Full Year 2026 audited results

Carclo plc

Full Year audited results for the year ended 31 March 2026

Carclo plc ("Carclo", the "Group" or the "Company"), a global precision engineering group with comprehensive, end-to-end manufacturing capabilities announces its audited full year results for the 12 months ended 31 March 2026 ("FY26").

Business highlights

Operational & Strategic

· Achieved the previously set mid-term financial targets for Return on Sales ("ROS") and Return on Capital Employed ('ROCE'), ahead of plan providing a strong platform to support further sustainable profitable growth

· Continued improvements in operational efficiency and manufacturing standardisation drove margin improvement

· Significant long-term contract renewal secured with a major life sciences customer

· Sustained strong health and safety performance across the Group with Incident Frequency Ratio of 0.7 per 100,000 hours worked (FY25: 0.7)

Financial

· Revenue of £114.2 million (FY25: £121.2 million), with CTP accounting for £98.2 million (down 8.2%) and Speciality delivering £16.0 million (up 12.5%) reflecting the rebalancing and management of our portfolio with a focus on higher margin contracts as demonstrated in our increased profitability, along with a reduction in D&E activity and foreign exchange headwinds

· Underlying operating profit of £12.6 million, up 28.1% (FY25: £9.8 million) driven by operational efficiencies and focus on higher margin business

· ROS improved to 11.0% (FY25: 8.1%), ahead of the 10% target set in 2022

· ROCE improved to 29.1%, ahead of the 25% target set in 2022

· Net Debt/underlying EBITDA of 1.3x a slight increase on prior year, largely driven by a one-off additional pension contribution of (£5.1m) in April 2025

2026

2025

Change

Revenue

£114.2m

£121.2m

-5.8%

Underlying EBITDA1

£18.6m

£16.4m

+13.6%

Underlying operating profit 1

£12.6m

£9.8m

+28.1%

Cash generated from operations 1

£12.0m

£19.1m

-37.1%

Net Debt

£23.9m

£19.2m

+24.5%

Statutory operating profit

£12.3m

£7.6m

+61.8%

Statutory profit for the year

£2.7m

£0.9m

+200%

Statutory basic earnings per share

3.7p

1.2p

+209%

1. Underlying operating profit are the equivalent statutory measures adjusted to eliminate the significant one-off items not linked to the underlying performance of the business. Underlying Earnings Before Interest Tax Depreciation and Amortisation (EBITDA) is reported on the same basis.

Precision 2030 growth plan

Over the past three years the Group has implemented a turnaround strategy to address the significant challenges it faced. Under this strategy, the Group has: exited its low-margin business and repositioned to higher value engineered solutions; optimised its manufacturing footprint; refinanced its debt; and agreed a long-term plan to eliminate the Group's pension deficit.

The success of these efforts can be seen through the delivery of the Group's financial targets ahead of schedule.

From these solid foundations our focus now turns to driving growth, through the adoption of the Precision 2030 growth plan. The plan's growth targets will be achieved through a combination of:

· expansion within our existing customer base with solutions we already deliver for major customers

· securing new programmes with new and existing customers by entering adjacent higher-growth markets such as drug delivery, wearables and pharma packaging

· Leveraging our innovation strengths to develop new solution categories where our precision engineering sets us apart

These initiatives are expected to lead to a steady increase in the Group's growth rates. As a result, our targets for 2030 are:

· Organic revenue growth at a compound annual rate of more than 8% across the plan period

· Net debt of less than 0.5x

· Ensuring new work continues to deliver on our minimum 10% ROS and 25% ROCE targets

Achievement of these targets is expected to create significant shareholder value and further enhance the competitive position of the Group.

Current trading and outlook

Three years ago, Carclo was a business facing significant financial and operational challenges. Through a sustained focus on operational excellence we have addressed those issues and today Carclo has a strong foundation and a disciplined plan for sustainable growth.

Market conditions across the Group are currently mixed. In Aerospace, demand remains strong and we are well-positioned to benefit from sustained sector growth in both civil and defence applications, supported by the additional capacity now in place. In Life Sciences, conditions are more varied: parts of the portfolio continue to perform well, while demand from certain diagnostics customers has been softer in the early part of this year. In particular, a notably weaker respiratory virus season has reduced testing volumes across the diagnostics industry, leading some customers to adjust inventory levels; an effect we expect to be temporary. We anticipate demand strengthening as we move through the year as a number of our new growth initiatives come on stream and accordingly expect trading to be weighted towards the second half and to deliver positive organic revenue growth for the full year.

Commenting on the results, Frank Doorenbosch, Chief Executive Officer said:

"In FY26 we delivered a resilient performance, benefiting from the measures we have put in place over the past three years to improve efficiency and using our deep domain knowledge and key customer relationships to focus on higher margin activities. Achieving our medium term financial targets clearly demonstrates the progress we have made.

In the past three years we have built a platform to deliver sustainable, higher profitability and increased cash generation. I am therefore excited to introduce our Precision 2030 growth plan, which highlights our confidence in our ability to innovate, to win new business and increase our growth rates. I look forward to reporting on our progress against the targets we have set."

About Carclo plc:

Carclo is a global precision engineering group that designs, industrialises and manufactures highly reliable solutions for Life Sciences, Aerospace and Safety & Security markets, manufactured in-region, for-region.

Carclo plc is a public company whose shares are quoted on the Main Market of the London Stock Exchange.

LEI: 21380078MEM399JPI956

Group Overview

Carclo is a global precision engineering group specialising in highly regulated markets which are often life-critical, requiring high performance solutions where reliability, compliance and technical precision are essential. As a result, the cost, complexity and risk to the customer of switching suppliers makes relationships genuinely long-term as evidenced by the long customer tenure for various solutions.

The Group operates through two divisions: Carclo Technical Plastics ('CTP') and Speciality.

CTP

CTP operates through two business units:

· Design & Engineering ('D&E'): This unit provides the product development and manufacturing engineering capability that turns market and customer requirements into engineered solutions, often setting new industry standards. It supports customers from early concept through to full-scale production, covering product design, tooling and mould engineering, development of protypes and production process engineering. Successful D&E projects drive the next wave of solutions manufactured by the Manufacturing Solutions unit.

· Manufacturing Solutions ('MS'): utilises a global production platform to deliver reliable, high-precision injection moulded components that form a customer's end products. Key segments include

o Life sciences

§ In-vitro-diagnostics ('IVD'). The Group manufacturers cuvettes, microfluidic cartridges, pipettes, and plastic analyser modules/housings for 6 of the top 10 IVD OEMs globally. The global market growing at a CAGR of 5%-7%.

§ The drug delivery market includes technologies for administering medicines, such as injection pens, auto-injectors, and inhalers. The injectable drug delivery segment is growing at 8%-16% per annum depending on product.

Speciality

The Speciality division combines precision engineering with deep sector knowledge to create solutions that operate in highly demanding environments. The division services two key end markets:

· Aerospace ('Aero'). Providing a range of high-performance mechanical cable assemblies and machined components. These products are designed to deliver reliable, traceable and high-performance components that keep aircraft and defence systems safe, operational, and compliant.

· Light and Motion ('L&M') is a precision optics business serving automotive, architectural, commercial, and industrial lighting markets.

Chief Executive's Business Review

Engineered for Growth

Frank Doorenbosch, Chief Executive Officer

Strategy is delivering. The next phase is growth.

Three years ago, we set out three objectives for the business: a safer and more sustainable company, operational excellence in every site, and a stronger, more resilient balance sheet. This, all with the overarching objective to deliver a sustainable Return on Sales of 10% and a Return on Capital Employed of 25%. Our FY26 results show the strategy has delivered on all fronts, ahead of our own schedule. From these foundations, our Precision 2030 plan sets out where we are taking the business from here.

