Good morning from Paul & Graham! We're having a catch up day today, so Graham's done shorter comments, and I'm carrying on probably to mid-afternoon, so watch this space! Also we're seeing some interesting reader comments, so do check that section below too, and thanks to everyone contributing. Today's report is now finished.

Agenda -

Paul's Section:

Churchill China (LON:CHH) - I have a good rummage through yesterday's interim results to 6/2022. The figures are good, and a decent outlook, with record order book. However, its end customers are under severe strain right now, so I am worried that order books could be heading for a fall. For that reason, it's difficult to justify the current valuation.

Joules (LON:JOUL) [no section below] - is going from bad to worse, with news yesterday that negotiations with Next (LON:NXT) for an equity stake to rescue it, have fallen through. It confirms the obvious, that it now needs to do an equity fundraising. I’m speechless at how badly handled this has all been.

The c.£12m market cap might be tempting for a punt, but we don’t know what the terms of the now inevitable refinancing will be. The bank has been very helpful so far, but the clock is ticking due to its Nov 2022 deadline. Dilution could be huge, given that the market cap is now so low, and the bank might require a substantial equity raise, and who would want to rescue it now? For that reason, I wouldn’t want to gamble on the outcome, and I’ll wait for a proper refinancing to be done, and a hopefully credible turnaround plan. The twin risks are of heavy dilution (which now looks almost inevitable), or an even bigger risk that it might end up being put into administration, and a pre-pack being done, wiping out existing shareholders altogether. Those grubby deals get done in private, often with no warning. Sorry again that this one has been such a disaster, it’s just been so badly run, by incompetent management. [no section below].

Best Of The Best (LON:BOTB) - an in line trading update today. Also I comment on the latest large management share selling, to strategic investor Tedi Sagi. This can be viewed two ways - disappointment at yet another big Director selling at just 400p, or excitement at a new investor bringing expertise and an international expansion strategy.

Naked Wines (LON:WINE) - plummets 33% today, due to a bearish-sounding update last night, and a recently appointed NED leaving immediately. I ponder whether WINE has become a value share yet, now that the sexy growth story looks to have unravelled. The short version is, probably not value, and I'm worried about the bloated inventories, and negative cashflow effect of the business shrinking - as seems likely now. Going concern was a "material uncertainty" with last accounts, but mgt said it has levers to pull - let's hope they are heavily leaning on those levers as we speak, as they need to be. It's now about survival, rather than growth, not a good basis for investing, in my experience.

Blackbird (LON:BIRD) - a reader request for me to look at its interim results today. Revenues tiny, at £1.5m in H1 but good growth of +78% vs H1 LY, but up less +29% vs H2 LY. EBITDA loss little changed vs H1 LY, at £637k, but favourable moves in LTIP costs have reduced the loss before tax. Underlying loss looks to be almost flat vs H1 LY, so nothing to get excited about there, in terms of underlying performance. Plenty of cash at £11.6m (and no debt), so cash not a worry, with years’ cash burn in the bank. Market cap of c.£70m is based entirely on future hope. So there’s nothing to support the price on fundamentals at present. Good luck with it!

Anpario (LON:ANP) - interim results show a big hit to gross margin, and little sales growth, but profits mostly maintained through admin cost cutting. Superb balance sheet. Wobbly outlook comments, may struggle to meet (let lone beat) 2021 results. It's looking increasingly difficult to understand why Anpario is still on a premium rating, despite the sluggish growth.

Trackwise Designs (LON:TWD) [no section below] - this has collapsed in stages, down to only 11.4p (£4m market cap). Thankfully, Graham talked me out of considering a small, speculative position in it here at end July 2022. The company needs cash, and today’s news says that the hoped-for asset backed lending has fallen through, because production orders from the main customer has been reduced. It’s negotiating with the main customer to amend its contract to provide up-front cash. TWD is also “reviewing a number of options for additional funding”. With the market cap already down to just £4m, it might be easier for someone to just buy the whole company, or let it go into administration, and buy the assets quickly & cheaply. Existing equity might well be in the last chance saloon now. What a pity, as the products sound very interesting indeed. I remain on the sidelines, watching. Big dilution/insolvency risks now look very high, I’m sorry to say. [no section below]

