Good morning!

The FTSE is set open slightly down this morning at 10,620.

The US-Iran ceasefire is ending in two days, with uncertainty reigning around basic facts such as whether face-to-face talks will even take place.

The Strait of Hormuz remains closed, and a US blockade of Iranian ports continues. Brent crude is up by over $4 to $95.

Apart from that, everything is fine and we can look forward to another typical week in the stock market.

Today's Agenda is complete.

Spreadsheet accompanying this report: link.

Companies Reporting

| Name (Mkt Cap) | RNS | Summary | Our view (Author) |

|---|---|---|---|

AstraZeneca (LON:AZN) (£235bn | SR74) | Tozorakimab met the primary endpoint in a Phase III MIRANDA trial in patients with COPD. | ||

GSK (LON:GSK) (£87bn | SR94) | Showed 42% reduction in risk of death and nearly tripled median progress-free survival rate versus a daratumumab-based triplet. Blenrep is the only anti-BCMA approved in 2L+ multiple myeloma in China. | ||

Plus500 (LON:PLUS) (£3.1bn | SR87) | Revenue up 18%, EBITDA +2%, new customers up 48%. 2026 revenue and EBITDA expected to be ahead of current market expectations (previous consensus forecasts for FY 2026 Revenue and EBITDA were $779.3m and $360.4m). | ||

Renishaw (LON:RSW) (£3.0bn | SR67) | Have recently seen strong demand from customers in semiconductor, electronics manufacturing and aerospace/defence, with further “substantial expansion” of our order book. | AMBER/GREEN = (Roland) Good performance in key high-tech industrial sectors has supported a 4% upgrade to revenue guidance and a 7% increase in adjusted PBT guidance (using midpoint figures). I am a long-term fan of this business, which I believe has valuable IP and differentiated engineering expertise. While profitability has dipped in recent years, I expect a recovery from FY26 – something underwritten by today’s increase in margin expectations for the year ending 30 June. Renishaw shares aren’t cheap, but I think the valuation remains potentially attractive on a long-term horizon. | |

Kainos (LON:KNOS) (£1.03bn | SR63) | Strong performance continued during the second half of the year, with double-digit percentage revenue growth and “record backlog levels”. Impact on margins due to increased use of contractors. Revenue is expected to be ahead of consensus with adjusted PBT in line with forecasts (consensus figures are £406.5m and £66.4m). | ||

Advanced Medical Solutions (LON:AMS) (£501m | SR51) | Company confirms it is in discussions with TA Associates regarding a possible offer. Deadline for a firm offer is 5pm 16 May 2026. | PINK (Roland) I took a neutral view on this business when I reviewed AMS’s annual results in March, noting good underlying cash generation but weak organic growth. I would guess that it’s the combination of cash generation and a relatively affordable valuation that has attracted the potential interest of private equity group TA Associates. There’s no indication in today’s update of the level of the potential offer, but the newswire references Sky News reporting a 280p possible offer, equivalent to over £600m. That would be 23% above Friday’s close – below the 30% threshold we often see as fair, but potentially within negotiating distance of an acceptable offer. However, given that forecasts suggest double-digit profit growth in each of the next two years, I would hope the Board won't cave in too easily here. | |

Auction Technology (LON:ATG) (£475m | SR35) | Expect to report H1 revenue of c.$125m (+9% pro forma). Arts & Antiques revenue increased, with a modest decline in Industrial & Commercial. H1 adj EBITDA in line with expectations. FY26 performance expected to be in line with market expectations. CEO announces departure after more than 10 years in the role. | ||

Caledonia Mining (LON:CMCL) (£374m | SR74) | Q1 gold production down 21% to 14,767oz, as expected due to mining sequence and grades. There were also equipment availability issues and “challenging ground conditions”. Remains comfortable with Blanket full-year guidance of 72,000 to 76,500oz, weighted to H2. | ||

