Core QVM - the strategy for the rational investor

We now come to the last of eight articles in our series on “The Strategy Map”, to explore an approach that sits at the centre of it all, with the aim of owning good, cheap, strong stocks. When everyone seems to know more than you about every stock out there, it’s easy to feel intimidated. There are brilliant minds on Twitter, brilliant minds in Stockopedia’s community, an industry of armchair and professional analysts poring over every company’s every move. How can you possibly find a stock picking edge?

You can, of course, outwork everyone, but it often seems like an exhausting endeavour. You could piggy-back on other’s ideas, but the shallowness of your own research can niggle and worry. The time-poor investor, with a desire to DIY, faces a conundrum. How can you run a successful portfolio without becoming a full-time analyst?

The answer lies in knowing the “base rates” of what pays off and why in the stock market. In this article we’ll be exploring how the stock market really works, why it rewards quality, value and momentum stocks (Q+V+M = QVM) and how you can construct a portfolio to harvest their rewards.

At the heart of this lie a few ideas that upend conventional thinking. Will you stay with the blue pill of ordinary reality, or take the red pill and follow me down the rabbit hole?

Is this right for you?

The kinds of stocks that qualify for a QVM approach are often rather dull, even if their returns can be anything but. As this strategy blends the best of quality, value and momentum, the kinds of stocks listed are varied. But as some lie at extremes, they can generate a range of psychological reactions:

Quality - good stocks are often rather dull. It’s controversial perhaps, but most novice stock pickers want exciting stories. You don’t always find excitement in steadily profitable companies. Can you really say no to the glamorous story stocks that all your friends are convinced will triple their money in bull markets?

Value - cheap stocks come with problems - they may be cheap for a reason. Stumbling profits, competitive issues, staff issues, sector obsolescence you name it. Can you really swallow a frog?

Momentum - strong stocks come with high prices - nobody likes buying stocks at highs. We’re programmed to do the inverse. Can you undo your innate programming and buy shares breaking out to new highs?

Beyond this, lists of high QVM stocks can often contain a few off-putting sectors. Cyclicals, basic materials, even sin stocks. If you want to save the planet and invest for good then some of these shares may not fit you. Sure you may be able to avoid the more unsavoury stocks in the lists if you want to keep a clean conscience, but you may well be guaranteeing average returns or worse if you do. There are easier ways to do so (like investing in ESG funds) but it’s not for me.

You’ll also need to be willing to stomach periods of underperformance. This strategy is based not upon fashion, fads or funks… it’s based on the perennial returns to “factors” - the true underlying return drivers in the stock market.

Over time, the stock market is rational. It rewards good quality stocks that reinvest their profits, it revalues cheap stocks upwards as they repair their business models, and it gradually recognises the information in new trends. These factors drive share prices upwards.

Whether you are an investor with a more statistical bent, or a stock picker seeking businesses in the “sweet spot” there’s something for you to learn from QVM. But there is a catch…

Background to combining Quality, Value and Momentum

When I started investing, I learned all I could about financial data and stock screening. Databases were just being made more broadly available on the internet. I read Jim Slater’s Zulu Principle and subscribed to the product launched based on his ideas - Company REFS - in fact, I loved it so much we eventually acquired its subscription business. It seemed to make finding profitable, reasonably priced, up-trending shares that much simpler. But his ideas at times seemed anecdotal, rather than statistically rigorous.