What we worked towards

The objectives set in October 2022, following my appointment as CEO, were not glamorous. They were the conditions Carclo had to meet before we could credibly speak about anything else.

The work that followed had three strands. Firstly, operational excellence across every site: we delivered lean, regional factories, each with a clearly defined and focused role, delivering enhanced asset utilisation, on-time delivery and our target margin. Secondly, financial resilience. We reduced the debt burden through stronger cash generation, better asset utilisation and strict working capital control. Finally, a cultural reset: One Carclo, with a single quality standard across three continents, and with safety and environmental stewardship embedded in how we run every shift in every site.

In FY26, the three strands came together. The factory specialisation programme across the CTP Division is complete, with every site now carrying a defined role inside our global network.

We delivered on our promises

The numbers for the year reflect this progress. Return on Sales increased to 11.0% (FY25: 8.1%), passing the 10% target we set in 2022. Return on Capital Employed reached 29.1% (FY25: 24.4%), passing the 25% target set in the same year. Underlying operating profit grew by 28.1% to £12.6m. Positive operating cash generation saw cash generated from operations at £12.0m (FY25: £19.1m).

Group revenue of £114.2m was below FY25 due to lower D&E activity in CTP driven by lengthy sales and validation cycles which reflect the criticality of the products we produce for customers.

During the past four years we made difficult decisions to exit low-margin, short-run work, mostly in the US, and we worked through the planned wind-down of the critical asset revitalisation programme in our Design & Engineering business, the multi-year cycle of rebuilding and upgrading mould and back-end automation across the network. This was a keystone to create a revitalised Carclo: a better not bigger business, that is more agile, more coherent and financially healthier one.

CTP Division

CTP generated revenue of £98.2m in the year (FY25: £107.0m). Within that headline number, the mix has improved materially. The completion of our operational excellence plan in the US has delivered, as planned, a consistent and sustainable contribution from our life sciences work across the globe.

Design & Engineering

Design & Engineering (D&E) is where customer projects are turned into manufacturable products, and where much of our innovation work sits. D&E revenue of £9.7m (FY25: £13.6m) reflects the planned end of the asset-revitalisation cycle that ran from FY23 to FY26. The programme aimed to optimise our manufacturing footprint, and the completion of this programme has resulted in a more efficient manufacturing base with higher capacity utilisation.

The order book and the pipeline tell a different story to the headline. New design verification protocols and enhanced simulation capability are compressing time-to-market on regulated programmes. C-Mould, our proprietary tooling platform, produces production-ready tools in weeks rather than months, and continues to deliver market leading qualification timelines. One example from the year: a 2K-moulded component for a drug delivery device programme, combining two materials shots in a single moulding step and thereby replacing a four-piece component, was qualified to the point of regulatory submission within three months of the first customer brief; an outstanding achievement most competitors cannot hit.

The Life Tech Solutions team operates as our innovation incubator, tightly aligned to where customer demand will be in three to five years' time. New developments in proprietary closures, drug-delivery solutions and connected inhalers all moved forward during the year; their role in our growth plan is set out under the Innovate section below. We also built and began piloting the Carclo AI Framework, with a six-person working group operating to a sixty-day mandate and a costed strategy. Five use cases have been prioritised, from in-line vision quality control at our regulated sites to AI-assisted computer-aided manufacturing in Speciality. The focus is engineering productivity; we will report outcomes when there are meaningful ones to report.

Manufacturing Solutions

Manufacturing Solutions, with its repeat, programme-based revenues, is the long-term value creation engine of CTP. Revenue of £88.5m (FY25: £93.4m) largely reflects the volume rebalancing across the network and the effect of foreign exchange rate movement. On a like-for-like basis, taking into account the effect of product lines we exited in the prior year and at constant currency, MS revenues were in line with the prior year. Having completed the strategic realignment of the portfolio, the business is now focused on delivering consistent operational performance following this portfolio restructuring. The US business has, as planned, come through its restructuring with materially higher operating margins, and is now an accretive part of the Group, and the unified Pennsylvania operation runs to the same operational and quality standard as our EMEA and APAC sites, delivering the same margin performance.

The standout site this year was Brno in Czechia. Volumes grew strongly, and we made significant progress on integrating new projects and solutions. The site also took the lead on our new Pharmaceutical Packaging and Closures growth vector, which we expect to be a material contributor by FY29. China continued to grow steadily, supporting our global In Vitro Diagnostics (IVD) programme now including regional life science customers.

India is a strategic opportunity for the group. Alongside our established ATM and optics work, we are completing the site's diversification toward life sciences, with our main customer's IVD programme as the anchor. We also gained local life science customers in an important, high growth market. Capacity that previously supported declining adjacencies is now being qualified for high-volume diagnostic disposables and drug delivery systems, and we expect the India site to look materially different in mix and margin profile in the future. In the UK, our site in Mitcham is focused on high-volume production runs. It delivered on plan, with regulated work from the life sciences sector continuing to grow.

During the year we completed the global roll-out of our polymer price and energy adjustment mechanism, indexed quarterly. This is a structural change for the business. It moves the conversation with customers from defensive price negotiation to transparent pass-through, and it protects gross margin through commodity cycles. This has been an important process in times where input cost can rise due to geopolitical changes. The sales team led the work and the discipline is now embedded across the group.

Speciality Division

Speciality revenue grew 12.5% in the year to £16.0m (FY25: £14.2m), with operating margins reaching 22.4%. From mid-2026 the aerospace parts of the division will operate closer together, and with technology exchange we are exporting 150 years of precision engineering at Bruntons Musselburgh, Scotland to our global customer base. Bruntons has a clear brand equity in aerospace. In Jacottet, our facility in Chartres in France, we have invested in new machinery capacity, allowing them to expand its offering from cable solution to include the precision machining components, allowing a consistent combined European offer.

Aerospace

Our Aerospace business delivered a third consecutive year of record orders. The franchise in streamline wire, the aerodynamically profiled bracing wire used on aircraft structures, and in flight-control cables for the main helicopter platforms continued to grow. The product lifecycle is worth explaining: once a component is qualified on an aircraft platform, it is typically supplied for the life of that platform, often decades. That makes the work slow to win and very hard to displace. Continued investment in machined components, at both our Musselburgh and Chartres sites, opened further opportunities across civil airframes and helicopter platforms.

Beyond the strategic customers with a long history at Bruntons, we made progress on adjacent OEM relationships, in particular in Defence. NATO defence spending, now indexed to a higher floor, supports a multi-year demand environment for the components and assemblies we produce. Record civil European aerospace backlogs are a second and the future growth of this business is supported by both growth trends

The Speciality leadership team continued to broaden the customer base and to grow its precision-machining output.The business we have built is meaningfully different from the one we started with.

Light & Motion

Light & Motion is a small part of the group, and we have positioned it accordingly. Fresnels, our passive infrared optics business, grew in the year and is now a part of our Safety & Security offering, with a focus on leisure mobility lighting and new geographies. iCoil, which supports the visually impaired, has a new brand and distribution strategy. None of it is dramatic. It is the right positioning of capital and attention.

Safety and people

Our Incident Frequency Ratio in FY26 was stable at 0.7 (FY25: 0.7). The two-year reduction from 2.3 in FY24 is substantial, but the discipline has to be renewed every day. Our third annual Safety Week reinforced the same principle in every site: every colleague has stop-work authority.

During the year we have focused on strengthening the team for the growth journey, and Steve Lents joined in April 2026 as VP Global Sales, Andrew Sargisson focused on global business development and Lee Dodd on Life Tech Solutions. These appointments are structural enablers for the growth phase. We have also strengthened the finance team leadership below board level to provide better management information and improved financial controls across the group.

