Good morning all, let's see what we've got in store for us today!

Companies Reporting

| Name (Mkt Cap) | RNS | Summary | Our view (Author) |

|---|---|---|---|

AstraZeneca (LON:AZN) (£163bn) | Rev +10%, adj EPS +21% to $2.49. FY25 guidance unchanged, five positive Phase III readouts. | ||

HSBC Holdings (LON:HSBA) (£147bn) | Adj PBT +11% to $9.8bn, RoTE 17.9%. Q1 divi of $0.10, $3bn buyback. Volatile macro outlook. | ||

BP (LON:BP.) (£57.8bn) | Und. RC profit $1.4bn (4Q24: $1.2bn). Divi 8 cents, $0.75bn buyback. Outlook mixed. | AMBER/RED (Roland) Today’s Q1 numbers appear to have missed expectations and flag up a sharp rise in debt. The company is accelerating asset sales and believes it remains on track to hit 2027 financial targets. However, oil prices are now below the level on which February’s guidance was based. BP’s higher leverage and sector underperformance also makes me cautious, given the uncertain external conditions. There could be value on offer here. But I think BP’s Value Trap styling is a timely warning that the stock may deserve a lower rating than peers. | |

Coca-Cola Europacific Partners (LON:CCEP) (£30.2bn) | Q1 in line, rev +5%, volumes +7.8%. FY25 guidance unchanged. | ||

Associated British Foods (LON:ABF) (£16.2bn) | Rev -2%, adj PBT -10% to £818m. £101m impairment in Sugar. FY outlook unchanged. | AMBER (Roland) [no section below] Today’s half-year results confirm that performance in the group’s Primark and Grocery business is on track to meet full-year expectations. However, the Sugar business is now expected to report an operating loss of up to £40m due to low sugar prices and some structural and regulatory issues. Restructuring efforts are underway. Frustratingly there’s no clear guidance on the impact to group profit expectations this year. However, based on previous guidance, I estimate a c.5% reduction in group earnings, which would be consistent with today’s share price fall. ABF was a Super Stock prior to today and I think the shares are probably reasonably priced on a long-term view. However, I think a neutral stance is more appropriate following today’s update. | |

Beazley (LON:BEZ) (£5.6bn) | Written premiums +2%, renewal rates -4%. Guidance unchanged for FY combined ratio in “mid-80s”. | ||

Howden Joinery (LON:HWDN) (£4.1bn) | Adj rev +3%, LFL +1.8%. Double-digit intl growth. Balancing margin and volume. FY in line. | ||

Entain (LON:ENT) (£4.0bn) | Q1 rev +11%, ahead of exps, FY25 outlook unchanged. New CEO appointed. | ||

Jet2 (LON:JET2) (£2.9bn) | FY25 results in line with exps with adj PBT +9% (£565-570m). FY26 YTD seeing late bookings. | GREEN (Roland) A solid update from this well-run business including news of an unexpected £250m buyback. Broker forecasts for the current year have been upgraded as a result. While there’s some uncertainty about demand this summer, I think the valuation already reflects this. I’m happy to maintain our previous positive view. | |

Breedon (LON:BREE) (£1.6bn) | Rev +9%, some project delays. Slight rise in total volumes, stable pricing. FY25 outlook unch. | ||

Telecom Plus (LON:TEP) (£1.5bn) | Net cust. growth +15%, FY25 guidance unchanged for PBT £124-£128m. Confident outlook. | ||

Travis Perkins (LON:TPK) (£1.1bn) | Q1 rev -2.1% LFL, “challenging”. Merchanting -3.2% LFL, Toolstation +3.7% LFL. | ||

Bakkavor (LON:BAKK) (£1.0bn) | China business sold for c.£50m, net profit of £15m expected on disposal. | PINK (possible offer) | |

Elementis (LON:ELM) (£759m) | Rev -2%, but adj op profit & margins ahead of Q1 24. FY exps unch, but warns of tariff risks. | ||

Alfa Financial Software Holdings (LON:ALFA) (£638m) | Q1 rev +20%, in line with exps. Total contract value “record” £227m. FY exps unchanged. | ||

THG (LON:THG) (£409m) | Rev -3.1%, adj EBITDA +0.3% at £114.4m “in line”. Q1 24 rev -7%, FY25 rev exps unch. | ||