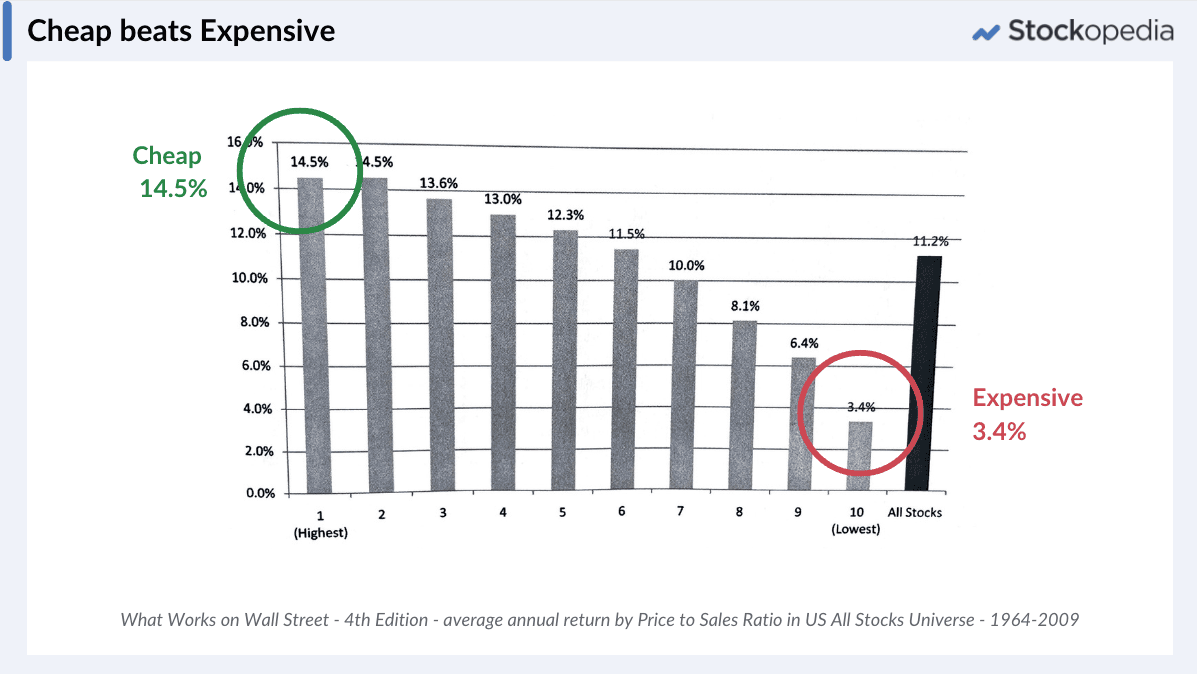

O’Shaughnessy’s “What Works on Wall Street” was the first accessible bible of financial data. He illustrated that portfolios of cheap stocks tended to beat portfolios of expensive stocks. The scan from his book below shows a 14.5% return to the cheapest stocks, versus a 3.4% return to the most expensive. Great validation for value investors.

Across nearly 700 pages he also showed that profitable stocks beat unprofitable stocks, that strong stocks beat losing stocks and so on. The statistics in the book outlined the "base rate"returns to groups of shares that displayed these traits - you can think of them as batting averages. He proposed combining these traits into “multi-factor” strategies and tested them against each other.

The catch - it’s impossible to screen for the perfect stock

But O’Shaughnessy’s strategies were simplistic. If you try to screen for more than a few rules at a time you come upon a really common problem and herein lies “the catch”. It’s almost impossible to find the perfect stock that combines all the best traits. The more rules you screen on, the less stocks you find.

In summary, everyone else is looking for the perfect stock too - so you won’t be able to find one. Screening for low valuation, high profitability, good growth, maybe paying dividends, not too much debt, maybe a good share price trend - you’ll be lucky to find any shares at all. As soon as any stock gets anywhere near qualifying for those rules, other investors have already bought it. The market is quite efficient.

So what most investors focus on is qualitative analysis. You can use much broader starting screens or checklists, and then go through the companies one by one, assessing business models, industries, management and more. It’s a time-proven, but laborious process for seeking investment winners.

Warren Buffett does it like this (“we start at the As”), and frankly, he’s proven pretty good at it. In some regards, you could say that Warren Buffett is the greatest QVM investor who has ever lived. Back in 2016 he started buying Apple - which had a StockRank of 86 at the time - making probably the most profitable trade of all time. He’s now up more than 7x on his original multi-billion dollar stake.

Of course, we aren’t all Warren Buffett, and while he makes it seem easy, it’s harder in practice, especially if you are a time poor investor. How many of us bought Apple only to sell when it got too expensive?

