Good morning! It's Paul here.

I have to complete this report much earlier than usual today, because I'm heading up to London for a lunchtime meeting with the Directors of Vianet (LON:VNET)

Please note that I finished yesterday's report in the evening, so it now covers: Vianet, FreeAgent, Character, Fulcrum Utility Services, and PCI-PAL. Here is the link to yesterday's completed report.

Bitcoin

Firstly, as it's a quiet day for interesting news, I have to comment on Bitcoin - surely the hottest topic in the financial world at the moment. People ask me if it's a currency, or a speculative bubble? Actually, I think it's both!

Currency? - as a friend pointed out to me recently, literally anything can become a currency if enough people decide to use it as a currency. If enough of us decide to use seashells as a currency, then seashells become a currency!

Bitcoin does seem to be gaining traction as an acceptable currency, although it's still very much on the margins as a niche thing. Also, I think a lot of the press articles about so and so accepting bitcoin, look like publicity stunts.

Why would anyone use Bitcoin? Possibly for experimental reasons, but mainly I think it seems to be a mechanism to by-pass the conventional financial system. Hence it is apparently the currency of choice for criminals, drug dealers, etc, seeking to launder their money. It may be the case that many, even most bitcoin transactions are legitimate. However, just using common sense suggests that a main motivating factor to use bitcoin is to bypass laws & regulations. Apparently it's popular in China as a way of hiving off money overseas, thus avoiding exchange controls.

This to me seems the obvious catalyst for bitcoin's eventual, inevitable collapse - that Governments are likely to ban, or regulate its use. It seems almost ridiculous to expect Governments to sit back and do nothing, whilst their control over the financial system slips away.

Only last week the UK Government announced that it was intending to regulate use of bitcoin. The UK might be insignificant overall to bitcoin, but it can only be a matter of time before big Asian economies like China and Japan also introduce regulation or outright bans on the use of bitcoin. The Chinese shut down a bitcoin exchange earlier this year, causing a sharp (temporary) fall in the price of bitcoin.

Blockchain technology - several technical & financial wizards have explained to me how exciting blockchain technology is. It seems to have potentially extensive uses, in many sectors. It could lead to a new wave of disintermediation, as conventional business models of stock exchanges, banks, etc, may be undermined & even replaced by blockchain-based systems.

That's all great, and it sounds exciting. However, that doesn't mean Bitcoin is worth hundreds of billions. It doesn't mean bitcoin is worth anything actually. Just because it operates through an innovative technology, does not in itself create the vast value which the market is currently attributing to bitcoin.

Store of value? One of the key requirements for something to be considered a currency, is that it must be a means of exchange, and a store of value. Supporters of bitcoin claim that, because it is limited to 21m bitcoins in total that can ever be issued, then it is better than conventional fiat currencies, as it can't be debased. That's a good point, and one of the things that is so clever about bitcoin.

However, this ignores the fundamental flaw that bitcoin is not backed by anything. So it's ultimately worthless. Just because people are currently willing to pass the parcel, at ever increasing valuations (the greater fool theory very much in play) seems to me a temporary aberration - a speculative bubble.

Aren't fiat currencies also backed by nothing? No. Currencies like the dollar, Euro, sterling, etc are all backed by Governments, which have tax-raising powers. Certainly, if Governments or arms of Government (central banks, etc), or bodies regulated by Governments (e.g. commercial banks) debase a currency by issuing too much of it, then they can destroy the trust that is essential to their own currency.

In such circumstances, the population usually switch to transacting in cash, in US dollars - still the world's main reserve currency. That's what happened in Zimbabwe for example - where is own currency was debased so much by the corrupt & incompetent Government of Robert Mugabe, that in the end the country simply abandoned its own currency altogether, and people use US dollars instead. Apparently there has also been interest in bitcoin in Zimbabwe recently.

Why would people prefer bitcoin to US dollars? I don't think it has anything to do with fears of the dollar being debased. That happens slowly, and isn't a problem, as people can buy assets with the dollars. You might be worried about debasement of the dollar if you just intend stuffing dollars under your mattress for 20 or 30 years. Who does that though? Cash deposit interest rates are deliberately set low, to push people into buying other assets with their dollars. So if we have surplus cash, we might buy shares, or a property to let out.

