Good morning!

Spreadsheet accompanying this report: link

14:00 - All finished there, see you tomorrow.

Companies Reporting

| Name (Mkt Cap) | RNS | Summary | Our view (Author) |

| AstraZeneca (LON:AZN) (£162bn) | Baxdrostat met primary endpt in BaxHTN PhIII trial | Showed statistically significant reduction of systolic blood pressure compared w/ placebo. | |

| GSK (LON:GSK) (£57.5bn) | GSK submits Arexvy for adults 18-49 AIR to FDA | Supported by Phase IIIb data, FDA decision expected H1 2026. Potentially large market. | |

DCC (LON:DCC) (£4.7bn) | Selling UK/Ireland Info Tech unit to PE group Aurelius for £100m. FY25 op profit c.£6m. | ||

South32 (LON:S32) (£6.8bn) | Uncertainty over electricity supply post-March 2026, when current contract expires. Impairing assets. | ||

Ashmore (LON:ASHM) (£1.20bn) | AUM +3% to $47.6m at 30 June 25. Investment performance +$2.2bn, net outflows $0.8bn. | GREEN (Roland) | |

Supermarket Income REIT (LON:SUPR) (£1.0bn) | Acquired Tesco Ashford for £54.1m, net initial yield 7%. 9yr unexpired lease, index-linked rent. | AMBER/GREEN (Roland - I hold) [no section below] This looks like a sensible acquisition to me, adding to the group’s core UK portfolio of Sainsbury and Tesco supermarkets at a reasonable purchase valuation. It’s been funded with proceeds from a recent JV with Blue Owl Capital. Management believes supermarket property valuations are attractive at current levels and notes that one growth route under consideration is adding new tenants (presumably other supermarket operators) to the portfolio. I’m leaving our view unchanged as I continue to see this as an attractive property income stock. | |

Filtronic (LON:FTC) (£360m) | Supplying modules for electronic sensor system. Delivery due from mid-calendar 2026. No change to Cavendish forecasts for FY26 (y/e 31 May 26). | AMBER/GREEN (Roland) [no section below] | |

Elixirr International (LON:ELIX) (£352m) | H1 25 revenue +35%. | AMBER/GREEN (Roland) [no section below] | |

Petrotal (LON:PTAL) (£342m) | H1 production avg c.22,160 bopd (+20% YoY). YTD prod in line, but delays with Block 131 drilling prog. | ||

Saga (LON:SAGA) (£263m) | 7yr partnership with NatWest Boxed to offer a range of savings products targeting over 50s. | ||

Serabi Gold (LON:SRB) (£144m) | Q2 gold production 10,532oz (+17% YoY). Net cash of $24.6m at 30 June 25. On track for FY25 prod guidance of 44-47koz. | AMBER/GREEN (Mark) | |

Beeks Financial Cloud (LON:BKS) (£124m) | Contracts valued at $10m over 4-5 year signed in June. Revenue will be recognised in FY25 & FY26 , contributing to a strong start to FY26. FY25 Trading (subject to audit): Revenue +25% to £35.5m, u/l EBITDA +29% to £13.8m, u/l profit PBT +41%. Broker forecasts unchanged. | AMBER (Roland) | |

Jadestone Energy (LON:JSE) (£110m) | 900m high-quality reservoir (double previous Skua wells). Initial production rates to exceed 3.5kbopd pre-drill estimates. Total capital cost of the Skua-11ST well is now US$96-100m up from US$70m. | AMBER (Mark - I hold) [no section below] | |

IG Design (LON:IGR) (£73m) | Three-year refinancing with HSBC and NatWest for £40m structured as a Recourse Receivables Finance Facility. The Group's UK overdraft facility will be cancelled upon commencement of this new facility. | AMBER (Mark) [no section below] | |

Braemar (LON:BMS) (£70m) | “The South Africa launch takes Braemar's global footprint to 19 offices across 14 countries.” | ||

Pulsar (LON:PULS) (£54.2m) | 25H1 Revenue flat, Adj EBITDA +19%, net debt £4.2m (24H1: £3.2m). “Given the momentum being shown across the regions, the Group continues to trade in line with the Board's expectations.” | ||

