Good morning! It's a relatively quiet day today, albeit with one or two nasty profit warnings.

The agenda is complete.

Update 12:15: I'm afraid that's all we have time for today, thanks for you all your comments.

Spreadsheet accompanying this report: link.

Companies Reporting

| Name (Mkt Cap) | RNS | Summary | Our view (Author) |

Shell (LON:SHEL) (£152bn) | EY’s 2023 and 2024 audits were non-compliant with SEC rules. Now restated with no changes. | ||

Direct Line Insurance (LON:DLG) (£4.0bn) | DLG shares will be suspended from 07:30 today. Holders will shortly receive new AV shares/cash. | PINK | |

Spectris (LON:SXS) (£3.8bn) | KKR has made a cash offer of £40. This is a 6.3% premium to the earlier Advent offer of 3,763p. | PINK | |

Greggs (LON:GRG) (£2.0bn) | PW: H1 rev +6.9% w/ 2.6% LFL growth. Slower in June. FY op profit now exp below 2024. | BLACK (AMBER - Megan holds) The improved trajectory in lfl sales growth has come to a sudden halt, to the extent that management now think op profits will be lower than last year. It’s hard to tell whether this is a short term blip or a more fundamental problem. I am wary enough to move back to neutral. | |

SSP (LON:SSPG) (£1.4bn) | SSP is IPO’ing its Indian JV, in which it will maintain a 50.01% stake. Price range c.£1.2bn. | AMBER (Roland) [no section below] This IPO is being carried out to allow SSP’s Indian JV partner to sell its stake in the Travel Food Services business. SSP is not selling and will not receive any proceeds from the IPO. However, SSP says the book cost of its 50.01% stake will be just £70.4m. If this IPO achieves its target valuation, SSP’s stake in TFS will then be worth c.£600m, or nearly half the group’s market cap. The StockRanks are neutral on SSP, but I wonder if this situation could be worth a closer look for interested investors. | |

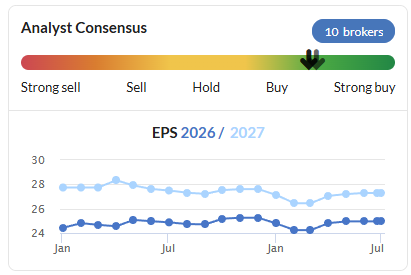

Bytes Technology (LON:BYIT) (£1.2bn) | Seen some deferred buying decisions. H1 op profit now exp below last year. FY update in Oct. | AMBER/RED (Roland) Bytes warns that a combination of internal and external issues has hit sales in H1 and is expected result in a fall in H1 profits. Full year guidance appears to have been withdrawn, with an update promised in October. I’m concerned by the change of tone since May’s results and the potential for a further de-rating, given the stock’s former High Flyer styling. For now, I think it makes sense to remain cautious. | |

Georgia Capital (LON:CGEO) (£706m) | Existing $50m buyback increased by $18m. Completes plan for GEL 300m of returns by end 2026. | ||

Capita (LON:CPI) (£379m) | Statement re H1 2024 segmental restatement & Amendment and Extension of RCF | £250m RCF extended by 12 mo. to 31 Dec 27 with £50m accordion. FY25 guidance unchanged for broadly flat rev w/ higher op margin. | |

Secure Trust Bank (LON:STB) (£152m) | Vehicle Finance to be run off. Pro forma FY24 PBT would be £56.6m (prev £39.1m) and +8% ROAE. | AMBER/GREEN (Roland) STB’s Vehicle Finance unit was heavily loss-making last year and accounts for more 30% of the group’s cost base. Today’s decision suggests to me that management can’t see a clear path to an attractive level of profitability. Given the more difficult regulatory and legal environment for motor finance at the moment, I think STB’s decision looks sensible and has the potential to improve overall returns. With a 50%+ discount to book value and 4%+ yield, I am happy to remain moderately positive here. | |

Avacta (LON:AVCT) (£118m) | FAP-Dox progressing in Phase 1b studies, FAP-EXd preparing for Phase 1 trial in Q1 2026. | ||

