Good morning and welcome to Wednesday.

The mood in markets seems to be one of cautious optimism this morning, with most major indices expected to open higher on reports of Iran talks. One major exception to this at the time of writing is the FTSE 100. Of course, things could change as the day unfolds:

- S&P 500: up 0.6%

- DAX: up 1.0%

- FTSE 100: down 0.1%

- Euro Stoxx 50: up 0.9%

Today's agenda is complete.

To start things off today, Graham has prepared backlog sections on Journeo and PZ Cussons, both of which issued updates yesterday.

Spreadsheet accompanying this report: link.

Companies Reporting

| Name (Mkt Cap) | RNS | Summary | Our view (Author) |

|---|---|---|---|

Rio Tinto (LON:RIO) (£105bn | SR67) | The Queensland and Commonwealth Governments will invest AU$2bn over 10 years to 2040 to support “the transition to long-term competitive power for the smelter”. This will combine with large solar and wind developments that have been underwritten by Rio Tinto. | ||

Diageo (LON:DGE) (£30bn | SR55) | United Spirits Limited has agreed the sale of its 100% equity stake in the Royal Challengers Bengalaru cricket teams for INR 166.6bn (approx £1.3bn) to a consortium including Blackstone. | ||

United Utilities (LON:UU.). (£8.5bn | SR40) | 2025/26 underlying EPS is expected to be in line with guidance “at around 100 pence”, with opex guidance unchanged. However, a change in the estimation technique used to value index-linked debt will lead to lower net finance costs and an increase in underlying EPS of c.5p. Electricity costs are fully hedged for Summer 26 and over 90% hedged for Winter 26/27. | ||

RS (LON:RS1) (£2.8bn | SR87) | FY26 like-for-like revenue is now expected to fall by 0.6% due to “difficult markets”. Adjusted pre-tax profit is still expected to be “marginally ahead of expectations” (consensus £241m/range: £230-247m). | ||

HICL Infrastructure (LON:HICL) (£2.17bn | SR84) | Sale of 24% stake in France’s A63 motorway for gross proceeds of c.£311m, a 21% premium to the most recent valuation. The sale will add 2.2p of NAV per share and is accretive to the portfolio’s expected return metrics. Intention to deploy proceeds into new investments exceeding the return hurdle set by share buybacks. The A63 was HICL’s second-largest asset and accounted for 8.4% of the portfolio in Sept 25. | ||

Volex (LON:VLX) (£803m | SR89) | Full-year results are now expected to be significantly ahead of current market expectations. Revenue is expected to be at least $1,220m, with underlying operating margins “slightly above the top end” of the 9-10% target range. Outperformance has primarily been driven by data centre demand, with full-year data centre revenue expected to be “approximately double” the $118m achieved in the prior year. Volex also announces that it is considering a move from AIM to the Main Market. | AMBER/GREEN = (Roland) A strong update showing Volex has continued to benefit from accelerated demand for the high-spec data transmission cabling that’s needed to fit out new AI data centres. Sales in this part of the group doubled last year. The company does warn that some 2026 sales were pulled forward from 2027, so at this early stage there’s a risk this demand might not be repeated this year. Even so, I am happy to maintain a broadly positive view here, reflecting the company’s strong growth and diversification in recent years. | |

WAG Payment Solutions (LON:EWG) (£684m | SR63) | Net revenue up by 12.9%, adj EBITDA up 8.5% to €132.1m. Adj EPS up 3.9% to 4.83c. Launched a new integrated platform for core services and saw total active trucks rise by 6.4% to 321,500. | ||