Newriver Reit (LON:NRR) (£346m) | CAL integration on track. LTV c.42%, FY25 UFFO and EPRA NTA to be in line with exps. | ||

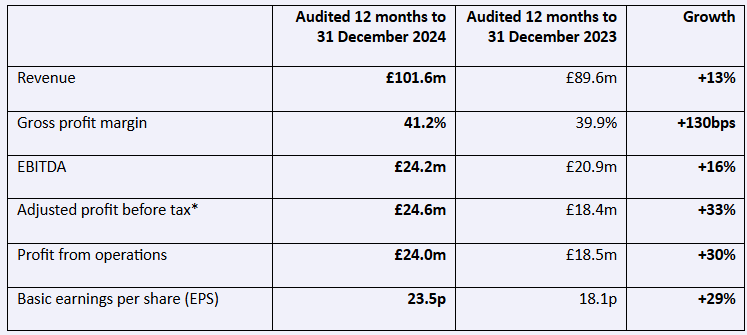

Warpaint London (LON:W7L) (£327m) | Rev +13%, adj. PBT +33% (£24.6m). Brand Architekts acq’n completed. Exps unchanged. | AMBER/GREEN (Graham) I'd like to be fully GREEN on this but there are a couple of issues. Q1 has been soft in terms of underlying growth, with quite a lot of month-to-month sales volatility. The company's big opportunity in the US is currently under the cloud of tariffs, whose impact at this stage is highly uncertain. It's a seriously impressive roll-out story all the same. | |

Pinewood Technologies (LON:PINE) (£320m) | All 350 VW/Audi dealerships in Japan. Rollout and revenues to commence in the first half of 2026. | ||

Mobico (LON:MCG) (£206m) | Adj. op profit £188m, in line. Unadjusted loss £794m. New Chair/COO. CEO steps down. | ||

Animalcare (LON:ANCR) (£167m) | Rev +4.9%, PBT £5.8m (LY: £3.3m). Net debt £9m. Randlab acq’n completed. Positive outlook. | ||

Hostelworld (LON:HSW) (£140m) | SP down 3% | GREEN Graham [no section below] | |

MPAC (LON:MPAC) (£126m) | Rev +7%, PBT £3.5m (2023: £4.7m). Net debt £37.5m. On track to achieve 2025 exps. | ||

Inspired (LON:INSE) (£109m) | Regent says offer is 71% premium to Jan 2025 placing price and 43% premium to price at which it began to increase its shareholding. | PINK (under offer) | |

Watkin Jones (LON:WJG) (£85m) | H1: small op. profit. Net cash £73m. Pipeline has “potential to deliver an expected stronger H2”. | ||

Focusrite (LON:TUNE) (£84m) | Rev +5%. Macro uncertainties persist. Exps “remain realistic” given 90 day pause. Debt £18m. | ||

Falcon Oil & Gas (LON:FOG) (£63m) | Pre-revenue. 2024 loss before tax $3m. Debt free with cash of $6.8m as of December 2024. | ||

Manolete Partners (LON:MANO) (£35m) | FY25 realised revenues (£29.5m), EBIT (£2m) and PBT (£0.3m) are ahead of market expectations. | ||

Nexteq (LON:NXQ) (£35m) | Confident in achieving 2025 full year market expectations. Net cash position $30.2m. | ||

Insig Ai (LON:INSG) (£32m) | Q4 and FY March 2025 ahead of previous guidance. Q4 revenue £249k, 11% ahead of guidance. | ||

SysGroup (LON:SYS) (£19m) | FY March 2025: revenue (£20.5m) and adj. EBITDA (£0.9m) in line with market expectations. | ||

KRM22 (LON:KRM) (£9.6m) | Payment of all interest deferred until June 2026, to conserve cash. Floating rate currently at 9.5%. | ||

Touchstar (LON:TST) (£6.0m) | A major order was delayed, but now confirmed for 2025. Solid potential in the sales pipeline. |

Graham's Section

Warpaint London (LON:W7L)

Down 4% to 387p (£312m) - Full Year Results - Graham - AMBER/GREEN

Warpaint London plc (AIM: W7L; OTCQX: WPNTF), the specialist supplier of colour cosmetics and owner of the W7, Technic, Skin & Tan, Super Facialist, Dirty Works and Fish Soho brands is pleased to announce its audited results for the year ended 31 December 2024.

