Good morning!

March was "the worst month since Covid" for the FTSE, according to a City AM headline today.

While that's true, with the index falling 7%, it's still up 2% year-to-date. January and especially February were very strong.

And it's set to open up another 1% this morning, as markets now apparently believe the Iran war will end sooner rather than later.

(Year-to-date FTSE 100 Chart.)

Today's Agenda is complete.

Spreadsheet accompanying this report: link.

Companies Reporting

| Name (Mkt Cap) | RNS | Summary | Our view (Author) |

|---|---|---|---|

Compass (LON:CPG) (£35bn | SR48) | The trading currency of CPG shares on the LSE from sterling penny (GBp) to US dollars (USD). This transition aligns the Group's share price trading currency with its reporting currency, reducing FX volatility in the share price and simplifying the investment case for global investors. | (Graham) [no section below] Thanks to a change in FTSE policies, companies can now remain in FTSE indices even if their shares trade in euros or dollars. | |

Smiths (LON:SMIN) (£7.1bn | SR58) | Immediate cash proceeds of c. £1.3bn. SMIN is currently fulfilling its commitment to return £1bn to shareholders via buyback. Balance to be used to invest in growth and further reinforce the balance sheet. | ||

Babcock International (LON:BAB) (£5.7bn | SR36) | BAB has agreed a six-month bridging agreement under their Future Maritime Support Programme contract with the UK Ministry of Defence (MOD) to maintain continuity of our naval base and nuclear submarine fleet support services. The contract bridges to a new long-term agreement which is in the latter stages of negotiation with the MOD. | ||

Berkeley group (LON:BKG) (£3.2bn | SR72) | As announced in recent TU, Berkeley expects to deliver pre-tax profit for FY26 of GBP 450 million, in line with guidance put in place two years ago, with around £300 million of net cash. Strategic levers for long-term value creation: new land investment, existing land holdings, investment in construction work-in-progress, investment in Berkeley Living, focus on operating margin, and shareholder returns (buybacks when share price is below NAV per share). Targeting a return on capital employed in the core business of at least 15% as soon as possible. | BLACK (AMBER =) (Roland) Multi-year profit guidance for 2027-2030 has been restated at £1.4bn, or around £350m/year. My impression is that this is c.20% below previous expectations, hence today’s share price slide. The company bemoans difficult macro and regulatory conditions, as well as cost inflation. There are good reasons for some of these complaints, in my view, but I think that cyclical factors (plus an element of lobbying) are also at work here. For me, the crux of the story is that the company expects to maintain net cash, repay land creditors and return a further £564m (about 20% of the current market cap) to shareholders by late 2030. With the stock trading around 25% below book value, I think the value case looks interesting and do not believe that downgrading to a negative view is justified. | |

Derwent London (LON:DLN) (£1.77bn | SR61) | Exchanged contracts for the disposal of Horseferry House SW1 for £131.8m. | ||

Great Portland Estates (LON:GPE) (£1.15bn | SR27) | The Great Ropemaker Partnership, a 50:50 joint venture managed by GPE, has completed the sale of the 53 year short leasehold interest in 103/113 Regent Street, W1 to a private client of JLL. The headline price of £52 million is marginally behind the March 2025 book value. | ||

Renew Holdings (LON:RNWH) (£673m | SR86) | Trading and net cash for H1 is anticipated to be in line with its expectations. The Group remains strongly positioned with a well balanced portfolio of businesses, providing us with confidence in delivering against our full year expectations. | AMBER/GREEN ↑ (Roland) An encouraging albeit in-line update from this infrastructure specialist construction group. I see Renw as an above-average business in this sector that’s benefiting from structural tailwinds such as the increase in water and electricity investment. The shares have risen by 30%+ over the last year and aren’t as cheap as when I last reviewed this business, but I think that this may be justified by recent progress and the potential for further growth. I have tentatively upgraded our view today ahead of May’s interim results. | |

Filtronic (LON:FTC) (£422m | SR63) | New contract from an existing customer. The contract, scheduled for delivery in FY2027, has an initial value of £0.4m. | (Graham) [no section below] Not material news for a company of this size: hence this is a “Reach” announcement. | |