Enquest (LON:ENQ) (£346m | SR88) | Pro forma production of 45,606 boepd (guidance: 40-45 kboepd). 2P reserves down 3.6% to 162.5 MMboe. Adj EBITDA down 25% to $503.8m reflecting lower oil prices. Net debt up 12.5% to $433.9m. 2026 Outlook: production expected to be 41-45 kboepd. | ||

| Pinewood Technologies (LON:PINE) (£270m | SR13) | Business Update | A five-year contract with dealer group Marshalls is running behind schedule. The rollout is not now expected to start until H2 2026 (previously Q1 2026). As a result FY26 underlying EBITDA will be lower than current market expectations. Guidance for underlying EBITDA of £58-62m by FY28 is unchanged. | BLACK (AMBER/RED ↓) (Roland) Following February’s takeover bid failure, Pinewood has announced delays to a major customer project. My reading also suggests possible slippage in its own internal North American rollout. While I think there should be a decent business here, the shares don’t look particularly cheap to me and I’m concerned by the weak outlook. I’m inclined to be cautious and have downgraded my previous neutral view today ahead of April’s full-year results. |

Luceco (LON:LUCE) (£257m | SR86) | Revenue up 11.9% (LFL +4.6%), adj pre-tax profit up 11.6% to £27.8m. Adj EPS up 20% to 15.0p. Growth driven by energy transition – EV charging sales rose by 85% last year. 2026 Outlook: good early momentum. Expects adj op profit “to exceed £37m”. | ||

Asos (LON:ASC) (£254m | SR39) | H1 Gross Merchandise Value down 9%, with sequential quarterly improvement. UK performed better with GMV -5%. FY26 guidance reiterated for FY26 adj EBITDA of £150-180m. | ||

Franchise Brands (LON:FRAN) (£217m | SR56) | System sales up 2%, revenue up 2% with adj pre-tax profit up 12% to £23.9m. Leverage reduced to 1.6x EBITDA. Outlook: early 2026 trading “varied” with strong performance at Filta International. FY results to be “within the range” of current forecasts, planning £10m buyback. | ||

Literacy Capital (LON:BOOK) (£202m | SR N/A) | Diluted NAV per share up 0.3% to 484.3p (share price: 335p). Diluted NAV £291.4m. “Literacy's investee companies remain prudently valued and modestly leveraged.” Weighted average EV/EBITDA multiple for ten largest investments was 9.4x (Dec 2024: 8.8x). Average net debt/EBITDA 2.8x. | ||

| James Latham (LON:LTHM) | Trading Statement | Revenue for the y/e 31 March 26 was in line with expectations, with volumes expected to be slightly up on the prior year despite challenging trading conditions. Cost prices remained stable during the year but freight rates and shipment times are currently increasing as a result of the conflict in the Middle East. | |

TT electronics (LON:TTG) (£186m | SR49) | Organic revenue down 2.7%. Adjusted PBT +5.5% (£28.7m). Actual revenue is down 7.6% and actual PBT is a loss of £36.7m (2024: loss of £33.4m). “The Board expects 2026 revenue and adjusted operating profit to be in line with Company compiled consensus.” | ||

Kore Potash (LON:KP2) (£183m | SR26) | “We look forward to an exciting year ahead in which we expect to achieve Financial Close under the EPC as well as start construction at Kola with a view to delivering production in the first half of 2030." (Kola is in the Republic of Congo). | ||

Fonix (LON:FNX) (£147m | SR66) | The company has authority to buy back up to 230,000 shares, which is 0.23% of its share capital (the presence of a Concert Party prevents it from buying more). | ||

Mobico (LON:MCG) (£122m | SR53) | The COO is promoted to CEO. He is also CEO of the Alsa division and will continue to oversee Alsa. | ||

Pharos Energy (LON:PHAR) (£111m | SR96) | Working interest 2025 production totalled 5,398 boepd net, in line with guidance of 5,200 - 6,000 boepd. 2026 outlook: working interest production guidance increased from 2025 to 5,200 - 6,400 boepd net. | ||

Quartix Technologies (LON:QTX) (£103m | SR64) | Revenue +12%, adjusted EBIT +38% (£8.8m), PBT +34% (£8.7m). “...outstanding progress in 2025 on all key measures.... The outlook for 2026 is very encouraging.” | ||

Avation (LON:AVAP) (£79m | SR37) | Commencement of a new lease and delivery of an ATR 72-600 aircraft (MSN 1387) to a new client, ETF Airways, a Croatian airline. | ||