We already covered the 2024 trading update here.

Today we have confirmation of the numbers:

As noted by Mark in February, operational leverage has turbo-charged the performance, giving us 33% growth in adj. PBT despite much more modest growth in revenue.

Cash finished the year at £21.9m, but most of that was escrowed to buy Brand Architekts.

The cash balance as of 8th April: £17.3m.

Dividend: total payout for the year is 11p, covered more than 2x by EPS.

Current trading and outlook: “solid start to trading in Q1 2025”, Q1 sales +14% year-on-year. Excluding Brand Architekts, sales are up 7% year-on-year.

Some seriously impressive brand rollout news:

Italian drug store Tigota is launching products in 200 stores, plus a “capsule collection” (smaller range) going into an additional 400 stores.

Dutch drugstore Etos is expanding its product assortment in all 546 stores.

Superdrug UK rolling out W7 into 140 news stores and travel size products in all stores.

Tesco: 150 store expansion of W7. Boots: Christmas gifting products for the first time in 350 stores.

CVS Pharmacy (United States): expanding W7 range and roll-out to a further 399 stores from August 2025, taking the total number of CVS stores stocking their products to 918.

They are “in talks with other large retailers in Europe, the UK and the US to stock the Group's products”.

Expectations are unchanged:

Despite continuing headwinds, including the effect of increased US tariffs, the Group has significant planned expansion opportunities and the board expects the Group's performance to remain strong and for sales and profits to grow in line with previous expectations over the remainder of 2025 and beyond. Accordingly, the board's expectations for the Group's financial performance in 2025 are unchanged

Estimates: thanks to Shore Capital for publishing on Warpaint today. Consistent with the above, they leave their forecasts unchanged.

Revenue this year is expected to grow by 26% to £128.6m - given that growth in Q1 was only 14%, that implies quite a significant acceleration through the rest of the year.

Shore acknowledges this, saying that their forecasts “do require an improvement in sales momentum for the remainder of the year”.

It sounds like there has been quite a lot of month-to-month volatility recently, with some months being weak and then others being very strong.

Therefore, I can't say that I have a great deal of confidence in these forecasts. To me, this sounds like the precursor to a profit warning. But then, given the volatility and the forthcoming store roll-outs, there is also the possibility of a surprise to the upside!

Adjustments: just a quick note to say that today’s accounts are very clean with only small adjustments, including modest share-based payments, creating very small gaps between EBITDA/operating profit and adjusted EBITDA/adjusted operating profit. Well done to the company for that. We’ll see if this can continue despite the recent acquisition.

Graham’s view

As I’ve said, I think that at this stage it’s difficult to have a great deal of conviction in how Warpaint is going to do this year. They’ll be busy, with lots of exciting expansion projects, but the financial result at this stage is a finger-in-the-air type of prediction.

At this stage it’s difficult to say how long-lasting or serious the tariff problem might be. With over 900 CVS stores in the United States stocking W7L products soon, that is a major opportunity for the company long-term.

The CEO’s comment suggests to me that difficulties with US sales are for now at least offset by opportunities elsewhere. He says with respect to US sales:

…we remain focused on ensuring that sales the Group undertakes remain profitable, whilst benefiting the longer-term strategic positioning of the Group's brands in a potentially improved tariff environment.

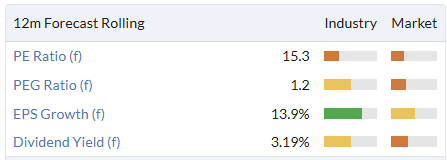

I’m inclined to leave our AMBER/GREEN stance unchanged here to reflect that I do see much more here to like than to dislike. The valuation doesn’t strike me as being particularly expensive for a successful roll-out with international opportunities:

Roland's Section

Jet2 (LON:JET2)

Up 16% to 1,567p (£3.4bn) - FY25 Trading Update - Roland - GREEN

Full year results in line with expectations and £250m Share Buyback announced

This AIM-listed airline and package holiday group is a company I’ve regarded highly for a long time and should probably have bought at some point.

Shares have risen strongly today, in part due to news of a £250m buyback which has prompted an upgrade to FY26 earnings per share forecasts.

