Good morning from Paul, Graham & Roland. We have a full house today! (as I [Paul] have to finish early, to swap AirBnBs here in Malta). It's working remotely, rather than a holiday - you need a change of scene every now and then, after working from home for the last 22 years!

Explanatory notes -

A quick reminder that we don’t recommend any shares. We aim to review trading updates & results of the day and offer our opinions on them as possible candidates for further research if they interest you. Our opinions will sometimes turn out to be right, and sometimes wrong, because it's anybody's guess what direction market sentiment will take & nobody can predict the future with certainty. We are analysing the company fundamentals, not trying to predict market sentiment.

We stick to companies that have issued news on the day, with market caps (usually) between £10m and £1bn. We usually avoid the smallest, and most speculative companies, and also avoid a few specialist sectors (e.g. natural resources, pharma/biotech, investment cos). Although if something is newsworthy and interesting, we'll try to comment on it. Please bear in mind the "list of companies reporting" is precisely that - it's not a to do list. We typically cover c.5 companies per day, with a particular emphasis on under/over expectations updates, and we follow the "most viewed" list of readers, so if you're collectively interested in a company, we'll try to cover it. Obviously with the resources available, we can't cover everything! Add you own comments if you see something interesting, and feel free to discuss anything shares-related in the comments.

A key assumption is that readers DYOR (do your own research), and make your own investment decisions. Reader comments are welcomed - please be civil, rational, and include the company name/ticker, otherwise people won't necessarily know what company you are referring to, if they are using unthreaded viewing of comments.

What does our colour-coding mean? Will it guarantee instant, easy riches? Sadly not! Share prices move up or down for many reasons, and can often detach from the company fundamentals. So we're not making any predictions about what share prices will do.

Green (thumbs up) - means in our opinion, a company is well-financed (so low risk of dilution/insolvency), is trading well, and has a reasonably good outlook, with the shares reasonably priced. And/or it's such deep value that we see a good chance of a turnaround, and think that the share price might have overshot on the downside.

Amber - means we don't have a strong view either way, and can see some positives, and some negatives. Often companies like this are good, but expensive.

Red (thumbs down) - means we see significant, or serious problems, so anyone looking at the share needs to be aware of the high risk. Sometimes risky shares can produce high returns, if they survive/recover. So again, we're not saying the share price will necessarily under-perform, we're just flagging the high risk.

Others: PINK = takeover approach, BLACK = profit warning, GREY = possible de-listing.

Links:

Paul & Graham's 2024 share ideas - live price-tracking spreadsheet (2 separate tabs at bottom), Video update of results so far, June 2024.

** New SCVR summary spreadsheet for calendar 2024 ** This is the live one! (updated 6/9/2024)

Archive - SCVR summary spreadsheet for calendar 2023.

Paul's podcasts (weekly summary of SCVRs & macro views) - or search on any podcast provider for "Paul Scott small caps" - eg Apple, Spotify.

Phil Hanson's data analysis measuring performance of our colour-coding system in the SCVRs, from July 2023- Mar 2024 (with live prices). My video explaining/reviewing it.

My other video (June 2024) - How to screen for broker upgrades on Stockopedia. More stock screening strategies here (possible bargains?) - 21/9/2024.