Professor Robert Haugen’s solution

A little book called “The Inefficient Stock Market” by the late Professor Robert Haugen is a tough read, but absolutely boggled my mind when I first read it. Haugen described the “ideal profile” of a stock as ”big, financially sound, low risk, momentum in the market, profitable in every dimension, and becoming more profitable in every way, yet selling at dirt-cheap market prices”.

He called this mythical beast the “Super Stock”.

Of course, he couldn’t find them through direct screening either. Going on Haugen said:

Super stocks go around disguised as mild mannered securities. Each has one or more components of the [ideal] profile, but not the whole thing. It’s only when Super Stocks are assembled into a portfolio that they remove their eyeglasses and reveal their true identities.

He realised he could construct portfolios of these stocks that had enough of these traits on average. He described this process as going directly to investment heaven.

The benefits of ranking over screening

Haugen’s approach to finding these shares is common in institutional circles, but a little complicated - and apologies if the next sentence goes over a few heads. Essentially, he’d calculate the expected return for each stock by regressing the performance of all stocks against a range of technical and fundamental characteristics (like quality, value and momentum).

While that approach is complicated, the more simple approach of simultaneously ranking stocks for the same multiple measures has been proven just as effective. This can be done in a spreadsheet program, and is the approach we’ve taken in constructing the StockRanks at Stockopedia. Every stock gets a standardised score (we use percentiles between zero and 100) which provides easy comparison.

If you were to just rank the market for a single measure, like the P/E ratio, you see only mild benefits over using a simple cutoff. For example, in the UK, there are 74 stocks ranking in the top 10% of cheapness, which is equivalent to screening for a P/E cutoff of less than 4.2.

But when you combine all the ranks for many measures into a single “composite” something magic happens. In the top 10% of all stocks for a QVM ranking (i.e. the StockRank), you have a pool of shares that have, as Haugen would put it, “one or more of the components of the [ideal] profile, but not the whole thing”.

This approach allows you to discover shares with good return prospects (on average), that the majority of investors can’t find when they screen for them directly.