Ricardo (LON:RCDO) - 439p (£271m mkt cap) [no section below] I remember a reader suggested this engineering consultancy group as a possible takeover candidate, when we were trying to guess what might be the next RPS (LON:RPS) (which received a big premium bid from Canada). I’ve just looked at RCDO results for FY 6/2022, and like what I see. In line with exps. Nice recovery from LY. EPS (continuing) was 28.5p, rising (forecast) to 33.2p this year (per Liberum). Bank debt now modest, and £150m+£50m facility agreed until July 2026, so has scope for acquisitions. Net debt £35.4m. 10.4p divi. Software business sold post year end for $17.5m + £3.0m possible earn out. The share price has bounced a lot from recent lows. PER still only 13.2 (on FY 6/2023 forecast). Still looks good value, and a bidder could afford to pay a lot more, if they value it like RPS. Interesting!

Graham's Section:

B.P. Marsh & Partners (LON:BPM) (£113m) (+3% yesterday) [no section below] - this is an investor in financial insurance businesses (mostly insurance intermediaries) with a good track record of growth in NAV per share over time. NAV has grown from 273p per share in Jan 2017 to 463p per share in Jan 2022. It has paid a small dividend every year since 2012, but the main attraction is the growth in capital value, and the share price (302p currently) tends to trade at a big discount to this value. Yesterday’s trading update also confirmed that the company aims “at least to maintain” the current dividend payout for the next two years - the forecast yield is 0.9%, according to the StockReport.

More importantly, “the majority of BP Marsh’s portfolio companies have performed well in the period”. Two of its major investments continue to grow strongly and looking forward, BP Marsh is confident that “it will continue with its historic growth trajectory”. Insurance rates are increasing such that increased costs “will at least be matched by an increase in premium rates”, i.e. inflation is being passed on. I’ve owned shares in this before and would consider owning a small stake in it again, trusting in the expertise and discipline of the management team.

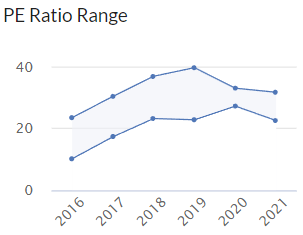

Bioventix (LON:BVXP) (£177m) (+8%) [no section below] - this famously successful biotech issues a strong trading update for FY June 2022. After a slow start to the financial year, “we have seen an improvement in performance and our trading result for FY2022 as a whole is likely to be significantly ahead of market expectations”. The company attributes this to post-Covid recovery (general diagnostic activity in hospitals and clinics reduced as a result of Covid measures). There is also a bounce related to the strong dollar/weak pound, as Bioventix earns 50% of revenues in US dollars but its results are reported in pounds.

At around 26x after this morning’s bounce, the Bioventix PE Ratio is still at the cheaper end of where it usually trades. This is a famously high-quality business earning revenues of c. £650,000 per employee (!). On the assumption that its intellectual property is just as valuable now as it was pre-Covid, this pricing could be seen as a buying opportunity for a stock that is almost never on sale.

Focusrite (LON:TUNE) (£438m) (-7%) [no section below] - this musical equipment supplier issues a profit warning: while revenues for FY August 2022 are in line with expectations at £180m, rising costs are hurting margins. These costs relate to the familiar issues with semiconductors and freight, and have so far only been partially offset by price increases. Administrative costs are also rising and as a result, EBITDA will be “slightly” below expectations.

Additionally, the company references the importance of cash generation: it has used up its cash balance on acquisitions and on rebuilding its inventory (another consequence of supply chain uncertainties is that companies need to tie up more cash in their inventories, to ensure that customer orders can be fulfilled). While Focus has an excellent long-term track record, the lack of growth and the loss of its cash balance - which reduces its flexibility when dealing with current challenges - suggests to me that the market is correct to treat it cautiously for the time being. It’s categorised by Stockopedia as a “Falling Star” and I agree that its multiples should continue deflating until it demonstrates better resilience in these economic conditions.

Hornby (LON:HRN) (£48m) (+2%) [no section below] - an in-line trading update from this model railways company. Sales and margins are unchanged from last year, and the company is gearing up already for the key Christmas season. Shipping dates have been brought forward in a sensible measure to prevent a repeat of the supply chain problems. As for the outlook, the company suggests that the hobby sector can tough out bad economic conditions: “We are mindful of the impact the current economic climate may have on demand, but remain encouraged by the historic performance of the hobby industry in prior downturns and our expectations for the full year are unchanged.”