Topps Tiles (LON:TPT) (£67m) | Q3 sales +10.1%, YTD +6.1%. LFL sales +4.4% YTD. Confident can deliver “meaningful” FY profit growth. Zeus forecasts unchanged today: FY25E EPS: 3.3p | AMBER/GREEN (Roland) [no section below] | |

Metals One (LON:MET1) (£56m) | Acquired Uravan project in Colorado for $50k +500k new MET1 shares. 10yr explo lease. | ||

| K3 Business Technology (LON:KBT) (£39m) | Proposed Tender Offer, Cancellation & Notice of GM | Proposed £29m tender offer at 85p to return Nexsys proceeds. Will then be delisted from AIM. | |

Ariana Resources (LON:AAU) (£26m) | Identified 500m long gold anomaly, “geochemically significant”. In priority area for drill testing. | ||

Empresaria (LON:EMR) (£13m) | Possible offer (see May) of 10pps + 50pps in 3y loan notes. Already has 57% shareholder support. | PINK | |

Blencowe Resources (LON:BRES) (£13m) | Completed 3 deep drill holes at Northern Syncline. Confirm mineralisation to below 100m. |

Megan's Section

Greggs (LON:GRG)

Down 14% to 1696p (£2bn) - Trading statement - Megan - BLACK/AMBER

I don’t like it when non-meteorological companies blame the weather for a poor sales performance. Summer is warmer than spring, winter is colder than autumn. We’re getting a few more extreme events every year but, by and large, it’s the same pattern that we all learnt when we painted pictures of the trees in nursery school.

And yet, it’s the warm weather which Greggs’ management is blaming for a slowdown in like-for-like store sales in June.

I am also frustrated by the mathematical challenge presented by the dates in these announcements:

On 20 May, we had an announcement saying like-for-like sales growth for the first 20 weeks of the year (to 20 May) was +2.9%

Today’s trading statement covers the first 26 weeks of the year (to 28 June) and reports that lfl sales are now up 2.6%

But also today’s statement says that the performance in the first 11 weeks (to 17 May) was good and the trend continued throughout the rest of May

And it has actually just been June (i.e. the last four weeks) when trading has been more disappointing

My interpretation of this muddle is that in May, management were tentatively hopeful that the slowdown in like-for-like sales reported in 2024 and early 2025 had come to an end and perhaps jumped the gun a bit on reporting this to the market.

If they had waited until now to report a 2.6% increase in like-for-like sales to the market, we’d have probably been delighted. Like-for-like growth at 2.6% is still a welcome turnaround from the 1.7% reported in January and even the 2.5% growth reported in Q4 of 2024.

I am still bothered by the blame being pinned on the weather (although I must admit that when I was in the Greggs on the A12 near Witan on Friday, the lady serving me my sandwich did have a little moan about the heat). My fear is that there is only so much marketing the mega-machine at Greggs HQ can do to encourage the British public to ditch their McDonald’s, Starbucks and M&S sandwiches and lurch for a sausage roll instead.

Growth opportunities are more readily found in the store roll-out programme, which remains on track. In the first half, the company opened 87 new stores and says it is on track for between 140 and 150 net openings for the full year.

Higher costs lead to profit slowdown

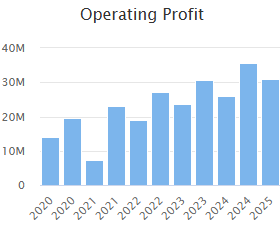

The combination of weaker sales growth and planned store refurbishment means operating profits are expected to be slightly lower than the first half of last year when management announces its full interim results on 29 July. (In H1 2024 operating profits were £75.8m off £960m of revenue).

With total interim revenues of just over £1bn in the first half and operating profits now forecast to be below £75.8m, we’re going to see another disappointing erosion of operating margins.

In the second half, the impact of higher national insurance contributions will also have more of an effect on costs, but management says its “mitigation measures” should enhance the second half performance. Still, annual operating profits are also expected to be down on last year’s £195m.