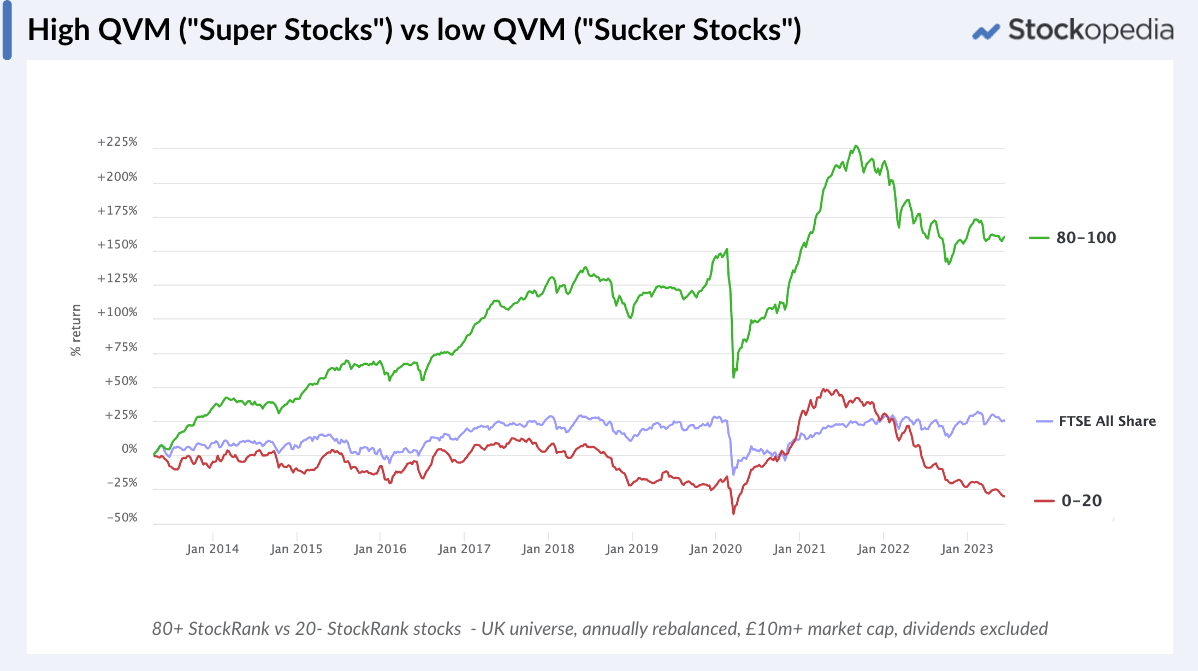

Haugen’s work not only inspired our own StockRank system, but also our Style classifications of “Super Stocks” and “Sucker Stocks”. With now more than 10 years of history in ranking the stock market ourselves, we provide further validation of the effectiveness of these principles.

I’m still amazed that I can construct a portfolio of shares using the StockRanks that, on average, have the characteristics of a share that can’t be found when screening for it directly. (Do read this article for more details).

In this way, you can synthesise the perfect stock as a portfolio, when the perfect stock itself can’t be found. This may not be mind-bending for you, but it always has been for me.

Making sure some of your stocks zig when the others zag

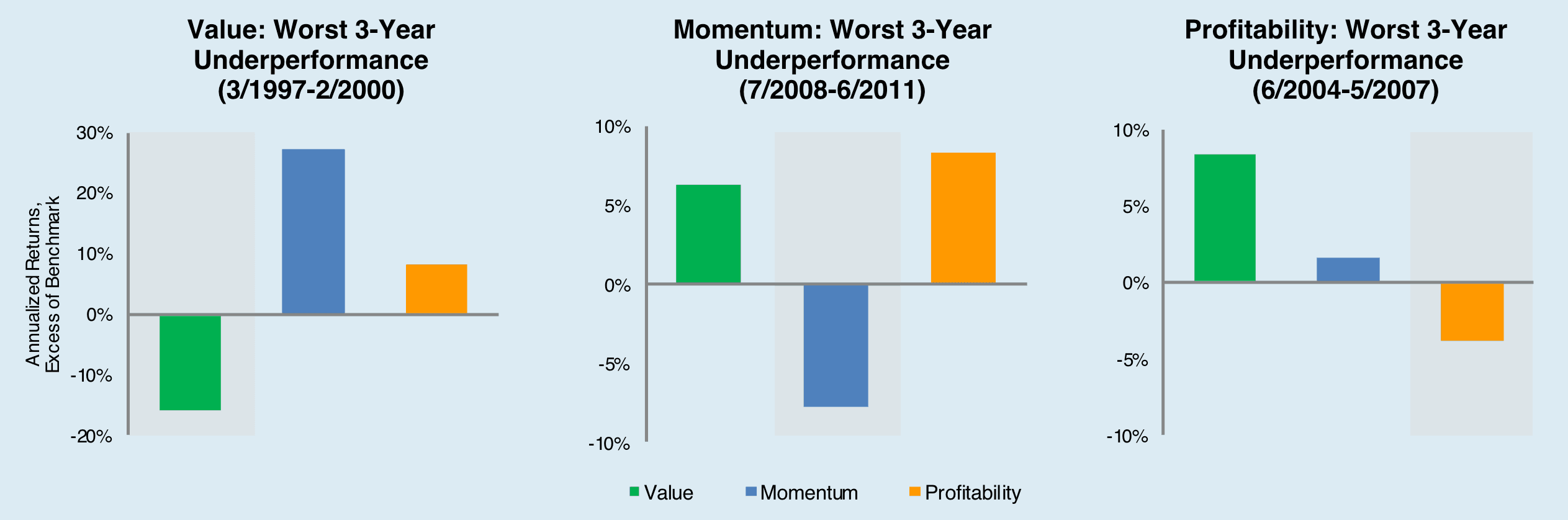

The great benefit of owning a mix of stocks, where some lean to value, some to momentum and so on, is that some of the portfolio may outperform when other parts struggle. A great paper “A New Core Equity Paradigm” by Cliff Asness et al, highlights the benefits of the core “QVM” style approach. The worst performing periods for each “factor” always come in different market cycles.

