Good morning! Paul & Graham here for Wednesday.

Agenda -

Paul's Section:

Motorpoint (LON:MOTR) (I hold) (£178m) - a Q1 (Apr-Jun) trading update. Tough comps for Apr & May saw volumes down, but June & July have returned to normal. It's a bit vague about the outlook. Tough conditions in this sector, and forecasts have come down a lot. Expansion with new sites is underway. Tough short term, but I think this is a winner long-term, especially when the high spending internet-only startups have gone bust. Broker forecast (Shore) unchanged today.

PCI- PAL (LON:PCIP) (£42m) - a very interesting little niche software business, that is generating stunning organic growth internationally, low customer churn, and growing recurring revenues. Still loss-making and cash-burning though, and it is defending a patent infringement case, creating ongoing uncertainty & risk. Today's update for FY 6/2022 indicates trading has been ahead of market expectations, and there's more cash left than expected. I like this share a lot, but risk from legal case means I wouldn't want big exposure to it at this stage.

Skillcast (LON:SKL) - brief comments are in the comments section below main article.

Graham's Section:

Nichols (LON:NICL) (£481m) - An excellent recovery in “out-of-home” soft drink consumption is confirmed by these results, after normal socialising resumed in the UK. With 75% of its revenues generated in the UK, these results show an excellent recovery from the Covid blues. International revenue is more challenging, in particular with respect to shipping difficulties. Overall, this is another very clean and very impressive set of results from Nichols, as expected. The dividend is almost “back to normal”, too. Valuation is at the upper end of the spectrum because few companies can match the quality and safety characteristics of Nichols.

Quartix Technologies (LON:QTX) (£160m) (+0.6%) [no section below] - we covered the H1 trading update from Quartix in detail here. Today’s H1 results confirm what we were told then: the company is confident of meeting unchanged full-year market expectations for £27.4m of revenues, £5.7m of adjusted EBITDA, and £4.1m of free cash flow.

Annualised recurring revenues have reached £26m, as flagged previously. The new electric vehicle product has launched, and the vehicle checking product is coming in H2, creating some additional growth opportunities.

This appears to be a high quality company in many respects but price erosion continues to be a concern, even if it has slowed (from 6.5% to 5.6%, as reported by the company). At the end of the day, how unique is the company’s technology? Top-line growth is modest and yet the shares continue to trade at six times annualised recurring revenues.

Everyman Media (LON:EMAN) (£101m) (+2%) [no section below] - this premium cinema chain compares its H1 2022 performance to H1 2019. I agree that this is the most helpful way to do things! Trading is in line with expectations.

H1 revenues are £40.7m and EBITDA is £7.5m: both are a big improvement on 2019, thanks partly to an increased number of venues. However, EBITDA does not strike me as a useful metric for a cinema. The company is not expected to make meaningful, or indeed any, profits in the current year. At a valuation of twice book value, I would approach these shares with caution. Meaningful profits should hopefully resume by 2024.

XLMedia (LON:XLM) (£85m) (+10%) [no section below] - this used to be considered a hot stock, but now it’s just a lowly-rated online publisher that funnels customers to betting websites. Trading is in line with expectations, which is great news for a company on such an apparently low rating (the PE ratio for the current year is c. 7x, after this morning’s rally).

H1 revenues are up 38% to $44.5m, while adjusted EBITDA is up 59% to $10.5m, compared to last year. This is not an organic result: the company has raised equity and completed multiple acquisitions since the beginning of 2021, in order to achieve this. The company has a new CEO and a new CFO, and is now heavily focused on the US sports betting industry (68% of revenues). The nature of the business might be too grubby for most people’s tastes, but I’d be surprised if the new management team can’t make decent money out of this for their shareholders.

Explanatory notes -

A quick reminder that we don’t recommend any stocks. We aim to review trading updates & results of the day and offer our opinions on them as possible candidates for further research if they interest you. Our opinions will sometimes turn out to be right, and sometimes wrong, because it's anybody's guess what direction market sentiment will take & nobody can predict the future with certainty. We are analysing the company fundamentals, not trying to predict market sentiment.

We stick to companies that have issued news on the day, with market caps up to about £700m. We avoid the smallest, and most speculative companies, and also avoid a few specialist sectors (e.g. natural resources, pharma/biotech).

A key assumption is that readers DYOR (do your own research), and make your own investment decisions. Reader comments are welcomed - please be civil, rational, and include the company name/ticker, otherwise people won't necessarily know what company you are referring to.