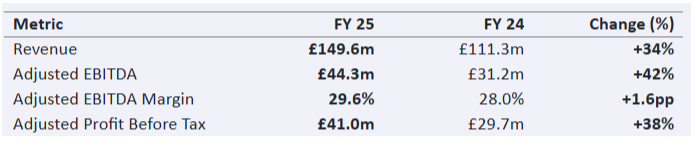

Elixirr International (LON:ELIX) (£354m | SR63) | Revenue up 34%, adj pre-tax profit up 38% to £41m. Strong demand for “AI-enabled, technology-led advisory services”. The number of £1m+ clients rose from 27 in FY24 to 34 in FY25. More than 65% of top 10 clients have been retained for over three years. 2026 outlook: record Q1, trading in line with management expectations. | AMBER/GREEN = (Graham) Organic growth is about 15% - still excellent, but only half the headline figure. They are navigating this AI-focused environment very well, but this valuation (PE >10x) is about as high I'm willing to go for a consultancy, no matter how well it's performing. On balance, I think a moderately positive stance continues to make sense. | |

Ferrexpo (LON:FXPO) (£278m | SR60) | Has sold a ship for $7.7m, expected to complete later this month. Expects the cash proceeds from this sale to extend the company’s cash runway to “approximately the end of August 2026”. Continuing to explore funding options, believes an equity capital raise is currently the most viable solution. Would be structured as a placing to raise at least $100m, in order to maintain operations at a reduced level for the next 18 months. | ||

City of London Investment (LON:CLIG) (£233m | SR97) | SP -8% FuM down 3% to $10.9bn at 31 March 2026, with net outflows of $(172)m and market performance of $(180)m. FuM at $11.7bn on 15 April 2026. No chance to Zeus forecasts today (house broker). | AMBER/GREEN = (Roland - I hold) [no section below] Today’s results have received a negative reception, presumably because of CLIG’s continued net outflows. The company’s seeming inability to win sufficient new business is a long-running concern, although I’m hopeful of progress under the group’s experienced and entrepreneurial new CEO. An update today from house broker Zeus shows forecasts unchanged today following February’s upgrade – so this isn’t a closet profit warning. CLIG shares have done well recently and remain 20% higher than one year ago. I think the valuation remains reasonable and believe the 7% dividend yield looks safe enough. For these reasons, I’m leaving our view unchanged today. | |

Evoke (LON:EVOK) (£175m | SR56) | Confirms media speculation that the company is in discussions with Bally’s Intralot regarding a possible offer of 50p per share, structured as an all-share combination with a partial cash alternative. There is no certainty an offer will be made. Deadline for a firm offer is 5pm 18 May 26. | PINK (Graham - I hold) | |

Supreme (LON:SUP) (£167m | SR79) | Strong performance across FY26 with significant growth in vape sales. “Record financial results expected to be significantly ahead of market expectations”. Revenue to be up 15% to c.£265m, with adj EBITDA of c.£40.6m (previous consensus: £245m and £37m). | AMBER/GREEN = (Roland) Supreme’s house broker has lifted FY26 earnings forecasts by 15% today, but has left FY27 forecasts unchanged at this point noting the uncertain impact of the UK vaping tax that will be introduced in October. I think the valuation looks undemanding given Supreme’s strong profitability and record of growth and diversification. However, earnings forecasts still suggest a declining trend from FY25-FY27, so I’ve left my moderately positive view unchanged for now. | |

M&C Saatchi (LON:SAA) (£140m | SR58) | LfL net revenue down 7.3% due to US government shutdown and tariffs, as well as touch macro. Outlook: “First quarter trading has been in line with our expectations despite the challenging comparator from last year and continued tough macro conditions.” Targeting net revenue growth, operating profit and operating margin improvement, in line with market estimates. | ||

Eurasia Mining (LON:EUA) (£89m | SR8) | EUA is working “to ensure the completion of both the West Kytlim sale and the Monchetundra detailed design completion, as announced in December 2025, as soon as practicable.” | ||

Mulberry (LON:MUL) (£71m | SR43) | FY26 revenue at constant currency +5.7% (-3.2% in H1, plus 13.6% in H2). FY26 was “a year of decisive progress”. | ||

Power Metal Resources (LON:POW) (£16m | SR57) | Diamond drilling programme completed with four holes and a total of 1,922 metres drilled. Highly encouraging hydrothermal alteration intersected. “While still early in our exploration, encountering such geological conditions is a significant milestone for the project.” | ||