If you are committed to just a single segment on the edge of the Strategy Map (such as Deep Value, Breakout Momentum, or Compounding Quality) you may suffer significant periods of underperformance. While a Core QVM approach will have its moments of underperformance too, they are often not as long or deep as single factor styles. When investing in a Core QVM portfolio approach, you can empathise when your committed deep value investing friend is struggling, while hopefully not feeling quite as much pain.

How to screen for good, cheap, strong stocks?

OK, I have said you can’t screen for these stocks using conventional screening rules, but it’s still worth a try.

Using financial ratios

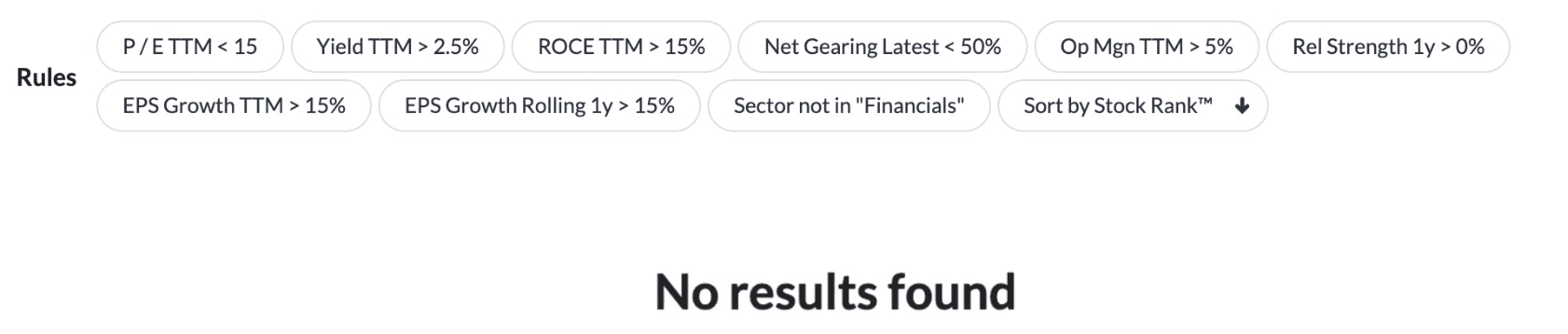

Some of the basic rules I might use to find “the perfect stock” would be:

Quality

Return on Capital > 15% - good profitability

Operating Margins > 5% - reasonable margins

Net Debt to Equity < 50% - not too much debt

Value:

Price / Earnings ratio < 15 - a reasonable valuation

Dividend Yield > 2.5% - a reasonable dividend yield

Momentum:

Relative Price Strength > 0% - beating the market

Growth:

Earnings per share Growth > 15% - growing nicely

Earnings per share Growth (forecast) > 15% - forecast growth to continue

At the time of writing, there is only 1 stock in the UK that qualifies for this set of rules right now, and only 10 in the entire world, with most hard to deal in Asia.

Here’s a few things you can do with those rules (or your own iteration on them):

Loosen the criteria in the screen by “pausing rules”, or changing the parameters.

Use them as a checklist - often many stocks just marginally fail one or two of those rules. Whenever you come across a stock you like, you can test it against a checklist like this, to quickly identify where it fails. Some of my favourite stocks are only marginal fails against this rule set.

Great books like Robbie Burn’s highly accessible “The Naked Trader” and Jim Slater’s “The Zulu Principle” encourage the use of similar checklist rules when assessing shares, and overlay a range of qualitative factors to assess further - such as looking for director buys, share buybacks, “something new”, and a competitive moat.