Separately to the trading statement, the company carries out a cleaning-up exercise; the independent directors had failed to express their “fair and reasonable” view in relation to some related party transactions with the Chairman, as required by AIM rules. They do so today.

For my detailed view on Hornby, see the SCVR of 16 June 2022. Today’s update lets us know that management remain confident in their plan, despite the various economic distractions and challenges of the past three months. I remain interested in the story of operating leverage possibly giving Hornby profits a big boost in the years ahead, although it could be argued that the market cap is already pricing this in.

Explanatory notes -

A quick reminder that we don’t recommend any stocks. We aim to review trading updates & results of the day and offer our opinions on them as possible candidates for further research if they interest you. Our opinions will sometimes turn out to be right, and sometimes wrong, because it's anybody's guess what direction market sentiment will take & nobody can predict the future with certainty. We are analysing the company fundamentals, not trying to predict market sentiment.

We stick to companies that have issued news on the day, with market caps up to about £700m. We avoid the smallest, and most speculative companies, and also avoid a few specialist sectors (e.g. natural resources, pharma/biotech).

A key assumption is that readers DYOR (do your own research), and make your own investment decisions. Reader comments are welcomed - please be civil, rational, and include the company name/ticker, otherwise people won't necessarily know what company you are referring to.

Paul’s Section:

Churchill China (LON:CHH)

1220p (up 4% yesterday)

Market cap £134m

These are good numbers, showing a nice recovery from the prior year H1, which would have been impacted by the pandemic.

Also, note from this handy table on Stocko, that pre-pandemic CHH had a consistent H2 bias to revenue & profits, so the good H1 numbers this time augurs well for FY 12/2022.

Here are my notes from running through the interims announcement -

H1 revenue up 73% to £41.4m, as it bounces back from the pandemic (don’t expect this rate of growth to continue though).

UK & Europe are the 2 main markets, at 39% and 42% of revenues. US & RoW are small, an opportunity for growth perhaps?

Profits (before tax) £3.4m in H1, up strongly from £1.0m LY (last year).

Adj EPS 24.7p (up from 4.5p LY)

Given the H2 seasonal bias to profits, the consensus forecast of 60.3p shown on the StockReport looks achievable or beatable - so lowish risk of a profit warning this year I’d guess. As for 2023 though? It's too early to say, although I'd be worried that a further rise to forecast 75p EPS in 2023 might be a struggle, if the current macro headwinds continue or worsen. So ideally I'd like to see forecasts quietly lowered for 2023, to prevent a profit warning.

No broker notes available, because the broker is Investec, who stop us getting access to research. EDIT: research notes from Singers have since come up on Research Tree, thanks for that (they weren't there earlier today when I checked, but I might have put in the wrong ticker)! End of edit. Time to change broker to a PI-friendly outfit, such as Finncap, Singers, Liberum, WH Ireland, or any other that publishes research on Research Tree? It beats me why any small cap would use a big broker, that has no interest in the main buyers of the shares - PIs. It's not just haughtiness though - due to MiFiD, brokers have to charge for research, so are then not keen to give it away to PIs, as that would undermine their source of income from institutional buyers of research. Time to scrap MiFiD?

Webinar - there doesn’t seem to be anything arranged for PIs. I’ve just nagged the PR, to ask if they would facilitate results webinars in future, because I know a lot of us find them invaluable, to increase our understanding of companies, and get a flavour of the people running them. So let’s hope the company takes up this suggestion. All companies should be doing results webinars for PIs these days, it should just be standard practice.

Balance sheet - remains very strong. There's been no dilution over the pandemic period, as the finances are more than strong enough to get through difficult patches.

Note that receivables has risen a lot, which I would expect, as business recovers from the pandemic. So that’s not a concern, although of course it has consumed cash.

I’d like to know what “other financial assets” are - there’s no explanation for this line. This has risen materially, from £1.0m a year ago, to £4.0m at Dec 2021, to £5.0m now. Although checking the last prelims, it refers to “net purchases” of other financial assets, so I’m wondering if this is cash on deposit, or hedging instruments? More detail should be provided, given the size of this line on the balance sheet.

Curiosity got the better of me, and note 16 to the 2021 Annual Report explains that these are term deposits (i.e. cash placed on deposit to get a higher interest rate), with Santander and Lloyds Bank. So this line should be seen as equivalent to cash, making the balance sheet even stronger.

I’ve gone a bit round the houses there, because the financial highlights disclosed “Net cash and deposits” of £15.7m, which we can quickly see is the combination of £10,650k cash, and £5,016k of “other financial assets”. Mystery solved!