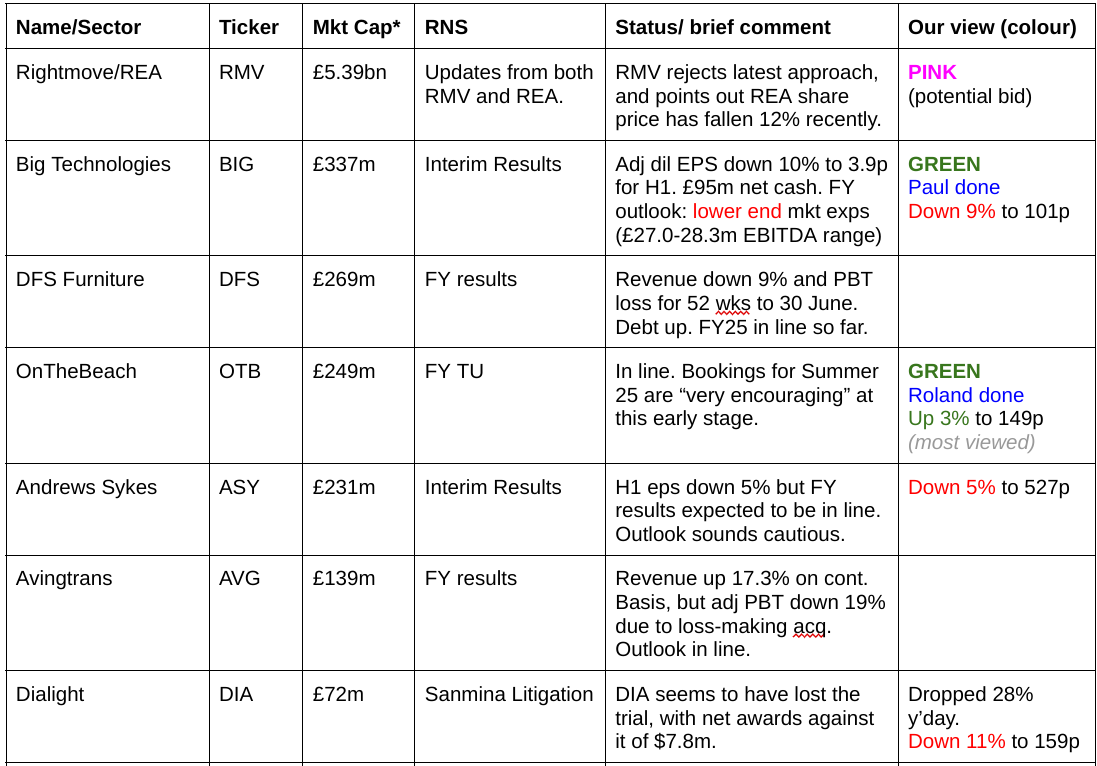

Companies Reporting

Summaries

On Beach group (LON:OTB) - up 3.3% at 149p (£249m) - Pre-close trading update - Roland - GREEN

This online travel agent appears to have had a strong finish to the year, with adjusted PBT up by 31% and an improved year-end net cash position. The pipeline of forward bookings appears positive, albeit it’s still early in the year. OTB shares look decent value to me, given the improved profitability implied by today’s trading update. I remain positive ahead of December’s FY results.

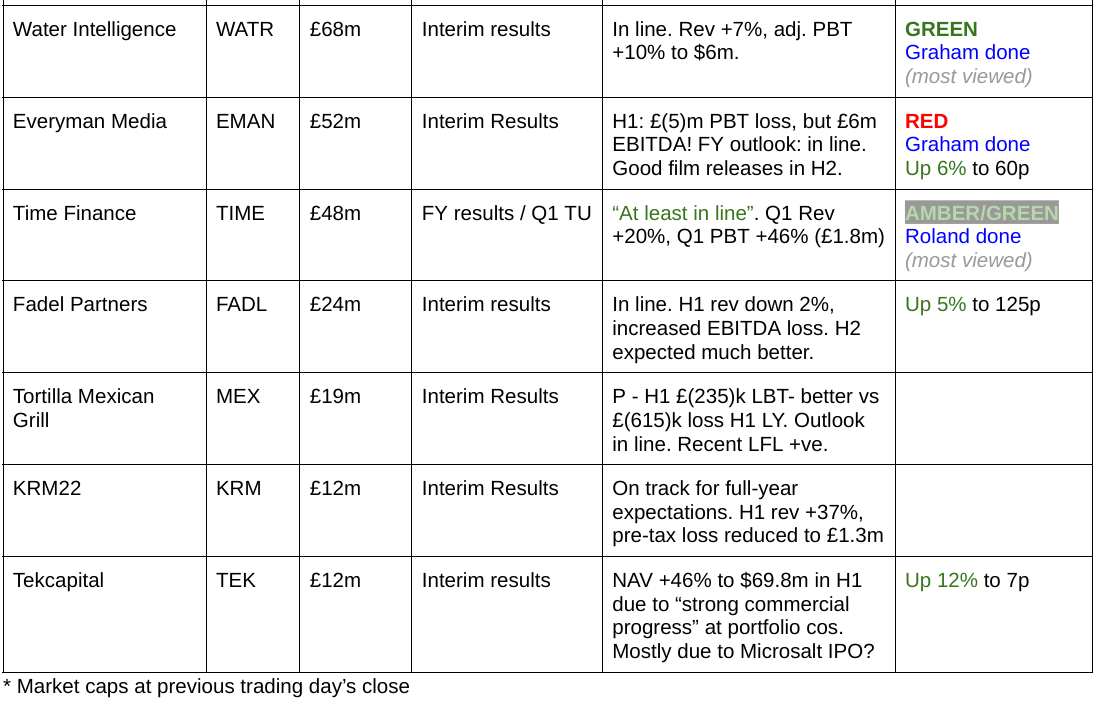

Water Intelligence (LON:WATR) - up 5% to 405p (£70m / $94m) - Interim Results - Graham - GREEN

I’m giving this a negative outlook when it comes to my stance on it! WATR has posted good interim results, in line with expectations and including a 10% increase in adj. PBT to $6m. However, to keep my positive stance on this share, I need it to do a little better when it comes to underlying sales growth (currently just 2%) and its quality metrics.

Time Finance (LON:TIME) - down 2% to 55p (£52m) - Final results / Q1 trading update - Roland - AMBER/GREEN

I’m encouraged by progress at this SME specialist lender and believe the valuation looks reasonable. This turnaround story gets a cautious thumbs up from me and appears to be gaining momentum into FY25.

