Good morning!

It looks like a relatively quiet day for news, but Megan has been speaking with the CEO of Ramsdens Holdings (LON:RFX) and has now posted a review of her thoughts on today's interim results below.

Update 14.00: today's report is now complete. Thanks for all your comments, see you tomorrow!

Companies Reporting

| Name (Mkt Cap) | RNS | Summary | Our view (Author) |

B&M European Value Retail SA (LON:BME) (£3.3bn) | Rev +4% at constant currencies thanks to 70 new stores. B&M UK business below expectations owing to market headwinds. FY26 outlook: impact of additional costs is said to be reflected in current consensus forecasts - in line? | AMBER (Roland) Today’s results highlight negative LFL sales in the UK business and debt levels slightly higher than I’d like to see. But the group’s 10% operating margin and strong cash flow suggest to me that there’s nothing here that the incoming CEO shouldn’t be able to fix. With B&M now trading on nine times forecast earnings and offering a possible 4.8% yield, I’m starting to think this is worth considering as a contrarian play. | |

Paragon Banking (LON:PAG) (£1.8bn) | Net interest margin 3.13% ahead of previous expectations. Underlying profits +2.1% to £149m. Motor finance provision of £6.5m. Return on tangible equity of 17.8%. | AMBER/GREEN (Roland) [no section below] Today’s results from this buy-to-let mortgage specialist showcase robust profitability and suggest the bank expects a minimal impact from its modest exposure to motor finance. A slight increase in bad debt levels is a reminder of the risk of the company’s property exposure, but does not seem a serious concern. At c.1.3x book value, the shares aren’t as cheap as they were. However, strong profitability suggests to me that the value remains fair. On balance I can see plenty to like here. I’m comfortable taking a moderately positive view on this initial review. | |

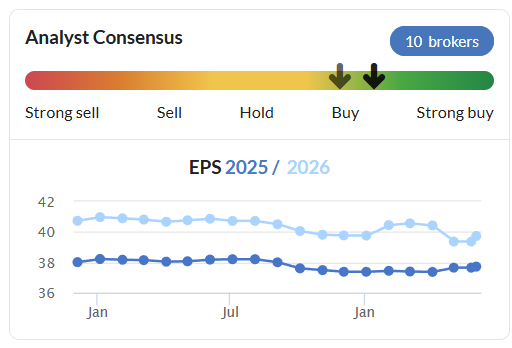

WH Smith (LON:SMWH) (£1.3bn) | Lfl sales +5% in the remaining travel business in line with expectations. Growth in North America remains slow (+2%). Sales of high street business due to complete by the end of June. | AMBER (Megan) | |

Ninety One (LON:N91) (£998m) | Net outflows of -£4.9bn, despite a return to inflows in H2. AUM +4% at £131bn. 76% of funds outperformed benchmark since inception, up from 73% one year ago. | AMBER/GREEN (Roland) [no section below] A return to net inflows in H2 is encouraging, as is the full-year increase in AUM. Although profits fell slightly last year, but the group still generated a respectable 31.2% adjusted operating margin, only slightly lower than the previous year. I’m also encouraged by the strong performance of the group’s funds. A new partnership with South African group Sanlam appears to offer growth prospects and N91’s 33% employee ownership should provide decent alignment with external shareholders. The 7% dividend yield is also covered comfortably by earnings, in contrast to some UK peers. At this point in the cycle, I think a moderately positive view is fair. | |

Empiric Student Property (LON:ESP) (£646m) | Reservations for 2025/26 academic year ahead of the wider market. Lfl weekly rent growth expected at 4% to 5% (ahead of inflation). | ||

Discoverie (LON:DSCV) (£610m) | Rev -3%, adj PBT +4% to £50.1m. H1 EPS ahead of exps. Med-term margin target increased to 17%. | AMBER (Roland) Today’s results look fine to me against a difficult market backdrop. But Discoverie’s rather average profitability suggests to me it doesn’t necessarily deserve the kind of premium valuation awarded to some other industrial buy-and-build operators. Forecast earnings growth is under 5% for the current year. On balance, I can’t help feeling that a P/E of 18 is high enough for now. | |