S&U (LON:SUS) (£231m | SR96) | CEO of S&U subsidiary Advantage Finance: “Although a redress scheme of any kind is not justified for Advantage in our view, we are pleased that this matter can now be concluded by the early Autumn. The provisions we have made for its costs will prove more than adequate. It should therefore in no way impede the ambitious plans we now have in place for building Advantage.” | ||

Mkango Resources (LON:MKA) (£125m | SR12) | Fundraise was upsized from gross proceeds of £10 million to £12.5 million (c. C$23.0 million). The new shares represent c. 10.8% per cent. of the share count prior to the Fundraise. | ||

Camellia (LON:CAM) (£124m | SR69) | The recent sale of some of the Company's artwork has realised proceeds of £3.7 million, with a profit of £3.6 million, to support investment into higher-return assets. Separately, CAM’s Indian subsidiary has announced the termination of an MOU re: the sale of its Barnesbeg Tea Estate. | ||

Topps Tiles (LON:TPT) (£68m | SR69) | Revenue down 0.1%. LfL revenue up 0.1%. CEO: “Topps continues to outperform a softer market. In light of subdued consumer sentiment and geopolitical uncertainty as well as the cumulative impact of cost inflation, the management team is implementing a targeted programme of self-help measures weighted towards the second half.” | BLACK (AMBER/RED ↓) (Roland) I’m moving our view down two notches today following a 20% cut to FY26 EPS estimates from commissioned research house Edison. I don’t think the scale of this change to expectations is clear from today’s RNS and while I think store closures and continued strong online growth offer medium-term promise, I think there’s still some risk of further near-term disappointment. | |

Arrow Exploration (LON:AXL) (£61m | SR85) | Mateguafa 11 well is on production in the Carbonera C7 formation, with 18ft of net oil pay. Currently producing 784 bopd at 31.5° API, with 25% water cut. Total corporate production is now 5,475 boe/d, cash on 1 March 26 was $6.4m. | ||

Petra Diamonds (LON:PDL) (£56m | SR26) | Sales results for Q3 FY 2026 and Sale of 41.82 carat Type IIb blue diamond | Sold 781,797 carats for $68m in Q3 ($87/carat) vs $49m and $98/carat in Q2. Diamond prices were -15% LFL. Finsch mine particularly affected due to mix, with an overall reduction of 22% on average prices received QoQ. Now expects Finsch to receive $60-70/carat in FY26. Petra has entered into an agreement to sell the 41.82 carat Type IIb blue diamond recovered at Cullinan in December 2025. | |

Billington Holdings (LON:BILN) (£46m | SR89) | Recently awarded new contracts with a combined value of c.£50m, mostly for delivery in 2026 and 2027. Confident 2026 will be in line with expectations. | AMBER/GREEN ↑ (Roland) A solid update that importantly reiterates expectations for 2026. After two profit warnings last year, this seems encouraging evidence. Contract win momentum seems positive and improves revenue visibility. Meanwhile, Billington’s valuation continues to look very reasonable to me, so I’m tentatively moving our view up by one notch today. | |

CML Microsystems (LON:CML) (£37m | SR62) | Revenue rose by c.18% in H2 vs H1 FY26. Full year revenue is expected to exceed £20m. However, phasing of order intake has led to lower operating margins and CML expects to see an H2 operating loss. An overall FY26 pre-tax profit of £1.8m is expected, aided by proceeds from property sales. Expect timing effects from FY26 to unwind in FY27 as shipments of a key product improve. | ||

Cavendish (LON:CAV) (£34m | SR66) | FY26 revenue to be c.£56m (FY25: £55.6m). Profitable during both halves of the year, net cash of £19m at 31 March. FY27 outlook: “strengthening pipeline and an improving operational platform”. Warns of potential impact of M. East situation. | AMBER/GREEN = (Graham) | |

One Health (LON:OHGR) (£33m | SR74) | Heather Craven appointed as part-time CFO. She will join the board. Chief Medical Officer will retire from the role to focus on his medical practice within OHGR. | ||