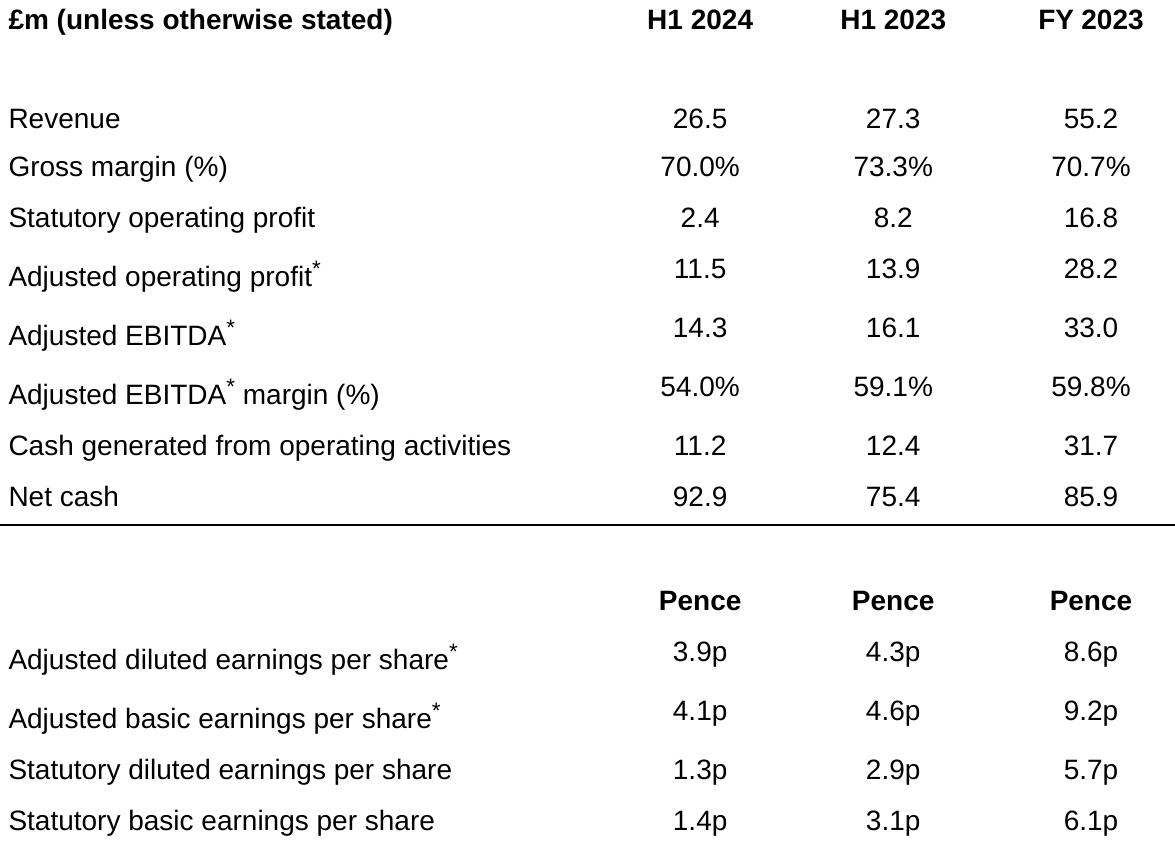

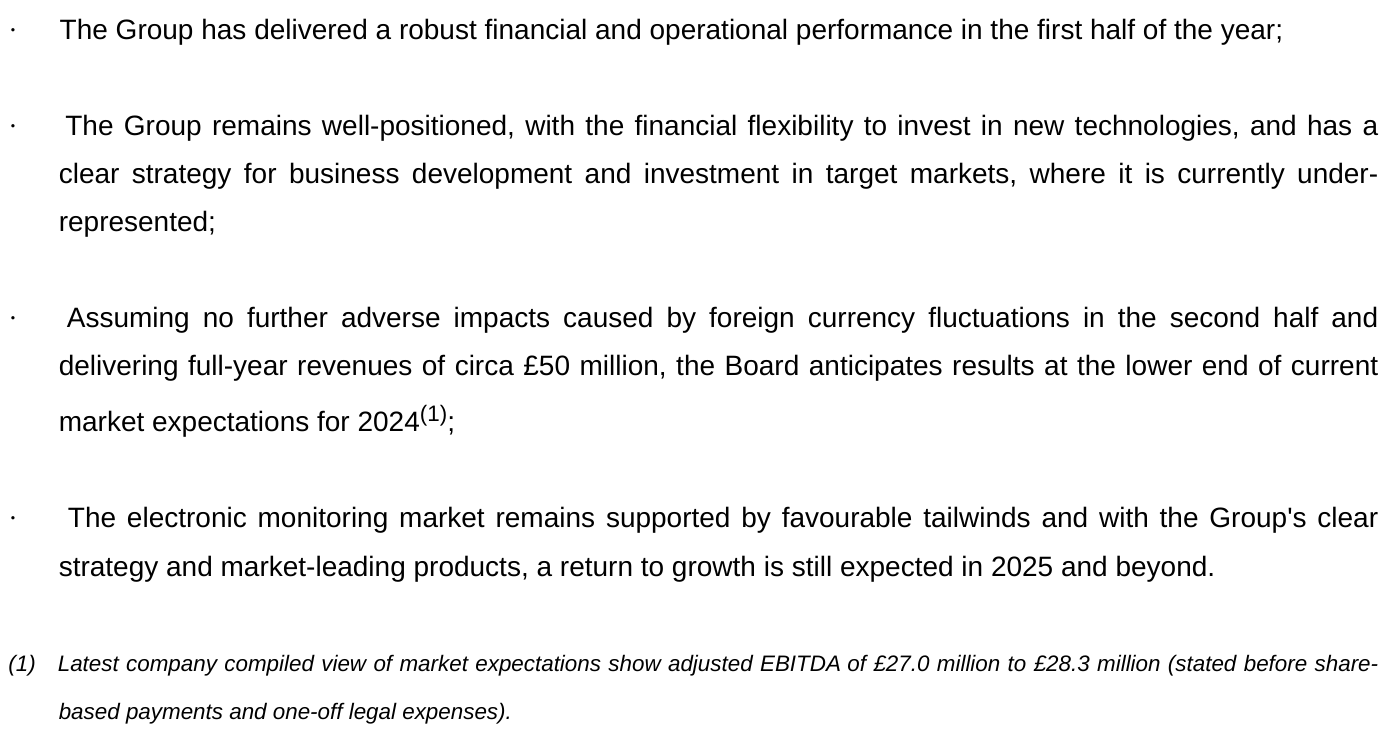

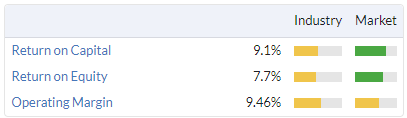

Big Technologies (LON:BIG) - down 11% to 99p (at 09:10) - £287m - Interim Results - Paul - GREEN

Almost, but not quite a profit warning today - at lower end of a fairly tight EBITDA range for FY 12/2024. Amazing balance sheet with about a third of the market cap in genuinely surplus cash, persuades me to take a positive view of risk:reward. Although bears might say it's now looking ex-growth. It's a high margin niche, and orders could be won for its innovative new devices (eg alcohol sensing tags). The price has come down a lot, and I find it more attractive value now.

Everyman Media (LON:EMAN) - up 6% to 60p (£55m) - Interim Results - Graham - RED

The outlook is in line with expectations for 2024 and the company warns that growth in 2025 might be lower, as it keeps its expansion plans limited. The market has treated this news positively, perhaps because of concern over the growing net debt position (£26m). Given its lack of real profitability, its capital intensity and its failure to demonstrate economies of scale up to this point, I see this a poor investment proposition.

Paul’s Section:

Big Technologies (LON:BIG)

Down 11% to 99p (at 09:10) - £287m - Interim Results - Paul - GREEN

Starts off with a nice simple explanation of what they do -

“Big Technologies PLC (AIM: BIG), the leading, integrated technology platform for the remote monitoring of individuals, is pleased to announce its interim results for the six-month period to 30 June 2024 (the "period").”