Braemar (LON:BMS) (£74m | SR49) | FY26 performance in line. Underlying operating profit c. £13.2m (FY25: £16.7m). Forward order book remains strong. “...the board remains confident in the Group's prospects and delivering on its FY30 objectives…” | ||

Centaur Media (LON:CAU) (£61m | SR55) | The max number of shares were validly tendered at 48p. New share count 18.1m. | ||

IG Design (LON:IGR) (£51m | SR58) | Completed the sale of a surplus warehouse to the Welsh government for £3.1m. Carrying value was £0.1m. | ||

Headlam (LON:HEAD) (£6m | SR36) | Revenue down 4.6%, negative EBITDA £12.5m (2024: negative £5m). Statutory operating loss £63.5m (2024: loss £31.3m). Net debt £31.4m. Trading conditions remain challenging in the near term. “The new core customer strategy will see a material planned reduction in revenue over 2026 and 2027… continues to have confidence in a return to profitability in 2027 as previously guided.” | ||

Aptamer (LON:APTA) (£18m | SR21) | Fundraise for at least £3.75m. Placing for £3.75m, retail offer for up to £0.5m. Issue price: 0.6p (last night’s close: 0.65p). Also includes one warrant for every three shares issued. Net proceeds to be used for working capital, extending the cash runway through to 2028, and to fund various development projects. | ||

Cadence Minerals (LON:KDNC) (£17m | SR47) | Funding Confirmation Notice has been issued; Cadence and REM Mexico intend to commence international arbitration against Mexico under the agreement between the UK and Mexico for the Promotion and Reciprocal Protection of Investments. | ||

Nexus Infrastructure (LON:NEXS) (£10m | SR50) | “While market conditions remain mixed in the near term, the fundamentals of our end markets are supportive. With a growing pipeline, a strengthened platform and continued operational momentum, we are well positioned to deliver sustainable long-term growth.” The Chair and a NED are stepping down. An Interim Chair has been selected. |

Graham's Section

Journeo (LON:JNEO) (Backlog)

Down 3% to 367.1p (£65m) - Final Results - Graham - AMBER/GREEN =

Journeo plc (AIM: JNEO), a leading provider of intelligent systems for transport networks and critical national infrastructure, is pleased to announce its final results for the year ended 31 December 2025.

We cover this one regularly, as it’s a frequent issuer of announcements and is a popular share, although Roland is usually the one who looks at it. Guess it’s my turn today!

Financial headlines:

Revenue +11% (£55m), which includes around £4m from an acquired business.

Adjusted PBT +13% (£5.7m)

Cash reduces to £12m (2024: £14.3m) after making an acquisition.

According to Cavendish, these results are in line with expectations.

Some operational headlines:

Won their largest ever Framework Award, with an anticipated value of £10m over three years from First Bus UK.

£4.2m purchase order from Alstom.

Development into overseas markets with new orders from Outfront Media (for platform-based displays).

CEO comment:

"Journeo has delivered another record year, driven by our customer-centric approach, the deployment of our proven technologies and a strategic, value-enhancing acquisition. With a strong order book, disciplined capital management and a talented team of nearly 300 people, we are well positioned to convert market opportunities into further sustainable growth."

And the outlook from the Chairman concludes as follows:

Across the operating businesses, we have strong orderbooks and a growing pipeline of sales opportunities which gives the Board confidence that Journeo will continue to deliver growth and increasing value for all stakeholders.

Estimates from Cavendish for 2026 are similar to what they published at the full-year trading update, with the differences probably not worth making a fuss over.

Revenue forecast £72m unchanged.

Adj. PBT £7.4m (previous estimate £7.2m).

Adj. EPS 32.2p (previous estimate 33.2p).

Graham’s view

I don’t have a very strong opinion on Journeo but the results are clean, with only modest share-based payments and acquisition-related expenses. The actual PBT result for 2025 is £5.6m (vs. adjusted PBT £5.7m).