Johnson Service (LON:JSG) (£609m) | Moving from AIM to Main Market “no later than early August 2025”. Extending £15m buyback to £30m. | ||

H & T (LON:HAT) (£279m) | Voting deadline for takeover is 30 June 2025. Completion expected in H2 2025. | ||

Tullow Oil (LON:TLW) (£220m) | Agreed deal to extend licenses covering Jubilee and TEN fields to 2040. 20 new wells planned. | ||

| Foxtons (LON:FOXT) (£196m) | Capital Markets Event 2025 | A new medium-term target for adj op profit of £50m has been introduced, double 2024 levels. | |

S4 Capital (LON:SFOR) (£160m) | FY revenue to be down by low single digits, previously flat.

LFL Operational EBITDA target unchanged but is now only expected to be “broadly similar to 2024”, with a higher H2 weighting. | AMBER (Roland) Today’s update strikes a cautious note on external conditions and suggests to me that full-year profits could still slip slightly below expectations. However, I think it’s fair to say that S4 is now on a more secure financial footing and is trading at a level that could offer value if market conditions improve over the next 12-18 months. On balance, I think it’s reasonable to take a neutral view here, although the stock's very low MomentumRank means I remain cautious about the near-term outlook. | |

Avacta (LON:AVCT) (£135m) | Results now due on 6 June 2025 due to auditors’ request (previously delayed to 4/6). | ||

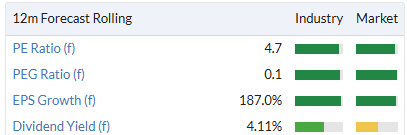

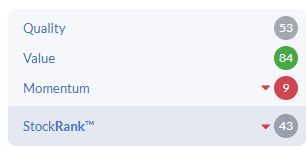

Ramsdens Holdings (LON:RFX) (£107m) | Rev +18%, PBT +52.5% to £6.1m. Growth in all divisions. FY PBT to exceed £15m, ahead of exps. | GREEN (Megan) An excellent play on the gold price and a well run, cash generative business with decent growth prospects. There is no denying the share price is linked to the price of the yellow metal (and any weakness there would likely be reflected in Ramsdens share price), but that doesn’t mean this isn’t a sensible long-term opportunity. | |

Cab Payments Holdings (LON:CABP) (£105m) | CAB has received approval to operate a representative office in New York. | ||

Synectics (LON:SNX) (£55m) | Five-year extension with major casino operator in Asia using SNX’s Synergy software platform. | AMBER/GREEN (Roland - I hold) [no section below] This is a useful and reassuring win, helping to support current market forecasts; house broker ShoreCap has left its FY25-FY27 estimates unchanged today. I remain moderately positive on this SIF folio stock, which continues to enjoy a high StockRank and Super Stock styling. | |

EMV Capital (LON:EMVC) (£11m) | Net loss of £3.7m, net assets -17.5% to £14.1m. Total AUM +33% to £98.5m. |

Megan's Section:

Ramsdens Holdings (LON:RFX)

Up 7% to 351p (£107m) - Interim results - Megan - GREEN

Ramsdens’ chief executive Peter Kenyon has a very nice set of results to chat to analysts and journalists about this morning. That doesn’t mean “you guys” haven’t been asking difficult questions, which apparently centre around two key areas: the rising price of gold and higher staff costs.

It’s not really surprising that these are the two biggest areas of concern for those interested in the company. The period for which these results relate saw the gold price rise 17% to $3,092/oz. It has since surged even further to an all time high of $3,564/oz.

The impact that has had on the company’s financial results is meaningful. Overall gross profits rose 20% to £27.1m in the first half of the 2025 financial year, with three of the four operating divisions enjoying a serious boost from the higher price of the yellow metal:

Purchase of precious metals gross profit £7.6m (+53%)

Jewellery £7.9m (+18%)

Pawnbroking £6.2m (+11%)

FX exchange £5.1m (+1%)

And as the gold price has swung upwards, Ramsdens’ share price has done so too, up 50% in the year to date to its own all-time high. For many investors, this company and its soon-to-be-acquired peer H&T Group, offer a lower risk exposure to safe haven gold.