Pension deficit is dropping, and is now £6.4m. There’s no information on what the deficit recovery payments are, if anything, so this would need more research - the answer is probably in the archive here, for previous SCVRs reporting on full year results.

Cash generation - wasn’t good, with cash reducing. This is due to working capital normalising, capex, and divis paid out, which combined exceeded cash generation. I don’t see that as a problem though, because cashflow should improve in H2.

Capex - the commentary today indicates more expenditure on automation & energy efficiency, but not quantified, but I anticipate a fair bit of cashflow is likely to be directed into continued capex, but not a worry if the payback on investment is decent.

Inflation - selling prices have been raised twice, but no figures have been provided - I would have liked a bit more detail on this, e.g. selling prices have been raised x%, in response to input costs rising y%. The commentary says price rises have “help offset” - which sounds ambiguous - does that mean fully offset, or only partially offset? Ah, I see it’s the latter, with the phrase “mitigate in part” later used. The price rises have been accepted by the market, and are similar to those introduced by competitors, it says, which reassures me.

Energy - clearly a big issue for this sector, given the need for expensive ovens to bake the clay, and other energy usage in factories.

Re energy price hedging, this looks good at hopefully cushioning CHH from the energy crisis for about the next year from now -

Our energy hedging position is relatively robust. We largely secured our volumes and pricing earlier in the year for a substantial proportion of our anticipated usage for the remainder of 2022 and the first nine months of 2023. We are mindful of the extended impact of volatile energy pricing and will continue to monitor market movements carefully.

Outlook comments are a bit vague, and no clear guidance is given, other than this -

We are aware of increasing levels of uncertainty in the general business and economic landscape and the possible effect of this on demand for our products, although we continue to benefit from good order levels after the period end. We are, however, mindful of the potential effects of an economic slowdown on our revenue and will manage our business accordingly. Input costs, in particular energy, remain volatile. Our energy costs are largely hedged well into 2023 and we will continue to monitor our exposure in this area. The business' principal focus over the next few months will be to develop our manufacturing operations to support increased output and efficiency levels both in the short and longer term. We will continue to invest in our people and our productive capacity.

We remain confident that Churchill is a resilient company and is well positioned to continue to grow in line with our established strategy over both the short and long term. We look forward to delivering an improved year on year performance in 2022.

Given that H1 is way ahead of H1 LY, then saying FY 12/2022 will be ahead of LY, is setting the boundaries pretty wide!

Note that in another part of the commentary, it refers to a record current order book.

So it looks as if the outlook should be pretty decent, although bear in mind the hospitality sector is having a seriously hard time right now, due in particular to energy costs, and consumers reining in spending in some areas.

My opinion - I’m impressed with these numbers, and have always liked this share, due to its decent products, widely used in the hospitality sector (e.g. my recent mystery shopping of J D Wetherspoon (LON:JDW) saw a curry served on a lovely blue patterned Churchill China plate), and excellent balance sheet. Although valuation is usually a stumbling block, in that CHH shares seem to usually command a premium that has tended to strike me as at least partly unjustified. Photographic evidence -

(above: "clean plate kid", as Mum used to say! I licked the plate clean for the last shot. As it was Wetherspoons, nobody batted an eyelid LOL!)

Given that CHH might do say 60-70p EPS this year, can a share price of 1220p really be justified? Especially when we know that CHH’s end markets are under severe pressure, and many independent hospitality outlets are likely to go under - due to severe cost pressures, and nervous consumer discretionary spending.

Although recent Govt support, said to be c.£40bn to help businesses for 6 months with an energy price cap, should help - but we haven’t yet heard the detail.

Taking everything into account, whilst the drop in share price for CHH shares make it more attractive, I really don’t see it as good value, given the intense strain that its end customers are now under - just look at share prices for restaurants & pubs to see what I mean.

On the upside, CHH is viewed by the market as a high quality company, so longer term, the current share price might be attractive, who knows?

.

Best Of The Best (LON:BOTB) (I hold)

440p

Market cap £37m

Best of the Best plc runs competitions online to win cars and other prizes.

The Board is pleased also to confirm that the Company is trading in line with market expectations for the current financial year. Further to the announcements made last week regarding the signing of a Letter of Intent with Globe Invest Limited and their subsequent strategic investment, we look forward to updating shareholders with more details in due course.