Skinbiotherapeutics (LON:SBTX) (£25m | SR9) | Shares suspended as interim results have not been published within the AIM market’s three-month deadline. Board investigation and forensic review continue, hoping for an update later this month. | RED = (Graham) [no section below] We turned RED on this in February when the CEO abruptly resigned with an investigation ongoing. The ramifications of that investigation continue to be felt with the shares now suspended, as expected. The “robust cash position” was £2.44m as of 19th March 2026, according to a previous RNS. However, I would expect some cash burn arising from this investigation and believe that a RED stance continues to make sense. Even in a best case scenario the group was supposed to be trading at around breakeven this year. So I expect some continued downward pressure on the cash balance in the near-term. | |

Insig Ai (LON:INSG) (£18m | SR1) | Revenue up 56% to £0.8m. FY27: expect revenue more than double that achieved during FY26. At this level the company would expect to achieve operating profitability. Cash at 31 March 26 was £100k. Considering a proposal from CEO to invest £0.5m at 20p (y/day’s close was 14.25p). Commenced discussions for a dual listing on NASDAQ. | ||

Prospex Energy (LON:PXEN) (£15m | SR19) | PXEN Tatra has been formally awarded the San onshore licence area in Poland. Process for award of Dunajec licence is ongoing. | ||

Tanfield (LON:TAN) (£12m | SR73) | Following a recent US court ruling in Tanfield’s favour re the acquisition of its 49% stake in Snorkel, the other party plans to appeal to the US Supreme Court. No date is currently set for the appeal. |

Graham's Section

Cavendish (LON:CAV)

Down 0.6% at 8.7p (£34m) - Full Year Trading Update - Graham - AMBER/GREEN =

Cavendish, a leading UK investment bank, today issues a trading update for the year ended 31 March 2026 ("FY26").

Hot on the heels of the Peel Hunt trading update, today we have news from Cavendish.

FY March 2026 revenues of £56m (looks slightly ahead of expectations)

“Profitable in both halves of the financial year”

Net cash of £19.2m

It’s always pleasant to see cash covering more than half of the market cap, though it underlines the market’s unwillingness to award this stock much an enterprise value - only £15m as of today.

Performance is a bit mixed:

In the public markets, FY26 delivered a robust performance against a challenging equity issuance backdrop… We added 27 new clients during the year, following an increased focus on and investment in client origination. For the first time since our merger, the movement in clients has been net positive during the second half…

But…

There has been some reduction in private market revenues in the year. The level of deal volume was broadly in line with the previous year, but the average deal size has been somewhat smaller. Encouragingly, underlying deal economics proved resilient, with the rolling twelve‑month median fee increasing...

Outlook sounds fine, with new offices in Birmingham and Manchester now up and running.

Looking ahead, the Group enters FY27 with a strengthening pipeline and an improving operational platform. The quoted client base is increasing, supporting higher recurring retainers and equity issuance activity. A stronger equity distribution capability is expected to generate greater commission income and our regional offices, now fully staffed, are positioned to capture higher‑value deal flow…

…sentiment remains heavily influenced by the current conflict in the Middle East, and dragged down by the protracted Russia Ukraine war, political uncertainty in the UK, heightened geopolitical risk and continued debate around returns on AI investment.

Graham’s view

I had high hopes for how this would perform after the Cenkos/finnCap merger.

That merger completed in late 2023.

Unfortunately, the actual results since then have not yet fulfilled these hopes, although results are currently on an upward trajectory:

This has also been a period of exceptionally difficult conditions in the UK small-cap market, with historically low levels of IPO activity and few big deals for the company to get its teeth into.

CAV’s private market business does at least provide some level of diversification away from activity in the stock market.

I still think that my original reasons for optimism had some merit. There were and are strong synergies from merging two very similar companies. Long-term I still think the merger will produce great benefits for shareholders.

However, I can’t say I have total confidence in the company hitting FY March 2027 earnings forecasts. If there aren’t enough deals for the company to work on, it’s simply not going to happen. Which I guess is an argument in favour of the market’s unwillingness to award this stock a proper earnings multiple.

Note that the P/E multiple above is before adjusting for cash. After adjusting for cash, the P/E is more like 3x.

And cash doesn’t quite tell the whole story of CAV’s balance sheet strength. At the interim results, working capital was £18m and there were various non-current assets that some investors might also include in their calculations (PPE, long-term investments, and tax assets). Tangible equity was over £25m.