The main markets are international, re law enforcement, tagging of offenders, but it also provides services for monitoring of elderly/frail.

Shares have done really badly, since being one of many opportunistic & over-priced IPOs in 2021. Are they now in value territory, I wonder?

Today’s news is a mild profit warning alongside not very good H1 results.

H1 headlines don’t mention my preferred measure of adj PBT unfortunately - but does include adj dil EPS (down c.10% on H1 LY), which is a reliable number I usually find - although note the big gap between adjusted and statutory, so we’ll have to check the adjustments for reasonableness -

BIG had previously disclosed that a large contract which was being extended on short-term renewals has now ended.

We’ve looked at it twice this year previously -

19/1/2024 - BLACK - fell 20% to 102p - profit warning. Loss of Colombian contract, and US startup costs. Zeus lowers 2024 fc by a quarter. Paul - amber/green as looking interesting value.

28/5/2024 - AMBER (Graham) 167p - In line TU. Some concerns, including valuation.

As you can see from the chart above, BIG had a nice recovery after its Jan 2024 profit, warning, but has seen all those gains wither away, and we’re now back down to Jan 2024 levels again.

So we have lacklustre H1 results, with adj dil EPS down 10%.

Some cost issues are blamed, but it still has very high gross margins -

“High gross margin of 70.0% in H1 2024, but down by 330bps due to the revenue decline, increased depreciation as we roll-out the latest 4G technology and increased operational costs”