The last broker note I can find, is from June 2022, which indicated 53.9 EPS for this year, FY 4/2023. So today’s confirmation of in line trading, suggests the PER is only 8.2 - cheap apparently, especially given the consistently good cashflows at BOTB which have resulted in generous divis, special divis, and tender offers in recent years. Although as we've seen, profitability can be volatile at BOTB, with high online marketing costs being a headwind.

Obviously the elephant in the room, is why have founder management been so keen to sell up? I can see why they took advantage of the pandemic boost to profits, to bank £60m at £24 per share in April 2021. The only surprise is that the institutions which bought those shares haven't sued, given that the share price started collapsing within weeks, as a wave of bad news began.

Management sold more in the recent 600p tender offer, then here on 8 Sept 2022 came news of founder management selling the bulk of their remaining shareholdings to the famous Tedi Sagi, who is acquiring a 29.9% stake from the founders (no new shares being issued), at just 400p. The existing management will continue running the business (for now).

My opinion - I’ve got mixed feelings about this. Bringing in a strategic investor could pave the way for a full takeover later? Existing management seem to have lost interest, and seem likely to move on, I reckon. So would I, with £60m+ in the bank!

So why should we pay over 400p for the shares now? Well maybe because the new major shareholder could bring expertise, contacts, and ideas into the business which existing management lack? The update on 8 Sept talks about plans to take the business international, which existing management seemed to baulk at previously.

Ultimately though, the people who know the business best, have now sold down most of their holdings, which tells me that they don’t see a great future.

It’s tempting to imagine that the new investor, and expertise, could turbocharge future growth. Previous management were often criticised for being too cautious, and not taking any risks, instead prioritising cashflow. That could be about to change.

There’s no doubt that events over the last three years have left a very sour taste.

However, there’s now a clear catalyst for accelerated growth, and potentially exciting international growth. I imagine we’re likely to see a change of management fairly soon, which might be for the best.

Personally, I only hold a tiny scrap of this share, as I want to keep a foot in the door. Could it be a potential future multibagger (again)? Under new management, new investors, and new ideas, it’s possible, but we’ll have to wait and see.

.

Naked Wines (LON:WINE)

97p (down 33% today)

Market cap £72m

Two announcements came out after the market closed last night, which I’ve only just spotted because the share price is a top faller today.

NED resigns - Pravin Ravi has resigned. He only joined the board on 25 August 2022, less than 1 month ago. He was a non-independent NED, being a representative of 10% shareholder, Punch Card Management.

We could speculate on the reason given for his rapid resignation, but no scenario I can think of would be positive. There’s no reason given in yesterday’s RNS.

Business Update - again, announced last night after the market had closed.

Unfortunately, this is rather vague, but it doesn’t sound as if things are going well, does it? -

The Group intends to provide a Trading update on the week commencing 17th October for the first half of FY23, which ends on September 26th.

The company is reviewing potential operational and financial plans for the next 18 months and will update on these plans alongside our trading update. The Group's focus is on developing plans demonstrating increased profitability, cost restraint and improved payback.

Alongside this process we are in active discussions to address our credit facility to reflect any revised plan. The Group remains in compliance with all obligations around this facility through Q1 and expects to have headroom to the Q2 covenant tests.

Reading between the lines, this sounds as if WINE has given up the idea of being a sexy growth story, and is now concentrating more on survival.

Clearly the market saw this coming, hence the share price collapsing -

.

.

In these situations, I focus on 3 things -

- Solvency - is there risk of it going bust (or having to cause major dilution with a rescue refinancing)?

- Is it now a value share - i.e. valuing it conventionally, on assets & likely future earnings?

- Could it be a convincing turnaround?

Looking at those in turn -

Solvency - the last balance sheet looked OK in total - with NAV of £110m. Writing off intangibles of £33.5m gives a still healthy NTAV of £76.5m.

The trouble is though, that inventories look way too high, at £142m, remember that’s at cost price too. If as seems likely, the business is now set to shrink in revenues, then its existing inventories would have to reduce very considerably - maybe by at least half? And that could require loss provisions to be made against some of those inventories.

Also, the £40m cash pile belongs to its customers - the equivalent liability to “Angels” who have paid money up-front, is much larger, at £76m. The trouble with that, is that as the business shrinks, then so does the benefit of customer cash reducing, thus it might even consume cash, rather than generate it, if the business shrinks.