Volatility - bitcoin is simply too volatile to be taken seriously as a currency. A currency that routinely swings in value by 10-20% in a few minutes is obviously unstable, and hence an unreliable store of value.

Of course, during the massive, parabolic run up in value, bulls will scoff at comments such as mine. They won't be quite so euphoric when it collapses in value, at some point in the future - I have no idea when, but as with all speculative bubbles, it will inevitably burst. It never is "different this time", because human nature never changes, and few people learn from history in the financial world - strange, but true. Some peoples urge to speculate overcomes any such lessons from history in the short term, during speculative bubbles.

Speculation - the main reason people are buying bitcoin is to speculate! It's more than 10-bagged this year alone, and the percentage gains from earlier back are absolutely stellar. The South Sea Bubble pales into insignificance, as it was only a 10-bagger before its evential collapse. Bitcoin has been much bigger than that. I see the latest news is that 2 brothers in America who "invested" $11m into Bitcoin are now billionaires. Good for them - but I hope they remember that a paper profit is not a real profit until you sell.

Galbraith - I have recently re-read a marvellous little book by the late renowned economist, Kenneth Galbraith. It's called "A short history of financial euphoria" - highly recommended. Whilst re-reading it, I kept muttering to myself, that's bitcoin!

Some key points that Galbraith makes;

- Free-enterprise economies are given to recurrent episodes of speculation

- He describes these as, "flights into what must conservatively be described as mass insanity". This book is insightful, but also amusing in his utter disdain for the people who participate in speculative bubbles.

- Speculative bubbles start when people, "wonder at the increase in values and wealth", which then causes a, "rush to participate that drives up prices", leading to an eventual crash.

- People who warn about the bubble - Galbraith comments that there are, "few matters on which such a warning is less welcomed ... it will be said to be an attack, motivated by either deficient understanding or uncontrolled envy, on the wonderful process of enrichment". Sounds familiar? That just about sums up the reaction to any less than bullish post on advfn bulletin boards! It also clearly applies to bitcoin.

- Galbraith says that a key feature of a speculative bubble is usually, "Some artifact or some development, seemingly new and desirable..." - yup, bitcoin ticks that box too.

- The price goes up exponentially, due to price rises sucking in more & more buyers.

- Then when the buying frenzy finally exhausts itself, everyone rushes to exit at the same time, causing a crash.

- Some participants genuinely believe in the new thing, and its wondrous properties. Others don't believe in it, but are happy to join the speculative frenzy in order to make money, believing that they can sell at the top. Everyone thinks they can sell at the top, hence why there is eventually an inevitable crash.

- "The eventual and inevitable fall ... cannot come gently or gradually. When it comes, it bears the grim face of disaster".

- "Something, it matters little what ... triggers the ultimate reversal. Those who had been riding the upward wave decide now is the time to get out".

- "The speculative episode always ends not with a whimper, but with a bang".

- There's much more fantastic stuff in Galbraith's little book, but that gives a flavour. Bitcoin literally ticks all the boxes for a speculative bubble. So in my view, it is doomed to eventual failure.

Proliferation - whilst bitcoin itself might be limited to just 21m units, there are numerous other crypto-currencies popping up on a daily basis. This makes sense. After all, people observe how bitcoin has wondrously created hundreds of billions of dollars wealth, out of thin air. Unsurprisingly, copycat variants, with new & and improved features, such as Ethereum have popped up. I note that even the Venezuelan Government has decided to launch its own crypto-currency, to get round American impediments to its economy.

Again, this is all classic behaviour one would expect in a speculative bubble. Remember the dot.com boom, when there was a rush to IPO all sorts of worthless junk. Gullible punters lapped up these issues, and they usually went to substantial premiums on listing. Investors were selling good assets, to fund purchases or speculative junk. Like all bubbles, eventually the buyers dried up, and prices crashed. First there was the 90% (fall in share price) club. A year or so later, that had become the 99% club. The bear market lasted from 2000 to 2003, and a huge amount of wealth vanished.

Conclusion - bitcoin, and other crypto-currencies are a fascinating thing to watch, but it's a very obvious speculative bubble, that is destined to ultimately burst.