Cordel (LON:CRDL) (£12m | SR19) | £3m contract for Point Cloud Data Processing to deliver Structure Gauging outputs at scale across Network Rail. Optional £1.3m extension. “..we remain confident of delivering a full year FY26 result in line with Board expectations.” | ||

Empresaria (LON:EMR) (£12m | SR56) | The new CFO begins on 1st May 2026. Results pushed back from 24th April to 18th May: the auditor needs more time, primarily due to the flow of information between UK auditor and overseas auditors. January trading update remains correct. | ||

Cadogan Energy Solutions (LON:CAD) (£11m | SR33) | Gross revenues $5.8m (2924: $9.2m). Loss $1.1m (2024: loss $6.2m). Cash $20.1m (including $6.5m held on deposit as collateral). Oil production down 9%. “Cadogan Energy Solutions is now a multi-energy group with a successful start of its new activities in the electricity business.” | ||

Nanoco (LON:NANO) (£10m | SR12) | Revenue £7.7m (H1 FY25: £3.4m) attributable “primarily” to litigation proceeds. Profit after tax £2.3m (H1 FY25: loss of £1m). Outlook: market trends position Nanoco to grow its product revenues, with further growth coming from other applications of quantum dots that require longer development. |

Graham's Section

Evoke (LON:EVOK)

Up 7% to 41.7p (175m) - Statement Regarding Media Speculation - Graham - PINK

(At the time of writing, Graham has a long position in EVOK.)

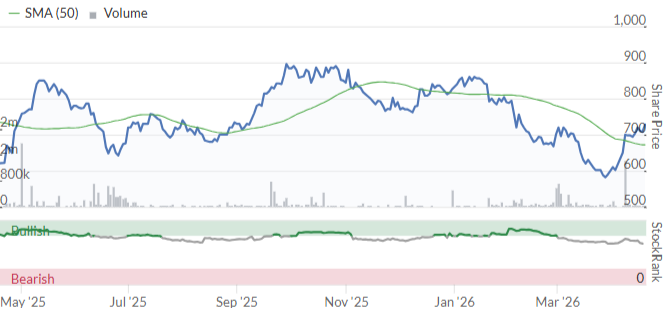

This already rose by four and a half pence on Friday, and it’s up another two pence today.

The rumour is confirmed: evoke “is in discussions with Bally's Intralot S.A. ("Bally's Intralot") regarding a possible offer for the entire issued and to be issued share capital of the Company at a price of 50 pence per share”.

The Board are "evaluating" the offer, with any firm indication yet as to whether or not such an offer would be recommended. But it hasn’t been rejected out of hand, which says a lot.

A put-up-or-shut-up period has begun: the potential buyer will confirm within 28 days whether or not it intends to make an offer.

Bally’s Intralot: I must confess that this name is unfamiliar to me. It’s a Greek gambling company, listed on the Greek stock exchange: Ballys Intralot SA (ATH:BYLOT).

According to its StockReport, it has a market cap equivalent to £555m and expected revenues this year of over €1.1 billion. It seems to be primarily a lottery operator and BCB provider of gambling-related systems.

Graham’s view

As a long-suffering shareholder, I’m not expecting much from my evoke shares. Previous management decisions ruined its prospects with the misjudged acquisition of William Hill.

So if I was offered a clean exit at 50p, I’d be OK with that.

While I did think they might find a buyer, I'm surprised that the potential buyer isn’t a bigger company.

The only way it makes sense is if Bally’s Intralot has a very detailed debt management plan.

Recap of the debt situation: evoke’s net debt was last reported at £1.8 billion (June 2025). The leverage multiple was 5x. The company’s plan was to reach an almost-acceptable leverage multiple of 3.5x by FY27.

But that was before the tax increases announced by Rachel Reeves in November. The expected annual financial impact of those increases was an eye-watering £125-135m, with only about half of that being mitigated by shutting stores, reducing marketing spend, etc.

Given the scale of the problem, it wasn’t a huge surprise that the company started a Strategic Review, looking for a buyer of the whole business and/or pieces of the business.

Bally’s Intralot plan: this Greek company seems to have a lot of Government contracts. The logic must be that they have enough revenue visibility to make it work and manage the debt load lower over time.