So the balance sheet argument is still there.

In conclusion, I am going to leave Mark’s AMBER/GREEN stance unchanged here. I still think the stock is very cheaply valued, and if another merger or a takeover were to materialise, I’d expect that its balance sheet value would be recognised. Against that, I have to acknowledge that earnings are not yet at the level I was hoping for, and I can’t predict whether or not FY March 2027 will be the year that this will happen. More patience may be needed, I’m afraid.

Roland's Section

Topps Tiles (LON:TPT)

Down 3% at 33.5p (£65m) - Half-Year Trading Update - Roland - BLACK (AMBER/RED ↓)

Topps Tiles Plc ("Topps Group", or the "Group"), the UK's leading tile specialist, announces a trading update for the 26-week period ended 28 March 2026.

I don’t think it’s entirely clear from today’s RNS, but this half-year update appears to be a fairly big profit warning.

Commissioned research house Edison has cut its FY26 EPS forecasts by 20% today and trimmed its forecasts for FY27. Given that Topps is a research client of Edison’s, I think we can safely assume that the analyst preparing these revised estimates had spoken to management first.

The market seems to have shrugged this off at this point, but Topps share price is still down by around 20% since the Iran war started at the end of February:

Here the main points from this morning’s update:

H1 revenue down 0.1% to £142.7m (including the CTD acquisition)

Revenue excluding CTD was up 2.1% (Q1 +3.7%, Q2 +0.6%)

H1 LFL revenue +0.1% (Q1: +2% LFL, Q2: -c.2% LFL)

Wider market -2% in H1

These figures show a marked slowdown in sales during the second quarter (Jan-Mar). Negative LFL sales in Q2 presumably reflects a decline in volumes or a shift to lower-value products. Neither is good news for a store-based retailer with relatively high fixed costs.

To address this situation Topps will be carrying out some self-help measures, including central cost savings and the closure of 23 underperforming stores this year. These changes are expected to improve group profitability.

Plans to return the CTD business to profitability are also “on track”, with housebuilder volumes rebuilding and +1% LFL sales in H1. The company says that volumes have suffered during the long CMA approval process for this acquisition, which prevented Topps from fully integrating the business.

Online brands are also continuing to perform well, with Pro Tiler sales up 21% in H1 versus the prior year. This business generated £35m of sales last year (group total: £296m) and was described as being close to achieving a target “8% net margin”. If I’ve understood this correctly, it suggests Pro Tiler might have contributed c.25% of profit last year, although I’m not sure if this is correct.

Outlook

CEO Alex Jensen makes this statement::

Topps continues to outperform a softer market. In light of subdued consumer sentiment and geopolitical uncertainty as well as the cumulative impact of cost inflation, the management team is implementing a targeted programme of self-help measures weighted towards the second half. These actions are designed to support year on year profit growth and provide a stronger financial platform for 2027 and beyond.

Personally, I think it would have been more useful if he had provided some explicit commentary on expectations versus existing forecasts.

As it is, we are left to find out the bad news from today’s Edison note. While freely available, this is not as widely distributed or seen as the RNS will have been.

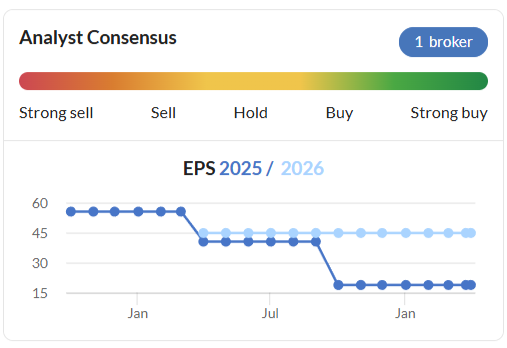

Edison’s updated forecasts:

FY26E adj EPS: 3.61p (-20% vs 4.5p previously)

FY27E adj EPS: 4.39p (-17% vs 5.27p previously)

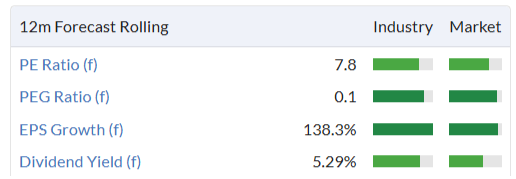

Based on these revised forecasts, the shares now trading on around 9.5x revised FY26 earnings forecasts with a possible 8% yield.