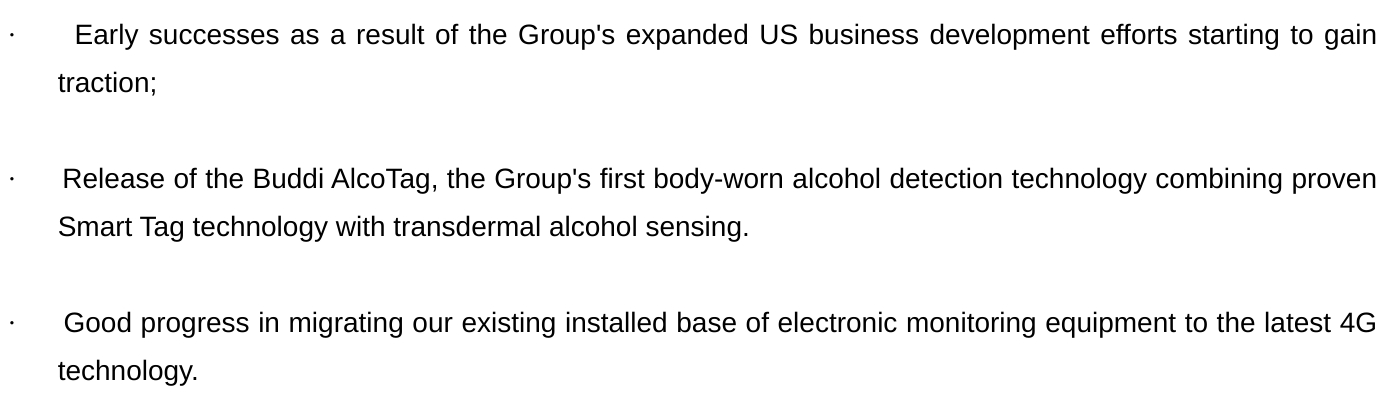

I like these points below, especially the obvious potential for an alcohol sensor, for enforced sobriety for people who do things a lot worse than just offending people on social media and via email when they get back from the pub -

What about the outlook - it’s a slight reduction in guidance to the lower end of quite a tight range, so personally I’m seeing this as only just a minor profit warning - although we’ll have to check the broker changes, to see if they’re slipping a big warning out by the back door.

Broker update - thanks to Zeus for providing more detail, really helpful. Zeus has 6.5p estimate for dil EPS in FY 12/2024. The StockReport has 6.94p consensus, so it looks a modest drop. FY 12/2023 actual was 8.5p, so clearly earnings are going in the wrong direction (down), and bears might point out that BIG now looks ex-growth, and with margin pressure.

It’s tricky to value it on a PER, since we don’t really know if future earnings are going up, or down!

Balance sheet - a very important consideration, as BIG is swimming in cash. It’s a pretty crazy balance sheet actually! There’s £95m of cash sitting there (and earning interest), with hardly any creditors offsetting it. So I would say BIG has about £100m of genuinely surplus cash/capital. That gives it lots of options (acquisitions, tender offer or buybacks/divis).

This surplus cash is about a third of the market cap, so it’s a highly favourable point which should be reflected in the valuation of its shares.

Legal costs - I’d forgotten about this. There’s a case rumbling on, see the update today. Hopefully not a serious risk, but it would be better not to have a legal case. Quite hefty legal costs of £3.1m are booked in H1. More work needed on this by potential investors.

Share based payments - are really excessive. Not good. Especially as it’s awash with cash, but doesn’t pay divis too. So whose benefit is this company actually run for? I hope the institutions vigorously flag this misalignment of interests to the 26% founder CEO.

Paul’s opinion - Despite various niggles, I think the valuation at BIG of c.100p is looking attractive, especially as a third of it is cash backed.

We’re having to guess a bit re earnings, which could go either way, I don’t know.

That said, it has a track record of operating, and innovating, in a profitable niche, where the costs of using its products to hopefully help rehabilitate offenders in the community are a fraction of the costs of prison - making obvious sense. However, there must be loads of other companies in the same field, so how do we know if BIG is going to be a long-term winner or not?

Overall, I’m going to push the boat out here, and say valuation is sufficiently attractive for me to go GREEN at c.100p, on my assessment of risk:reward (which is partly subjective of course, and I don’t know what the future holds, so could end up being wrong as the facts change over time).

Graham’s Section:

Water Intelligence (LON:WATR)

Up 5% to 405p (£70m / $94m) - Interim Results - Graham - GREEN

Water Intelligence plc (AIM: WATR.L) (the "Group" or "Water Intelligence"), a leading multinational provider of precision, minimally-invasive leak detection and remediation solutions for both potable and non-potable water is pleased to provide its unaudited Interim Results for the period ended 30 June 2024.

I was positive on this primarily US-based business back in February after the release of its full-year trading update.

Let’s see if its interim results can justify my confidence:

Sales across the entire WATR network up 2% (includes both franchised stores and corporate stores).

Revenue +7% to $41.5m.

Adj. PBT +10% to $6m.

The revenue mix has changed a little, with more revenue from corporate stores and a slight (2%) reduction in franchise royalty income. In February, we discussed how WATR was buying back one of its US-based franchise stores, in order to operate it directly. It looks like there have now been several of these acquisitions.

As a general principle, when a company buys back its franchisees, this tends to increase revenues and profits, while at the same time reducing the company’s quality metrics.

Net debt of $3m, down from net cash of $1m at Dec 2023.

Exec Chairman snippet:

"We achieved strong double-digit growth in profits and EBITDA during 1H while continuing to invest in our long-range growth plan. Our balance sheet remains strong and under-levered enabling us to have "dry powder" to complement our organic growth plans with accretive acquisitions…

Expansion: in addition to existing UK/EU business, WATR recently purchased an Irish plumbing business for a total cost of €2.3m.

