Good morning!

The agenda is now complete.

Update 11.50: today's report is now complete. I hope you're able to enjoy the long weekend! The Daily Report will be back on Tuesday.

| Name (Mkt Cap) | RNS | Summary | Our view (Author) |

Games Workshop (LON:GAW) (£5.2bn) | Expect FY25 rev of c.£610m, PBT at least £255m. Record licensing revenue, exp lower in FY26. | GREEN (Roland) Today’s update is ahead of previous expectations, as far as I can see. These are certainly exceptional figures from the Warhammer maker, only tempered slightly by a warning that licensing revenue is expected to be lower this year. Given the group’s exceptional quality and track record of outperformance, I’m going to maintain our positive view. | |

AJ Bell (LON:AJB) (£1.9bn) | Rev +17%, PBT up 12% to £68.8m. Customers +9%, AUA +5% to £90.4bn, £3.3bn net inflows. FY results to be ahead of previous expectations. | GREEN (Roland) I am staying positive on this well-run investment platform after today’s strong half-year results. Upgraded guidance for the full year highlights strong trading momentum and customer acquisition. Profitability remains excellent despite price cuts and the business is investing in its brand and offering to support continued market share gains. On a P/E of 20, I think the shares remain fairly priced on a longer-term view. | |

Assura (LON:AGR) (£1.6bn) | Due diligence underway on improved Primary Health Properties (LON:PHP) offer. A planned General Meeting to vote on the KKR offer has been adjourned. | PINK (Roland) [no section below] With two firm offers on the table for this healthcare REIT, a deal of some kind seems very likely to me. For shareholders, the weakness of the PHP offer is that it’s a cash/shares offer, whereas KKR’s 49.4p offer is all cash. At current prices, I estimate both offers are almost identical in terms of value (49.4p vs 49.6p). With AGR stock trading at book value (49.5p) and in line with the current value of both offers, investors may want to consider whether to lock in some gains or hold out in hope of a slightly better outcome. | |

Begbies Traynor (LON:BEG) (£157m) | Revenue, EBITDA, net cash ahead of exps. Rev +12%, adj PBT +7% to £23.5m. | AMBER (Roland) Today’s update is (slightly) ahead of expectations, but I don’t see much to change my view that this business is not really profitable enough to deliver the kind of rewards shareholders might hope for. However, the business seems fine and I can’t fault these numbers in themselves. The valuation also remains modest at under 10x earnings. On balance, I’m happy to stay neutral here. | |

Epwin (LON:EPWN) (£125m) | YTD trading in line with exps. Revenue +8% ahead of prior year. FY op profit exp to be in line. | GREEN (Roland - I hold) [no section below] This building materials group continues to look attractively valued and in good health to me. While housing market conditions remain mixed, I think Epwin is well positioned to benefit in an upturn. In the meantime, the 6% dividend yield and ongoing share buyback look affordable. The buyback is likely to generate value for shareholders at current levels, in my view. | |

Seascape Energy Asia (LON:SEA) | Year end cash £2.8m, op loss £5.7m. Since received c.$11m cash. Progress with SE Asia portfolio. | (Roland) - this oil and gas stock was previously known as Longboat Energy. The company has sold its Norwegian/North Sea assets and pivoted to Southeast Asia. | |

Tekcapital (LON:TEK) (£17m) | Net assets +46% to $70.1m, NAVps +22% to $0.33. After-tax profit $19.2m. | AMBER (Roland) [no section below] This investment group targets IPOs for its portfolio companies. When successful this can generate significant gains, as highlighted by last year’s net profit of $19m. Last year’s UK listings included MicroSalt and GenIP, both on AIM. The discount to book value is over 60%, but similar peers in the UK (e.g. Molten Ventures, IP Group) also trade at large discounts, presumably reflecting the difficulty and uncertainty involved in realising gains. There could be value here for an investor willing to research the investee businesses, but it’s too speculative for me. | |