Sustainability and Project Zelda

Project Zelda, our programme on waste reduction, energy and yield, continued to deliver throughout the year. UK operations now run on 98% CO₂-neutral electricity. CO₂e per £1m of revenue improved by a further 18%% during the year. APAC continued to progress toward CO₂ neutrality, and we have begun the equivalent groundwork in the US. The full detail sits in our TCFD disclosure. The principle is simple: less waste and less energy is good manufacturing practice, and the environmental benefit comes from the same work.

Next step: Precision 2030

Completing a turnaround does not, on its own, tell you where a business is going. It gets you back to the starting line. We have done that work, and the question of whether Carclo can deliver on its commitments has been answered positively. What matters from here is growth, in scale and in pace. Precision 2030 is how we intend to deliver it.

Precision 2030 is our five-year plan that sets out how we will deliver sustainable organic growth whilst maintaining our financial discipline. Our Precision 2030 headline targets are:

· Organic revenue growth at a compound annual rate of more than 8% across the plan period

· Net debt of less than 0.5x EBITDA by FY31

· Whilst ensuring new work continues to deliver on our minimum 10% ROS and 25% ROCE targets

These targets are organic. We anticipate that we will be in a position to consider bolt-on acquisitions in the later years of the plan. Any future acquisition will be assessed under a disciplined buy-and-build criteria and would accelerate the trajectory and represent upside to these targets.

Precision 2030 rests on two pillars: Expand and Innovate, building on the foundations we have just delivered. Expand is the key driver of revenue growth through the plan. Innovate keeps that growth defensible and provides longer-term margin upside potential.

Expand

We will grow on the platform we have built, through three areas of activity:-

Deeper relationships with existing customers

Carclo serves six of the top ten In Vitro Diagnostic ("IVD") OEMs, with an average customer tenure of more than fifteen years. Our largest customer relationship alone runs across around sixty separate programmes, in multiple sub-sectors, capabilities and geographies. During the year we secured a five-year contract renewal with this customer, evidence that the partnership approach works both ways.

In Aerospace we agreed a three-year contract renewal with our major customer in the commercial aircraft segment, demonstrating that every part of the business contributes to stability and growth.

The next layer of growth is more programmes, more components and more value-add per component at the customers where that trust already exists.

Entering adjacent segments where demand growth is structural

In drug delivery, our pen and auto-injector capability is still relatively modest, but it has earned us credibility and we have already won new, smaller contracts on the back of it. The opportunity we are aiming at is the rising demand for self-injectable GLP-1 therapies: the new generation of diabetes and weight-loss treatments.

In pharmaceutical packaging and closures, we are entering a large and steady market that is moving in our direction. The growth in biologic medicines and in device-based delivery is raising the technical bar for the components that contain and dispense those drugs. Seals and closures now must do more, interact less with the medicine inside, and survive sterilisation. Liquid Silicone Rubber, micro moulding and proprietary materials are what let us meet that bar. These are not commodity capabilities. They are hard to qualify, and once a customer designs our component into a regulated product, that work tends to stay with us for years. This is higher-value engineering that broadens our Life Sciences base beyond diagnostics. It is a clear example of what the Innovate pillar is meant to do: technology that opens new revenue and makes the wider relationship stick.

In wearables, we expect to benefit from growth in continuous glucose monitors, patch pumps and smart pens, devices that combine precision plastics with electronics and sit directly on the patient. In veterinary care, projects already running give us a foothold in a higher-value adjacency that is less contested.

In defence, spending is rising. The sector demands the high standard of quality and accreditation, which Bruntons already delivers for our civil aerospace business. That accreditation is what positions us to deliver in the defence sector, and once a part is qualified the demand is sustainable.

Reaching customer bases we have historically under-served

In APAC our focus for growth is life sciences. We have long produced for the global giants; the opportunity now is with the many smaller local players we have never seriously courted.

In India, we sit in the heart of a growing aerospace industry. By building on the metal machining capabilities we already operate there, we are creating new routes to market for the Aerospace business. These are categories we have under-played in the past.

Innovate

Innovate is where we build intellectual property of our own, and it matters for clear commercial reasons.

When the technology, the material or the product is ours, the customer designs their product around something only we can supply. Once we are designed in, we are difficult to design out. The relationship deepens well beyond price, and the margins are structurally higher. Owning the technology also opens doors to new segments and new customers, in pharmaceutical packaging, drug delivery and wearables. Revenue of this kind is more dependable and harder to dislodge, and that is what creates lasting value in a business like ours. That is what Innovate is for: building things our competitors cannot offer.

We are investing in three areas, detailed below. Not every programme will succeed, and the plan does not need them all to. The growth we have committed to is carried by the wider business. What Innovate adds is durability, turning that growth into a business that holds its position and its margins over time.

Proprietary technology

We are investing in a range of new manufacturing capabilities. Our Liquid Silicone Rubber capability at our Czechia site gives us a certified position in a material the device market increasingly demands. Micro-moulding, which we can deliver in the US and EMEA, producing components measured in fractions of a millimetre, is what the next generation of drug-delivery devices and wearables requires, and few suppliers can make it at production quality. C-Mould, our new tooling platform, turns tool production from months to weeks, which gives us a time-to-market advantage on every new programme we quote. New fusion-bonding metallurgies and 3D metal printing improve the mould tools themselves. In plain terms, better ways of joining metals inside the tool give us better cooling and material flow, and that is what makes tight tolerances achievable at production speed.

Proprietary materials

We are developing new stopper solutions for injectable drug packaging, where tightening US and EU regulation is pushing the market toward engineered alternatives and rewarding the supplier that moves first. We are also working on unbreakable barrier vials that replace glass with engineered plastic, removing the breakage risk that matters most in biologic packaging.

Proprietary products and services

We are working with partners on standardised drug-delivery engines: pre-approved internal architectures that customers can customise on the outside while the engine remains ours, cutting their development time and keeping the intellectual property with Carclo. One example is the development of connected inhalers, integrated with our proprietary Syncura digital layer for adherence tracking and dose verification.

We also run innovation as an open process rather than a closed one. The Carclo Sandbox is how we do that, a space where we work with innovation partners to bring ideas in from outside and take them through to a commercial product. We gain more ideas to draw on and we reach a workable solution faster. We also avoid having to build every capability in-house.

The direct revenue contribution from Innovate within Precision 2030 is modest but this understates its role. Innovate is the reason existing customers stay, and the reason new ones come to us when the problem is difficult to solve. It is also what raises quality growth whilst Expand delivers value, keeping more higher margin proprietory work.

What the growth phase asks of us

Operational Excellence was a leadership-driven reset of our entire organisation. Expand and Innovate cannot be delivered in the same way. They need three behavioural changes across the organisation, and all three are already underway.

Firstly, we are repositioning from order takers to value engineers. Every customer conversation now starts with a problem worth solving rather than a part number, and engineering insight has to walk into the meeting alongside sales. What makes this real this year is the new talent joining our Customer Partnership team.

Secondly, we are moving from defenders to hunters. During the turnaround we defended the base. The growth phase needs the opposite reflex: to go and find the customers, segments and geographies that do not come to us on their own. Examples we are targeting are veterinary care, defence and the Indian aerospace market: none of these turn up at the door.

Thirdly, we are moving from reactive engineering to proprietary IP. Historically we engineered to a customer brief, and the customer owned the IP that came out of it. To grow on our terms, we need platforms that are ours, that we can sell many times over, and that are difficult for a competitor to copy. The LSR capability, the inhaler platform and the Sandbox are early examples of a much bigger shift.