Paul’s Section:

Motorpoint (LON:MOTR) (I hold)

198p (up 3% at 08:04)

Market cap £178m

Trading Update for Q1 (Apr-Jun 2022) -

MOTR sells secondhand cars via large out of town sites (car supermarkets) and online.

Q1 Revenue up c.30% to £402m.

Growth partly from price inflation.

Volumes down in Apr & May though, vs LY (LY boosted by re-openings).

June & July have returned to Y-on-Y volume growth.

Q1 gross margin down vs exceptional LY comps, but “more in line” with H2 of LY.

Finance commissions are lower, due to holding rate at 8.9% APR.

Pushing ahead with expansion - 3 new sites planned (each site is big, remember - there are 17 existing sites, averaging c.£75m revenues each [FY 3/2022 revenues of £1.32bn, divided by 17])

Outlook - far too vague! - I assume this means they’re trading in line with expectations, but would have liked that specifically stated - that’s the whole point of a trading update! -

As part of our recent Final Results announcement on 15 June 2022, we highlighted that the impacts of rising inflation and worldwide vehicle supply chain challenges were likely to continue to affect our markets, and this remains the case.

Despite the ongoing uncertainty, we will continue to invest with the consumer front of mind, in order to drive our strategy of significantly increasing our market share through price leadership, whilst continuing to deliver appropriate levels of profitability.

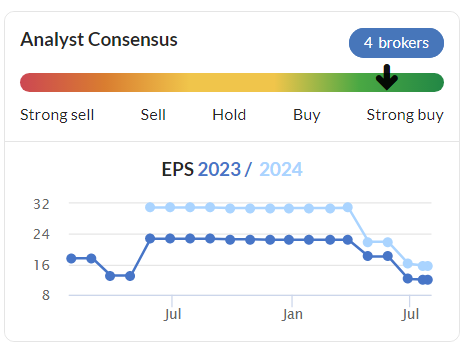

Forecasts - have already come down a lot -

.

EDIT:

Broker forecast - many thanks to Shore Capital for putting out a short note on Research Tree, which provides some useful extra colour. Shore leaves forecasts unchanged after this morning's update.

EPS of 11.7p is expected this year FY 3/2023, well down from 18.7p LY. Stockopedia's broker consensus figure is in the same ballpark, at 12.0p.

We know that car dealers generally are facing tougher conditions this year, so it makes sense to see undemanding forecasts, which hopefully reduces the risk of a profit warning. It's not cheap on a PER basis, as other car dealers are, but MOTR has a different model, and there's arguably more % upside on its profits in future, coming from a very low base.

End of edit.

My opinion - I’ve always liked the car supermarket business model - low margins, but low overheads, thus an attractive customer proposition. Easy to scale up.

MOTR is going for growth, rather than maximising profits, which is fine by me, but might unsettle some investors.

The used car market is currently distorted by many new entrants, who seem to think selling online, and spending vast amounts on advertising, is somehow disruptive. It’s not disruptive, because other companies (including MOTR) already sell online, for the small minority who actually want to buy a car in that way.

The interesting question, is what happens when (inevitably I reckon) these online new entrants run out of cash, and can’t get follow-on funding? This is exactly what happened to many loss-making startups in the 2000-2 tech boom & bust. I see $CZOO has already joined the 95% club (i.e. down 95% from its peak). I’m expecting it to join the 99%, then the 100% loss club in due course.

MOTR is about the same size in revenues as Cazoo, but makes a profit, as opposed to the hundreds of millions in losses per year that Cazoo is squandering.

There are lots of others too, competing in this space, which is heavily distorted by deep-pocketed backers, who may not be quite so deep-pocketed in future, given how much tech markets have sold off.

Hence I reckon MOTR could pick up market share gradually, as competitors go bust, or at least retrench just to survive.

It wouldn’t surprise me if BCA (a large car auctions group) bids for MOTR, to take out a fast-growing competitor, and provide more infrastructure for its other businesses.