Totally (LON:TLY) (£2.8m) | Offers have been received for subsidiaries. Board has concluded disposals are only option to fund liabilities. Sale of business expected before further funding required, but potential proceeds are unlikely to meet all future liabilities - “there could be no value in the ordinary shares” | RED (Roland) [no section below] Completely uninvestable, in my view. I think the only sensible choice is to assume that shareholders will face a total loss. |

Roland's Section:

Games Workshop (LON:GAW)

Down 3% to 15,390p (£5.1bn) - Full Year Trading Update - Roland - GREEN

The Group's profit before taxation ("PBT") is estimated to be not less than £255 million (2023/24: £203.0 million).

Games Workshop’s share price is down slightly this morning, but today’s full-year update appears to be ahead of broker forecasts.

When the maker of Warhammer last issued a trading update in March, paid research provider Edison issued a FY25 forecast for pre-tax profit of £242m. Today’s figure of £255m is comfortably ahead of this.

The total FY25 revenue figure provided today of c.£610m is also higher than the £590m consensus estimate shown on Stockopedia.

I think it’s reasonable to view today’s trading statement as another ahead of expectations update from this impressive company.

FY25 trading update: here’s a quick summary of the numbers provided today for the 52 weeks ended 1 June 2025.

The company divides this reporting into core (the wargaming business) and licensing:

Core revenue “not less than” £560m (FY24: £494.7m)

Licensing revenue of c.£50m (FY24: £31m)

Core operating profit “not less than” £210m (FY24: £174.8m)

Licensing operating profit of c.£45m (FY24: £27m)

Core trading: these figures tell us that core sales rose by 13.2% last year, driving a 20% increase in operating profit. When profits rise faster than sales it means margins are expanding – in this case the numbers imply a core operating margin of 37.5% (FY24: 35.3%).

Licensing: licensing revenue is generated from deals for Games Workshop intellectual property to be used in other media - TV, games and films. It’s almost 100% margin and rose by around 60% to a new record high last year. However, the company does sound a note of caution on licensing prospects for the current year:

Licensing revenue in the period is at a record level and we are not expecting this to be repeated in 2025/26. Licensing remains a significant area of focus.

This is perhaps one area where the company could be more transparent – the statement above leaves a lot to interpretation. It doesn’t, for example, make any mention of progress with the company’s Amazon deal.

Staff profit share: Games Workshop’s employees have received profit share payments of c.£20m during the year, paid on an equal basis to each member of staff. Last year’s annual report indicates the company has c.3,500 staff, so they may each have received a payment of around £5,700.

The company consistently reports high staff retention and its employees clearly make a big contribution to its success.

For contrast, shareholders received dividends during the same period of £171.4m, so there’s clearly no clash between treating employees fairly and rewarding investors. Perhaps a lesson other companies could take on board.

Outlook & Estimates: apart from the comment on licensing, there’s no forward guidance in today’s update. This is in line with Games Workshop’s normal practice of largely restricting its reporting to facts.

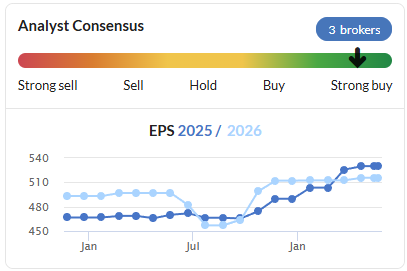

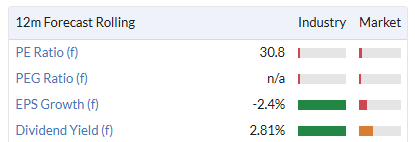

However, the last broker note I can find (from 6 March) suggests revenue and earnings could fall during the 25/26 financial year. This is also reflected in our consensus forecasts:

Based on past performance, there’s a reasonable chance these estimates may be upgraded over the coming year. As things stand, these numbers leave the shares on a forward P/E of 30.

Roland’s view

Ed recently highlighted Games Workshop as one of only two multibaggers from his NAPS portfolio that would have been worth holding over the whole 10-year history of the portfolio. It’s tempting to think that normal rules don’t apply to this business, but of course they do.