The balance sheet is fine, too: there’s no tangible asset backing that is worth speaking of, but at the same time there’s a healthy cash position and working capital surplus, with minimal borrowings.

The major long-term liability is £4.4m of deferred revenue: this is “good debt” as it represents customers paying upfront for Journeo’s products.

The six operating companies cover a broad range of activities and a few different geographies:

Fleet Systems: CCTV, telematics, communications and passenger counting

Passenger Systems: hardware and software for public transport information systems, smart-ticketing and wayfinding

Infotec: information displays hardware for rail applications

Crime and Fire Defence Systems (new from 2025): protection of critical national infrastructure

Journeo A/S based in Denmark, serving Denmark, Sweden and Iceland

Journeo AB based in Stockholm, providing technical services to public transport customers in Sweden.

My overall impressions of the business are pretty positive, and I concur with the AMBER/GREEN most recently given by Roland.

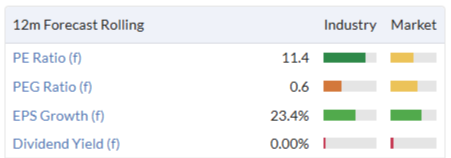

At the end of the day, it is an order-driven B2B type of company, and this limits the sort of rating I’d be willing to pay for it. At the moment it’s trading at 11x earnings, with a low PEG ratio based on the EPS growth that is anticipated. There are no 2027 forecasts yet.

I’m personally of the view that this valuation is fair enough. At Fleet Systems for example, which is Journeo’s largest division and was responsible for over 40% of revenues in 2025, there was 3% revenue growth.

Passenger Systems grew revenue by 33%, while Infotec declined by 35%.

The point I’m getting at is that the underlying growth rates here are something of a mixed bag. A big chunk of the expected revenue growth in 2026 will be from the addition of Crime and Fire Defence Systems Limited (CFDS), which will add an additional £13m of revenue (as it only added £4m in the late stages 2025, and will add c. £17m in 2026).

I calculate that the expected organic growth rate in revenues for 2026, excluding the impact of CFDS, is about 7%-8%.

Hopefully this helps to underscore the role played by acquisitions in the growth story here: without them, the actual growth achieved would be much less interesting. But this doesn’t take away from my overall impression that Journeo is a decent business that is not particularly expensive.

3-year chart:

PZ Cussons (LON:PZC) (Backlog)

Up 11% at 81.6p (£350m) - Q3 Trading Update - Graham - AMBER/GREEN ↑

We had a brief but very pleasant update from PZC yesterday. It was just a few sentences long. Here are the first two of those sentences (emphasis added):

The positive trading momentum in the first half of the year has continued, with 6.3% Group LFL revenue growth in Q3 (H1 FY26: 9.5%). On a reported basis, revenue growth was 5.0% (H1 FY26: 8.0%).

Reflecting the performance to date, with further stability in the Nigerian Naira and careful cost management, the Group now expects to report adjusted operating profit towards the upper end of the previously updated £53-57 million guidance range.

The share price reacted very strongly (+11%) to this message that profits would be “towards the upper end” of the range.

Graham’s view

It seems to me that this was an outsized reaction to moderately positive news: even a result at the very top end of the range (£57m) would only be <4% higher than a result at the midpoint of the range.

Therefore, I’m going to interpret this movement in the same way that I interpret a share price rise in response to an “in line” update: I assume that investors were braced for negativity.

The PZC share price has been fairly uninspiring over the past year, going almost nowhere in that time while the FTSE is up 15%.

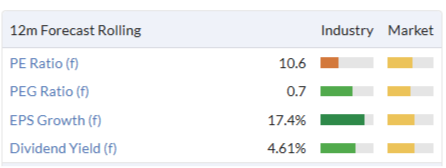

And for a branded consumer goods business (owning the likes of Imperial Leather, Carex, Original Source and St. Tropez), the rating is fairly weak:

Of course, the company is not without its challenges.