Underneath all three sits a broader change, from a turnaround culture to a growth culture. In a turnaround, leadership cascades the plan and the team executes. In a growth phase, the team identifies opportunities and leadership clears the path. The move into life sciences in India started at the site itself. The AI Working Group grew from the teams, and so did the Sandbox. The mindset is already changing, and Precision 2030 makes it the operating model.

Outlook

Three years ago, Carclo was a business facing significant financial and operational challenges. Through a sustained focus on operational excellence we have addressed those issues, and today Carclo has a strong foundation and a disciplined plan for sustainable growth.

Market conditions across the Group are currently mixed. In Aerospace, demand remains strong and we are well-positioned to benefit from sustained sector growth in both civil and defence applications, supported by the additional capacity now in place. In Life Sciences, conditions are more varied: parts of the portfolio continue to perform well, while demand from certain diagnostics customers has been softer in the early part of this year. In particular, a notably weaker respiratory virus season has reduced testing volumes across the diagnostics industry, leading some customers to adjust inventory levels; an effect we expect to be temporary. We anticipate demand strengthening as we move through the year as a number of our new growth initiatives come on stream and accordingly expect trading to be weighted towards the second half and to deliver positive organic revenue growth for the full year.

The last three years have asked a great deal of the people at Carclo, and they have delivered. The phase ahead will ask different things of us. It needs more ambition and more initiative, and a real curiosity about where the next opportunity lies. I see those qualities in the business already. To everyone who helped get us here, and to those joining us now: thank you.

Frank Doorenbosch

Chief Executive Officer

30 June 2026

Chief Financial Officer's review

Overview

The Group delivered a resilient operating performance against a backdrop of macroeconomic weakness, achieving its key financial targets ahead of schedule. The drivers of this performance were continued improvements in efficiency and the successful execution of our move to higher margin business.

The positive operational performance enabled the achievement of the Group's medium-term targets for the key metrics of Return on Sales ("ROS") and Return on Capital Employed ("ROCE"). ROS improved to 11.0% (FY25: 8.1%), ahead of the 10% target, whilst ROCE improved to 29.1% (FY25: 24.4%), ahead of the 25% target, both set in 2022, which now become the reference point for the business in the future.

The accomplishment of these targets is directly related to the actions taken over the past three years to restructure the business, focussing on advanced process optimisation, increased asset utilisation and efficiency, improved pricing, better purchasing and a drive to reduce waste whilst demonstrating robust cost management.

Underlying EBITDA was £18.6 million, up 14% (FY25: £16.4 million) driven by exiting low-margin, short-run work and concentrating the portfolio on regulated markets. As a result, underlying operating profit of £12.6 million increased by 28% (FY25: £9.8 million).

Net finance charges for the period were £7.4 million (FY25: £4.9 million), of which £3.5 million relates to non-cash items, accordingly bank and lease interest was broadly in line with the prior year. Profit before tax increased to £4.8 million (FY25: £2.7 million). Adjusting items were £0.3 million (FY25: £2.3 million), and statutory earnings per share increased to 3.7p (FY25: 1.2p).

We also completed a refinancing of our primary external financing facility and agreed a deficit recovery plan for the Group's UK defined pension benefit plan at the beginning of the year. Together, the operating performance and the financial measures we have taken provide a sound platform for the implementation of the Group's Precision 2030 growth plan.

We use a range of KPIs to manage performance of the business and to measure progress against our strategic goals, these are highlighted and discussed throughout this report.

Financial performance

Revenue

Group revenue during the period was £114.2 million, a decline of 5.8% or 3.7% on a constant currency basis over the prior year (FY25: £121.2 million).

This year is the first full reporting year following the strategic portfolio reset. In FY25, we completed the planned exit from small series, non‑scalable business and the closure of the Tucson, Arizona site. Revenue of £2.2 million was recognised in FY25 in relation to products not transferred to other sites.

The business operates with two divisions, CTP and Speciality. The CTP division reported full year revenue, of £98.2 million (FY25: £107.0 million). The CTP division operates through with two revenue streams, Design and Engineering ("D&E") and Manufacturing Solutions ("MS"). MS revenue within CTP (excluding foreign exchange impacts and the site closures in FY25) was in line with the prior year, at £88.5 million (FY25: £93.4 million or £91.0 million on a constant currency basis, inclusive of £2.2 million exited and not transferred to other sites). Strong growth in China and Czechia was partially offset by lower revenues in India, due to reduced demand in customers' end markets. UK revenue was broadly in line with the prior year with US revenue 4% lower in local currency as we streamlined the product portfolio. The nature of D&E revenue is such that fluctuations in the level of annual revenues are not unusual, given it is project driven. Following the completion of significant D&E projects in prior years, which saw significant investment from long standing, established customers in specific projects, there has been lower activity during FY26, primarily in the US. Since these investment programs have concluded, focus has turned to ongoing regular business. Whilst there was an increase in the second half of FY26, the full year revenue for D&E was £3.8 million (28.2%) lower than FY25 at £9.7 million. During the year we worked on 193 projects, the majority of which we expect to convert into production contracts.

The Speciality Division reported full year revenue of £16.0 million (FY25: £14.2 million), an increase of 12.5%. Continued growth in Aerospace revenues, driven by increased demand as well as expanded precision machining capabilities, delivered a third consecutive year of record Aerospace sales. An analysis of divisional revenue and operating profit is provided in the table below.

£000

FY26

FY25

Change

Change %

CTP

MS revenue

88,487

93,443

(4,956)

-5.3%

D&E revenue

9,730

13,555

(3,825)

-28.2%

Total CTP revenue

98,217

106,998

(8,781)

-8.2%

Operating profit

15,089

12,373

2,716

+21.9%

Operating profit %

15.4%

11.6%

+3.8%

Speciality

Total Speciality revenue

15,994

14,221

1,773

+12.5%

Operating profit

3,584

2,801

783

+27.9%

Operating profit %

22.4%

19.7%

+2.7%

Group revenue

114,211

121,219

(7,008)

-5.8%

Central costs

(6,409)

(7,594)

1,185

-15.6%

Group operating profit

12,264

7,580

4,684

+61.8%

Group operating profit %

10.7%

6.3%

+4.5%

Our top five customers accounted for 70% of revenue (FY25: 68%) with tenure for these customers being on average 23 years. For our largest customer, we produced 25 different products. This demonstrates both the highly-regulated nature of the markets in which we operate as well as the depth of customer relationships underpinned by our excellent quality and delivery metrics.

Central costs were £1.2 million (15.6%) lower than the prior year, reflecting a £1.8 million reduction in refinancing costs to £0.3 million (FY25: £2.1 million), partially offset by continued investment in people and organisational capability.

During the year, the business submitted an insurance claim in respect of property damage incurred. Management considers recovery under the relevant insurance policies to be probable; however, due to the status of discussions and the claims assessment process, the amount and timing of any recovery cannot be estimated reliably at the reporting date. The claims assessment process is expected to progress during the second quarter of FY27.

Underlying operating profit

Despite the reduction in revenue, full year underlying operating profit increased substantially to £12.6 million (FY25: £9.8 million) as a result of the Group's margin expansion initiatives. Our key measure of ROS was 11.0% showing a significant increase from 8.1% in FY25. ROS during the second half of the year was 12.6% up from 9.6% in the first half, underlining the positive trajectory of margin growth.

The medium term target of achieving ROS of 10.0% was established in 2022, and the accomplishment of this target is directly related to the actions taken over the past three years to restructure the business, focussing on advanced process optimisation, increased asset utilisation and efficiency, improved pricing, better purchasing and a drive to reduce waste whilst demonstrating robust cost management.