So what happens when the gold isn’t marching upwards?

Mr Kenyon is comfortable with a floor more than 20% lower than its current price, but seems pretty confident that gold will continue its upward trajectory. An analyst he trusts thinks that with Donald Trump’s ongoing shenanigans, the gold price could hit $6,000/oz. And with H&T Group soon to leave the market, Ramsdens is likely to keep attracting the attention of investors who want exposure to gold without having to buy the asset directly, or invest in the miners.

Remember Albemarle & Bond?

The trouble with Ramsdens is, unlike H&T, the gold price exposure has a more meaningful impact on the company performance. H&T Group gross profits are about 7 times higher in the pawnbroking business compared to gold purchasing. At Ramsdens the figure is roughly equal. The last time a listed pawnbroker was overexposed to the price of gold, things didn’t end too well. In 2013, Albemarle & Bond had to melt down its gold to help repay its debts, it eventually went bust.

But Ramsdens is more diversified than its former peer and it has a well managed balance sheet with £7.37m in net cash and £1.9m of net debt including lease liabilities.

It is also conservative with its pawnbroking loans, offering roughly 60% of the value of the melted-down gold, but just 40% of the resale value of the jewellery. Almost 90% of its pawnbroking clients repay their loans in full and, of those that don't, about 50% of the assets are resold via the jewellery business and 50% sold through the precious metal purchase division.

Investment in further growth

Management employs a policy of reinvesting about half of its additional profits in further growth opportunities and returning the other half to shareholders. That’s why today investors are getting a 25% increase in the underlying dividend (to 4.5p) plus a 0.5p special. Mr Kenyon thinks that if the gold price trajectory remains, investors are likely to get another special at the end of the year.

Capex and store expansion has been more muted in the period. A decision taken amid the uncertainty of a new government and policy decisions. But now, investment will ramp back up again.

Terms have been agreed on three new stores and there are a further two being looked at by the legal department. In the medium term, the company wants to get back to between six and eight new store openings a year.

Impact of higher national insurance contributions

Higher national insurance contributions are expected to cost £800,000 a year and will have a five month impact on FY2025 annual numbers.

The company also plans to boost marketing expenditure to help showcase the value of its online and instore services. The company’s new, dedicated pawnbroking website was launched in November 2024 and has helped draw in new customers. Further marketing efforts are expected to bring in even higher numbers.

Even with the rising costs, the company expects full year pre-tax profits to exceed £15m. That's a 31% increase on last year.

Megan’s view:

I was ready to be sceptical about the company’s exposure to the gold price. Especially considering the FX business, which is the only one not to enjoy the boost from gold, is also the only one not to have had a very impressive first six months of the financial year.

I wouldn’t pin the investment case on the gold price going to $6,000/oz. But if it does, there is no denying that Ramsdens will benefit.

And if it doesn’t? This is still a well run, highly cash generative business with good prospects for growth both online and in store estate expansion.

The forecast dividend (including two 0.5p specials) is currently yielding 4.3% and the PE ratio, based on consensus forecasts prior to any upgrades is 11x. That’s not the incredible value that was on offer a couple of months ago, but it’s still hardly taxing.

Having smashed through its previous price target of 340p, broker Panmure Liberum has this morning updated its price target to 385p - up 10% from current levels. But even that feels conservative if the gold price keeps marching higher.

I have looked hard, but can find no reason not to stay GREEN.

WH Smith (LON:SMWH)

Up 3% to 1052p (£1.3bn) - Trading statement - Megan - AMBER

I’ve been quite negative about the recent string of announcements from WH Smith and it hasn’t gone down particularly well in the comments. So I would like to start by clarifying. I really like WH Smith. I like the fact that the high street division has received almost no attention (and very little financial support) in recent years as management invests in its far more prosperous travel division. And I like that the decision has been made to cull that lower performing division so all attention can be put on the section of the business where growth prospects remain.

Historically, it has had decent quality metrics, including double digit operating profit margins, a strong return on capital employed and impressive cash inflows. I am hopeful that with focus now solely on the travel business, these qualities can come back.

