Good morning, it's Paul here!

Comments published before 8 am

A couple of video games companies update us today. I don't tend to invest in, or comment much on this sector, as you really need sector-specific knowledge about the quality & longevity of the various games franchises, which I don't have.

Team17 (TM17)

I'm flagging this, as the company seems to be performing well;

The Company has continued to experience strong customer traction from both new and established games since the start of the year and now expects both adjusted EBITDA and revenue to be ahead of market expectations for the current year...

It's not a share I've looked into before, but will check out & report on its next set of numbers, due out in Sept 2019.

Frontier Developments (LON:FDEV)

Record financial performance announced, but no indication of how performance has been against market expectations.

Frontier expects to report record annual revenue of approximately £89 million for FY19, which is more than two and a half times the previous financial year (FY18: £34.2 million)...

Frontier expects to report an operating profit margin of approximately 21% for FY19 (FY18: 8%) when full financial results are announced in early September 2019.

Both Liberum & Finncap cover this share, so there should be updates available on Research Tree later today, I imagine.

A recent Liberum note forecast £84.4m revenues, which the company looks to have beaten comfortably today. The broker forecast a 22% EBIT margin (same as operating profit margin), which the company looks to be below, at 21% actual.

Afternoon comments

Had a bit of writer's block today, so there's only one solution when that happens - a full English at my local Turkish LOL! On we go. Let's get this show back on the road;

Castleton Technology (LON:CTP)

Share price: 106.5p (unchanged today, at 14:13)

No. shares: 81.6m

Market cap: £86.9m

Castleton Technology plc (AIM: CTP), the software and managed services provider to the public and not-for-profit sectors, announces its unaudited preliminary results for the year ended 31 March 2019.

This company used to be called Redstone.

Reading through the results statement today, it seems to specialise in software for social housing organisations. I like the sound of that, as it immediately says to me: niche, sticky (i.e. long term) clients, solid recurring revenues, and probably little bad debt risk.

The financial highlights certainly look appealing - although as always, it's important to remember that these are often cherry-picked to be appealing! Hence more digging is always important. I'm sure many of us have been guilty of hitting the buy button just on positive highlights, only to discover that things are not quite so positive overall as the headlines suggest. For me, this share falls into that category, I'll explain why below.

Acquisitions - this group has grown partly through acquisitions. That's resulted in a rather horrible balance sheet, containing £34m in goodwill - so very top heavy.

Before considering buying this share, I would want to find out how much of the growth demonstrated below has come from acquisitions? It must be a fair bit, since goodwill is over a third of the market cap:

With acquisitive businesses I usually do a CTRL+F to search for the words: organic growth. That phrase is mentioned 6 times today, in a positive light (preceded by the words: strong, further, good levels of). The final time we're actually given some figures;

Organic growth which excludes revenue of £0.3 million and adjusted EBITDA* of £0.2 million for Deeplake, has been 7.3% at the revenue level and 13.0% at the adjusted EBITDA* level, demonstrating, as in prior years, continued operational leverage.

That sounds pretty good - in an ideal world acquisitive groups are also generating decent organic growth, as seems the case here.

Balance sheet - in my view, the group has an overly top-heavy balance sheet as mentioned above. Here are my usual key measures;

NAV: £25.3m. Once we deduct goodwill of £34.0m, this produces

NTAV: negative, at £-8.7m. For me this is a significant negative, as I really don't like buying anything with negative NTAV. Although software companies can often operate fine on a weak balance sheet, because they can charge fees in advance of providing the service.

Current ratio: calculated very simply, by current assets divided by current liabilities. This is only 0.71 in this case, which strikes me as uncomfortably low. The stand-out number is £13.9m in trade payables, which is almost certainly made up of deferred income (i.e. customers having paid up-front). Sure enough, note 12 shows £8.3m of deferred income.

Net debt: £5.1m

With acquisitive groups it's important to look for acquisition-related liabilities. There's only a minimal amount of that here. Although I do notice £1,883k liability of convertible loan notes - we should always check what potential dilution might come about, and at what price. Note 14 explains this;

Kypera Loan notes

On 31 January 2016, in order to fund the acquisition of Kypera, the Company issued £3.5 million of unsecured loan notes ("Kypera Loan Notes"), which have a term of 5 years and carry interest at a rate of 5% per annum. The Kypera Loan Notes can be converted into new ordinary shares of 2 pence each at a price of 85.6 pence per Ordinary Share. Conversion is at the option of the holder at any time during the 5-year term. The Company can redeem the Kypera Loan Notes from the third anniversary of issue if not already converted.

On 9 August 2018, MXC Guernsey Limited, a wholly owned subsidiary of MXC Capital Limited ("MXC") served a conversion notice with respect to the remaining convertible loan notes ("CLNs") it held, together with the accrued interest, amounting to £632,000 in total. The CLNs were converted at 85.6 pence per ordinary share of 2 pence each in the capital of the Company therefore 738,896 new ordinary shares of 2 pence were allotted to MXC on 17 August 2018.

Since the conversion price of 85.6p is well below the current share price of 106.5p, then it's likely the loan notes will be converted into new shares. The total of £1,883k would result in about 2.2m new shares being issued to extinguish this liability, which I calculate as dilution of 2.7% to existing holders - so not something to worry about.

