Good morning, it's Paul here.

Election Day today, so should be interesting.

I finished off yesterday's report in the evening, with 3 new sections on companies that we've not discussed before here, namely;

Global Ports Holding (GPH) - independent owner/operator of cruise ship ports - thanks to sharw and jwebster, for adding excellent reader comments expanding on my review of GPH - very helpful indeed & informative. It does look as if this might be a bit risky, hence best avoided perhaps?

Eurocell (ECEL) - looks quite interesting - a profitable & reasonably priced building products company. Looks quite similar to Epwin. Good value maybe?

DWF (DWF) - acquisitive law group.

Here's the link to yesterday's completed article, to get you started on Thursday morning whilst I think up what to write about the fresh news out on Thurs morning.

Estimated timings - I'm hoping to be finished by 2pm

Update at 13:39 - today's report is now finished.

Zytronic (LON:ZYT)

Share price: 182.5p

No. shares: 16.0m

Market cap: £29.2m

(at the time of writing, I hold a long position in this share)

Further comments from me, as I've now had time to properly read the results commentary. My initial review of the numbers for FY 09/2019, & outlook statement, are here, in Tuesday's report. Therefore the points below are additional points not covered in Tuesday's SCVR here.

Positive

The outlook sounds quite positive;

The lack of growth this year has resulted not from a lack of opportunities, but from a slower than normal conversion of the larger projects into sales. As Mark Cambridge, CEO, explains in his review, in terms of opportunities the number of live projects has increased by 41% during the year.

Vending market is growing (third largest market for ZYT), but not enough to offset losses in gaming & financial

Big increase in sales pipeline, specific figures given;

As at 30 September 2019, there were 494 opportunities in the system with a projected value of £83m, 58 classified as Projects, and are expected to generate £13.4m of sales over their future production cycle. This compares with data as at 30 September 2018 of 414, £65m, 41 and £8.0m respectively.

Sounds as if production yield issues have been fixed, and costs reduced - better performance in future then perhaps?

Prudent accounting policies - e.g. capitalises very little into intangible assets - only £144k capitalised in FY 09/2019, less than £430k P&L amortisation charge.

Management commentary is always very straightforward, telling it like it is. Hence outlook comments have more weight than at perma-optimist companies.

Negative

Largest market is gaming - ie. casino machines - is struggling. Reason given is 2 existing projects "moving significantly towards end of life". Does this imply further falls in gaming sector revenues could be ahead?

Second largest market (financial - ie. ATM machines) is also struggling. Problem is move towards cashless transactions, e.g. card payments, and online transactions growing, cash reducing.

Trend of profits has been downwards for 3 years, and is forecast to continue to fall in FY 09/2020. Although there could be scope to surprise on the upside perhaps, with expectations set low (FY 09/2020 forecast of 13.6p EPS, versus actual of 16.8p for FY 09/2019)

Sitting on unnecessarily large cash pile of £13.1m - although a nice problem to have!

My opinion - largely unchanged. The run-off of end of life projects in its 2 main markets is a concern. However, it also has growth potential, and a strong, growing pipeline. Therefore, the prospects for this share will rest on how successful management is in converting a big pipeline of opportunities (c. 4 yrs worth of potential sales) into actual sales.

Given that the net cash pile is 82p per share, and the business remains decently profitable & cash generative, even on reduced revenues, then this looks low risk to me. I think risk:reward looks good, for investors who are prepared to be patient.

The downside is that the company may not be able to replace end of life projects with new projects, in sufficient size to make up the shortfall.

Note that the company has recovered in the past from setbacks.

It has paid 143p in total dividends, since the financial crisis in 2008. Plus built up an unnecessarily large cash pile over and above that. A superb track record.

Superdry (LON:SDRY)

Share price: 479p (down 4.5% today, at 10:52)

No. shares: 82.0m

Market cap: £392.8m

This is a well-known fashion brand, selling through its own retail branches, online, and wholesale. The founder, Julian Dunkerton, the founder, took back control after hired management made a mess of things.

There seem to be some similarities with the predicament that Ted Baker (LON:TED) finds itself in. Although SDRY doesn't seem quite as bad as that, due to having a stronger balance sheet.

Bad results were expected, and the out-turn is just below breakeven in H1, at -£2.3m underlying loss before tax (down from £12.9m profit LY H1).

There seems to be an H2 profit weighting, as LY it produced £41.9m full year underlying profit before tax (so 31% in H1, and 69% in H2). The prior year it made a profit of £97.0m, so profitability is rapidly collapsing here.

The big question is whether the founder can stop the rot, let alone turn it around? His strategy of focusing on more desirable fashions, and full price sales (as opposed to constant promotions) makes a lot of sense.