Graham’s view

There’s plenty of detail in this report to get your teeth into.

The big picture from my point of view is that WATR is continuing along its chosen strategic path: trying to find organic growth wherever it can, investing in new technologies and expanding through M&A.

The resultant growth is not particularly dramatic in the short-term but over the long-term it has made progress, without too much growth in its share count:

The Executive Chairman owns 28% of the company and has been the driving force behind the company for 14 years. So I think he has no shortage of credibility or alignment.

I’m going to leave my positive stance on this one unchanged. However, I won’t do this indefinitely - I will need to see some improvements if I’m going to stay GREEN.

Firstly, I would like to see network sales growth pick up from the current 2% level, at least to match the current US inflation rate (2.5%) and preferably higher than that.

Secondly, the company’s quality metrics are still OK but are lower than they were historically (according to Stockopedia’s calculations), and are not at the level I’d expect from a quality company using the franchise model. If WATR continues buying back its franchises, perhaps these metrics will remain under pressure?

Without any improvement in the network sales growth rate or the quality metrics, I’ll probably be adjusting my stance on this one lower at some point in the foreseeable future.

The StockRanks still love it (StockRank is 94) but the weakest ranking it gets is the one relating to Value. Let’s see if it can boost performance over the next 6-12 months, to justify the rating it’s on:

Everyman Media (LON:EMAN)

Up 6% to 60p (£55m) - Interim Results - Graham - RED

Let’s check out the H1 results to June from this premium cinema group.

Financial performance: everything moving in the right direction. The outlook is in line with expectations for 2024.

Remember that the entire film/TV industry (including the likes of Adf (TSE:DRX)) was affected by Hollywood strikes last year, which had knock-on effects for this H1 period that is reported today.

With the effects of those strikes receding, there is a strong H2 weighting expected for the current year.

The film roster over the next few months includes Joker 2, Gladiator 2, Wicked, Moana 2 and a Lion King movie. A powerful set of releases, in my view!

Everyman’s full-year expectations: revenue £108m, adj. EBITDA £19.3m. This implies a 30% increase in revenues in H2, compared to H1 - that doesn’t seem unrealistic at all to me, given the upcoming film releases.

Everyman has also enjoyed a remarkable increase in market share over the past twelve months, from 4.2% to 5.6%.

As a premium offering, there are going to be limits in terms of what it can achieve on this front, which arguably makes the increase in market share all the more impressive! But of course the challenge is to operate profitably as it opens new venues in more locations.

One new venue opened in H1 2024, and another two will open in H2. Four openings are planned for 2025.

Additionally, there has been a 76% increase in membership, to over 45,000 - a year ago, it was only 26,000. New apps for Android/iOS offer customers a range of services and help to promote the membership offering.

Outlook - this includes a warning that growth in 2025 will reduce from current market expectations.

Having carefully evaluated our expansion opportunity, we are comfortable that continuing to scale at current levels - three new venues in 2024, and four in 2025 - will provide a robust increase in footprint. Whilst this level of openings will naturally reduce the rate of growth in 2025 from current market expectations, this allows the company to strengthen its balance sheet and reduce net debt moving forward. This will give us the scope and flexibility to take advantage of excellent pipeline opportunities in 2026 and beyond.

Given the share price reaction, it seems that the market is taking the news of slower expansion as good news (assuming that investors have read the entire announcement, which can’t always be taken for granted!).

Net debt is mentioned as a reason to keep growth at a modest pace over the next year. It currently stands at £26m. This is purely the financial debt - there are also significant lease liabilities (having a present value of over £100m)..

Graham’s view

If I had only read the introduction and the CEO’s statement, I would have no choice but to be excited about this stock.

However, the bad news is left to the FD to explain.

This business just doesn’t seem to make any money, no matter how big it gets:

H1 revenues are up and the pre-tax loss is up, too.

But a bigger loss isn’t reflected in deteriorating EBITDA. On the contrary, EBITDA is looking better than it did in H1 last year.

The FD explains that more venues have driven higher admin expenses including higher fixed costs, depreciation and pre-opening expenses. Labour was the highest cost increase, with the national living wage increase being a factor here, too.

If I was trying to find a bullish perspective on this stock, I’d start by pointing to the pre-opening expenses as one-off in nature. But they only amounted to £200k in H1. So they can’t help to bridge the gap between EBITDA and the pre-tax loss.

Depreciation/amortisation is the elephant in the room: it was over £7m in H1 alone.

There are also financial expenses of £3.2m.

Thanks to modern lease accounting rules, EMAN’s rent payments are included in these two categories

The upshot is that adj. EBITDA remains utterly useless as a measure of profitability, and I find it embarrassing that the company continues to report it in its “Summary of Financial Performance” while leaving out any stricter measure of profitability.

Paul was AMBER/RED on this one in April and I could leave that stance unchanged but with net debt having increased since then and with the company still showing no signs of real profitability, I’m inclined to stick with the RED that I originally put this on.