Statutory operating profit and non-underlying items

The statutory operating profit for the year of £12.3 million was significantly better than the prior year (FY25: £7.6 million) as a result of the increased underlying operating profit and reduced non‑underlying charges.

Non-underlying items for the year were a net charge of £0.3 million comprising rationalisation and refinancing costs, being partially offset by net proceeds relating to the insurance claim previously mentioned. In FY25, the Group had £2.3 million of non-underlying costs, principally associated with the refinancing of the Group's borrowing facilities (see below).

Net finance expense

Net finance expense for FY26 was £7.4 million (FY25: £4.9 million). This includes two non-cash items: imputed net interest on the defined benefit pension liability of £2.7 million (FY25: £1.7 million) and amortised finance costs of £0.8 million (FY25: Nil) arising from the debt restructuring completed in April 2025. Bank and lease interest paid in the year is largely in line with FY25, reflecting the lower average net debt in the year, combined with a higher interest rate margin paid on the new debt facilities.

£000

FY26

FY25

Change

Interest payable on bank loans and overdrafts

2,923

3,075

(152)

Lease interest

458

679

(221)

Other finance costs

543

-

543

Interest receivable on cash and cash deposits

(46)

(571)

525

Total cash items

3,878

3,183

695

Amortised refinancing costs

843

-

843

Interest on the net defined benefit pension liability

2,711

1,745

966

Total non-cash items

3,554

1,745

1,809

Total finance expense

7,432

4,928

2,504

Taxation, profit after tax and earnings per share

The income tax charge for the year was £2.1 million (FY25: £1.8 million), representing an effective tax rate of 44.2% (FY25: 67.1%). The effective tax rate varies depending upon the geographical source of profits, corporation tax rates in the countries where profits are generated as well as the availability of local allowances including the carry forward of prior year losses. The Group's effective tax rate in FY26 is higher than the UK corporation tax rate of 25% due to a movement in unprovided UK deferred tax assets (£787k) largely losses in the UK which are not recognised for deferred tax purposes and withholding tax (£265k) incurred on the repatriation of funds to the UK from certain overseas jurisdictions.

Alternative performance measures

Statutory profit after tax was £2.7 million (FY25: £0.9 million), giving statutory earnings per share of 3.7 pence (FY25: 1.2 pence). Underlying profit after tax was £3.0 million (FY25: £3.1 million), giving underlying earnings per share of 4.1 pence (FY25: 4.3 pence). The underlying earnings per share is impacted negatively by non-cash interest charges.

In the analysis of the Group's financial performance, position, operating results and cash flows, alternative performance measures are presented to provide readers with additional information. The principal measures presented are underlying measures of earnings including underlying operating profit, underlying profit before tax, underlying profit after tax, underlying EBITDA and underlying earnings per share.

This results statement includes both statutory and adjusted non-GAAP financial measures, the latter of which the Directors believe better reflect the underlying performance of the business and provides a more meaningful comparison of how the business is managed and measured on a day‑to‑day basis. The Group's alternative performance measures and KPIs are aligned to the Group's strategy and together are used to measure the performance of the business and form the basis of the performance measures for remuneration. Underlying results exclude certain items because, if included, these items could distort the understanding of the performance for the year and the comparability between the periods.

A reconciliation of the Group's non-GAAP financial measures is shown in the section "Information for shareholders".

Comparatives are provided alongside all current year figures. The term "underlying" is not defined under IFRS and, as such, the underlying measures reported may not be comparable with similarly titled measures used by other companies.

All profit and earnings per share figures relate to underlying business performance, as defined above, unless otherwise stated. A reconciliation of underlying measures to statutory measures for FY26 is provided below:

£000

Underlying

Non-underlying items

Statutory

CTP operating profit

15,101

(12)

15,089

Speciality operating profit

3,424

160

3,584

Central costs

(5,925)

(484)

(6,409)

Group operating profit

12,600

(336)

12,264

Net finance expense

(7,432)

-

(7,432)

Group profit/(loss) before taxation

5,168

(336)

4,832

Taxation expense

(2,146)

(9)

(2,137)

Group profit/(loss) for the year

3,022

(327)

2,695

Basic profit/(loss) per share (pence)

4.1p

(0.4)p

3.7p

The non-underlying items reported in the Group profit/(loss) before taxation comprise:

£000

FY26

FY25

Refinancing costs

(270)

(2,137)

Rationalisation costs

(225)

(122)

Net proceeds of insurance claim

159

-

Settlement of legacy health claims

-

1

Total non-underlying items

(336)

(2,258)

Cash flow

Cash generated from operations was £12.0 million (FY25: £19.1 million) reflecting the continued focus on cash generation via operational improvements and capital expenditure management. The full year cash conversion rate was 65.6% (FY25:135.0%).

Following the significant working capital cash inflow in FY25 (£5.8 million), FY26 saw a working capital outflow of £6.3 million. This was due to a significant change in provisions and accruals when compared to the prior year, along with a change in some customer payment terms associated to the Group's new financing arrangements. The movement in accruals arises from the specific requirement for accrued costs (mainly energy and employee benefit costs) at FY25 that have unwound during FY26, resulting in a working capital outflow for the year. Inventory levels increased by £1.1 million when compared to FY25, with slightly higher levels of raw materials being held in light of current economic conditions. Working capital was at a level of 9.7% of revenue during FY26, with further pressure on this ratio foreseen during the coming year with an expected increase of 100-150 bps over FY26. Net cash outflow from investing activities during the year was £2.8 million (FY25: £0.4 million). There has been continued careful control of capital expenditure, focusing on those investments that deliver a rapid payback and support both asset performance and asset utilisation. Additions to tangible fixed assets in the year were £3.4 million (FY25: £2.4 million) of which £0.8 million (FY25: £1.4 million) was through right-of-use leased assets.

Substantial capital expenditure in previous years and more efficient use of assets, driven by operational improvements, has reduced the required level of capital investment in the last two years. This is reflected in the value of tangible fixed assets and increased asset utilisation rate of 3.5x (FY25: 3.4x) over this period.

Net cash outflow from financing activities during the year was £5.6 million (FY25: £7.0 million), comprising £3.0 million repayment of lease liabilities (FY25: £4.2 million) and net repayment of other borrowings of £2.6 million (FY25: £2.8 million). There was an overall £4.2 million decrease in cash and cash equivalents during the year (FY25: increase of £4.0 million).

Cash generated by the Group was principally utilised to make capital investment and lease repayments, pension deficit contributions, scheduled bank loan repayments and interest payments. The Group's full cash flow statement is set out in the statements below.

Financial position

Net debt

Net debt as at 31 March 2026 was £23.9 million, an increase of £4.7 million compared to the prior year (FY25: £19.2 million). This reflects the one-off pension scheme contribution of £5.1 million made in April 2025 at the time of finalising the Group's refinancing, along with the annual contribution of £3.5 million, together with a working capital outflow. The Group's focus remains on operational improvements, cash generation and the prudent management of borrowings.

Net debt comprised gross debt, from borrowings and leases, of £29.7 million (FY25: £29.9 million) less cash and cash equivalents of £5.8 million (FY25: £10.7 million). The gross borrowings reflect the current financing arrangements, along with outstanding leases of £4.9 million after lease repayments in the year of £3.0 million.

Borrowing facilities

On 24 April 2025, the Group refinanced its primary external borrowing arrangements through a three-year multi-currency facility with BZ Commercial Finance DAC ("BZ"), comprising a £27.0 million term loan and a revolving credit facility ("RCF") of up to £9.0 million.