We can see cuts to consensus estimates already showing in the trend chart on the StockReport, although Edison’s cuts are larger than this. I suspect further updated forecasts may yet filter through in the coming days:

Roland’s view

We have been AMBER/GREEN on Topps in recent times, due to the modest valuation and apparent robust performance in a subdued market.

Sales have clearly declined in Q2 after a promising Q1. This isn’t entirely surprising given the macro backdrop, of course, but it’s disappointing all the same.

The lack of clarity on expectations in today’s update is also disappointing, in my opinion.

The main bright spot for me is that the shrinkage of the group’s store portfolio and the continued strong online growth at Pro Tiler may create a more robust and profitable business on a medium-term view.

Today’s updated forecasts from Edison suggest the dividend will be held at 2.9p this year, giving a potential yield of more than 8%. Topps Tiles reported net cash (exc lease) of £7.4m at the end of last year, so it’s possible the payout will remain supportable.

Personally, my feeling is that the chances of a dividend cut have probably increased following today’s update. I am not sure I would want to rely on this payout being maintained.

This may seem harsh, but I am going to move our view down two notches to AMBER/RED ahead of Topps’ half-year results in May. I think there’s still some risk of further disappointment and don’t think the current valuation is especially compelling.

Berkeley group (LON:BKG)

Down 15% at 2,920p (£2.8bn) - Strategy and Trading Update - Roland - BLACK (AMBER =)

London- focused brownfield specialist housebuilder Berkeley has cut its guidance for the period to 2030, citing difficult market conditions, rising costs and burgeoning regulatory headwinds.

Recent years have seen an unprecedented increase in cost and regulation, at a time of increasing interest rates and faltering consumer confidence, amidst prolonged geopolitical and macro-economic volatility and uncertainty.

A promising start to the current year has rapidly petered out:

In the first two months of 2026, we had begun to see signs of a modest recovery in sales volumes. However, we indicated in our Trading Update, that recent geopolitical events and the macroeconomic consequences, including reduced potential for further rate cuts, could reduce confidence in a near-term market recovery. This has now become a reality.

While existing guidance for pre-tax profit of £450m in the year to 30 April 2026 is unchanged, the company has revised its 2035 strategy to reflect current conditions:

Berkeley now expects to generate £1.4bn of pre-tax profit for the four years from 2027 to 2030.

Averaging this gives a figure of £350m per year, although management says this may be weighted slightly to 2027, with the remainder evenly spread.

From what I can see, previous expectations were for pre-tax profit of c.£450m per year during this period – so this represents a cut of c.20% to profit guidance

The company aims to achieve a return on capital employed of 15% “as soon as possible” and is forecasting ROCE of 11% to 15% in the intervening period (for more context, see my recent comments on profitability in this sector here).

Balance sheet strength and net cash will be prioritised, with land creditors reducing.

Book value is expected to be c.£39/share at the year end. While the shares trade below this level shareholder returns will be focused on buybacks, which prrovide “the best way to maximise shareholder value”. Targeting a further £564m of shareholder returns by 30 Sept 2030 – around 20% of today’s market cap.

Underlying this revised financial guidance are a number of changes to the company’s strategy.

No new land purchases, as prices are currently too high to achieve satisfactory returns.

Focusing on optimising existing land holdings, which total 50,000 homes with a pipeline for a further 10,000. Aim to add £2bn of value to these holdings by 2035 and “have made good progress in the last 12 months”.

Phasing construction to meet market demand and the (slow) pace of Building Safety Regulator approvals.

Continue current phase of build-to-rent programme (Berkeley Living). First phase is now being marketed, “we will review phasing of the second tranche on an ongoing basis”.

Roland’s view

Berkeley is widely viewed as an excellent operator that’s one of the few capable of taking on large, complex brownfield redevelopments. For example, the company is currently redeveloping a number of former gas holder sites in London.

Part of this model relies on long-term planning, more so than peers. I think it may be fair to say that the company’s focus on large, upmarket apartment developments in London also means it’s more exposed to fluctuations in demand from overseas buyers. These elements of the business model appear to leave Berkeley at a disadvantage currently.