Using the Ranks

But of course, QVM is the basis of Stockopedia’s entire StockRank system. To simplify finding these kinds of shares, you can just sort the market using the StockRank in the screener. Here’s a link to our QVM “Top StockRanks” screening page where you can thumb through the list or copy it to add further criteria. The StockRank incorporates a broad range of QVM factors including:

whether it’s a good, long term profitable stock.

whether it has improving fundamentals.

whether it’s safe from bankruptcy or earnings manipulation risks.

whether it’s cheap relative to what it owns, earns, sells and pays out in dividends.

whether its share price is strong relative to the market, and its own recent history

whether its earnings expectations are trending upwards and surprising to the upside

When looking at the stocks that have high StockRanks, you’ll find all kinds of warts and surprises. It’s very hard to swallow the stocks individually, but they have tended to perform very well on average.

A guide to investing in good, cheap, strong QVM stocks

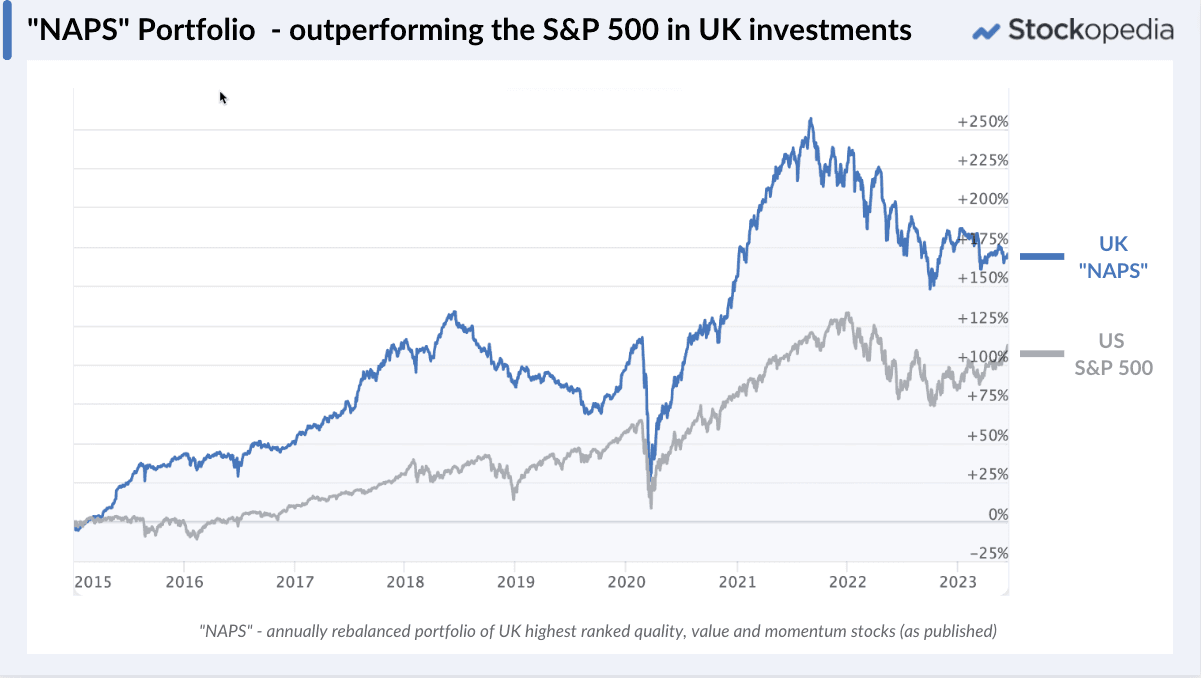

The most obvious illustration of the how to implement a blended QVM approach is from the history of the “NAPS Portfolio”. This is my own “No Admin Portfolio System” that has been published on Stockopedia at the start of each year. While the approach has adapted over time, it leans heavily on the StockRanks for stock selection, and diversifies across ten sectors, rebalancing equally every January. The original rules were:

Sort the market by StockRank descending.

Remove small (less than £20m market cap) and hard to trade (more than 5% spread) stocks.

Construct a portfolio with no more than 2 stocks from each of 10 sectors.