CML Microsystems (LON:CML) (£49m) | Sale of surplus non-operational land expected to generate total cash proceeds of £7 million. £4m immediately & the balance of £3m during March 2026. | AMBER/RED (Mark) [no section below] | |

Helix Exploration (LON:HEX) (£48.1m) | Significant helium gas-shows up to 948ppm (190x background) in drilling mud. Ready for testing. | ||

ECO Animal Health (LON:EAH) (£38.6m) | Revenue down 11% to £79.6m, adj EBITDA down 9%, in line with (previously reduced) expectations, EPS +61% 2.49p. Net cash £25m (40% held outside of China.) | AMBER (Mark) These results are poor, but in line with previous guidance. The outlook is rather vague and without updated brokers’ notes we have to assume this means in line. However, this puts them on a high forward P/E, and their preferred measure of adjusted EBITDA is largely meaningless for a company that capitalises so much R&D spend. The bull case remains that new products take-off or they slash R&D costs if they don’t. However, valuing this requires specialist knowledge that few investors will possess. | |

Touchstone Exploration (LON:TXP) (£34.6m) | 25Q2 gross production averaged 3,023 boe/d (1,965 boe/d net), approximately 17.05 MMcf/d of natural gas and 181 bbls/d of NGLs. | ||

Ariana Resources (LON:AAU) (£28.7m) | Tavsan Mine (23.5% Ariana Resources interest) is expected to achieve operational status from late July 2025, ready for the commencement of gold production from the heap-leach. | ||

Vast Resources (LON:VAST) (£14m) | “...positive progress has been made in the primary beneficiation process of preparing the diamond parcels for tendering.” | ||

Empresaria (LON:EMR) (£11m) | Hendriks Family signed a non-binding LOI confirming their intention to vote in favour of the Takeover Offer. Now 70.14% support for the offer. | PINK (Mark) [no section below] | |

| Pennant International (LON:PEN) (£11m) | Global Partner Appointed & Auxilium Presentation | Agreement with Siemens to offer GenS as part of Teamcenter. Appointed Win-Tek and Eva Aviation as sales representatives for Auxilium in South Korea and Japan, respectively. | AMBER/RED (Mark) [no section below] |

Roland's section

Beeks Financial Cloud (LON:BKS)

Down 1% to 210p (£141m) - Significant Proximity Cloud Wins and Trading Update - Roland - AMBER

Beeks Financial Cloud Group plc (AIM: BKS), a cloud computing and connectivity provider for financial markets, is pleased to announce the signing of c.$10 million of Proximity Cloud contracts in June as well as to provide an update on trading for the year ended 30 June 2025 (FY25).

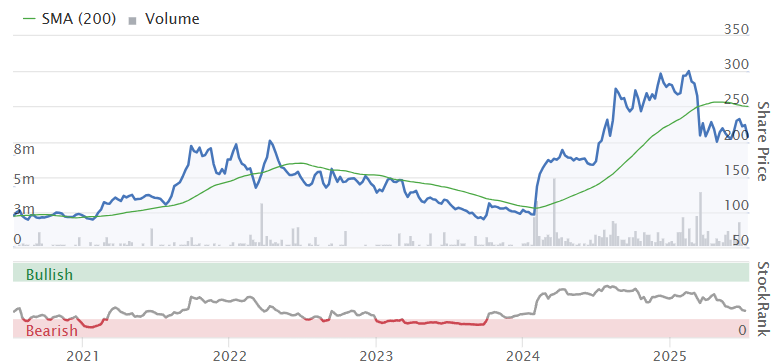

Today’s contract win and full-year trading update from this low latency cloud hosting provider has been given a cool reception by the markets. We’ve been neutral on this in recent months and I notice that the Stockopedia algorithms have recently reclassified Beeks as a Falling Star. That’s a potential reversal of its former High Flyer status that – statistically – might signify the stock is entering a more prolonged period of underperformance.

Let’s take a look at the details of today’s update to see if a cautious view is justified, or if the stock’s recent de-rating could signal a potential opportunity.

Contract wins

Beeks reports $10m of contracts signed for its Proximity Cloud service, which is hosted in clients’ own trading environments. Management says that June was a “record month” for Proximity Cloud.