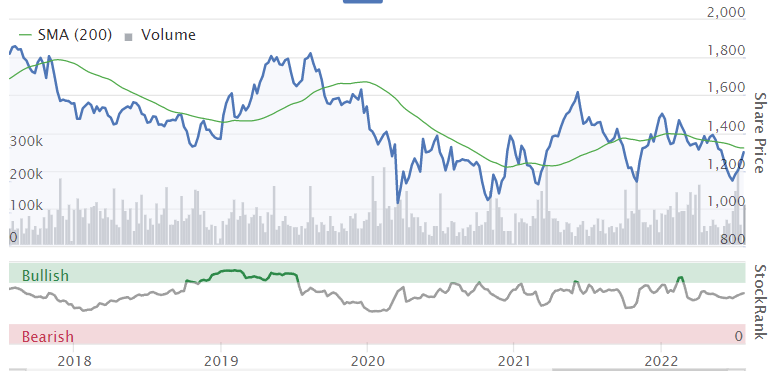

Macro factors are likely to make this sector difficult for a while, which is reflected in a share price that's near the lows, despite the business having grown considerably since it listed in 2016. MOTR has been profitable every year since listing. I believe that US shareholders have pushed it into a more aggressive growth strategy.

MOTR shares are surprisingly illiquid I've found, as they seem very tightly held. Hence, with a wide spread, it's not something to trade. I've found that it's often not possible to buy or sell more than 2,500 shares at a time.

Here's the long-term chart since listing in 2016 - as you can see, there's a nice discount for uncertainty at the moment -

.

PCI- PAL (LON:PCIP)

63p (up 7% at 08:39)

Market cap £42m

PCI-PAL PLC (AIM: PCIP), the global cloud provider of secure payment solutions for business communications, is pleased to announce a trading update for the year ended 30 June 2022.

Company’s headline -

Strong revenue growth during period of upscaling for business delivers results ahead of recently upgraded expectations

I’m giving this announcement priority here, because it’s ahead of market expectations. It comes with a very helpful footnote too - all companies should include this information, in every trading update & results statement -

Key points -

Revenue up 60% to £11.9m (consensus is £11.5m, so that’s a £0.4m revenue beat)

Still loss-making though, with guidance of adj LBT of £(2.9)m - nice to have a real profit figure quoted, instead of the more usual EBITDA (which is often misleading). This loss is £0.2m better than market expectations.

I’m a little confused as to why it quotes two different recurring revenues measures, with TACV at £13.3m, and ARR at £11.0m. But they’re both up 40-43% anyway, on a year earlier.

Customer churn - a key measure for recurring revenue businesses. It’s only 3% here - so customers look very sticky. Impressive.

Cash was £4.9m (down from £7.5m a year earlier, but only down £0.6m in last 6 months) - so it’s still burning cash, but not at an alarming rate. Forecast previously was £4.2m, so actual is a useful £0.7m ahead of that. Hopefully it should get to breakeven without another placing, although Finncap’s model shows it burning through another £3.4m this year FY 6/2023, so things could get a little tight for cash over the next couple of years - worth bearing in mind with a big legal case underway, where costs could escalate.

Patent infringement case - no update, and this looks like it could drag on for a while, inevitably casting a cloud over this share -

There is no further update on the unfounded patent case claims over and above that released to the market on 28 June 2022. The Board remains confident in its position on both the defence of the claims made and on the counterclaims made by the Company against its competitor Sycurio (previously known as Semafone).

Outlook -

"Our financial performance in the year is especially pleasing to me given it has been delivered against the backdrop of the unfounded patent claims being made against us, a very competitive recruitment market, and the recent global economic and geopolitical uncertainty.

Our high customer retention rates and market-leading partner eco-system are a credit to both our products and services, as well as our team who make the difference.

"The Board is encouraged by the continued progress being seen by PCI Pal and is therefore confident in the outlook and prospects for the Group."

Balance sheet check - when last reported at end Dec 2021. Looks adequate, with NTAV of nil. That works, because customers pay up-front, so the business is funded by about £9m of cash up-front paid by customers (reflected in deferred income creditors). However, NTAV is likely to turn negative, so dilution risk from another placing cannot be ruled out, but might only dilute by say 10-15%, so not worth worrying too much about. The risk comes mainly from the legal case I think. If that goes horribly wrong, then who knows, a bigger placing might be needed?

My opinion - I think this is one of the most credible rapid organic growth small caps in the UK market. How many other companies are reporting 60% organic revenue growth?! Because it’s mainly recurring revenues, then PICP is building an ever-increasing pipeline of high margin future revenues. That’s a cracking business model, if the rapid growth can be maintained, as a tipping point is reached, where it then becomes increasingly profitable & cash generative. That is forecast not for this year FY 6/2023, but for next year - near enough to make it interesting.

On the downside, escalating costs (particularly salaries, and the legal case) do concern me somewhat. Although +60% revenue growth is so big, that it should be ample to mop up anything, other than a large adverse legal case outcome.

Some investors are suggesting that a compromise agreement might be reached on the legal case. Who knows, I wouldn’t want to speculate on that.