Buy an equal weighted proportion of each stock on the first trading day in January. Repeat steps 1-4 each January, selling those that no longer qualify, buying new qualifiers, and rebalancing the weights of any stocks still held across both periods.

As you can see, the performance since inception has been powerful. I would normally present the performance against a UK benchmark, but given the S&P 500 is heralded as an “unbeatable” benchmark by most of the financial press, and presented as justification for investing in index funds, why not use it for comparison.

It’s not all roses. The post pandemic period saw poor returns to the NAPS, in line with the broader market but underperforming the large cap FTSE All Share and the S&P 500. But the long term results are quite stellar, and on my last inspection, had outperformed 95% of professionally managed listed funds. (Our own research has shown that this NAPS approach has mostly worked in international local markets all around the world.)

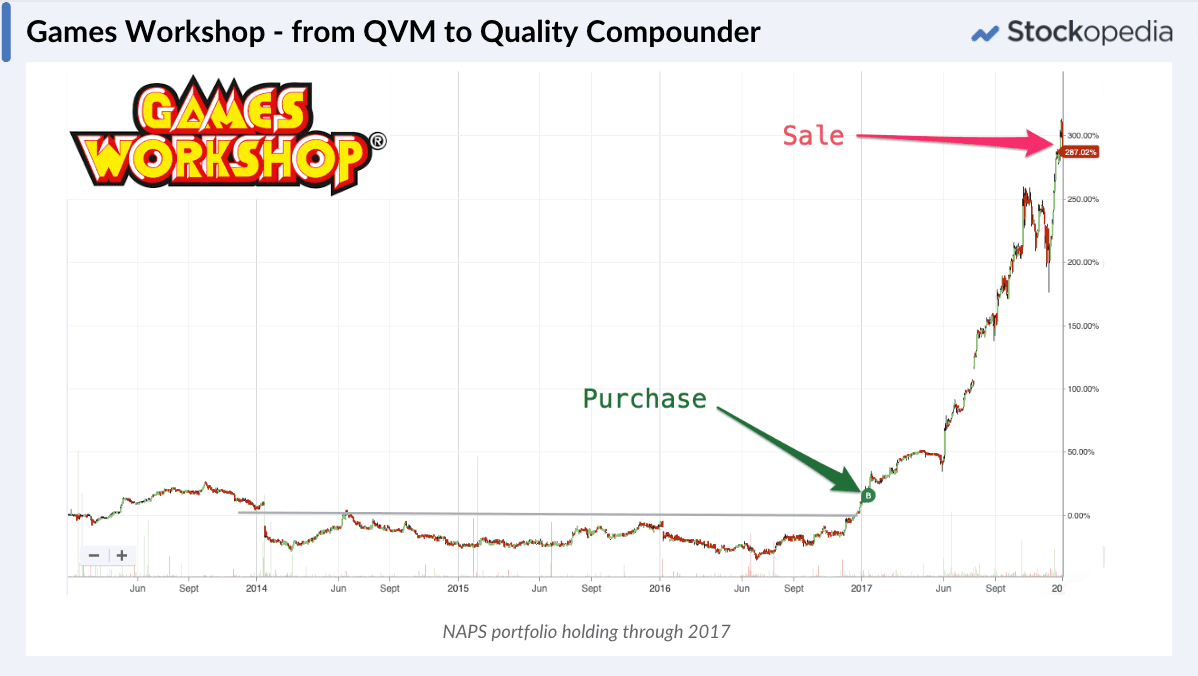

There have been some spectacular winners through the years. One of the greatest businesses in the UK market right now is Games Workshop, which was originally bought for the NAPS in 2017. At the time this stock was completely ignored by the market, but the robust StockRank process identified it and held it to a 250% gain through 2017.

Of course, being a systematic process, the NAPS sold this stock too early. If it had been held for another five years it would have returned 1200% before dividends. Herein lies the opportunity for a great qualitative investor to add more value. Sometimes, hidden in a list of Haugen-esque “Super Stocks” lie the multi-bagging, growth stock winners of the future (as well as rather a lot of more mundane businesses!).