As a cinema buff, I genuinely like what Everyman is doing - I just find it difficult to imagine a bright financial future for its current shareholders.

Roland’s Section:

On Beach group (LON:OTB)

Up 3% to 149p (£249m) - Pre-close trading update - Roland - GREEN

Today’s trading update from this beach holiday specialist covers the year ending 30 September 2024, including the key summer season.

The considerable progress made over the last twelve months has set us up for further success in FY25.

Checking back through the archives, I see that we last covered On The Beach in May, when Graham reviewed the interim results. He concluded that “the stock is cheap” and the business could be well placed for the future.

We’re now on the far side of this year’s peak holiday season, so what’s changed?

On The Beach’s share price hasn’t moved over the summer, but today’s update seems broadly encouraging. Let’s take a look.

On The Beach says its Total Transaction Value (TTV) rose by 15% to a new record of £1.2bn last year. I imagine some of this reflects price rises rather than volume growth, but it still seems positive to me.

As an agent, OTB won’t report all of this as statutory revenue. For context, Stockopedia’s consensus forecasts show revenue rising by 8% to £184m this year.

As this is a trading update, the company has not included details of revenue or profit, other than to report:

Adjusted PBT in line with market expectations, despite incurring significant one-off costs related to the Ryanair integration.

A helpful footnote confirms that the consensus estimate for adjusted PBT is £31m, 31% above the £23.6m reported last year.

I would guess this means that adjusted earnings will also be in line with consensus. Stockopedia shows forecast earnings of 14.7p per share for FY24. This would represent an increase of 27% from FY23 adj earnings of 11.6p ps.

I’m encouraged to see earnings rising more quickly than revenue, as this appears to confirm that the business is delivering positive operating leverage as volumes recover post pandemic.

The group’s capital-light model means it can add volume without a corresponding increase in fixed costs. When this happens, profit margins rise more quickly than sales.

Indeed, On The Beach confirms this in today’s update, reporting “significant improvement in operating leverage”.

I expect the group’s operating margin and return on equity to return to double digits this year, as they were prior to the pandemic:

With the stock only trading on 10 times FY24 forecast earnings, I think stronger profitability could potentially support a much higher share price.

Cash generation also appears to have been strong. The group ended the year “debt free” and with a cash position of c.£95m. This reflects peak cash at the end of the summer trading season, but it’s still an improvement over the comparable cash figure of £76m at the end of FY23.

It’s worth noting that On The Beach does still appear to rely on debt during the year – the half-year results showed a net bank debt position of £47m, by my reckoning. So there are some big movements in working capital during the year as the company accepts customer prepayments and pays its own suppliers.

Dividend: following the reintroduction of the interim dividend in May, the board expects to recommend a final dividend as well.

Ryanair partnership - costs? On The Beach signed a deal with this leading budget airline in February that gives OTB “free and fair access to Ryanair seat supply”.

This deal marked an end to a legal dispute between the group and seems positive to me, but it appears that setting up this partnership has incurred “significant one-off costs”. These might be worth checking in the results, as they could impact statutory profits.

Outlook: CEO Shaun Morton says that Winter 24 volumes are currently 34% ahead of last year, with “customers seeking winter sun and enjoying our long-haul destination packages”.

At this early stage, bookings for Summer 25 are said to be “very encouraging”.

No formal outlook statement was provided today, with further detail promised with the FY results in December.

Roland’s view

I was a fan of this business prior to the pandemic and am pleased to see that its recovery is continuing.

Share price reaction has been muted this morning, presumably because the results are in line and no outlook has been provided for FY25.

It may also be worth noting that earnings growth is expected to slow significantly in FY25, according to Stockopedia’s consensus numbers:

Perhaps some caution is merited, given the risk that consumer spending could remain under pressure.

However, the stock’s valuation looks very reasonable to me for a cash-generative business where I expect to see double-digit returns on equity.

I share Graham’s previous view that the stock continues to look cheap and will stay green on this one.

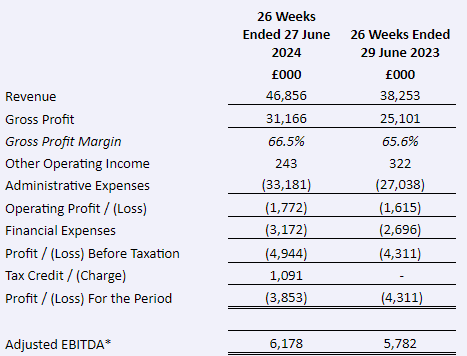

Time Finance (LON:TIME)

Down 2% to 55p (£51m) - Final results & Q1 trading update - Roland - AMBER/GREEN

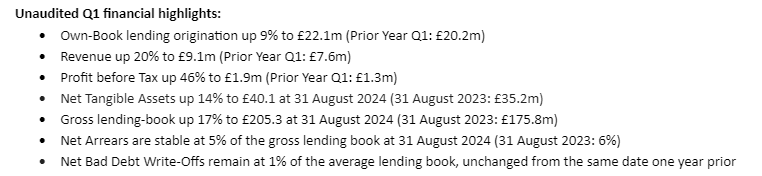

Significant increases in Revenue, Profit Before Tax and Earnings Per Share. Own-Book origination and Lending continue to grow as Net Arrears fall

This small-cap business lender specialises in providing asset, loan and invoice finance to UK SMEs. It has proved to be a successful turnaround, although the shares have yet to return to their historic highs.

