Good afternoon! It's Paul here. I've got the whole afternoon free, so will be updating this article gradually until teatime.

Interquest (LON:ITQ)

Share price: 28p (down 1.8% - back from temporary suspension)

No. shares: 38.7m

Market cap: £10.8m

Appointment of NOMAD and broker - this announcement is particularly important, because Interquest's shares had been suspended due to the company firing its NOMAD. Moreover, management (through a vehicle called Chisbridge Ltd) had attempted to buy out the company's minority shareholders through an offer at 42p. The offer failed to secure enough acceptances to allow the company to delist.

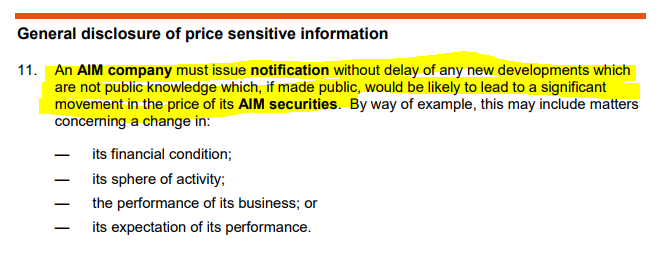

Yet Interquest then announced here on 6 Sep 2017 that it had given 1 month notice to sack its NOMAD on 10 Aug 2017! So this vital information was withheld from the market until just a few days before the 1 month notice was due to expire. This issue has arisen before, with other companies. It seems to me that giving notice to sack your NOMAD is very clearly price sensitive information under AIM rule 11;

So there's no question that the sacking of a company's NOMAD, leading to the suspension of its shares, is very significantly price sensitive. So a breach of AIM rule 11 has obviously happened, in my view. What will happen - nothing of course, there are rarely any consequences for breaching AIM rules. It only has a very thin veneer of regulation, which are often flouted, unfortunately.

It very much looked as if Interquest was deliberately trying to de-list by the back door, by firing its NOMAD. However, rather suprisingly the company has today announced the appointment of a new NOMAD, Allenby. The shares have therefore come back from suspension, and can be traded once again, as from noon today.

Today's announcement is worth reading, and covers the following points;

A relationship agreement has been enterered into between Interquest & Chisbridge, in order to ensure that Interquest is managed in the interests of all shareholders. I imagine that the NOMAD and broker probably insisted on this before taking on the roles.

A further NED (independent of Chisbridge) is to be appointed. Remember that during the attempted takeover, the only independent Director opposed the deal. I can't help feeling that having to put independent people on the Board to stop the other Directors doing things to harm independent shareholders, is just an admission that the whole board & company is dysfunctional as things currently stand.

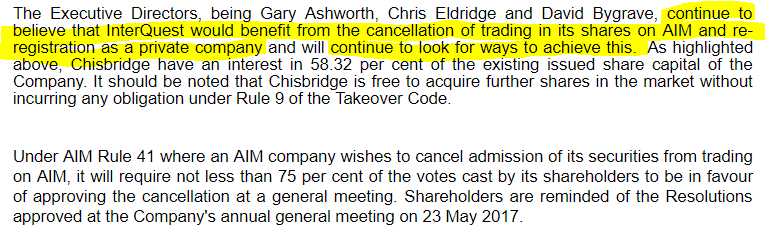

As usual, there's a sting in the tail - Directors making it clear that they won't give up trying to de-list, they just need to find a way to do it;

My opinion - I feel we're not being told the full story here. If the Directors don't want the company to be listed, then why have they appointed a new NOMAD? I wonder if minority shareholders might have either shamed, or threatened legal action against the company?

It would have set an appalling precedent, if a company had de-listed by simply sacking its NOMAD. Yet it does seem to be a glaring loophole in the AIM regulations, which needs urgent attention.

De-listing

De-listings are a shareholder's worst nightmare. When a company announces its intention to de-list, then it can easily trigger a 50% plunge in share price, almost instantly. The trouble is that this can be a devious way to force out minority shareholders - many of whom are not able to hold shares in private companies.

Therefore, I think we all need to really carefully consider the risk of any shares in our portfolios de-listing. Generally, the smaller the market cap, then the more difficult it is to justify the expense of maintaining a stock market listing.