Today’s update is clearly disappointing and represents a significant cut to expectations – effectively a multi-year profit warning.

However, Berkely shares are trading at £29 as I write, giving a 25% discount to the c.£39 book value indicated today.

I can’t help feeling that on a long-term view, the shares are likely to offer value and potentially attractive returns from this level.

I would also note that management expects to maintain a net cash position and reduce land creditors over the coming years. This should reduce financial risk and could lead to an attractive recovery in profits if market conditions do improve.

I was neutral (AMBER) on Berkeley following the company’s update on 13 March and I’m going to leave that view unchanged today.

While there’s still risk of further disappointment, Berkeley has a very respectable track record of creating value for shareholders through the cycle. With the stock trading 25% below book value and net cash, I don’t think a negative view is justified.

Billington Holdings (LON:BILN)

Up 7% at 377p (£48m) - Contract Wins & Notice of Results - Roland - AMBER/GREEN ↑

The contract awards posted today cover a range of sectors, totalling £50m in value for delivery in 2026 or 2027. For a company with annual revenue of c.£100m, these wins clearly provide a useful improvement in visibility:

A carbon capture facility in the North of England;

A school in Sheffield;

A steel bridge, Tubecon’s largest bridge order to date;

An extension to the National Railway Museum;

A structure for a silicon chip manufacturing facility;

A London data centre.

Other similar opportunities appear to be in the pipeline:

The Group is also seeing significant further opportunities, particularly in the energy-from-waste and the wider low-carbon power sector, as well as potential further data centre contracts, for delivery later in 2026 and 2027.

Outlook

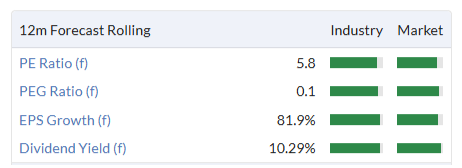

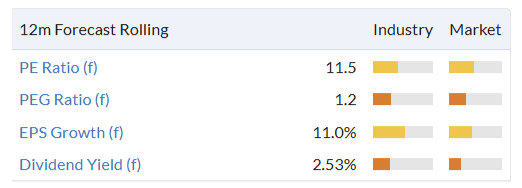

There are no changes to forecasts for FY25 or FY26 today, according to broker Cavendish. That leaves Billington trading on around eight times FY26 forecast earnings, with a potential 5% yield:

Roland’s view

Today’s guidance for 2026 to be in line with expectations seems particularly encouraging given the series of downgrades to FY25 forecasts last year:

Billington’s more confident stance is also an interesting contrast to rival Severfield’s downgraded guidance yesterday.

Mark was AMBER on Billington in September last year following the company’s second profit warning (see above).

I am inclined to move our view up by one notch to AMBER/GREEN today, given apparent strong contract momentum and today’s reiterated guidance for the current year. While it’s still early in 2026, I think the combination of value and quality on offer here looks tempting – Billington is still trading close to its tangible net asset value and the latest balance sheet showed a net cash position.

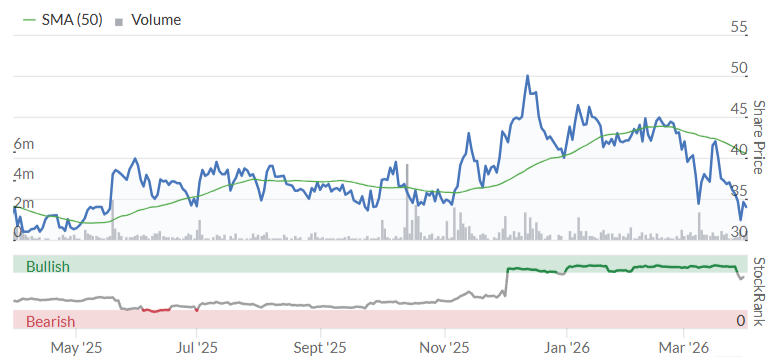

I note the StockRank has also risen steadily over the last six months:

2025 results are due to be published on 21 April, at which time we may get further insight into the outlook and market conditions.