Overall then, to me, this balance sheet looks a bit stretched. That's not necessarily a problem, it just means there isn't a buffer in case anything serious were to go wrong. So risk is increased with a weak balance sheet, as we've seen recently with Staffline (LON:STAF) (different sector, but same principle).

Taxation - note that both this year, and last year, earnings are substantially boosted by a negative tax charge. As you can see below (FY 03/2019 highlighted) almost three quarters of earnings (post tax) comes from the negative tax charge (which I think is brought forward tax losses - a temporary factor);

This is an extremely important point, as investors could end up significantly over-valuing the business, if applying a PER ratio to earnings that are temporarily inflated by negative tax.

Personally I would adjust the earnings figures to use a normalised tax charge, to arrive at a meaningful valuation.

Valuation - checking out the FinnCap forecast available on Research Tree, it's a detailed & useful note with some competitor analysis too, they seem to use a normalised tax charge. So I'm happy to rely on FinnCap's 7.0p EPS forecast for FY 03/2020. At 106.5p share price, the forward PER is 15.2 - which looks about right to me.

The forecast cashflow statement looks good too. Capitalised development spend is quite modest, at £1.0m p.a., so there should be scope to pay down debt rapidly - FinnCap has it being paid off in full this year, moving into a net cash position of £5.5m by March 2021. Plus there is scope to introduce divis.

Outlook - comments sound generally upbeat, but note one division has under-performed, but it doesn't sound serious;

The one area that has not yet lived up to our expectations is our Australian Operation (reported within our Software Solutions division) - we have taken action to address this, but it has had a slight impact on our outlook for next year...

Overall the outlook sounds positive;

The combination of a healthy pipeline of new business, together with our new development capabilities and our improved organisational structure, give me confidence for the year ahead and I expect that we will show continued progress in both our financial and operational metrics when we next report.

This bit also caught my eye in a positive way - I love small businesses that focus on a specific niche, and become dominant in that space. It sounds as if that might be on the cards with Castleton - although it would be important to find out who its competitors are, and how they are peforming. Is Castleton gaining or losing market share, etc?;

With our sector focus and breadth of product offering, we continue to see enormous potential to become the supplier of choice for software and IT services in the social housing market.

There remains a significant cross-sell opportunity across our existing customer base as 50% of our c.600 housing association customers only take one of our products or services.

My opinion - as I've looked through the figures & forecasts, my initial scepticism has reversed, and I've ended up rather liking this share.

It looks to be operating in a lucrative niche, and the weak balance sheet should strengthen over the next 1-2 years, from internally generated cashflow.

Recurring revenue, cash generative, and growing, there's quite a lot to like about this business. The valuation looks reasonable, providing growth continues. It's going on my watch list, as something that's worth doing more research on.

Some brief comments to finish off on;

K3 Business Technology (LON:KBT)

Share price: 210p (down c.5% today at market close)

No. shares: 42.9m

Market cap: £90.1m

K3, which provides mission‐critical business software, cloud solutions and managed services, is pleased to provide a trading update for the six months ended 31 May 2019.

Trading update -

... the Board believes that K3 remains on track to meet current market expectations for this year although results will be more second-half weighted than usual.

Management's focus on cash generation and strong financial management continues, and net debt at 31 May 2019 is 32% lower at £5.8m than a year ago (31 May 2018: £8.5m), with the improving trend expected to continue.

The strong weighting towards the second half of the financial year reflects the high proportion of software licence and maintenance contract renewals that fall in the final quarter, but also Brexit-related disruption. This was felt in prolonged customer decision-making processes, which consequently affected services activity in the period. However towards the end of H1 a number of major deals closed, with the ongoing pipeline looking very healthy.

A bit of a mixed bag there, but increased H2 weighting clearly increases the risk that forecasts may not be met.

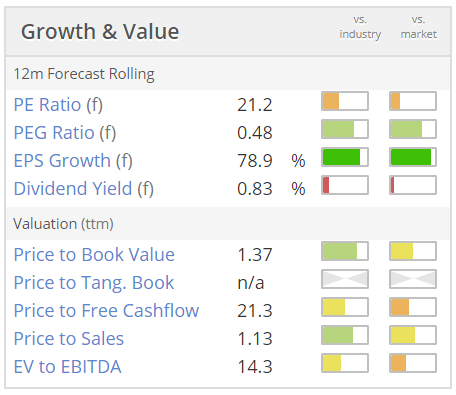

To me, this is not an attractive set of numbers on Stockopedia;

Summary of above graphic: Quite a high PER, low divi yield, weak balance sheet (whenever you see a "n/a" at Price to Tang. Book value, but strong EPS growth.

With the H2 weighting announced today, I don't find the valuation appealing at all. Risk:reward doesn't look good to me.

Access Intelligence (LON:ACC) - another small software company. It's put out an in line update today.

The shares look expensive, given that it's only small, and historically loss-making. A small profit is forecast this year.

Client list does look impressive though.

That's me done for today, sorry it took all day to finish. Sometimes writing flows easily, sometimes it's like pulling hens teeth!

Best wishes, Paul.

See what our investor community has to say

Enjoying the free article? Unlock access to all subscriber comments and dive deeper into discussions from our experienced community of private investors. Don't miss out on valuable insights. Start your free trial today!

Start your free trialWe require a payment card to verify your account, but you can cancel anytime with a single click and won’t be charged.