On inception, £29.9 million was drawn under the BZ facility, comprising £26.8 million under the term loan and £3.1 million under the RCF. The proceeds were used to discharge all amounts outstanding under the Group's previous borrowing arrangements with HSBC, make a one-off £5.1 million contribution to the Group's defined benefit pension scheme and provide funding to support ongoing operations.

The facility includes an asset-based lending arrangement under which borrowings are permitted against specified classes of assets held by the Group's UK and US businesses. Of the £27.0 million term loan, £8.0 million is supported by owned land and buildings, £5.0 million by owned plant and machinery, and the remaining £14.0 million comprises a non-asset-specific cash flow loan. Of the £9.0 million RCF, up to £7.0 million is available against eligible trade receivables and up to £2.0 million against eligible inventory.

The facility permits borrowings in GBP, EUR and USD. Carclo plc, Carclo Technical Plastics Limited and Bruntons Aero Products Limited are currently authorised borrowers under the facility. Cross-guarantees are provided by the authorised borrowers and other material subsidiaries, as defined in the facility agreement.

As at 31 March 2026, £24.9 million remained outstanding under the term loan following repayments of £1.9 million during the year. There were no drawings under the RCF at the year end, leaving available headroom of £9.0 million, subject to applicable borrowing base limitations.

Defined benefit pension scheme

The triennial actuarial valuation of the Group's UK defined benefit pension scheme at 31 March 2024 was completed during April 2025. The valuation, prepared by the Scheme Trustees on a technical provisions basis, reported a deficit of £64.5 million, a significant reduction from the £82.8 million liability reported as part of the previous triennial valuation of 31 March 2021.

On a technical provisions basis, the estimated net liability has fallen steadily each year from 2021 as a result of the Company settled cash contributions and the gross liabilities falling by more than the change in pension scheme asset values. The 31 March 2024 valuation reflected higher government bond yield rates, driving up the discount rate and reducing scheme liabilities, partially offset by an increase in assumed member life expectancy, which increased Scheme liabilities.

A deficit recovery plan was agreed with the Trustees in parallel with the refinancing arrangements finalised in April 2025. This includes a lump sum one off payment into the Scheme of £5.1 million made at the time of finalisation of refinancing in April 2025 and annual contributions of £3.5 million for five years to 31 March 2029 followed by annual contributions of £5.8 million, which are inflationary indexed annually until 31 March 2037, being 2 years earlier than the deficit recovery plan from the 31 March 2021 valuation. During FY26, total contributions paid into the Scheme were £8.6 million (FY25: £3.2 million).

Since the completion of the 2024 triennial valuation, the estimated technical provisions deficit has fallen further to £52.9 million at 31 March 2026.

The IAS 19 valuation of the Scheme liabilities at 31 March 2026 resulted in a net liability of £46.7 million, a £5.0 million decrease from the net liability at 31 March 2025 (FY25: £51.7 million). The principal driver of the decrease in the IAS 19 net liability was company contributions, alongside relatively smaller gains on scheme assets (£0.4 million) and a net reduction in liability arising from changes in assumptions and experience losses (£0.2 million).

The IAS 19 valuations are adopted for statutory reporting purposes and do not form part of the ongoing management of the pension schemes. IAS 19 actuarial calculations can be volatile from year‑to-year because the liabilities are measured by reference to corporate bond yields, whereas the majority of the pension scheme's assets are invested across a variety of asset classes that may not move in the same way. Gain on scheme assets in excess of interest income during FY26 totalled £0.4m and was mostly driven by the decrease in the value of the Scheme's liability-driven investment funds ("LDI").

These LDI funds are designed to hedge movements in liabilities due to changes in interest rates and inflation expectations. As interest rates have increased across the accounting period, the value of the LDI funds have decreased accordingly. The liability calculated under technical provisions includes more prudent assumptions, but at any time, provides a more accurate reflection of the longer term cash commitment required to settle the member liabilities. The actuarial gains and losses arising from variances against previous actuarial assumptions are recognised in the statement of financial position with corresponding movements in reserves.

The Company and the Scheme Trustees are committed to working collaboratively towards reducing the Scheme deficit.

Treasury

The Group faces currency exposure on its overseas subsidiaries and on its foreign currency transactions. In addition, as set out in the principal risks and uncertainties section of the annual report and accounts, the Group is reliant on regular funding flows from the overseas subsidiaries to meet banking, pension and administrative commitments.

To manage this complexity, the Group has a centralised Treasury function that manages the Group's cash, debt and foreign exchange risks.

The Group reports trading results of overseas subsidiaries based on average rates of exchange compared with sterling over the year. This income statement translation exposure is not hedged as this is an accounting rather than cash exposure and, as a result, the income statement is exposed to movements in the US dollar, euro, renminbi, Czech koruna and Indian rupee. In terms of sensitivity, based on the FY26 results, a 10% increase in the value of sterling against these currencies would have decreased reported profit before tax by £0.7m.

Dividend

Under the BZ borrowing facility agreement, dividend payments are permitted, but they require prior approval of the lender.

The current focus is on cash flow generation to support strategic growth and as such no dividend is proposed in respect of the year ended 31 March 2026. The Board will continue to review the Group financial performance, capital allocation and reserves regularly to determine the appropriate time for dividend payments.

Accounting policies

The Group's annual consolidated financial statements are prepared in accordance with UK-adopted International Accounting Standards and with the requirements of the Companies Act 2006. There have been no significant changes to the Group's accounting policies during the period.

Post balance sheet events and going concern

Post balance sheet events

There are no post balance sheet events to report.

Going concern

A £36m asset-backed borrowing facility with BZ, that was announced on 24 April 2025, provides available borrowings for a three-year term to April 2028. The level of borrowings is contingent upon the value of current and non-current asset categories held by the Group's UK and US trading subsidiaries.

There are three primary financial covenants required to be tested under the BZ facility agreement as follows:

The Group remained compliant with the Minimum EBITDA and FCCR financial covenants throughout the year ended 31 March 2026. In accordance with the facility agreement, these covenants were tested monthly from May 2025 and, following twelve months of compliance under the agreement, including compliance in the two preceding quarters, testing has moved to a quarterly basis. The CAPEX covenant is tested annually from the start of each reporting period.

The Group has prepared a forecast of financial projections for the three-year period to 31 March 2029, which has been utilised as the base case underpinning the going concern assessment for the period through to June 2027, being 15 months after the year end and 12 months from when the financial statements are authorised for issue. These projections include assumptions around revenue growth, modest margin improvements, consistent working capital trends and stable interest rates. The Directors have reviewed cash flow and covenant forecasts over this period considering the Group's available borrowing facilities and the terms of the arrangements with the Group's lender and the UK defined benefit pension scheme. The forecast shows adequate headroom and supports the position the Group can operate within its available borrowing facilities and in compliance with covenants throughout this period.

The Group is subject to a number of key risks and uncertainties, as detailed in the principal risks and uncertainties section on pages 42 to 48 of the Annual Report. Mitigating actions to address the risks are also set out in that section of the report. These risks and uncertainties have been considered in the base case, and downside sensitivities and have been modelled accordingly. These sensitivities consider the uncertainties facing the Group and model the impact of a range of severe but plausible downside scenarios, as well as considering the impact of aggregating certain of these, and shows that the Group would be able to operate within its available facilities and meet its agreed covenants were these scenarios to arise.

The specific climate-related matters set out in the TCFD section on pages 33 to 41 of the Annual Report have been considered and they are not expected to have a significant impact on the Group's going concern.

The severe but plausible downside sensitivities modelled included reductions in forecast revenue of up to 6.6%, a 4% increase in direct material costs (equivalent to approximately 2.2% contribution margin erosion) and a 2% increase in interest rates. The downside scenario modelling assumes management bonuses are not payable where the relevant performance conditions are not achieved but does not include the benefit of any other mitigating actions available to management.