But there are also elements of the investment case that I don’t like.

The first is the relatively meagre valuation for the high street sale. An enterprise value of £76m is just 2.4x the annual trading profit of the division. And it’s going to bring in just £25m of net cash. The valuation hints of some desperation. Management was done with the division and wanted to make a quick sale. The new owner doesn’t even get to keep the name.

The second is the fact that the pace of sales growth in the North America region is declining. This was a big growth prospect for the travel business and it’s not currently living up to expectations. This morning, the company has reported like-for-like sales growth of just 2% in North America. That has been bulked up by new store openings and positive FX movements, but it’s still not great for the division which accounts for a fair chunk of the investment case.

The final (and most substantial) problem I have is the share buyback programme. In the first half of the financial year, the company reported a free cash outflow of £69m. Management blamed this largely on the seasonal effects of the travel business which led to a working capital outflow of £87m. But the company also reported a working capital outflow in the last set of annual results. Does working capital seasonality impact the whole year? The upshot is that the £23.3m share buyback programme currently being worked through is being funded by debt. It’s also going to eat up almost all of the cash inflow from the sale of the high street business. For a company looking to make its mark on the global travel market by investing in a substantial store rollout programme, this use of non-existent cash to fund a buyback programme is frankly bizarre.

Current trading

Is there anything in this morning’s update for investors to appreciate?

The UK travel business reported a 6% increase in like-for-like sales which is decent and represents growth across the three areas of interest (airports, train stations and hospitals). The company is increasing its investment in the quality of its store portfolio, which customers will no doubt appreciate. Better quality could potentially lead to even higher markups at these high footfall locations.

The North America business benefited from 10 new openings to send reported revenue up 7%. Airports is where a lot of the attention is focused in this business division and here the like-for-like revenue growth numbers were slightly better (+4%).

Growth is fastest in the far smaller ‘Rest of the World’ division where management points to ‘significant opportunities’.

Megan’s view:

On balance, the current decision making at WH Smith makes me a little nervous. A reduction in the number of lease liabilities once the high street business is disposed of will help the balance sheet, but this is still going to be a highly geared company. Management doesn't expect to fall back within its leverage target until August 2026 (I ask again, why on earth are they buying back shares!?)

I am also slightly anxious about the distractions of the ‘rest of the world’. That’s a big market, but so is North America and evidently there are still growth opportunities remaining in the UK. Perhaps a little more focus on the most exciting prospects might make more sense.

There is a value argument to be made. Shares are trading on 11.5 times forecast earnings and 3.8 times the book value (although it is more expensive than the price management negotiated for the high street business).

I will maintain that I like WH Smith and I hope that my doubts get proved wrong, but I am too nervous to keep our cautiously positive stance and move back to AMBER.

Roland's Section:

S4 Capital (LON:SFOR)

Up 5% to 27p (£166m) - AGM Statement - Roland - AMBER

S4Capital plc (SFOR.L), the tech-led, new age, new era digital advertising, marketing and technology services company

I am not sure if today’s statement could end up being a profit warning in disguise. S4 Capital has warned that net revenue will now fall this year, compared to previous expectations for a broadly flat performance. The company says this reflects the previously-announced reduction in revenue from a major client, which is still cycling through the numbers.

However, the company says that it is managing costs carefully and has left its full-year target for “like-for-like operational EBITDA” unchanged. This heavily-adjusted measure of profit is now expected to be “broadly similar to 2024, with a higher second half weighting than last year”.

The word “broadly” and warning of an H2 weighting are sometimes signs that a result could be weaker than expected, but management says this reflects the timing of revenue from new business wins. Encouragingly, these are said to include General Motors, Amazon and T-Mobile.

Another positive is the reported reduction in month-end average net debt, which has fallen by nearly 30% to £144m during the first five months of this year.

Less positive is the commentary on the external environment, especially in the tech sector, which generates nearly half S4’s revenue:

Market conditions in the first five months of 2025 reflect the continuing impact of, to say the least, volatile global macroeconomic conditions. As a result, clients remain generally cautious given the uncertainty, with technology clients, which account for almost half our revenue, in particular, continuing to prioritise capital expenditure on expanding AI capacity.