There are significant currency risks in its African business - it recently abandoned efforts to sell this, having already failed to sell its fake tan business.

But helping to boost the positivity yesterday, there were also some calming words on the currency question:

While this guidance remains subject to movements in the Nigerian Naira in the remaining weeks of the financial year, the actions management have taken to mitigate against future volatility have continued to reduce the Group's sensitivity to such fluctuations.

I don’t take much convincing to get bullish on a cheap stock for a branded consumer goods business, so I’m inclined to upgrade our stance here to AMBER/GREEN (my co-writers have been fully neutral).

The interim results to November 2025 showed the company having net debt of £84m, which appears manageable (the leverage multiple being only 1.1x). LfL revenue growth was strong at 9.5%, and H1 PBT was solid both on an adjusted (£29.8m) and unadjusted (£34.3m) basis.

This old share has been in the doldrums for years now - maybe it’s time to look at it with fresh eyes?

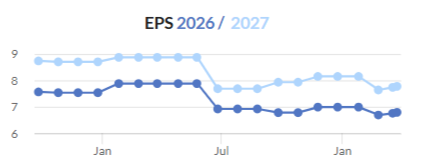

EPS forecasts have actually held up quite well here over the past year:

Perhaps it’s a nice time to start taking this one a bit more seriously?

Roland's Section

Volex (LON:VLX)

Up 9% at 475p (£873m) - Trading Update - Roland - AMBER/GREEN =

Today’s trading update from cabling specialist Volex is a relatively rare beast – a company guiding for full-year results to be “significantly ahead of current market expectations”. I don’t think we’ve had many of those recently.

Volex is benefiting from booming demand for the sophisticated high-speed data transmission products that are required to fit out new AI data centres. The company says that sales in its Complex Industrial Technology division are now expected to be around double the $118m achieved in the FY25 financial year (y/e 31 March) – or nearly 20% of total FY26 revenue.

Interestingly, the company says it’s benefited from being able to pull forward supply to meet “accelerate customer requirements”, where “other suppliers have not been able to meet these needs”. There is a potential downside to this of course in terms of next year’s demand, which the company acknowledges:

The Board is encouraged by the strength of the Group's positioning in this market, although this particular dynamic may not recur at the same level in FY2027.

Trading elsewhere in the business is said to have remained “broadly in line with the first half of the year”. Checking back to the H1 results shows a fairly mixed picture, suggesting to me that Data Centres and EV-related products were the main bright spots during the year:

H1 EV - organic revenue up 13.1%

H1 Consumer Electricals - organic revenue down 6.3%

H1 Medical - organic revenue down 9.9%

H1 Complex Industrial Technology (inc. data centre products) - organic revenue up 48.2%

H1 Off-Highway - organic revenue up 20% due to a one-off project completed in H1 – so perhaps a flat performance otherwise?

Updated profit guidance

The company has provided the following guidance today for FY26, which ended on 31 March:

Revenue to be at least $1,220m (previous consensus $1,173m)

Underlying operating margins to be “slightly above” the top end of the group’s 9-10% target range, thanks to both operating leverage and cost savings.

Previous consensus for underlying operating profit was $114.8m (in a range of $111.5m - $117m). Assuming a full-year margin of 10.3% gives me an underlying operating profit estimate of at least $125m, c.9% above current consensus.

Happily, Volex is one of a growing number of companies that has adopted the more democratic approach of including consensus forecast information in its RNS releases – this makes the estimates above much easier for investors without access to broker notes.

Main Market move?

Volex has also announced today that it’s considering moving its listing from AIM to London’s Main Market, where it would be likely to join the FTSE 250.

In conjunction with the expectation of being eligible for inclusion in the FTSE250 Index, the Board of Directors of Volex (the "Board") believes that a move to the Main Market would facilitate access to deeper pools of capital and a broader range of investors, supporting increased liquidity in trading of the Group's shares.

The Board also believes that a Main Market listing would increase the corporate profile of the Company and enhance its reputation with a larger and more global customer base.