Note that a $60m credit facility was only recently put in place, but there is already a risk re covenants.

Note from the going concern statement with the last accounts, it highlighted that a covenant waiver might be needed in Q1, Q2, and Q4. It seems that Q1 & Q2 were OK in the end, but what about Q4? Going concern concluded with saying there was a “material uncertainty” - never a good look. However, the company countered with saying it has “levers” to pull which could provide £30m extra cash headroom - e.g. cost cutting, disposing of wine on the wholesale market (which worries me about provisions being possibly necessary).

Value - is it a value share yet? No, not really. The market cap is £72m, slightly below NTAV, but the trouble is, that NTAV could shrink, both from trading losses, and inventory write-offs.

We can’t value it on a PER, because WINE has never made any significant real profits. It invented its own measures, such as “Contribution profit”, and “Standstill EBIT”. I’ve always been highly sceptical of these measures, as you’ll see from our archive.

Turnaround potential - much to early to say. Yesterday’s update seems to be focusing on the need to hunker down and survive, rather than being confident about the future.

My opinion - I’ve never rated this share, because it seemed more hype than substance. And it never made any real, meaningful profits. The story was that repeat customers are highly profitable. Those supposed profits were then funding expansion. Now that expansion is no longer the story, then overheads will need to be slashed. Will that end up creating a smaller, but highly profitable business? I’m very doubtful, but we’ll see.

Overall, this looks a salvageable situation, because it’s still got decent net cash. The key point to survive, is turning those bloated inventories into cash. If that can be done without too much of a hit to profits, then equity holders could be OK.

Unwinding the cash owned by Angels, would however see cash outflows.

Overall, it looks quite finely balanced to me, hence I wouldn’t be interested in getting involved. The most likely outcome, is a continued grinding down in share price, but that depends on future newsflow. It’s difficult to see much of a catalyst for a reversal in the downward trend. Would it be attractive to a bidder? Probably not, but that’s always difficult to anticipate. Is there anything unique about Naked Wines? Not really, I see little difference between it, and the other subscription wine services, such as Virgin Wines UK (LON:VINO) and the unlisted competitors. Margins are quite low, and the product handling & storing costs are significant, and customers shop around for the best deals.

.

Anpario (LON:ANP)

500p (down 12% today, at 12:45)

Market cap £120m

This niche animal feeds business has shed £16m of yesterday’s market cap, on release of interim results. Here are my notes from reviewing the H1 figures -

H1 revenues only up 3% to £16.5m - emphasising how small and niche this company is, which is selling globally in a huge overall market. It doesn't seem to have convinced many farmers of the benefits of its products.

Gross margin sharply reduced to 42% (from 50% H1 LY), reducing gross profit from £8.05m to £6.9m. Reason - cost increases, and time lag from raising prices. Margin now improving in H2.

Energy costs - very little gas used. Solar panels have reduced electricity consumption by 32%, so sounds fine.

Admin costs down sharply, from £5.4m to £4.6m, which has absorbed most of the reduction in gross profit, preserving profitability mostly.

Operating profit £2.3m vs £2.65m last H1.

Low tax charge this time has artificially boosted EPS vs last year, so be careful with EPS & PER calculations.

Balance sheet - is amazingly strong. Includes £13.3m of net cash. Current assets: £31.2m, current liabilities £4.0m - that seems excessive working capital to me - a nice problem to have.

Cashflow - poor this time, but for acceptable reasons - building inventories, to ensure the co has product availability.

Outlook - a bit wobbly. Says full year may not meet LY. Talks about international expansion, and more acquisitions.

My opinion - this is a decent little company, with a good track record, and a strong net profit margin. However, the growth has been quite pedestrian over the years, and it must only be scratching the surface of potential markets globally. So why isn’t growth more exciting? Are management ambitious enough, or happy to just keep growing modestly, and hoard cash? Talk of further acquisitions suggests to me that growth potential for existing products is probably limited.

In tough, bearish small caps markets, the risk here is that increasingly investors might question why a company with apparently little growth potential, is still on a premium rating?

I think we need to see something more exciting happen here - namely a more ambitious plan to aggressively grow organically.

.

See what our investor community has to say

Enjoying the free article? Unlock access to all subscriber comments and dive deeper into discussions from our experienced community of private investors. Don't miss out on valuable insights. Start your free trial today!

Start your free trialWe require a payment card to verify your account, but you can cancel anytime with a single click and won’t be charged.