How committed are management to the listing? Is there a dominant shareholder (e.g. Gary Ashworth at Interquest) who might attempt to scupper the listing if they wish? How trustworthy are management?

I think the risks at really tiny companies are such, that I'm increasingly trying to avoid shares with a very small market cap (say, under £20m). De-listing is one of the biggest risks, especially as it often comes after a period of poor performance at the business - so it's heaping more misery onto shareholders who have already seen the value of their shares plunge.

Needless to say, given the track record of the Directors at Interquest, that share is totally uninvestable now, in my view. As indeed, any other company with the same Directors involved, would also be uninvestable.

Revolution Bars (LON:RBG)

Share price: 209.6p (down 0.6% today)

No. shares: 50.0m

Market cap: £104.8m

(at the time of writing, I hold a long position in this share)

In all honesty, I haven't even bothered to read all the announcements from Deltic/Ranimul on their merger proposal, since it just doesn't appeal, and I think is very unlikely to get much support from RBG shareholders. The problem is that Deltic/Ranimul management want to run the combined entity. That would give them personal control, through not only being the new Directors, but also owning 35% of the enlarged group. Yet who are they? Why would RBG shareholders want to put ourselves in their hands? Existing management may not be perfect, but they have limited control, due to small personal shareholdings, so we can kick them out easily, if we (shareholders collectively) want to.

My sector expert also tells me that Deltic is a poorer quality business than Revolution. The main reason being that it operates from larger sites, focused on the nightclub market. This is more cyclical than the town centre, broader market served by Revolution, which includes all-day opening, (not very good) food, and premium cocktails. So Deltic's sites require continuous, heavy capex, given that they are such big sites. Also Deltic was previously called Luminar, and went bust a few years ago, which reinforces worries about cyclicality, capex, etc.. Mind you, Luminar did have a very weak balance sheet, with a lot of debt.

EDIT: another reservation I have about the Deltic proposal, is that Deltic shareholders could simply be eyeing Revolution's stock market listing as an exit route from their own shareholdings in Deltic. So if the merger proposal were to go ahead, then Deltic shareholders might depress the enlarged group's share price by offloading their shares gradually into the market.

Why is the RBG share price still comfortably above the 203p cash offer from Stonegate then? My feeling is that there's a good chance that Stonegate could be forced to pay a higher price. It's interesting that Artemis has pulled its previous support for the Stonegate bid. Therefore, I am hoping that RBG shareholders vote down the bid proposal from Stonegate. That would then force Stonegate to pay a higher price.

Some broker analysis I read recently, suggested that Stonegate is only offering a price which equates to about 4 times site EBITDA. Whereas the industry average is more like 7 times. That implies scope exists for Stonegate to pay more. There is the risk that Stonegate might just walk away, which would see the share price slip down to maybe 150-160p.

Personally, I've top-sliced about 20% of my holding, and am sitting tight on the rest, to await developments. An exit at 203p wouldn't be a disaster. Yet there could be scope for a much more attractively priced bid. Stonegate is being far from generous at 203p, which Deltic emphasised in their announcements.

EDIT: The 5pm today Takeover Panel deadline for Deltic to put up or shut up, has now passed. Sure enough, Deltic has put out a statement saying that it does not intend to launch a takeover bid for RBG. This is not a surprise at all, because Deltic clearly doesn't have the money to bid for RBG.

It's difficult to avoid the conclusion that Deltic have basically been timewasters, in trying to gatecrash the party.

FreeAgent Holdings (LON:FREE)

Share price: 83p (down 8.3% today)

No. shares: 40.7m

Market cap: £33.8m

Trading update - for the 6 months to 30 Sep 2017.

This company provides cloud-based accounting software for micro businesses (sole traders & companies with under 10 employees). The main competitors are Xero (more complex to use than FreeAgent but has more functionality), and Quikbooks. I think Sage has a cloud-based offering now too.

I use FreeAgent personally for one of my little limited companies, and it's a dream to use - very simple & user friendly. The main advantage is that you don't have to key in any information - the system automatically downloads your bank transactions. Revenues are recurring, and sticky - as users pay a monthly fee. Once you're set up on any of these systems, there's really no incentive to move to another supplier. If FREE can reach a tipping point, where it recruits enough customers to move into profit, then there should be considerable operational gearing, given the 80% gross margins. So this share is really all about growth.