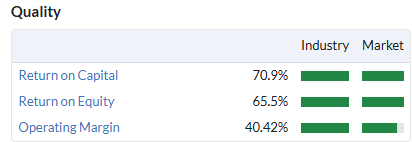

The shares have not looked cheap for a long time, but a combination of exceptional quality metrics and continued growth has meant that they’ve offered value regardless, truly living up to their High Flyer styling.

I don’t know when this long run of success might end, but for now I’m inclined to give the firm the benefit of the doubt despite the forecast drop in earnings this year. Games Workshop’s strong performance and exceptional quality means I’m going to maintain our GREEN rating for now.

AJ Bell (LON:AJB)

Up 7% to 490p (£2.0bn) - Interim Results - Roland - GREEN

AJ Bell plc ('AJ Bell' or the 'Company'), one of the UK's largest investment platforms, today announces its interim results for the six-month period ended 31 March 2025.

We’ve written favourably about this investment platform previously. Today’s results highlight many of the things we like so much about this business and put the company on track to deliver full-year results ahead of previous expectations (my emphasis):

In the first half of the year we have delivered strong financial results. We expect this momentum to continue with full-year revenue and PBT anticipated to be higher than that previously guided at the start of the financial year.

H1 results summary: AJ Bell’s revenue for the half year rose by 17% to £153.2m, supporting a 12% rise in pre-tax profit to £68.8m. Shareholders will be rewarded by a blended mix of dividend growth and a further buyback:

In accordance with our capital allocation framework, we are pleased to declare an interim dividend of 4.50 pence per share, up 6% versus prior year, alongside the initiation of a second share buyback programme of up to £25 million, reflecting our ongoing commitment to return surplus capital to shareholders.

While conventional fund managers are struggling to attract new customers, this doesn’t seem to be a problem for the leading retail investment platforms.

AJ Bell saw customer numbers rise by 9% to 593,000 during the period, while total assets under administration (AUA) rose by 5% to £90.4bn. The majority of this increase came from net inflows of £3.3bn, topped up with a £0.6bn gain due to market movements.

Today’s profits show the group’s pre-tax profit margin falling from 46.8% to 44.9% (still an outstanding figure). However, the company says this reflects planned investment in the company’s brand and customer proposition to drive long-term growth.

Fortunately, the underlying profitability of the group’s asset management operation remained stable, despite a £20m package of price cuts in April. AJ Bell’s revenue margin for the half year was 32.4bps (i.e. 0.324%), compared to 32.3bps for the same period last year.

Revenue margin represents revenue as a percentage of AUA. Management says this stable result was driven by the benefit of higher transaction volumes and AUA-related fees offsetting lower prices.

Outlook: CEO Michael Summersgill says the growth momentum seen during the company’s first half has continued into the second half (i.e. April onwards), “despite significant market volatility”.

He says DIY investors (vs advised investors) were particularly active, investing over £300m in just 10 trading days at the start of April, mostly in equities and bonds.

Full-year revenue and pre-tax profit are now expected to be ahead of previous guidance, which appears to be for revenue of £296m and a pre-tax profit of £124m (source: Hannam & Partners Dec 24).

We aren’t given details of upgraded guidance today and I don’t have access to any updated broker notes. However, assuming H2 pre-tax profit is level with H1, full-year PBT could be c.£137m – roughly 10% above previous estimates. This is consistent with the c.10% share price gain seen this morning.

Roland’s view

I think this is an excellent and well-run business. I like AJ Bell’s dual approach of providing a platform for financial advisers and DIY investors. This addresses two areas of strong growth, without requiring the company to commit to a single segment.

AJ Bell is continuing to invest to broaden its offering and maintain high service quality, taking advantage of strong trading to support this spend without impacting overall margins.