Image Scan Holdings (LON:IGE)

Share price: 8.0p (down 14.7% today)

No. shares: 136.0m

Market cap: £10.9m

(at the time of writing, I hold a long position in this share)

Preliminary results - results issued at 08:11 - incredibly annoying! Please always issue future results at 07:00 like (almost) everyone else, so that we can read the figures before trading starts at 08:00.

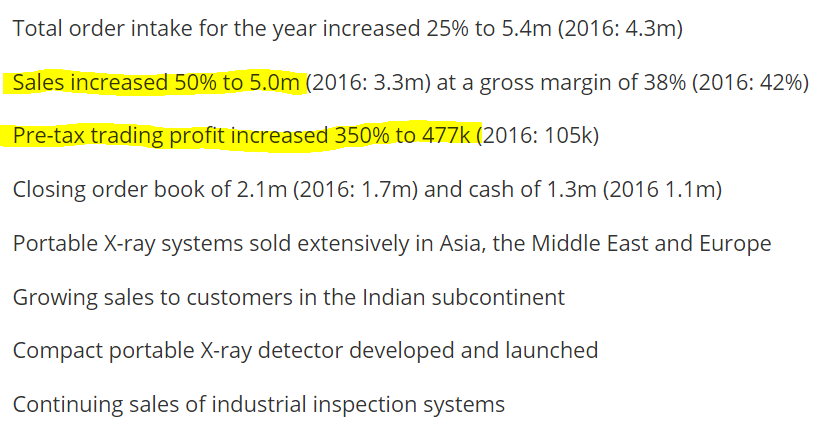

Image Scan (AIM: IGE), the specialist supplier of X-ray screening systems to the security and industrial inspection markets, today announces preliminary results for the year ended 30 September 2017.

There have been a series of positive trading updates from this little company in recent months, so the decently improved results today were expected.

The company is small, but had a much improved performance;

Outlook - this is the most important part. The question investors are asking, is whether this was a one-off good year, or whether this is the start of something bigger?

The Company starts 2018 with a robust order book, although we need to finalise the extended delivery dates on a proportion of those orders. The Company has an encouraging sales pipeline and a product range that allows a wide range of customers and markets to be addressed. Further portable X-ray product launches are planned during the year and these should allow the company to continue to extend its customer base.

The security equipment market continues to be very active, reflecting the continuing high level of the terrorist threat, as portable X-ray systems are important tools for early detection/identification of a threat and often one of the first security technologies to be deployed after a threat is detected. We expect continuing healthy demand for these products.

Note the more cautious tone about phasing of deliveries - I think this has caused the wobble in share price today.

Placing - an interesting situation developed recently. A large shareholder wanted to sell some shares, but as with most small caps, the market was too illiquid to take them. So the shares were placed through a broker, I think it was Cantors. I took some stock in the placing, at 8p, to add to my existing position. This price was well below the market price at the time (which had been around 12p at the time the deal was initiated).

Now clearly, person or persons unknown must have taken some stock to flip it for an instant profit. That's very annoying. So the open market share price has been dragged down to the 8p placing price, at which level flippers stop selling, because there's no profit to be had.

This highlights the big problem we have with liquidity in micro caps. The market price is set by small trades between private investors. However, that may be very different from the price that big buyers are prepared to pay, if there are any big buyers at all, which clearly there are not in this case - the market cap is too small for most Instis, even if they do like the company.

We saw a similar mismatch between market price, and the company's value, with EG Solutions, which was sold to a trade buyer & delisted, but at a price which was about 10% below the share price at the time.

I suggest that any similar holders of illiquid stocks engage the services of Primary Bid, if they want to liquidate a block of shares. That seems a much more natural market to fragment an institutional holding, by dispersing it to private investors who are bidding up the price in the open market. So far, the quality of companies using Primary Bid has been lamentable. However, it's a good concept, and I would like to see it succeed, as it increases the options available to companies and investors. So hopefully in future, Instis who want to liquidate illiquid positions might use Primary Bid instead, rather than selling to flippers through a conventional broker.

My opinion - new management at IGE seem to have improved the company considerably. I like that there is growing demand for its security products. It all hinges now on whether management can continue growing the company & profits. As a speculative growth company, I quite like it - at least it's profitable.