Today's 8.3% share price fall, suggests that the market is not sufficiently impressed with growth. Although there are only 111k reported shares traded. So as with most small caps, the market price moves in the short term, just reflect possibly a handful of trades. There could be plenty of other buyers/sellers who cannot deal in the size they want. So share prices are really rather artificial with small caps, at least in the short term. It tends to be the small trades that set the price.

Key points from today's trading update;

H1 revenues £4.6m (up 28% on H1 2016/17). Although note that H2 2016/17 revenues were £4.4m, so there has only been a £0.2m rise sequentially.

Still loss-making - an adjusted EBITDA loss of £0.4m, means that proper losses will be worse than that.

This raises the question of whether growth might be stalling? That's especially the case given that mention is made of reimbursed development spend, under a partnership with RBS. So I think the user growth numbers could be disappointing, when revealed with the actual results for H1 (no mention is made today of user growth).

Revenues & losses "broadly in line" with company's expectations, and full year outlook.

Net cash of £3.4m "comfortably ahead" of forecast.

IR35 "off-payroll" rules have been a headwind. I've googled and found this- public sector organisations have to deduce PAYE & NICs from temporary staff instead of allowing them to dodge tax through operating via their own limited company. So clearly that would be harmful for FreeAgent, as some of their customers wouldn't need to operate their own accounts, once they're on PAYE.

RBS partnership - sounds as if it's starting to deliver some sales growth.

My opinion - I just can't get excited about this share. The company is forecast to make an adjusted loss of £0.9m this year, ending 03/2018, and an adjusted profit of £0.8m the following year. Given that today's update is a bit soft, then I'd say there's a risk that the company might not meet those forecasts.

The cash position sounds fine, and on existing forecasts there doesn't look to be any need for a further fundraising.

The RBS relationship could be interesting, and provide possible upside. I'm not aware of the details, other than that the idea is to package FREE software with new business bank accounts.

Overall I'd say that the market cap of £33.8m looks about right, given where the company has got to. For me, the growth isn't rapid enough to excite me.

SRT Marine Systems (LON:SRT)

Share price: 37.8p (down 7.2% today)

No. shares: 127.7m

Market cap: £48.3m

Half year trading update - this company makes electronic devices for ships, to track their location.

There's no getting away from the reality that the company traded poorly in H1;

Group revenues for H1 2017 were 2.9 million, a 10% increase on the same period last year ("H1 2016"), resulting in a loss of 1.7 million before tax and exceptional items and a cash balance of 2.1 million as at 30 September 2017.

The achilles hell of this business is lack of revenue visibility, from projects that are frequently delayed, e.g.

No material milestones from projects were completed during H1 2017 and thus no project revenues were recognised..... We have several projects which are either pending or under contract, therefore we look forward confidently to the second half of this financial year."

Same old story - jam tomorrow.

Note that the company recently announced a flexible borrowing facility, for up to £10m. It's very expensive, at a coupon of 9.5%.

My opinion - I'm increasingly sceptical about this company. The project delays, and lumpy contracts, make it impossible to forecast performance. I really hope the company is eventually successful, but at the moment I think the market cap of nearly £50m seems completely detached from what has actually been achieved to date, in terms of revenues & profitability.

Good luck to holders, but risk:reward looks very unattractive here, to me.

Redstoneconnect (LON:REDS) - I've had a very quick look at the interim results out today from this office services company. The figures look poor to me - barely above breakeven at operating profit level. Also, receivables on the balance sheet strike me as too high. I can't see anything to spark my interest. I did hold some shares for a little while, after being impressed by a company meeting, but sold them once my interest had waned.

The outlook comments sound upbeat. Although that optimism is not showing through in the figures yet. I don't see value here - the market cap looks a bit too high to me, for a not very good business.

That's it for today, thanks for reading & commenting, and see you tomorrow.

Regards, Paul.

See what our investor community has to say

Enjoying the free article? Unlock access to all subscriber comments and dive deeper into discussions from our experienced community of private investors. Don't miss out on valuable insights. Start your free trial today!

Start your free trialWe require a payment card to verify your account, but you can cancel anytime with a single click and won’t be charged.