Under each of the standalone downside scenarios modelled, the Group maintains adequate liquidity throughout the assessment period and remains compliant with all financial covenants. The Directors also assessed a combined downside scenario incorporating both a significant reduction in forecast revenue and a sustained increase in direct material costs. Under this combined scenario, no liquidity shortfall arises; however, there is a temporary breach of the FCCR covenant. The Directors consider the concurrent occurrence of these downside assumptions to be remote. Furthermore, the scenario does not reflect a range of mitigating actions available to management, including the reduction of discretionary expenditure and the deferral of non-essential capital expenditure. Modelling performed by management demonstrates that actions considered achievable and within management's control would be sufficient to restore covenant compliance under this scenario.

Given that FCCR represented the most sensitive covenant within the Group's financing arrangements, the Directors performed additional covenant-focused downside testing, including scenarios in which EBITDA remained broadly flat against FY26 levels and reduced by 10% compared with FY26. While these scenarios resulted in reduced covenant headroom, management identified specific mitigating actions that are considered achievable and within management's control and which would be sufficient to maintain compliance with the Group's covenant requirements.

The Group is not exposed to high-risk sectors or countries but is dependent on certain key customers, creating risks and uncertainties, which are documented in detail alongside mitigating actions in the principal risks and uncertainties section.

It should be noted that the Group is operating in a period of material geopolitical and macroeconomic uncertainty. The Directors continue to monitor these risks and their plausible impact; however, the potential severity is dependent upon many external factors and is difficult to predict. Accordingly, the financial impact of these risks may materially differ from the Directors' current view.

At 31 March 2026, the Group reports net liabilities of £8.7 million (FY25: £11.8 million net liabilities) largely attributable to the IAS 19 valuation of the UK defined benefit pension liability of £46.8 million (FY25: £51.8 million). Pension contributions are funded from cash generated by operations and have been reflected in the cash flow and covenant forecasts reviewed by the Directors. Given that these amounts are considered manageable by the Directors, the balance sheet presentation of net liabilities at 31 March 2026 does not imply an inability for the Group to meet its third-party liabilities over the going concern period.

On the basis of the base case forecast and the severe but plausible sensitivity testing, the Directors have determined that it is reasonable to assume that the Group will continue to operate within available borrowing facilities available and adhere to the covenant tests to which it is subject throughout at least the 12 month period from the date of signing the financial statements through to June 2027.

Accordingly, these financial statements are prepared on a going concern basis.

Ian Tichias

Chief Financial Officer

30 June 2026

Consolidated income statement

for the year ended 31 March 2026

Notes

2026

£000

2025

£000

Revenue

114,211

121,219

Underlying operating profit

3

12,600

9,838

Non-underlying items

4

(336)

(2,258)

Operating profit

3, 6

12,264

7,580

Finance revenue

5

46

571

Finance expense

5

(7,478)

(5,499)

Profit) before tax

4,832

2,652

Income tax

6

(2,137)

(1,780)

Profit for the year

2,695

872

Attributable to:

Equity holders of the Company

2,695

872

Non-controlling interests

-

-

Equity holders of the Company

2,695

872

Profit per ordinary share

Basic

13

3.7p

1.2p

Diluted

13

3.6 p

1.2p

Consolidated statement of comprehensive income

for the year ended 31 March 2026

Notes

2026

£000

2025

£000

Profit for the year

2,695

872

Other comprehensive income/(expense)

Items that will not be reclassified to the income statement

Remeasurement losses on defined benefit pension scheme

12

51

(15,253)

Deferred tax arising

-

-

Total items that will not be reclassified to the income statement

51

(15,253)

Items that may in the future be reclassified to the income statement

Foreign exchange translation gain/(losses)

506

(955)

Net investment hedge

(141)

371

Deferred tax arising

(1)

13

Total items that may in the future be reclassified to the income statement

364

(571)

Other comprehensive income/(expense), net of tax

415

(15,824)

Total comprehensive income/(expense) for the year

3,110

(14,952)

Attributable to:

Equity holders of the Company

3,110

(14,952)

Equity holders of the Company

3,110

(14,952)

Consolidated statement of financial position

as at 31 March 2026

Notes

2026

£000

2025

£000

Non-current assets

Intangible assets

9

22,531

21,801

Property, plant and equipment

10

32,247

35,842

Deferred tax assets

83

641

Contract assets

74

170

Trade and other receivables

540

594

Total non-current assets

55,475

59,048

Current assets

Inventories

11,029

9,928

Contract assets

1,742

1,551

Trade and other receivables

18,347

15,659

Cash and cash deposits

14

5,769

10,745

Current tax assets

-

104

Total current assets

36,887

37,987

Total assets

92,362

97,035

Current liabilities

Loans and borrowings

11

7,568

24,844

Trade payables

10,250

9,697

Other payables

7,705

11,094

Current tax liabilities

442

752

Contract liabilities

1,737

1,624

Total current liabilities

27,702

48,011

Non-current liabilities

Loans and borrowings

11

22,108

5,105

Deferred tax liabilities

3,467

3,041

Provisions

969

975

Retirement benefit obligations

12

46,785

51,743

Total non-current liabilities

73,329

60,864

Total liabilities

101,031

108,875

Net (liabilities)/assets

(8,669)

(11,840)

Equity

Ordinary share capital issued

13

3,671

3,671

Share premium

7,359

7,359

Translation reserve

7,014

6,650

Retained earnings

(26,687)

(29,494)

Total equity attributable to equity holders of the Company

(8,643)

(11,814)

Non-controlling interests

(26)

(26)

Total equity

(8,669)

(11,840)

Approved by the Board of Directors on 30 June 2026 and signed on its behalf by:

Frank Doorenbosch Ian Tichias

Chief Executive Officer Chief Financial Officer

Registered Number 00196249

Consolidated statement of changes in equity

for the year ended 31 March 2026

Attributable to equity holders of the Company

Notes

Share capital £000

Share premium £000

Translation reserve £000

Retained earnings £000

Total £000

Non-controlling interests £000

Total equity £000

Balance at 31 March and 1 April 2024

3,671

7,359

7,221

(15,135)

3,116

(26)

3,090

Profit for the year

-

-

-

872

872

-

872

Other comprehensive income/(expense):

Foreign exchange translation differences

-

-

(955)

-

(955)

-

(955)

Net investment hedge

-

-

371

-

371

-

371

Remeasurement losses on defined benefit pension scheme

10

-

-

-

(15,253)

(15,253)

-

(15,253)

Taxation on items above

-

-

13

-

13

-

13

Total comprehensive expense for the year

-

-

(571)

(14,381)

(14,952)

-

(14,952)

Transactions with owners recorded directly in equity:

Share-based payments

11

-

-

-

22

22

-

22

Balance at 31 March and 1 April 2025

3,671

7,359

6,650

(29,494)

(11,814)

(26)

(11,840)

Profit for the year

-

-

-

2,695

2,695

-

2,695

Other comprehensive income/(expense):

Foreign exchange translation differences

-

-

506

-

506

-

506

Net investment hedge

-

-

(141)

-

(141)

-

(141)

Remeasurement losses on defined benefit pension scheme

10

-

-

-

51

51

-

51

Taxation on items above

-

-

(1)

-

(1)

-

(1)

Total comprehensive expense for the year

-

-

364

2,746

3,110

-

3,110

Transactions with owners recorded directly in equity:

Share-based payments

11

-

-

-

61

61

-

61

Balance at 31 March 2026

3,671

7,359

7,014

(26,687)

(8,643)

(26)

(8,669)