Updated Estimates: with thanks to Dowgate Capital, we have access to an updated note today confirming that earnings forecasts remain largely unchanged after today’s update:

FY25E EPS: 4.2p (previously 4.3p)

FY26E EPS: 5.2p (previoulsy 5.6p)

Roland’s view

As I discussed when I reviewed March’s results, SFOR has a concentrated customer base with heavy exposure to the tech sector and this remains a headwind.

I dislike the company’s focus on heavily-adjusted profit metrics, but when I reviewed the company’s full-year results I concluded that S4 did generate genuine free cash flow last year. This year’s reduction in net debt appears to provide further support for the company’s claim that its “liquidity and cash flow was much improved”.

Executive chairman Sir Martin Sorrell has not yet managed to repeat his historic success at WPP. However, it’s fair to say conditions in this sector have been very tough over the last couple of years and S4 is not the only company to have faced challenges.

On the assumption that FY25 profit expectations remain broadly unchanged, I think it’s fair to say that some value could be emerging here. Now that S4’s balance sheet appears to be under control, I can imagine that performance could improve meaningfully when cyclical conditions improve:

Stockopedia’s algorithms have also spotted possible signs of value, awarding a Contrarian style to the stock.

However, the ultra-low MomentumRank is perhaps a warning that a recovery is not yet in sight. Mark discussed this topic in more depth in a recent article.

Personally, I’d be inclined to stay on the sidelines a little longer here before considering an investment. But I’m tentatively going to upgrade our view to AMBER today, reflecting the company’s improved financial stability, valuation, and broadly unchanged outlook.

B&M European Value Retail SA (LON:BME)

Down 6.9% to 311p (£3.1bn) - Full Year Results - Roland - AMBER

B&M European Value Retail S.A. ("the Group"), a leading European variety goods value retailer, today announces its Preliminary Results for the 52 week financial reporting period to 29 March 2025 ("FY25").

Today’s results from discount retailer B&M are not all that terrible. But they do highlight issues we’ve been commenting on for a while and only provide rather broad and cautious guidance for the year ahead. I’m not surprised the market has taken a downbeat view ahead of the arrival of new CEO Tjeerd Jegen on 16 June, but I can't help thinking an opportunity may be emerging here.

Let’s take a look.

FY25 results summary: we already knew it had been a difficult year for B&M, thanks to a profit warning in February and a full-year update in April, both highlighting weak trading in the core UK business.

Today’s results are in line with February’s revised guidance:

Revenue up 3.7% to £5,571m

Adjusted operating profit down 1.8% to £591m

Reported pre-tax profit down 13.2% to £431m

Adjusted EPS down 6.7% to 33.5p

Ordinary dividends up 2% to 15.0p per share

Net debt up 5.9% to £781m

Sales rose last year, but the company admits this was “primarily driven by the contribution from new stores”.

However, these figures show the group’s operating margin falling to 10.2% (FY24: 11.1%), reflecting a 7% increase in operating costs. While weaker than previously, it’s worth remembering this is still far higher than the 3.8% operating margin achieved by Tesco last year.

B&M’s business model remains much more profitable than that of the big supermarkets. I calculate these results show a creditable return on capital employed of 18.8%, compared to 10.7% for Tesco last year. This superior profitability is why B&M has – historically – been able to pay such attractive dividends; I’ll look at this topic in more detail shortly.

UK: in the core B&M UK business, like-for-like (LFL) sales fell by 3.1%, while the smaller Heron Foods (a discount food retailer) saw total revenue fall by 0.6%.

The common theme seems to be disappointing sales of fast-moving consumer goods (FMCG) - e.g. branded food/drink & cleaning products. The company says that sales of these products were negative in both sales value and volume last year. I’d imagine this may be because the group’s core, lower-income customer base was shopping down to cheaper supermarket own brands and/or simply buying less.

Elsewhere in the UK business, sales of general merchandise in categories such as homewares, toys and seasonal products remained positive, with LFL growth for the year. My perception is that B&M remains a price leader in these markets and may also attract a broader range of shoppers for such products.