On the positive side, I think there are some signs of a turnaround (or at least stabilising things) in the commentary, but it's still early days. A company this size takes a few years to turn around, if that can be done at all (and usually turnarounds in this sector fail).

Online sales could help stop the rot, replacing High Street sales, but that's not happening - it's a big concern that online sales fell -10.7% in H1. I wouldn't be interested in buying into any retailer where online sales are going backwards.

Wholesale - the main worry here is bad debts, as customers go bust. Note there was a £6.9m charge in the period for irrecoverable debts. A key question is what concentration risk there is. Who are the main debtors, and what is the strength of their finances? More bad debts seem likely to me.

Dividends - greatly reduced to just 2.0p in H1 (LY H1: 9.3p) - I can't see the point in maintaining a smaller divi, it would be better to cut it altogether, to preserve cash.

Net debt of £9.3m looks fine to me.

Going concern - this is a big worry. Whilst there doesn't seem to be any imminent threat to viability, looking a few years forward, that could change;

The Board reports that, having reviewed current performance and forecasts, it has a that the Group has adequate resources to continue operations for the foreseeable future.

This is further supported by our existing uncommitted facilities and the £70m revolving credit facility that was secured in January 2019. For this reason the Group has continued to adopt the 'going concern' basis in preparing the financial information.

As disclosed in the Group Annual Report FY19, a sustained downturn as a result of the new strategy not turning the business around, and a failure to renew the revolving credit facility in January 2022, would threaten the viability of the business over the four-year viability period.

That's a full & open disclosure, but it flags up that the downside risk here, if things go wrong, could be a total loss for shareholders. That's probably enough to scare me off.

My opinion - I feel that Dunkerton might succeed in turning this company around. However, it's fraught with risk, hence in my view, this is not something I would want to speculate on.

It ultimately boils down to product. If they get the designs right, and wow the customers again, then the business could recover somewhat. But it's up against horrible macro headwinds, as shoppers increasingly desert the High Street, and employee costs rise.

IFRS 16 has dismally failed to give me any meaningful information on the key issue - how quickly SDRY could exit from loss-making shops. Lease liabilities don't matter a jot, if a company is trading profitably from each site. However, if a company is locked into leases from which they trade at a heavy loss, then that could pull down the whole company.

Therefore, the information that investors need is a table, listing every lease, whether or not the site is profitable, and the time to expiry or break clause. Without that detailed information, we're really in the dark.

Overall, for me, this looks too risky for me to want to get involved.

Purplebricks (LON:PURP)

Share price: 104p (flat on the day, at 11:55)

No. shares: 306.8m

Market cap: £319.1m

Purplebricks Group Plc (AIM: PURP), a leading estate agency business, announces its Interim Results for the six months ended 31 October 2019

The original, rapid, international growth plan for this online estate agent, hasn't really worked - with US and Australian operations being closed.

Interim results today seem lacklustre - like-for-like ("LFL") revenues up only 1.9% to £64.8m in H1.

Adjusted operating profit of only £1.6m (down 74% on H1 LY)

So why on earth is it valued at £319m market cap? Possibly because it is the leading brand in online estate agency in the UK? Brand awareness is 97%, but not necessarily positive awareness, given those infuriating TV ads. Plus maybe investors are assuming that growth in housing transactions may return in future?

Balance sheet looks fine, with plenty of cash. No issues there.

My opinion - now that the growth potential seems fairly limited, I can't get excited about this.

In the last 3 years, this share went from £1 to £5, and has now come all the way back down again. Yet it still looks over-valued, given that the growth potential seems to have largely fizzled out.

My family bought a flat through PurpleBricks, and found them largely useless. It's really just a facility for private sellers to get their property listed on Rightmove, and a simple app for potential buyers to contact the seller.

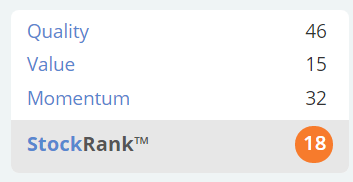

Stockopedia's clever algorithms also reject the offer, with a lowly StockRank;

Costain (LON:COST)

Share price: 158p (down 18% today, at 12:20)

No. shares: 108.3m

Market cap: £171.1m

Trading update & A465 contract

Costain, the smart infrastructure solutions company, today issues an update on the Group's contract with the Welsh Government for the construction of the A465 Heads of the Valleys road (the "A465 Contract") and the Group's trading for the year ending 31 December 2019 ("FY19").

A465 contract - this is a dispute between Costain & the Welsh Govt. An adjudication has decided to split the costs, whereas Costain had previously thought it would win. It describes this as disappointing, but doesn't spell out the financial impact, which is being negotiated. £40m of cash is being withheld on the A465 contract, so it looks quite a significant problem of about £20m loss, if we assume half the withheld cash is likely to be recouped maybe?