An update will be provided following consultation with the Company's largest shareholders.

While specialist AIM investors (e.g. IHT funds) will no doubt feel sad at the prospect of losing such a strong performer, it does seem logical to me for a business of this size and quality to be listed on the Main Market.

Roland’s view

Volex was one of the stocks I profiled at the Stockopedia panel event at Mello in November. I’d been struck by the rapid growth in demand for data centre products and thought this might continue for some time yet.

Today’s update appears to support this view, with the caveat of course that the AI spending boom is likely to come to a halt at some point. How predictable that slowdown might be remains to be seen. With the US tech giants planning to spend $650bn on AI collectively this year, the current rate of growth can’t continue indefinitely.

Volex’s FY26 performance has clearly been driven by data centre demand, with revenue in the Complex Industrial Technology product group accounting for nearly 20% of the group total. Although Volex doesn’t report margins for each product group, I would guess these high-spec data centre products are likely to carry higher margins than some of the group’s more commoditised products. In the event of a slowdown in AI demand, this could result in a larger hit to profit than might otherwise be the case.

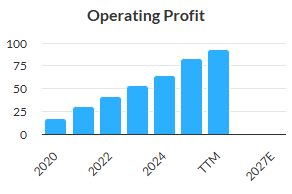

Despite this concern, I can’t ignore Volex’s strong track record in recent years:

I think the valuation also remains reasonable, albeit not cheap for an industrial manufacturer:

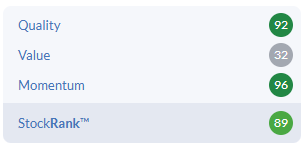

The StockRanks concur with my view, with High Flyer styling reflecting strong Quality and Momentum, with weaker Value:

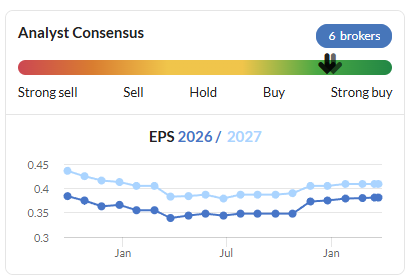

Broker forecasts prior to today suggested further earnings growth in FY27, albeit we don’t know if today’s upgrade to FY26 expectations will be carried forward to FY27 – unfortunately I don’t have access to any updated broker notes today:

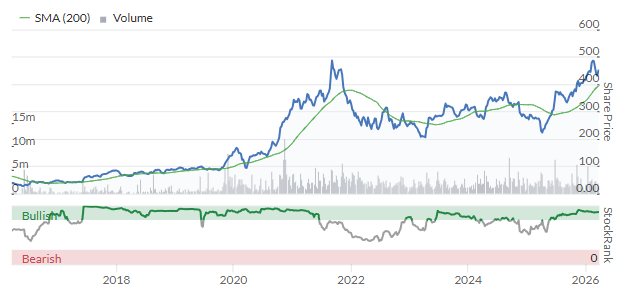

Following this morning’s gains, shares have almost doubled over the last year and have now returned to the previous record highs seen in 2021:

On balance, I don’t see any reason to change my broadly positive view today – AMBER/GREEN.

Pinewood Technologies (LON:PINE)

Down 7% at 219p (£252m) - Business Update - Roland - BLACK (AMBER/RED ↓)

After a promising start to listed life as a standalone software company, things seem to be going downhill at automotive group Pinewood Technologies. The company failed to agree a takeover in February and has today issued a profit warning due to delays with a major client project.

Let’s take a look at the key points from today’s update.

Marshalls Implementation: this is the bad news. Pinewood signed a five-year contract with Marshalls Motor Group in October 2024 to rollout its Pinewood.AI system across Marshalls dealerships.

To me (as a former IT engineer) it sounds like a nasty dose of scope creep has taken place, pushing back delivery:

Since then, Pinewood.AI and Marshalls have been working collaboratively across a number of key areas, including aligning with many other complementary technology projects that Marshalls is implementing to modernise its systems for the future. This integrated approach is designed to maximise the long-term benefits to Marshalls, once the Pinewood.AI system is launched.