FY25 trading update: today’s update covers the 12 months to 31 March 2025 and looks very reassuring to me. Let’s take a look at the main points:

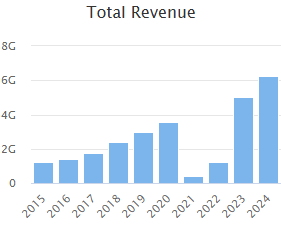

FY25 pre-tax profit expected to be between £565m and £570m (FY24: £520.1m);

This represents an increase of 9% and is in line with expectations;

Jet2 will also report an additional £10m of disposal profits, largely from the sale of retired Boeing 757 aircraft;

Total cash of £3.2bn and own cash (excluding customer deposits) of £1.1bn;

£250m share buyback programme.

Profit: although 9% profit growth is substantially lower than the 33% growth reported for FY24, it’s still a strong result and should continue to support the attractive quality metrics we’ve come to expect from this business:

Cash/balance sheet: Jet2’s strong balance sheet is another attraction. In addition to providing support for growth investment and fleet renewals, it’s also a useful source of income in itself – net interest received in FY24 was £84m. I’d expect a comparable result for FY25.

However, it’s worth noting that Own Cash is not net cash – Jet2 reported total debt of £1.3bn at the half-year market and my impression is that net cash/net debt will be close to zero in the full year accounts. The company is working its way through a previously flagged £5bn/6yr expenditure programme. Elements of this completed over the last year include:

Opening two new operating bases

Purchasing 4 new Airbus A321neo aircraft using its own cash

Purchasing £159m of shares for the Employee Benefit Trust to reduce future dilution

FY26 trading commentary: Jet2 is continuing to add capacity this year despite more uncertain market conditions:

Capacity for Summer ‘25 is currently 8.3% of Summer ‘24, at 18.6m seats;

New bases at Bournemouth and Luton have contributed about half the new capacity;

So far this year the company is seeing a late booking profile, limiting forward visibility;

The mix of passengers is currently skewed more heavily to (lower margin) flight-only bookings than it was last year

Pricing remains stable, with “modest average increase” in holidays and a “slight increase” to flight prices, helping to offset cost rises

CEO Steve Heapy sounds cautiously optimistic and has promised a fuller update when the results are published in July:

Although still very early in FY26, we are satisfied with progress for Summer 2025 so far.

Outlook: with thanks to broker Canaccord Genuity we have updated forecasts today. Despite the company billing today’s FY25 profit guidance as “in line”, Cannacord has upgraded its earnings forecasts for both FY25 and FY26:

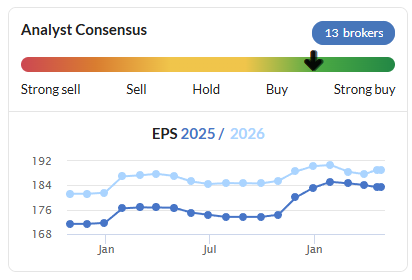

FY25E EPS: +14.5% to 215.1p (previously 187.7p)

FY26E EPS: +7.4% to 223.9p (previously 208.5p)

The previous numbers are slightly ahead of consensus forecasts on Stockopedia, so assuming Canaccord’s modelling is in line with the company’s internal expectations, this looks like a fairly meaningful upgrade.

These estimates leave Jet2 trading on a FY25E P/E of 7.3, falling to a FY26E multiple of 7.0. This doesn’t seem expensive to me, even for a travel business.

Roland’s view

Today’s update does nothing to change my positive view on this business. While there’s clearly some uncertainty about the outlook for this summer, past experience with Jet2 is that it’s generally fairly conservative with guidance. I wouldn’t be surprised to see a modest upgrade later in the year.

A strong balance sheet and clear-headed long-term growth model helps differentiate this business from rivals, in my view. Jet2’s long-term record suggests this approach also delivers a high level of customer satisfaction:

I was GREEN on Jet2 in February and I’m happy to maintain that positive view today.

BP (LON:BP.)

Down 3.8% to 348p (£55.1bn) - Q1 Results - Roland - AMBER/RED

Today’s first-quarter numbers from BP have met with a poor reception from the markets despite bullish commentary from under-pressure CEO Murray Auchincloss:

So far this year we have started up three major projects, made six exploration discoveries and have progressed our divestment programme - all while delivering strong operational performance, with over 95% upstream plant reliability supporting the best operating efficiency* on record, and over 96% refining availability.