Megan’s view:

I am really on the fence here.

Evidence from studies suggests that the worst thing to do in the event of a profit warning is nothing. Either take advantage of the share price weakness and double down, or cut your losses. Being caught in uncertainty is a mistake.

On the one hand, I really don’t think today’s announcement is as bad as all that. Further weakness in operating margins is disappointing, especially as some of that seems to be coming from the refurbishments which can’t be a surprise to anyone.

On the other, this is a change in trajectory. And it was the improved trajectory in like-for-like sales growth which made me add Greggs to my portfolio in the first place. Any change in the investment case is a reason to cut and run.

I am going to sit on this today and not make any rash decision, but my hunch is that Greggs might be getting replaced in my portfolio. I really don’t want stocks that make me uneasy and there are a few things in this announcement which just don’t sit right. AMBER

Roland's Section

Bytes Technology (LON:BYIT)

Down 24% to 383p (£922m) - AGM Statement - Roland - AMBER/RED

Bytes Technology stock opened down by 25% this morning, after the company warned of deferred buying decisions and a drop in H1 operating profit. Perhaps more worryingly, Bytes appears to have withdrawn its full-year guidance, instead promising an update with its interim results in October.

Commiserations to shareholders. I suspect many are looking at their screens and wondering what’s changed in the seven weeks since the company issued FY25 results in mid-May, when management confidently guided for “high single-digit operating profit growth” in FY26.

Today’s AGM Statement is relatively brief and I don’t have access to broker notes for this company. So what I’ve tried to do is to identify the key points and check back to the full-year result in May to see what was said on these topics at that time.

What’s gone wrong?

Bytes’ financial year starts on 1 March, so today’s commentary covers the first four months of the year.

Deferred buying decisions: the company says some customers have deferred buying decisions due to macroeconomic conditions, especially in the corporate sector.

In May, Bytes said “sustained demand in structural growth areas” underpinned confidence for continued strong sales growth in FY26.

Restructuring sales teams: the company has reorganised its corporate sales from generalist teams into segments based on customer size (e.g. enterprise, corporate, mid-market). This process seems to be taking longer than expected, although it is expected to deliver positive results eventually:

While this transition has resulted in a longer than expected readjustment period, it positions us to deliver more relevant solutions and drive sustainable services annuity income growth during the second half of the financial year ending 28 February 2026 and beyond.

This reorganisation was mentioned in May but no comment was made on any potential impact.

Microsoft enterprise sales incentives: apparently some changes made this year have had an adverse impact on H1, due to high levels of public sector renewals in March/April and June.

This was mentioned in May’s results, but again the impression I got was that Bytes had been able to plan ahead and mitigate this impact:

This year, Microsoft communicated a particular amendment to its enterprise agreement program, reducing certain transactional incentives, in advance of it taking effect in January 2025. This provided time for us to prepare and to realign our software and services offerings, as we have often done in the past […]

Updated outlook

As a result of all these factors, Bytes has issued the following guidance for H1 today:

H1 gross profit at a similar level to last year

H1 operating profit “marginally lower” than last year

Expect normalised growth in both metrics in H2

Update on FY26 guidance will be provided in October

For context, consensus forecasts prior to today suggested Bytes would deliver c.14% revenue growth and 9% EPS growth this year.

Roland’s view

A slowdown in corporate sales may not be good news for Bytes. Although the public sector generated 65% of the group’s gross invoiced income last year, higher margins on corporate sales mean that the private sector contributed 65% of gross profit.

The issues raised in today’s update also suggest to me that operational failings or miscalculations may have worsened the impact of macroeconomic trends. I can’t help wondering if the process of restructuring the corporate sales team may have disrupted some corporate sales wins.

In the absence of updated forecasts, I’ve taken a stab at estimating what level of operating profit might be suggested by today’s statement.

Looking at the numbers, Bytes profits have consistently been weighted to H1 in recent years:

The H1/H2 operating profit split last year was £35.6m/£30.8m.