France: the group is also rolling out the B&M model in France. This division is less mature and performed better last year. Sales rose by 7.8%, including a 2.6% increase in LFL sales. The profit contribution from France was stable at £48m, reflecting higher costs and depreciation charges.

Balance sheet & cash flow: in the financial highlights at the top of today’s results, B&M reports the growth in its ordinary dividend but rather coyly doesn’t mention January’s £150m special dividend.

Crunching the numbers suggests to me that there could be a good reason for this – it was effectively paid using debt, rather than genuine surplus cash.

Total dividends declared for FY25 were £301.2m, including January’s special. The company’s own measure of free cash flow reported today was £311m, suggesting all payouts were covered by surplus cash.

However, my FCF calculation suggests free cash flow of £258m. The main difference between this and the company’s FCF figure is c.£60m of financing costs. I always include such items when calculating FCF, as in general they must be paid ahead of dividends.

The difference between total dividends and my measure of free cash flow is £43m, which almost exactly matches the £44m increase in net debt to £781m last year.

This represents a leverage multiple of 1.26x EBITDA, which is reasonable enough. But the group also has £1.4bn of lease liabilities, taking reported net debt to £2.2bn, or 2.56x EBITDA (FY24: 2.4x).

Today’s balance sheet shows net lease liabilities of £271m, perhaps suggesting some stores are currently loss-making. In this context, the leases can be seen as a debt-like liability, as they must be paid regardless of store profitability.

As we’ve commented before, B&M seems to use a little more debt than is really necessary – and more than I’d hope to see. I suspect the new chief executive may take a firmer grip on this. I’ve previously thought that a cut to the ordinary dividend might be needed, but today’s figures suggest to me that B&M may be able to reduce debt gradually by simply pausing any further special dividends.

Outlook: interim CEO (and permanent CFO) Mike Schmidt sounds cautious about the year ahead, but today’s commentary does seem to suggest that FY26 expectations are unchanged (my emphasis):

The Group recognises that FY26 will bring retail sector-wide challenges of increased minimum wage costs, higher employee national insurance and other taxes, and inflation on input costs. Work continues to reduce the impact of these pressures, through driving productivity improvements and sales volume growth. The impact of these additional costs and mitigations are reflected in the current range and median of analyst consensus operating profit forecasts for FY26.

Helpfully, B&M has included its view of current consensus forecasts in the footnotes of today’s results:

FY26E adj EBITDA: £621m (range: £569-646m)

FY26E adj op profit: £585m (range: £524-628m)

Consensus earnings estimates on Stockopedia suggest these figures could drop through to adjusted earnings of 34.3p per share, a slight increase on today’s FY25 figure of 33.5p.

After this morning’s drop, that leaves B&M shares trading on a P/E of nine, with a possible 4.8% yield if the ordinary payout is maintained.

Roland’s view

I took a negative view on B&M in February and April, but I am upgrading to neutral today.

These results have not revealed any fresh shockers and appear to be tentatively in line with existing consensus expectations.

Incoming CEO Tjeerd Jegen has an impressive CV and is very experienced in this sector.

While I’d like to see a reduction in debt, I don’t think leverage is likely to become problematic and the group’s continuing cash generation suggests to me that this may be achieved without needing a dividend cut.

B&M shares have fallen by 40% over the last year and are starting to look cheap to me. I share the algorithm’s view that this business could be worth considering as a contrarian pick at current levels. AMBER.

Discoverie (LON:DSCV)

Up 13% to 718p (£692) - Full Year Results - Roland - AMBER

discoverIE Group plc (LSE: DSCV, "discoverIE" or "the Group"), a leading international designer and manufacturer of customised electronics to industry, today announces its preliminary results for the year ended 31 March 2025 ("FY 2024/25" or "the year").

We haven’t covered this interesting-sounding company since April 2023, when Graham suggested it might be worthy of further research.

The share price at that time was 770p. It’s 712p at the time of writing, so it looks like Discoverie may not have delivered as much as investors had hoped for since then. However, with the stock up by more than 10% following today’s results, now seems a good time to take a fresh look.