Today’s contract wins are said to comprise “four-to-five year contract wins and renewals for brokerage and fintech firms” in the UAE and Europe, with revenue to be recognised in FY25 and FY26.

Unfortunately Beeks does not specify the split between new business wins and contract renewals, so this information gives us no insight into the growth implied by the headline $10m figure.

While renewals are obviously positive, the stock’s forward P/E of 24 and track record of heavy capex implies expectations about growth. It would be useful to know if the Proximity Cloud service was attracting sizeable new clients.

Full-year trading update

Today’s trading update covers the year ended 30 June 2025 and looks a little mixed to me.

The headline numbers show strong growth over the last year, but appear to be below Stockopedia consensus and broker forecasts:

Revenue up 25% to £35.5m

Underlying EBITDA +29% to £13.8m

Underlying pre-tax profit up 41% to £5.5m

Net cash of £6.96m (FY24: £6.58m)

For comparison, Stockopedia shows consensus revenue for FY25 of £37.3m, while broker Canaccord Genuity had revenue and adjusted pre-tax profit figures of £37.8m and £6.0m respectively. Paid research provider Progressive has FY25 figures of £36.8m and £5.7m.

In fairness, it looks like the revenue miss is largely accounted for by a one-off customer delay in Mexico that is outside Beeks’ control:

Within the FY25 results, £1.3m of revenue related to the Exchange Cloud contract with Grupo Bolsa Mexicana de Valores (BMV), announced on 18 February 2025, has been deferred into FY26 due to constraints at the Mexico City Disaster Recovery data centre, delaying the launch of one of the two services into H1 FY26. The primary site has gone live in recent weeks.

On balance, I don’t think today’s trading update flags up any major concerns. But I do think it’s worth noting what the company is saying about the composition of its underlying growth:

ACMRR (annualised committed monthly recurring revenue): this important growth measure only rose by 5% to £29.5m in FY25, compared to +7% in H1. The company says this was due to a reduction of £0.7m in AMCRR when a client switched from a Private Cloud (hosted by Beeks) to a Proximity Cloud solution (hosted in clients’ own data centres).

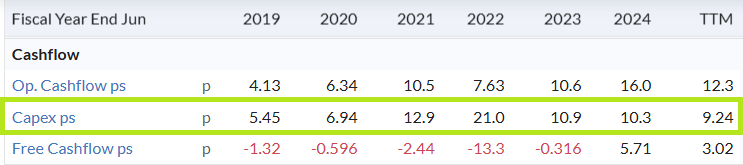

What this does remind us is that Beeks' business is an odd mix of software and equipment leasing. This means margins and cash generation are both weaker than we’d expect to see in a true software-as-a-service business.

As we’ve commented many times before, the company has to invest significant amounts in hardware upfront before reclaiming this revenue in monthly payments from its customers:

This is evident in today’s trading update. Despite a 25% increase in revenue and 46% increase in adjusted PBT, Beeks’ net cash was almost unchanged at the end of the year. This suggests that the additional cash generated from higher profits was required to support ongoing capex.

Outlook & Estimates

CEO Gordon McArthur sounds positive about the year ahead but stops short of issuing any concrete guidance:

We enter FY26 with ongoing confidence in our ability to convert the strong pipeline of opportunities across our offerings.

There are no changes to either FY25 or FY26 forecasts from Canaccord and Progressive today.

FY25 forecasts have been left unchanged by both brokers, despite the company’s update suggesting a slight miss.

FY26 forecasts are unchanged pending the receipt of more detailed guidance when October’s full-year results are published.

Given that Beeks is only covered by two brokers, I think we can assume that consensus estimates remain unchanged today:

FY25E EPS: 7.6p

FY26E EPS: 8.8p

These estimates put Beeks on a FY25E P/E of 28, falling to a P/E of 24 for the current (FY26) financial year.

Roland’s view

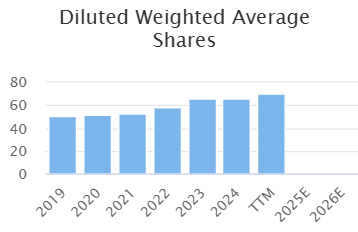

I remain slightly concerned by Beeks’ capital-intensive business model. Supporting this has required regular equity raises since its 2017 listing, albeit shareholders have still done well.