Both parties have been focused on optimising the sequencing and efficiency of these key technology projects. This process has taken longer than originally anticipated, compared with the expectations set out in the 24 September 2025 announcement, but is expected to deliver a more effective outcome for Marshalls once completed.

The rollout to Marshalls’ dealerships was originally expected to start in Q1 2026 but is now expected to begin during the second half of 2026.

Based on the description above, I’d argue that Pinewood’s agreement with Marshalls wasn’t adequately defined – or that Pinewood has allowed itself to be drawn into unplanned work in an effort to keep a large client happy (Marshalls is owned by US firm Constellation Automotive Group).

I wonder if there will be any extra payment relating to compensate for the extra work? There’s no mention of this today. I wouldn’t bet against further delays, either.

North American System rollout: Pinewood is rolling out its system to Lithia dealers in North America (see here for the backstory on this).

Today’s update says the pilot is “performing as planned” but I think the main rollout may be running slightly late. Guidance today is for a full rollout “in the second half of 2026”. In September, the company said the wider rollout would start “in mid-FY26”.

Other news: a system implementation across Lookers dealerships is said to be “progressing to schedule” and “is scheduled to complete on time”, in Q4 2026.

Pinewood has also acquired its last remaining reseller, in The Netherlands, for £3.3m. This is expected to add around £0.7-0.8m in annual EBITDA. This sounds like a sensible transaction.

Updated Guidance

As a result of the change in timing of the Marshalls implementation, FY26 underlying EBITDA will be lower than current market expectations. The Board of Pinewood.AI also reaffirms its expectation that the Group will achieve underlying EBITDA of £58-62m by FY28. This is underpinned by good visibility from existing signed contracts and a strong pipeline of opportunities.

I don’t have access to any updated broker notes today and Pinewood’s management has not included details of previous consensus forecasts in today’s RNS. The analyst consensus link on the company’s website also goes to a 404 (not found) page!

However, a forecast from broker Zeus in September 2025 suggested FY26E adjusted EBITDA of £25.9m. As far as I can see, consensus hasn’t really changed since then:

In the absence of further guidance I think it’s prudent to reduce FY26 estimates by at least 10%. That gives me a FY26E adj EPS estimate of 11.6p.

At a price of 222p, that still leaves Pinewood shares trading on a forward P/E of 19.

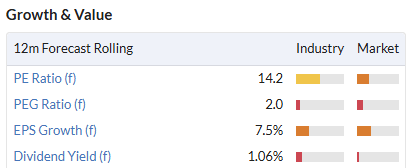

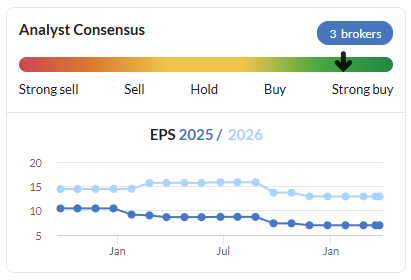

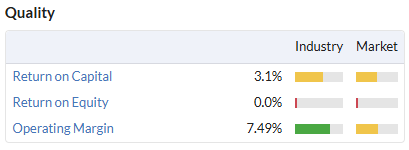

That seems quite a full valuation to me, given the stock’s low quality metrics:

Roland’s view

I’m struck by how far Pinewood’s share price and StockRank have deteriorated.

I think there could be an attractive business here, in principle.

But given the current valuation and uncertain outlook, I am not inclined to bet against the algorithms at this time. My feeling is that there could be a risk of further slippage on project timings this year. I’m cutting my view to AMBER/RED today ahead of April’s FY25 results.

See what our investor community has to say

Enjoying the free article? Unlock access to all subscriber comments and dive deeper into discussions from our experienced community of private investors. Don't miss out on valuable insights. Start your free trial today!

Start your free trialWe require a payment card to verify your account, but you can cancel anytime with a single click and won’t be charged.