Overall, there are risks with PCIP, but such good organic growth, with sticky clients & recurring revenues, makes me lean towards thinking this share could be a good punt for a small to medium sized position. I’ve held previously, but am sitting things out for now, mainly due to lack of funds! Personally at this stage I wouldn’t go big on this one, due to the uncertainty of the legal case. We can always load up (albeit paying more) once that is resolved, if it is resolved well. I’m tempted to buy a few when funds permit.

The chart seems to have found a level of decent support this year -

.

Graham’s Section:

Nichols (LON:NICL)

- Share price: 1320p (pre-market)

- Market cap: £481m

This soft drinks group has helped to enrich many people over the years, but its share price has been a bit flat recently:

Since around 2015/2016, net income has failed to make much progress, though revenues have been rising (apart from during Covid).

Let’s see the results for H1 2022:

- Revenues +19% to £80.2m

- Adjusted operating profit +24% to £11.2m (actual operating profit is £10m)

- ROCE improves to 25.2% (from 14.6%)

Please note that I view it as an enormous green flag, whenever a company goes to the trouble of calculating and highlighting its own ROCE.

Few companies do this - probably because they don’t understand its importance, or because their ROCE isn’t particularly good.

If a company reports a poor ROCE, then at least I know that it cares about this metric, and might try to improve it in future.

In the case of Nichols, we have a very strong ROCE reported, thanks to the post-Covid recovery in trading.

Performance

Geographically, there is a 29% bounce in the UK, thanks to a more than doubling of “Out of Home” revenues, as normal socialising resumed.

The Vimto brand is reported to have continued outperforming the broader squash market - soft drink volumes in the UK are down, due to the inflation that’s hitting so many key input costs (ingredients, packaging and distribution). But Vimto is holding its own in this market.

International revenues, however, are down 7%, after suffering from various complications. These include container shortages affecting US-bound shipments. Hopefully these are all temporary issues, relating to temporary economic woes, and are nothing to worry about in the long-term.

International revenues account for only one quarter of Vimto’s total, so the UK recovery is the really big story here.

Cash and dividends - Nichols has historically been excellent at generating cash, and finishes H1 with £49m on hand. This is after spending £5.5m on repurchasing its own shares during the period, and making a nearly £6m working capital investment.

The share buyback is touted as helping with the company’s Save-As-You-Earn employee option scheme and with the LTIP, so I won’t get excited about the prospect of seeing the share count at Nichols reduce any time soon (the share count at Nichols has been stable for many years, but has not meaningfully reduced).

The interim dividend increases by over a quarter to 12.4p. Divis were reset by Nichols at a lower level during Covid, but there is no doubt that this company is a dividend champion. It has made a payment to shareholders every year for three decades.

Outlook - there are “significant and accelerating inflationary pressures”. Thanks to mitigating actions by the company, adjusted PBT expectations for the full year are unchanged at £25.2m.

CEO John Nichols:

The Board remains mindful of the potential earnings impact of continued inflation into FY23 and beyond. We have a long-term track record of growth, a proven, diversified strategy, and a quality range of brands. All of this is underpinned by a strong balance sheet. As a result, the Board remains confident that the Group is well positioned to deliver its long-term growth plans.

My view

Nichols has usually had very “clean” accounts, and that remains the case today.

The £1.2m difference between the “adjusted” profit and the actual profit relates to the changing of the contract manufacturer for the Dilutes category, for the purpose of increasing capacity and speed:

Significant costs were incurred during H1 in making this change, including additional storage capacity, new systems, restructuring costs and legal fees.

Given the track record of Nichols, and the simple explanation for the above, I’m perfectly happy to use the “adjusted” numbers the company provides.

On that basis, we get adjusted EPS of almost 25p.

There is usually a noticeable H2 weighting for Nichols, and the full-year (adjusted) EPS estimate is 55p.

That looks achievable and I’m wondering if the company might even beat this number? Maybe some very hot weather could help motivate people to drink more Vimto, and boost the soft drinks market in general?

The earnings multiple is around 24x and this reflects the lower risk profile of Nichols - investors know what they are getting, and they like it. It’s hard to imagine that the shares can run much higher from the current level any time soon, but this remains a safer place to park funds than the vast majority of listed companies, in my opinion.

See what our investor community has to say

Enjoying the free article? Unlock access to all subscriber comments and dive deeper into discussions from our experienced community of private investors. Don't miss out on valuable insights. Start your free trial today!

Start your free trialWe require a payment card to verify your account, but you can cancel anytime with a single click and won’t be charged.