A fall in Q1 profits versus last year was expected due to lower commodity prices. The problem with today’s results seems to be that they have missed consensus expectations – and not for the first time in the company’s recent history.

Here’s a summary of the main numbers for Q1 2025:

Underlying Replacement Cost (RC) profit: $1,381m (Q4 24: $1,169m, Q1 24: $2.723m)

Net debt: $26,968m (Q4 24: $22,997m)

Quarterly dividend unchanged at $0.08 per share

BP is more heavily geared than most rivals, certainly more so than Shell. Aggressive buybacks have contributed to this – the $4bn increase in net debt in Q1 was partly due to $1.9bn of buybacks. Perhaps in a sign of pressure, buybacks for the current quarter have been scaled back to $0.75bn – the bottom end of February’s guidance.

In fairness, BP says it’s confident that proceeds from divestments and disciplined spending will allow the group to meet its target of net debt of $14-18bn by the end of 2027.

Personally, I’m not a fan of companies buying back shares with borrowed cash. My feeling is that BP should have used the bumper profits of recent years to accelerate debt reduction, rather than relying on divestments in what could prove to be more difficult market conditions.

Outlook: oil prices have continued to fall since the end of the first quarter, suggesting that Q2 will not be any easier for this business:

At current levels, oil is trading below the $70 per barrel on which the company’s updated financial targets were based in February.

Today’s full-year guidance is broadly unchanged, but the company is now accelerating its disposal plans and is targeting $3-4bn of disposals this year, from “around $3bn” previously.

I don’t have access to any broker coverage for BP. But consensus estimates have trended consistently lower over the last year. I wouldn’t be surprised to see them trimmed again following today’s update:

Roland’s view

Today’s Q1 update isn’t great, but to be honest, I don’t think it’s that important either. In my view, investors considering BP at the moment need to focus on the bigger picture:

Cyclical risk – where are we in the cycle? This is harder than usual to understand, given tariff-related uncertainty;

Can BP establish a consistent and successful strategy and reverse its track record of underperformance?

Consensus forecasts for BP have fallen by nearly 45% since April 2024. In contrast, estimates for Shell’s 2025 earnings have only been cut by 18% over the same period.

While the two companies aren’t exactly equivalent, I think this helps us separate the impact of commodity prices from BP’s company-specific underperformance.

BP CEO Murray Auchincloss is currently under pressure to improve performance from activist investor Elliott Management, which has built a 5% stake.

Mr Auchincloss has already announced plans to reverse the group’s 2020 strategy and focus more heavily on oil and gas production, cutting renewable spending. However, Elliott believes the changes don’t go far enough and is reportedly calling for big spending cuts.

BP’s share price has fallen by 35% over the last year and the stock is now – arguably – priced at a level where some cyclical value could be on offer. Stocko data shows BP trading at less than eight times 10-year average earnings, compared to nearly 13 times for Shell:

The company has previously said its dividend is covered by cash down to a Brent Crude price of $40. If Auchincloss can improve profitability and cash generation, then the current 6.5% yield could be safe and the shares could recover strongly when market conditions improve.

On the other hand, there is not yet much sign of the improving momentum we might seek to provide confidence in a turnaround. BP’s MomentumRank has now dropped to extremely low levels, reflecting the combination of a falling share price and falling earnings estimates:

As a result, Stockopedia’s algorithms are now styling the shares as a Value Trap – an underperforming style:

Investors with a keen interest in this sector might want to take a closer look.

However, BP has a long track record of periodic missteps and incomplete recoveries and has underperformed Shell on 1, 2, 5, 10 and 20-year timeframes:

Given BP’s disappointing Q1 result and worsening quantitative metrics, I think it’s sensible for me to downgrade our previous neutral view to be mildly negative. AMBER/RED.

See what our investor community has to say

Enjoying the free article? Unlock access to all subscriber comments and dive deeper into discussions from our experienced community of private investors. Don't miss out on valuable insights. Start your free trial today!

Start your free trialWe require a payment card to verify your account, but you can cancel anytime with a single click and won’t be charged.