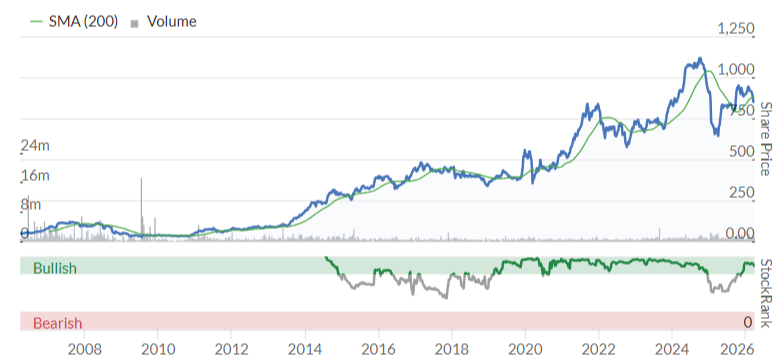

Renew Holdings (LON:RNWH)

Up 2% at 868p (£675m) - H1 Trading Update & Notice of Results - Roland - AMBER/GREEN ↑

We don’t seem to have covered this specialist infrastructure construction group since exactly one year ago. At the time I was neutral as Renew recovered from a profit warning, but I suggested the valuation could be reasonable.

My attention has slipped since then but it seems other investors have been paying attention. Renew shares have risen by 33% over the last year:

Today’s half-year trading update covers the six months to 31 March and leaves full-year expectations unchanged. Commentary highlights the company’s exposure to a number of sectors that are seeing increased expenditure at the moment:

Water: “Overall demand and momentum for our water services remain ahead of expectations as we move into the second year of AMP8”.

Rail: “performance within Rail remains in line with our expectations”. Reduced renewal volumes have been offset by increased demand for maintenance services.

Infrastructure: “momentum has continued to build”. Renew is “well positioned” to capitalise on opportunities in the latest Highways investment period, which begins today.

Energy: the group’s expansion into the Electricity Transmission and Distribution sector has been “well received”. Strike action at Sellafield is continuing to impact the group’s Civil Nuclear business, but existing frameworks are expected to support a healthy pipeline of work. However, the group’s onshore wind business is currently being affected by the underperformance of its French subsidiary.

Outlook

Management report a record order book (presumably ahead of the FY25 figure of £915m) and reiterate full-year expectations:

Underpinned by extensive Government spending commitments and long-term framework positions, the Group's order book continues to be at record levels, demonstrating our core capabilities and established presence in a diverse range of long-term, sustainable growth sectors. The Group remains strongly positioned with a well balanced portfolio of businesses, providing us with confidence in delivering against our full year expectations.

Roland’s view

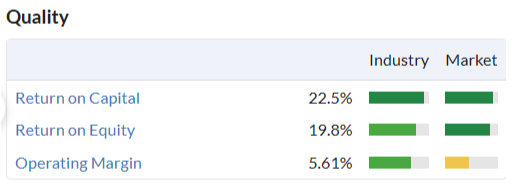

The investment thesis here is built around Renew’s differentiated capabilities in sectors such as water and nuclear. I think this story remains largely intact and note the stock’s impressive long-term record:

The group’s quality metrics are also consistently excellent, to me suggesting strong bidding and operational discipline, and good financial controls:

My decision today is whether to upgrade to AMBER/GREEN or retain my previous neutral view. It’s a slightly tough choice. In general, I probably wouldn’t want to pay much more than the current rating for a business in this sector:

On the other hand, Renew’s quality metrics and long-term track record are both unusually good.

Forecasts suggest further growth in 2027 and it is true that sectors such as water and electricity are seeing structural growth in investment at the moment, with a potential runway stretching several years ahead.

On balance I am going to tentatively move my view up to AMBER/GREEN today, to reflect solid progress and my view that this business is somewhat differentiated and operates in some attractive sectors.

Renew’s interim results are due to be published on 12 May, so we may not have long to wait to find out if my confidence is justified!

See what our investor community has to say

Enjoying the free article? Unlock access to all subscriber comments and dive deeper into discussions from our experienced community of private investors. Don't miss out on valuable insights. Start your free trial today!

Start your free trialWe require a payment card to verify your account, but you can cancel anytime with a single click and won’t be charged.