Profitability has also remained decidedly average at a statutory level:

However, I’m hopeful that last year’s increase in year-end net cash may signify that the business is now large enough to have become self funding, without needing further equity raises. Profitability might also improve with higher utilisation and economies of scale.

The ongoing evolution of its revenue model to include a higher proportion of revenue-sharing may impact cash generation, although I don’t know the business well enough to evaluate this (broker Progressive also comments today that this change makes revenue “more difficult to forecast”.

Is this a profit warning? The combination of today’s update and unchanged forecasts beg the question – as posed by Rusty2 in the comments – is today’s update from Beeks a profit warning?

With slight reluctance, I am going to take the view that this is not a profit warning and leave our neutral view unchanged today. However, I’ll caveat this by saying that I think the shares remain fully valued, so any evidence of slowing growth or downgrades to forecasts could prompt a sharp de-rating.

Personally, if I was considering investing, I might be inclined to wait until after the FY25 results are published.

Ashmore (LON:ASHM)

Up 2% to 171p (£1.2bn) - Trading Statement - Roland - GREEN

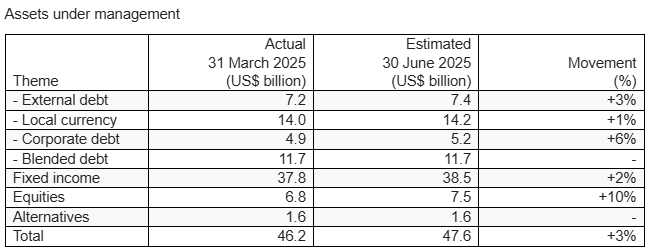

Ashmore Group plc ("Ashmore", "the Group"), the specialist Emerging Markets asset manager, announces the following update to its assets under management ("AuM") in respect of the quarter ended 30 June 2025.

Emerging Markets specialist Ashmore appears to have benefited from a strong recovery in equity prices during the second quarter, just like many UK investors!

Joking aside, today’s quarterly update shows a recovery in assets under management in the final quarter of the company’s financial year, which ended on June 30.

Total assets under management rose by 3% to $47.6m during the quarter. Equities and fixed income were the biggest contributors in monetary terms, while corporate debt also performed well in percentage terms, although it’s a smaller share of overall assets:

Market movements vs flows: while positive market movements are a good thing, what asset managers really need right now is evidence of inflows of investor cash.

Unfortunately net flows remained negative for Ashmore during Q4, with all of the positive performance being driven by investment performance:

Investment performance/market gains: +$2.2bn (Q3 25: +$1.3bn)

Net outflows of $0.8bn (Q3 25: $3.9bn net outflow)

While total assets under management remain below the $48.8bn seen at the end of 2024, the improving trend is welcome. Both investment performance and flows improved significantly in Q4, on a sequential quarterly basis.

Within the company’s different themes, there was some variation in performance in Q4:

Equity net inflows were positive

Flows were flat in external debt and alternatives

Flows were negative in blended debt, local currency and corporate debt

Ashmore says the emerging market indices it follows rose by between 2% and 12% during the quarter. This leaves us to wonder how much of the 10% increase in equity AUM relates to market movements, and how much to equity inflows. Did Ashmore’s equity products outperform their benchmarks?

Outlook

Founder CEO and 29% shareholder Mark Coombs can always be relied upon for a glass-half-full commentary. But in this case I think his optimism may be justifiable. Coombs’ comments certainly seem to suggest that Ashmore could be well positioned at the moment:

Consequently, investors are beginning to rebalance portfolios away from heavily overweight US positions towards more attractively valued asset classes, including those in EM. While recent EM mutual fund inflows have been concentrated in exchange traded funds, previously this has been a precursor to broader institutional behaviour.

Roland’s view

Graham usually covers Ashmore and was GREEN on this FTSE 250 stock in April. While the 10% dividend yield is not covered by earnings, this company has a very strong balance sheet – Graham estimates over £700m of tangible equity in April.

Founder ownership is a positive factor, in my view, and it’s certainly true that the outperformance of US stock markets has made life very difficult for many other institutional investors over the last few years.

I am cautiously encouraged by today’s statement. If Ashmore could achieve positive net inflows and investment performance, I think we could see a decent re-rating here.