The rest of the business is performing in line with expectations.

Contract wins leave the order book "healthy", flat against last year, at £4.2bn. This includes £1.1bn relating to HS2, so if this is cancelled by the new Govt, that could be a serious problem, perhaps?

Overall trading for FY 12/2019 -

As a result, the Group now expects FY19 underlying operating profit to be in the range of £17 million - £19 million and the year-end net cash position to be c£20 million, with the net cash position being impacted by c£40 million of cash currently withheld on the A465 Contract.

Valuation - there's an updated broker note out today, which slashes FY 12/2019 forecast to 10.9p, due to the one-off contract loss of about £20m. FY 12/2020 is forecast to bounce back to 20.6p EPS, for a PER of 7.7 - which looks decent value.

Balance sheet - the receivables & creditors numbers are so large, that it's difficult to assess. Although this does at least have a decently positive NTAV of £120m. That's a lot better than some other contracting companies.

My opinion - this RNS is a great example of why I avoid all contracting companies these days. They're dealing with lots of large, complex projects, often only earning a modest profit margin, yet the contracts are very risky. Unexpected costs, or remediation work, can crop up unexpectedly, and wipe out a lot of the profit - which is exactly what has happened here.

It doesn't look life-threatening for the company though. So if you like Costain, then today's announcement could be a buying opportunity, to grab some shares at an 18% discount, for a one-off factor that is probably likely to be forgotten after a while.

It's not for me though, as I eschew the entire sector, after so many similar companies have gone badly wrong.

I'm running out of time now, as have to travel to London shortly, for an election party, then a lunch tomorrow. So don't expect too much from tomorrow's report!

Titon Holdings (LON:TON)

An interesting little building products company, with a very strong balance sheet relative to its size.

Results for FY 09/2019 seem lacklustre, with underlying PBT down 22% to £2.15m.

EPS of 14.5p looks a miss against forecast of 15.5p.

Good net cash position.

Current trading "challenging" for Oct-Nov 2019.

Share price is down 10% today to 122p, which strikes me as about the right valuation.

Dividend yield is about 4%, assuming that is maintained.

Overall, not madly exciting, but not terrible either. Although it has had a nice steady track record of revenue & profit growth in the last 6 years, as well as paying OK dividends.

Vianet (LON:VNET)

Interim results look fairly good, with revenue up 9.5%, and adj operating profit up 11.1% to £2.0m for H1.

This is the Brulines cash cow business, plus some small, but growing operations in vending machines telemetry.

It's always looked a potentially interesting little company, but growth has been painfully slow.

At 148p, I think it's probably priced about right. It's talking about accelerating growth, from upgrades, and cross-selling. There's a useful 4% divi yield too. Quite good overall.

Billington Holdings (LON:BILN)

A positive trading update today, together with an upbeat outlook for 2020, for this structural steel company.

The directors of the Company anticipate revenue for the financial year ending 31 December 2019 will be higher than the current market expectation of £78 million following the successful completion of a number of large projects in the year.

Pleasingly, profits are also expected to be above the market forecast of £5.2 million and we envisage the level of cash generation to be similarly positive.

That's very good. Although this is a cyclical business, so am not sure I'd want to get involved at this stage of the cycle.

The valuation looks quite attractive though, but cyclical companies often look cheap near the end of the economic cycle, and then see profits crash once the economy goes into reverse. Although we don't know for sure where we actually are in the economic cycle until after the event, so it's tricky.

Tungsten (LON:TUNG)

Poor interim results. It's still loss-making, showing little growth, and has a very weak balance sheet. I think it looks as if another equity fundraising will be necessary, but who would want to support it, given the dismal track record & failure to deliver on all the hype in the past?

Personally I wouldn't touch it, far too risky.

Robinson (LON:RBN)

A decent update for FY 12/2019 from this packaging company;

Revenues for 2019 are anticipated to be £35m, which represents a 7% increase on last year. The directors anticipate profits for 2019 will be ahead of current market expectations, reflecting the benefit of falling resin prices in the current year.

The share price has responded with a 11% rise today.

The PER looks low, and dividend yield high. Very illiquid share though, so it's difficult to get in & out of, as with many micro caps.

That's all I've got the time & energy to cover today!

As always, thanks for your comments below.

See you tomorrow, when we'll know who is going to be running the country.

Regards, Paul.

See what our investor community has to say

Enjoying the free article? Unlock access to all subscriber comments and dive deeper into discussions from our experienced community of private investors. Don't miss out on valuable insights. Start your free trial today!

Start your free trialWe require a payment card to verify your account, but you can cancel anytime with a single click and won’t be charged.