Consolidated statement of cash flows

for the year ended 31 March 2026

Notes

2026

£000

2025

£000

Cash generated from operations

14

11,993

19,066

Interest paid

(3,924)

(3,694)

Tax paid

(1,406)

(1,259)

Defined benefit pension scheme contributions net of Company-settled administration costs

(2,518)

(2,633)

Net cash from operating activities

4,145

11,480

Cash flows from/(used in) investing activities

Proceeds from sale of property, plant and equipment

36

85

Interest received

46

571

Purchase of property, plant and equipment

(2,522)

(1,054)

Purchase of intangible assets

(333)

(49)

Net cash used in investing activities

(2,773)

(447)

Cash flows used in financing activities

11

Drawings on existing and new facilities

29,911

-

Refinancing costs associated with the new facility

(2,544)

(150)

Additional defined benefit pension scheme contributions paid to release security for new financing facility

(5,100)

-

Repayment of borrowings excluding lease liabilities

(24,870)

(2,525)

Repayment of other loan facilities

-

(95)

Repayment of lease liabilities

(2,973)

(4,228)

Net cash used in financing activities

(5,576)

(6,998)

Net increase/(decrease) in cash and cash equivalents

(4,204)

4,035

Cash and cash equivalents at beginning of year

9,980

5,974

Effect of exchange rate fluctuations on cash held and cash equivalents

(7)

(29)

Cash and cash equivalents at end of year

5,769

9,980

Cash and cash equivalents comprise:

Cash and cash deposits

5,769

10,745

Bank overdrafts

-

(765)

5,769

9,980

Notes to the consolidated financial statements

for the year ended 31 March 2026

1 Presentation of the financial statements

i) General information

Carclo plc (the "Company", together with its subsidiaries, the "Group") is a public limited company whose shares are listed on the London Stock Exchange, is incorporated and domiciled in the UK and is registered in England under the Companies Act 2006.

The principal activities of the Company and its subsidiaries (the "Group") and the nature of the Group's operations are set out in note 3.

The financial statements are presented in sterling, which is Carclo plc's functional and presentational currency. Certain Group subsidiary entities have functional currencies other than sterling. The financial position and performance of all such subsidiary entities is translated into the presentational currency (sterling) in accordance with the foreign currencies accounting policy as detailed within the accounting policy section of this note. All amounts disclosed in the financial statements and notes have been rounded off to the nearest thousand pounds unless otherwise stated.

Judgements made by the Directors in the application of these accounting policies that have a significant effect on the financial statements and estimates with a significant risk of material adjustment in the next year are discussed in note 2.

ii) Compliance with IFRS

The consolidated financial statements have been prepared and approved by the Directors in accordance with UK-adopted International Accounting Standards and with the requirements of the Companies Act 2006.

The accounting policies have been applied consistently to all periods presented in the consolidated financial statements, unless otherwise stated.

iii) Going concern

A £36 million asset-backed borrowing facility with BZ, that was announced on 24 April 2025, provides available borrowings for a three-year term to April 2028. The level of borrowings is contingent upon the value of current and non-current asset categories held by the Group's UK and US trading subsidiaries.

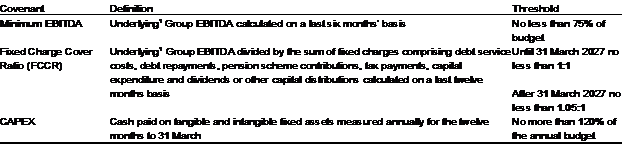

There are three primary financial covenants required to be tested under the BZ facility agreement as follows:

Covenant

Definition

Threshold

Minimum EBITDA

Underlying Group EBITDA calculated on a last six months basis

No less than 75% of budget

Fixed Charge Cover Ratio ("FCCR")

Underlying Group EBITDA divided by the sum of fixed charges comprising debt service costs, debt repayments, pension scheme contributions, tax payments, capital expenditure and dividends or other capital distributions calculated on a last twelve months basis

Until 31 March 2027 no less than 1:1

After 31 March 2027 no less than 1.05:1

CAPEX

Cash paid on tangible and intangible fixed assets measured annually for the twelve months to 31 March

No more than 120% of the annual budget

The Group remained compliant with the Minimum EBITDA and FCCR financial covenants throughout the year ended 31 March 2026. In accordance with the facility agreement, these covenants were tested monthly from May 2025 and, following twelve months of compliance under the agreement, including compliance in the two preceding quarters, testing has reverted to a quarterly basis. The CAPEX covenant is tested annually from the start of each reporting period.

The Group has prepared a forecast of financial projections for the three-year period to 31 March 2029, which has been utilised as the base case underpinning the going concern assessment for the period through to June 2027, being 15 months after the year end and 12 months from when the financial statements are authorised for issue. These projections include assumptions around revenue growth, modest margin improvements, consistent working capital trends and stable interest rates. The Directors have reviewed cash flow and covenant forecasts over this period considering the Group's available borrowing facilities and the terms of the arrangements with the Group's lender and the UK defined benefit pension scheme. The forecast shows adequate headroom and supports the position the Group can operate within its available borrowing facilities and in compliance with covenants throughout this period.

The Group is subject to a number of key risks and uncertainties, as detailed in the principal risks and uncertainties section in the annual report and accounts. Mitigating actions to address the risks are also set out in that section of the report. These risks and uncertainties have been considered in the base case, and downside sensitivities have been modelled accordingly. These sensitivities consider the uncertainties facing the Group and model the impact of a range of severe but plausible downside scenarios, as well as considering the impact of aggregating certain of these, and shows that the Group would be able to operate within its available facilities and meet its agreed covenants were these scenarios to arise.

The specific climate-related matters set out in the TCFD section in the annual report and accounts have been considered and they are not expected to have a significant impact on the Group's going concern.

The severe but plausible downside sensitivities modelled included reductions in forecast revenue of up to 6.6%, a 4% increase in direct material costs (equivalent to approximately 2.2% contribution margin erosion) and a 2% increase in interest rates. The downside scenario modelling assumes management bonuses are not payable where the relevant performance conditions are not achieved but does not include the benefit of any other mitigating actions available to management.

Under each of the standalone downside scenarios modelled, the Group maintains adequate liquidity throughout the assessment period and remains compliant with all financial covenants.The Directors also assessed a combined downside scenario incorporating both a significant reduction in forecast revenue and a sustained increase in direct material costs. Under this combined scenario, no liquidity shortfall arises; however, there is a temporary breach of the FCCR covenant. The Directors consider the concurrent occurrence of these downside assumptions to be remote. Furthermore, the scenario does not reflect a range of mitigating actions available to management, including the reduction of discretionary expenditure and the deferral of non-essential capital expenditure. Modelling performed by management demonstrates that actions considered achievable and within management's control would be sufficient to restore covenant compliance under this scenario.

Given that FCCR represented the most sensitive covenant within the Group's financing arrangements, the Directors performed additional covenant-focused downside testing, including scenarios in which EBITDA remained broadly flat against FY26 levels and reduced by 10% compared with FY26. While these scenarios resulted in reduced covenant headroom, management identified specific mitigating actions that are considered achievable and within management's control and which would be sufficient to maintain compliance with the Group's covenant requirements.

The Group is not exposed to high-risk sectors or countries but is dependent on certain key customers, creating risks and uncertainties, which are documented in detail alongside mitigating actions in the principal risks and uncertainties section.

It should be noted that the Group is operating in a period of material geopolitical and macroeconomic uncertainty. The Directors continue to monitor these risks and their plausible impact; however, the potential severity is dependent upon many external factors and is difficult to predict. Accordingly, the financial impact of these risks may materially differ from the Directors' current view.