How to pick stocks from the list?

I want to start this with a huge caveat. Joel Greenblatt, author of “The Little Book that Beats the Market” published the top 30 “good, cheap” stocks that qualified for his famous magic formula on a website. After some time he assessed how people using the lists had done. He was astonished to find that the investors who picked shares from the list underperformed those who just bought the whole list. Investors had taken a winning system and made it worse with their own selections.

Nonetheless, even if models have been found to create a ceiling from which we detract performance, rather than a floor to which we add - there’s nothing stopping us trying.

The challenge with a “QVM” list is that you are going to see a wide range of different types of businesses on these lists. You will find turnarounds, contrarian stocks, high flyers and a range of others. There will be growth-at-a-reasonable price stocks, and there may even be a few asset plays.

If you want to pick your own stocks, you should practice becoming adept at identifying the differences between how to approach these styles of stock. It’s for another day to go into the weeds of this, but Peter Lynch’s “One up on Wall Street” is one of the most accessible sources for understanding how to do this. You can find a summary of his insights here.

Other than the obvious themes of high profitability, low valuation, strong balance sheet and consistent earnings and sales trends, Lynch would look for:

A dull or ridiculous name, a disagreeable or even depressing business line in a niche.

Strong management, where directors have skin in the game, and are buying more shares.

Good capital allocation, a share buyback scheme is beneficial, bad acquisitions not so.

Is the prime product a major part of the company’s business? This may be scalable.

Has it proven its expansion in other towns or regions, and is there room to grow?

Low institutional ownership “the lower the better”.

Of course, if the company isn’t a growth stock, some of the above may not be relevant. The NAPS has even seen some stellar runs in mature utilities like Drax. I often find at the end of a year that the biggest winner is one I’d never have predicted at the start.

Some Risks and Limitations of QVM Investing

Temporary Underperformance

One of the hardest things to do in investing is to stick to a strategy that you know will work in the long run, even when in the short run it is struggling. Whenever QVM investing isn’t "working" I remind myself that if the stock market isn’t rewarding good, cheap, strong shares then what on earth is it doing? When it rewards the opposite - expensive, weak, junk (which Haugen would call “stupid stocks”) - then Mr Market has lost his mind. He’ll regain his senses in time.

Given this, there is the risk that you throw in the towel to join a market party elsewhere. In the pandemic, high StockRank shares suffered very badly. Profitable stocks were not rewarded - in fact many bombed. Speculative stocks soared, as meme-stocks like Gamestop, and speculative biotech names became all the rage. In those environments you have to keep your head. Maybe you can join those parties for a trade or two, but keep your wits. The good will out.

Sector Skews - You are highly likely to see many cyclical names in a QVM list. Some sectors have lower valuations than others, and some sectors have higher profitability than others. A ranking system like the StockRanks, does not factor this in as it treats all sectors the same. What you need to do is add a portfolio construction layer after you’ve sorted the market and selected stocks. I like to force my portfolios into sector buckets - you don’t have to go as extreme as to own stocks in every single sector, but try to own shares across at least 5 sectors to reduce the chance that you take a “single sector bet”.

Thinking “this is the one” - it’s so easy to get over-excited about a stock that you think “has all the perfect traits”. This isn’t helped with a ranking system that excites me even today when I see a “99” ranked stock. The reality is that all stocks are speculative, and there’s a variable set of outcomes that will occur. Some will do well, some will do badly. On average, the NAPS Portfolio has only selected marginally more winners than losers in the average year. But it’s still crushed the market over time due to a few stocks that do exceptionally well year to year. Stay patient, diversify and don’t get overconfident.

Safe investing!

Further Reading

“The Inefficient Stock Market” - Robert Haugen

"What works on Wall Street" - O’Shaughnessy

“The Naked Trader” - Robbie Burns

“The Zulu Principle” - Jim Slater

“One up on Wall Street” - Peter Lynch

“A New Core Equity Paradigm” - AQR