CFOs.

From the statement:

The Group is confident that Fynapse will accelerate the Group's growth in the medium and long term whilst also generating higher gross margins due to the cloud native technologies on which the platform is built. Fynapse provides differentiated finance digitalization capability to a market in which the Group already has outstanding credentials with the successful Aptitude Accounting Hub.

My view

For this type of software company, I tend to check the market cap as a multiple of recurring revenues. In this case, the multiple drops out at 4x.

I’ve seen many examples of companies trading higher than this - e.g. Quartix Technologies (LON:QTX) which trades on six times recurring revenues.

Of course margins and profitability should also be taken into account, and if there are any other risks such as customer concentration. According to the most recent Annual Report, Aptitude did not have any customers accounting for more than 10% of total revenue. So I’m going to assume that customer concentration is not a factor here.

Given the modest organic growth rate of 10%, I still find it difficult to get on board with the market’s valuation of Aptitude.

But when I looked at this company two and a half years ago, it was trading at more than 10x recurring revenues, not 4x.

At 4x, it makes much more sense, especially for someone who thinks that organic growth can accelerate from the current level.

See what our investor community has to say

Enjoying the free article? Unlock access to all subscriber comments and dive deeper into discussions from our experienced community of private investors. Don't miss out on valuable insights. Start your free trial today!

Start your free trialWe require a payment card to verify your account, but you can cancel anytime with a single click and won’t be charged.