There's a brilliant video here of the Chairman giving a presentation at Mello, in Sep 2017. Many thanks to PIWorld for producing this video to help investors get a better understanding of this company.

easyHotel (LON:EZH)

Final results - for y/e 30 Sep 2017, for this small group of hotels.

These results look rather poor to me. I cannot fathom why this company is valued at £120m, at the current 120.5p per share - that looks far too high.

Net assets are £70.2m. However, given that the assets only generate a poor return, then if anything those assets look over-valued to me.

Based on these results, I'd struggle to get to a valuation of even half the current share price.

Adjusted EBITDA was £2.3m, but there's an £831k depreciation charge to take into account, so that reduces pre-exceptional profit to only £1.47m.

Overall then, unless I've missed something, the valuation looks far too high, so I wouldn't touch this one at the current price. To my mind, little value is added by adding the word "easy", and painting everything orange.

The company says it may raise fresh equity & loans to fund further expansion.

Plastics Capital (LON:PLA)

Unimpressive interim results today.

Profit is down, and the interim divi is suspended.

Talk of H2 being stronger, but full year expectations now "marginally below" market consensus.

I don't rate this group. There seems little point to it owning a collection of plastics businesses. The central overheads don't add any value, arguably they destroy value with unnecessary costs, mainly group Director salaries.

Redhall (LON:RHL)

Results for y/e 30 Sep 2017 look OK, showing some improvement in profits - £1.43m profit vs £856k last year.

The company has restructured, so debt interest costs should reduce in future.

Has a pension scheme.

Doesn't interest me, I dislike small contracting businesses like this, as something expensive usually goes wrong.

Numis (LON:NUM)

Impressive results for y/e 30 Sep 2017 out today.

I note the big profit margin, and EPS up 17% to 27.4p. Divis flat at 12p for the year.

Smashing balance sheet, with £127.5m net current assets, of which £95.9m is cash.

Has a good repuation, and their research notes are usually good, in my view.

This type of broking business is very cyclical, but the outlook comments sound positive.

My choice in this sector, on valuation & dividend grounds, is Cenkos Securities (LON:CNKS) (where I hold a long position).

Maintel Holdings (LON:MAI)

Profit warning - shares down 13%.

The Group had expected to recover the reduction in gross margin in the first half of this financial year, but it is now evident that this will not happen for the following reasons...

An upbeat outlook section is probably what has limited the share price fall today, to considerably less than the usual 30% that a profit warning triggers. Well done to the company for quantifying revised guidance. I think that also helps limit share price falls, as investors are properly informed, rather than having to guess;

The Board now expects adjusted EBITDA for the year ended 31 December 2017 will be in the range of 12.5m to 13m.

Reflecting our confidence in underlying cash flows and the longer-term prospects for the Group, we remain committed to our progressive dividend policy. It is our current intention for the total full year 2017 dividend to grow 10% year on year, in line with existing guidance.

We will provide more detail on expectations for 2018 at the time of the preliminary results announcement in March, however, at this juncture, the Board remains confident in delivering substantial growth in revenue and EBITDA in the full year to 31 December 2018. Growth will be driven by improvements in trading conditions, a recovery in Avaya installations, continued growth in the ICON cloud business and additional cost cutting and synergy realisation across the business. The Board expect this recovery to accelerate into the first half of calendar year 2018.

My opinion - I'm avoiding any businesses that do telecoms or cloud services. There was a very interesting note recently from Kevin Ashton, the renowned tech analyst, currently at Cantors. He points out that Amazon is aggressively reducing prices for its cloud services. This is putting the cat amongst the pigeons with smaller competitors, squeezing their margins.

I'm not keen to invest in anything which is in Amazon's cross- hairs, as it has a track record of destroying margins for the incumbent competition.

Sorry that was such a mad rush, and please add your comments below. I will respond to comments this evening, after the meeting with Vianet (LON:VNET) .

Regards, Paul.

See what our investor community has to say

Enjoying the free article? Unlock access to all subscriber comments and dive deeper into discussions from our experienced community of private investors. Don't miss out on valuable insights. Start your free trial today!

Start your free trialWe require a payment card to verify your account, but you can cancel anytime with a single click and won’t be charged.