A P/E of 20 doesn’t seem excessive to me for a business with a strong growth record, good market share and outstanding quality metrics:

Graham went GREEN on AJ Bell in January, when the shares were trading at around 440p. The share price is nearly 15% higher now, but given the group’s strong progress and today’s upgrade, I am inclined to maintain our positive view.

Begbies Traynor (LON:BEG)

Up 2% to 100p (£159m) - Year-End Trading Update - Roland - AMBER

Begbies Traynor Group plc (the 'company' or the 'group'), the professional services consultancy, announces an update on trading for its financial year ended 30 April 2025.

The market seems underwhelmed by today’s trading update, despite insolvency specialist Begbies Traynor proudly flagging these figures as “ahead of consensus expectations”.

The headline figures show solid revenue growth, but with profits rising more slowly than revenue, it seems that overall margins weakened last year (even at an adjusted level):

Revenue expected to rise by 12% to c.£153m (including 10% organic growth)

Adjusted EBITDA to be up by c.10% to c.£31.3m

Adjusted pre-tax profit to rise by c.7% to c.23.5m

Net cash of £0.9m at 30 April 2025

In its insolvency business, Begbies says it saw an increase in insolvency activity over the last year, especially in higher value cases. Revenue in this division rose by 11%, without any acquisitions.

Begbies claims a market-leading position in this sector by number of appointments and says it has expanded its team to support growth, with a strong pipeline for FY26.

Property-related legal services: the company’s other division is focused on property. Organic revenue growth of 7% was doubled by acquisitions last year, to give a total increase of 15%.

Management says that strong growth in property auctions and increased geographic coverage contributed to last year’s gains. Again, extra senior staff have been hired to support further expansion.

Outlook & Estimates: There’s no comment on the outlook for the year in today’s update – that’s likely to be provided with the full-year results in July.

However, broker Shore Capital has released an updated note today slightly upgrading its earnings estimates for FY25 and FY26:

FY25E EPS: 10.5p (previously 10.4p)

FY26E EPS: 10.5p (previously 10.3p)

The very small size of these upgrades probably tells us why the share price hasn’t moved much today. However, this fresh update is useful and confirms the shares should be trading on less than 10 times forecast earnings, with a useful 4%+ dividend yield.

Roland’s view

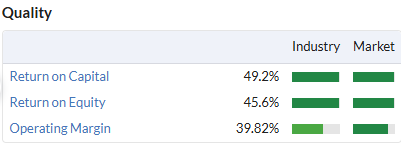

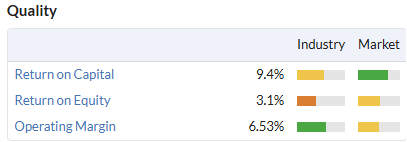

My main concern with this business is that its profitability is consistently low, at least a reported level:

This low profitability may explain why the share price is unchanged from five years ago, even though revenue and profits have doubled over the same period:

This business doesn’t seem to be profitable enough to expand and create value for its shareholders.

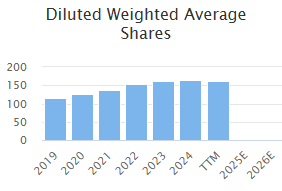

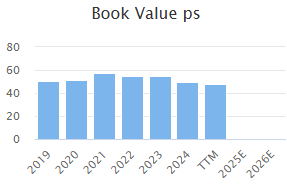

Regular acquisitions have often been part-funded with new equity. As a result, the share count has risen by 50% since 2019, but book value per share has actually fallen slightly:

I can’t help wondering if this professional services group is run more for the benefit of its partners and senior fee-earners than for its shareholders.

We’ve previously been neutral on Begbies Traynor, a view that’s also reflected by the StockRanks:

I don’t see anything in today’s announcement to suggest that I should change that view. (AMBER)

See what our investor community has to say

Enjoying the free article? Unlock access to all subscriber comments and dive deeper into discussions from our experienced community of private investors. Don't miss out on valuable insights. Start your free trial today!

Start your free trialWe require a payment card to verify your account, but you can cancel anytime with a single click and won’t be charged.