While there’s no guarantee this will happen – outflows may continue – I think the value on offer here is potentially attractive. I am happy to leave our positive view unchanged today.

Mark's section

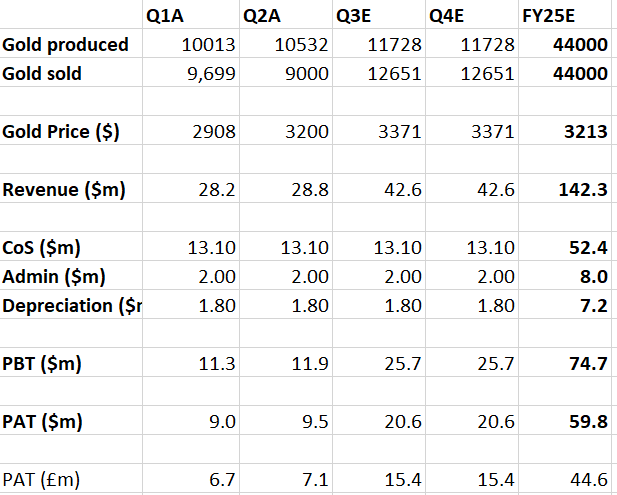

Serabi Gold (LON:SRB)

Up 4% to 198p - Q2-2025 Production Results & Operational Highlights - Mark - AMBER/GREEN

This morning we get Q2 production figures from this popular gold miner. Strangely they issued these at 6:30am instead of the more normal 7am giving investors more time to digest them. However, they also coded them as “General” so some investors may have missed them. Here is the key figure:

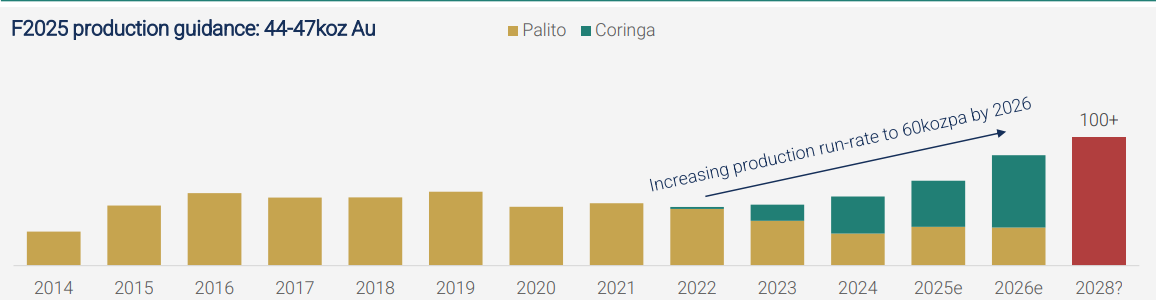

Gold production of 10,532 ounces, a 17% increase from Q2-2024

This sounds impressive. However, it is worth noting that this is only up around 5% on Q1, and someway below the run-rate needed to hit their 44-47 koz production target for the year, which they re-iterated today. This is what I calculated they need to do to hit the midpoint of their production guidance after the Q1 production results:

Here is what it looks like today to hit the same figures:

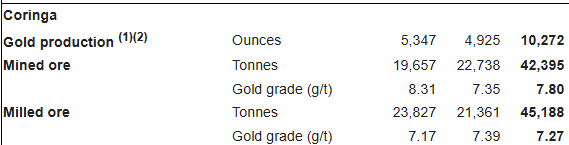

Slightly worrying is that Coringa has seen production drop in the quarter:

This is where all of their production growth is forecast to come from:

I’m not sure this is fully explained in the narrative, where they say:

A 17% increase on the corresponding quarter in 2024, and most pleasing within these numbers was the grade improvements at both Palito and Coringa. Palito plant feed grades year-to-date are 27% improved on the 2024 average, whilst Coringa plant feed grades improved 12%...At Coringa, the ore sorter has now been operational for 6 months with excellent performance. During this period, we have taken advantage of favourable economics and have been using the ore sorter to process low grade ore stockpiled since the mine opened, whilst higher grade ROM is transported directly to the Palito plant. By doing this we can produce more ounces from Coringa this year than originally planned.