Today’s results and Q1 update suggest to me that progress is continuing to plan.

Final results summary: Let’s start with a look at the lender’s numbers for the year ended 31 May 2024.

Revenue up 30% to £33.2m

Pre-tax profit up 41% to £5.9m

Earnings per share (dil) up 30% to 4.8p

Loan book up 18% £201.2m

Net assets up 7% to £66.1m

Net tangible assets (ex goodwill) up 13% to £38.6m

Financial performance improved last year, although the board does not yet feel that it’s appropriate to pay a dividend – the last payout was in 2019.

Credit quality and exposure to any wider slowdown in the UK economy is obviously a relevant factor for a business of this kind. Fortunately, performance seems to have improved modestly last year:

Net deals in arrears at 31 May 24 of 5% (31 May 23: 6%%)

Net bad debt write-offs equal to 1% of loan book (31 May 23: 2%)

Trading commentary: the company has continued to increase its focus on own-book lending, rather than lending through brokers. Own-book loans accounted for 97% of lending last year, down from 96% in FY23.

In numerical terms, own-book origination increased to £91.6m last year, from £73.4m in the prior year.

Lending growth was strong in both of the group’s core divisions:

Invoice financing up 16% to £65m YoY

Asset Finance up 37% to £85m YoY (particular strength in hard assets)

Time Finance said it had funding headroom of “over £65m” at the end of May, providing ample scope for further lending growth.

Profitability: this isn’t a business I’m hugely familiar with, and when I looked at the StockReport, I was struck by the apparent low profitability of the business (in terms of return on equity):

However, these results highlight a large difference between net assets (£66.1m) and net tangible assets (£38.6m).

Checking the balance sheet shows that the difference between these two figures is largely made up of £27.3m of goodwill. I haven’t researched the origins of this figure, but it’s unchanged from last year and doesn’t seem recent.

I don’t normally ignore goodwill (which typically represents past capital allocation decisions). But in this case I think it makes sense to focus on tangible assets, so we can understand the level of return being generated by the business on its trading assets (i.e. loans).

Based on last year’s net profit of £4.4m, my sums suggest a return on tangible equity of 11.5% (FY23: 10.2%).

This seems reasonable to me, if not outstanding. However, the improving trend from last year suggests the company’s strategy may be delivering positive results.

Balance sheet: Equity on a lender’s balance sheet can be a small number that’s the difference between two very large numbers. Big banks are a classic example of this. A small change in asset (loan) values can wipe out equity almost completely.

In Time’s case, the tangible equity on the balance sheet does seem to be more meaningful. Tangible assets of c.£38m represents the difference between net receivables (loans) of £178m and payables (funding) of £141m.

Thus, in theory, the company might be able to absorb losses approaching 20% of its loan book before its equity was completely wiped out.

In practice, things probably wouldn’t be allowed to get this far. But on first inspection, the balance sheet seems fairly decent to me.

Q1 trading / outlook: progress so far this year appears positive, with the trends I’ve highlighted above continuing into FY25. Indeed, momentum appears to be strengthening, with Q1 PBT 46% higher than the same period last year.

I’ve pasted in these highlights, to save me retyping them:

An updated note from house broker Cavendish is available on Research Tree today (with thanks).

Cavendish has FY25 earnings estimates of 5.6p per share, rising to 6.5p in FY26. Consensus shown in Stockopedia ahead of these results for FY25 is 5p per share, so I suspect we will see upgrades coming through over the coming days.

This FY25 estimate prices the stock on approximately 10x forward earnings.

Roland’s view

Time Finance seems to be becoming a mini Close Brothers (LON:CBG) – this troubled FTSE 250 lender has a significant business providing secured lending to UK SMEs.

I’m encouraged by today’s results and while I’d want to learn more about the lender’s customer base and lending policies and funding arrangements before considering an investment, my view is broadly positive.

In terms of valuation, I think the shares look reasonable, although not necessarily as cheap as they might seem.

Based on the Q1 net tangible asset figure of £40m, the stock is trading at around 1.3x net tangible assets.

Assuming a return on tangible equity of 12% gives a return on cost of equity of about 9% for buyers at current levels, according to my sums.

That looks about right to me, but Time Finance’s strong execution and continued growth mean I’m happy to take a positive (amber/green) stance here.

See what our investor community has to say

Enjoying the free article? Unlock access to all subscriber comments and dive deeper into discussions from our experienced community of private investors. Don't miss out on valuable insights. Start your free trial today!

Start your free trialWe require a payment card to verify your account, but you can cancel anytime with a single click and won’t be charged.