A mixed year: Discoverie says that its sales fell by 3% last year as “an industry-wide inventory correction works through”. This is consistent with what we’ve heard from other listed companies in this sector and was reflected in the group’s working capital, with a reduction in both payables and receivables.

Fortunately, the company was able to manage costs carefully and improve its margins, supporting a 36% increase in operating profit to £42.4m. Performance was particularly strong in the Sensing & Connectivity (S&C) segment, where profit doubled to £23.7m, thanks to a mix of cost savings, contributions from acquisitions and a modest increase in sales.

S&C is said to benefit from demand recovery earlier in the cycle than the group’s other division, Magentics & Controls (M&C). This has yet to see a recovery in demand with organic sales down 11% last year and operating profit down 4% to £30.5m.

Balance sheet & profitability: Discoverie is a highly acquisitive business – today’s results note that the company has completed “28 carefully selected, well-integrated acquisitions over the past 14 years”. I suspect this is one reason why the group’s profitability seems rather average. Management may have paid a full price for the added growth, depressing returns on capital.

I calculate an operating margin of 10% and return on capital employed of 8.5% based on today’s results. Both are rather average figures, although last year’s operating margin does represent an impressive 3% improvement on the 7.1% achieved in FY24.

Buy-and-build models can generate a lot of value for shareholders when they’re done well. But I’m not sure the returns being generated here are quite high enough.

While Discoverie’s debt levels look manageable to me, the company does have some leverage and has also diluted shareholders somewhat over the last five years:

Underlying cash generation seems quite good to me, so I suspect the combination of debt and increasing share count indicates to me that the business hasn’t been profitable enough to fully self-fund its acquisitions (or that management has overpaid for some acquisitions).

Outlook & Estimates: CEO Nick Jefferies warns of some remaining uncertainty relating to tariffs and broader macroeconomic conditions. However, he sounds confident that cost savings made last year are sustainable and could support further improvement in margins.

The company has increased its medium-term adjusted operating margin target to 17%, from 14% previously.

Our flexible production model together with Group-wide operating efficiencies more than offset lower sales, protecting profitability through this stage of the cycle. This is a great strength of the Group, enabling growth in operating profits and margins in each of the last 10 years (in-line in the Covid year) and reducing earnings cyclicality. We see the potential to deliver further manufacturing efficiencies and commercial synergies across the Group and have upgraded our five-year operating margin target to 17%.

Broker Cavendish has kindly provided updated forecasts today, putting through a very modest upgrade:

FY26E adj EPS: 40.3p (previously 39.8p)

FY27E adj EPS: 41.1p (previously 41.0p)

These figures leave Discoverie shares trading on a FY26 P/E of 17.8, with a 1.8% dividend yield.

Roland’s view

Today’s note from Cavendish compares Discoverie’s valuation with that of larger industrial buy-and-build peers such as Halma and Diploma. Discoverie shares are indeed cheaper, but I would argue that this is justified by the group’s lower profitability.

Both Halma and Diploma have statutory operating margins of c.18% and generate mid-teens returns on capital employed – well above Discoverie's equivalent FY25 figures of 10% and 8.5%.

The compounding effects of these higher returns means that shares in the other two companies have comfortably outperformed those of Discoverie over the last decade:

In fairness, last year’s results do seem to point to a worthwhile improvement in profitability. With the business hopefully now emerging from a low point in the cycle, I can see scope for further organic improvements in profit and profitability.

However, broker forecasts are largely unchanged today and suggest fairly modest earnings growth of 4% in FY26 and just 2% in FY27. Further acquisitions seem likely to enhance growth, hopefully at valuations that will enhance shareholder value.

On balance I’m going to maintain Graham’s previous neutral view today. While the valuation has eased slightly, profits remain below the previous high watermark and near-term growth prospects seem tepid. I’d want to see evidence of organic growth and improved profitability to justify a premium valuation. AMBER.

See what our investor community has to say

Enjoying the free article? Unlock access to all subscriber comments and dive deeper into discussions from our experienced community of private investors. Don't miss out on valuable insights. Start your free trial today!

Start your free trialWe require a payment card to verify your account, but you can cancel anytime with a single click and won’t be charged.