They say these production figures are ahead of expectations and that they will see the ramp up in Q3 & Q4:

Year-to-date, that gives total gold production of 20,545 ounces, slightly above budget and leaving us tracking guidance. Development rates were also excellent, 10% improved on the first quarter…Our production profile will see greater quarterly production in Q3 and Q4 to reach guidance.

I have no reason to doubt these management statements, but I also don’t see why we shouldn’t treat this any differently to a trading company that says that they will be significantly H2-weighted and apply a suitable risk factor.

As this is just a production update, we don’t get an update on the gold sold in the quarter. However, with the net cash increasing $3.5m, versus $4.9m in Q1 where the spot gold price has averaged $3,200/oz in Q2, vs $2908/oz received n Q1, it does suggest that sales are a little behind production for the quarter (or costs increasing):

Net cash at quarter-end (after interest bearing loans and lease liabilities) of $24.6 million (Q1-2025: $21.1 million).

Sales versus production to to be largely just be issues of timing, and if the gold price has risen in the quarter (as it has) this can actually be a benefit. Updating my simple model here, but with caution on the production figures by taking the bottom end of the guidance range, gives the following result:

It is the strength of the gold price that is helping here and assuming current spot prices are a good estimate for future prices, this is a healthy beat on current expectations:

Even assuming some quarterly cost inflation, yields a PAT figure some 10% above current estimates:

Meaning this continues to look cheap, despite recent rises:

Mark’s view

I am naturally sceptical of any company that has a strong H2-weighting, even more so in the mining sector where operational slip ups are par for the course. However, even assuming Serabi only manage to meet the lower end of their production guidance, the current strong gold price means that they look on course to still beat current broker consensus. The risks I mentioned when I last looked at this on the DSMR remain, namely:

The production uplift required in the remaining quarters of FY25 suggests there is work to do to hit production forecasts for the full year.

Most of the phenomenal results so far have been driven by the gold price. While the company have done well to keep costs flat in an inflationary environment, they have largely been passengers in these strong results. This means that they will remain passengers if the gold price falls significantly in the future.

When companies produce windfall profits as a result of commodity rises, there is always the risk of governments wanting a bigger slice of the windfall via increased taxation or other means.

However, they are still fundamentally very cheap, and I am happy to keep my AMBER/GREEN stance.

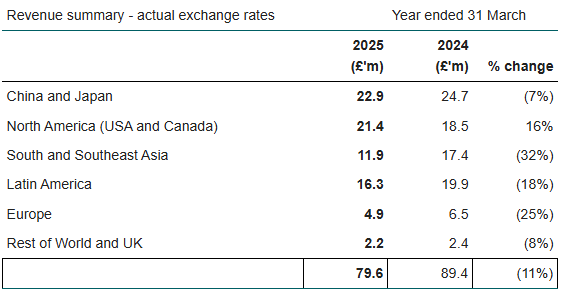

ECO Animal Health (LON:EAH)

Up 10% to 62p - Final Results - Mark - AMBER

On the surface there looks to be little to write home about here:

Revenue in-line and adjusted EBITDA in-line with revised market expectations following strong second half to the year

Group sales of £79.6m (2024: £89.4m)

Pretty much all areas of the business are performing badly, apart from North America (which carries its own risks at the moment!):

Profitability:

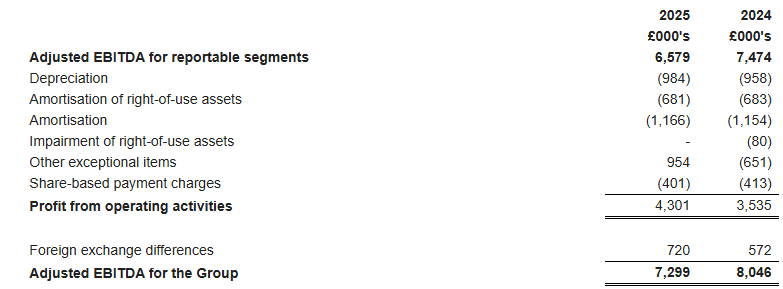

Things look better at the profitability level:

However, this is largely due to cost-cutting, lower (expensed) R&D and a one-off gain from selling non-core assets.