If we assume that today’s guidance for “marginally lower” H1 operating profit suggests a figure of perhaps £34m, then today's guidance for “more normalised growth” in H2 might suggest a figure of perhaps £32-33m.

A result like this would leave FY26 operating profit broadly unchanged from last year’s result of £66.4m.

This would be a downgrade from previous FY26 guidance of “high single-digit operating profit growth”, but perhaps not a disaster in the scheme of things.

I suspect the underlying reason for today’s big share price fall was that Bytes’ shares were priced for strong growth, on a P/E of 20. This kind of High Flyer styling isn’t sustainable without regular doses of positive news:

The combination of a de-rating and a likely earnings downgrade has resulted in a sharp fall – but Bytes shares are still trading on 17x FY25 earnings.

Private investors will have to wait to see what changes to consensus forecasts feed through in the coming days. I’m concerned by the company’s decision not to issue any updated full-year guidance today.

Statistically, we’ve found that a company’s first profit warning is often the start of a longer period of underperformance.

For now, I have no choice but to downgrade our view on this stock to moderately negative. AMBER/RED.

Secure Trust Bank (LON:STB)

Up 8% to 861p (£164m) - Strategic pivot to increase Group ROAE - Roland - AMBER/GREEN

Secure Trust Bank PLC ("STB" or the "Group"), a leading specialist lender, announces a pivot in its strategy away from Vehicle Finance that, over time, is expected to improve its Return on Average Equity ("ROAE").

Motor finance has become a difficult and fraught area for UK lenders recently due to a range of regulatory and legal interventions. Secure Trust Bank has decided to cut its losses and exit this sector altogether, in order to focus on its more profitable property and business lending operations.

With immediate effect, STB has decided to stop Vehicle Finance lending and put its existing loan book into run off. This division generated a pre-tax loss of £21.8m last year on net lending of £558m. Stripping this out would have increased the bank’s overall return on average equity by 8% last year, according to today’s update.

One problem here seems to be that Vehicle Finance carries unusually-high overheads. This division reported operating costs of £31.6m last year, or 30% of total costs. This is a higher share than for any of the group’s other (profitable!) lending lines. I’d guess this might partly be due to a relatively large number of small loans, creating a lot of overhead dealing with borrowers and brokers.

The average remaining Vehicle Finance loan length is 37 months and the longest is 60 months, so winding this unit down will be a gradual process. But management expects to achieve £25m of cost savings by 2030, with 284 roles at risk including 78 in FY25.

Roland’s view

This decision looks sensible to me. Motor finance lending seems to have got tougher and Secure Trust’s lack of profitability in this market means it seems prudent to exit if there is no clear line of sight to an attractive level of profitability.

Secure Trust has a new CEO starting later this year who has promised to prioritise returns from the business.

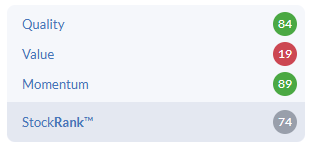

With the stock still trading more than 50% below its book value, there should be some scope for a re-rating here if this goal can be achieved.

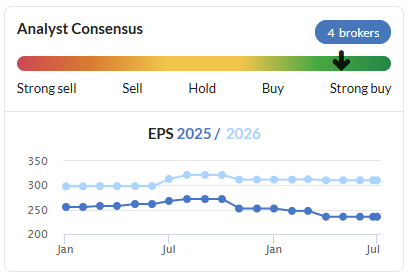

Broker forecasts suggest solid earnings growth over the next couple of years:

With a well-supported 4% dividend yield and big discount to tangible book, I think the risk-reward balance continues to look reasonably attractive here. While there will always be macro and regulatory risks, I’m happy to maintain our moderately positive view today. AMBER/GREEN.

See what our investor community has to say

Enjoying the free article? Unlock access to all subscriber comments and dive deeper into discussions from our experienced community of private investors. Don't miss out on valuable insights. Start your free trial today!

Start your free trialWe require a payment card to verify your account, but you can cancel anytime with a single click and won’t be charged.