Their preferred measure is presumably EBITDA as they mention this 30 times, and say:

EBITDA is a key performance measure for the Group; the removal of amortisation, depreciation and other non-cash charges to profit provides a good indication of the underlying cash trading performance of the business.

However, this looks little better than the sales performance:

Adjusted EBITDA of £7.3m (2024: £8.0m), in line with consensus

In my opinion, adjusted EBITDA is a pointless measure here. The issue isn’t just the exceptional items and SBP charges:

But they are spending significantly more than they are amortising on intangibles:

Cash flow:

Looking at the cash flow statement, we have:

Operating cash flows before movements in working capital of £7.3m

Finance costs of £0.2m

Income Tax £1.5m

Net cash used in investing activities £4.6m

Lease interest & principal £0.9m

Meaning free cash flow before movements in working capital is just £0.1m. Of the cash that they do have, a significant proportion remains in China JV’s:

Net cash at the end of the period £25.0m (2024: £22.4m), reinforcing the Group's strong balance sheet with 40% of cash held outside China (2024: 36%)

This, together with the lack of sustainable free cash flow is presumably why no dividend is paid this year despite this net cash figure. Chinese JV’s also add to the risk here, not just on the cash front.

Outlook:

The outlook is a little vague, with no specific mention of trading figures, nor comparisons with market expectations:

Aivlosin® continues to perform well in high-growth territories, and the Group remains well positioned to take market share in North America and Latin America. Trading continues to follow a seasonal pattern and remains second-half weighted. We are encouraged by improving market conditions in China.

I can’t see any updated brokers’ notes today, so I would assume these forecasts remain the same and on the current rating, the near term trading is not really a strong factor in valuation:

It is also worth noting that Aivlosin represents 92% of sales which is used as an antibiotic containing 62.5% w/w tylvalosin (as tylvalosin tartrate). ECO Animal Health (LON:EAH) say this is patented, but it is unclear how widespread this protection is. There are a number of tylvalosin competitors with claims of antibiotic treatment of animals, for example. This may limit the scope for recovery, especially in less-regulated markets, such as China.

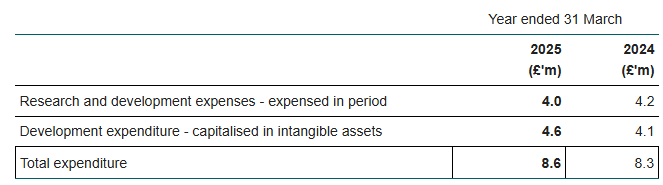

R&D:

A badly performing business not generating any sustainable free cash flow is not the whole story here. They are spending significant sums on R&D, both capitalised and expensed:

The bulk of this is spent developing animal care vaccines, which they expect to be their next successful product. Here they say:

All R&D programmes progressed well during the year, and the milestone of dossier submission to the regulatory authorities for our first mycoplasma poultry vaccine was reached - ECOvaxxin® MS. The group expects further submissions in the next and following years supporting the targeted investment in innovative vaccine technology. The strong market potential and technical success supports the capitalisation of late stage R&D expenditure which showed no indications of impairment. At the current time the Group capitalises expenditure on ECOVaxxin® MG and ECOVaxxin® MS as well as a long acting Florfenicol based anti-infective, ECOFlor, for swine respiratory disease.

If these aren’t successful and R&D costs are slashed, this would make the cash flow look significantly better. So there may well be an upside option on one of these products being successful in the future. I just have no idea how to price that option.

Mark’s view

When I last looked at this briefly on the DSMR I said:

I think I have been a little harsh on this in the past, as it now trades at a discount to TBV. However, the bull case is largely in their new product developments being successful (or them being willing to aggressively cull headcount if they aren’t successful). Something that requires the kind of specialist knowledge that very few possess.

I stand by this assessment. Those who are experts in this area, may be able to price this option more accurately. However, for the generalist investor, such as myself, this is far too hard. This is complicated by the core business struggling at the moment. I see nothing in today’s results to justify the c10% rise in the share price. However, I retain my AMBER view.

See what our investor community has to say

Enjoying the free article? Unlock access to all subscriber comments and dive deeper into discussions from our experienced community of private investors. Don't miss out on valuable insights. Start your free trial today!

Start your free trialWe require a payment card to verify your account, but you can cancel anytime with a single click and won’t be charged.