As a likely seller of my EVOK shares - either directly on the market or via a takeover - I’m grateful for the interest, and I am tempted to sell now, without waiting to see whether or not this deal goes through.

Zero is a realistic outcome here, in my opinion, if a takeover doesn’t materialise. That’s why I’ve been RED on the shares for some time, and I would be RED again today, if not for the takeover potential.

The 1-year chart tempts me to sell and move on:

Elixirr International (LON:ELIX)

Up 3% at 730p (£364m) - Results for the year ended 31 December 2025 - Graham - AMBER/GREEN =

Elixirr International plc (ELIX.L), an established, global, award-winning challenger consultancy, is pleased to announce its final results for the year ended 31 December 2025.

This “challenger consultancy” had a great year in 2025:

They say “AI and technology are core growth drivers”, with AI-enabled work being their fastest-growing segment, and internally developed AI tools enhancing productivity.

Organic growth: I think this should be emphasised at the top of the results, but organic revenue growth was 15.3% - still excellent, but only half the headline figure. They are targeting one-two acquisitions annually.

Current trading and outlook: they are trading in line with expectations.

There is “continued demand for AI-enabled, technology-led advisory”:

As AI reshapes how consulting is delivered, the Board believes the Group's senior-led, agile model is well positioned to adapt and capture this opportunity.

“Senior-led” means that partners and other senior staff members are involved in delivering client work - they don’t offload it to junior staff.

CEO comment:

FY 25 has been a defining year for Elixirr. We delivered record revenues and sustained industry-leading profitability, completed our transition to the Main Market and further strengthened our capabilities, particularly in AI, whilst also expanding our geographic footprint through acquisitions.

They are hoping to get into the FTSE-250 - and they are close. The smallest companies in the FTSE-250 have market caps of £350-400m, so they are right on the border.

Sample work: looking at a company like this can be a bit abstract. Here’s a specific example of their work:

…we recently worked with a major European bank to redesign its product development lifecycle using an AI-native model. The programme is expected to deliver them over £200 million in benefits over ten years, reduce product development cycles to as little as 2-6 weeks, and deliver an 18% reduction in long-term technology run costs.

Net debt: £24m. The total dividend for the year is 22.6p, well-covered by 37p of diluted earnings per share.

Graham’s view

I share many of the concerns expressed by Mark last September. In particular, I note that adj. PBT of £41m translated into actual PBT of just £27.6m.

Some of the adjustments are genuinely one-off. For example, I have no problem adjusting out Main Market listing costs of £1.5m. But I do not allow £5m of share-based payments to get adjusted out.

The “real” adjusted PBT here is more like £30-35m, in my view.

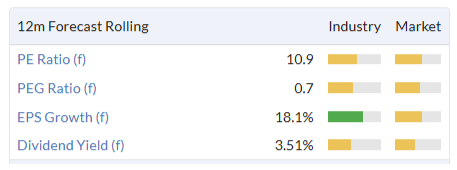

At a market cap of £360m, and with a PBT forecast of about £50m for 2026, I suspect that ELIX is fully valued here, given the sector. A P/E multiple of about 10x is about as high as I’m willing to go for a consultancy, even if it’s performing very well, as this is.

The StockRanks agree, awarding it a ValueRank of 41:

Given how well it’s performing, with very solid organic growth and inorganic growth on top of that, I think our existing AMBER/GREEN stance continues to make sense. AndI note that the shares have traded higher than the current level in the recent past:

Roland's Section

Supreme (LON:SUP)

Up 8% at 154p (£183m) - Trading Statement - Roland - AMBER/GREEN =

It’s a short-but-sweet update from vaping and consumer goods group Supreme this morning, with an upgrade to guidance for the year ended 31 March 2026:

FY26 revenue and adjusted EBITDA expected to be significantly ahead of expectations.

Strong growth in vape sales and “a positive impact from acquisitions and new products” are said to have resulted in “a strong performance across FY26” with “record financial results”.

Vaping category sales are expected to be >10% higher than the prior year, even with impact of the UK ban on disposable sales from 1 June 2025;

Drinks & Wellness category performed strongly, “boosted by an excellent contribution from Slimfast”.

This is clearly good news, but I think the company’s claim of record results is being quite heavily spun and deserves some context. Supreme’s profits were previously expected to fall this year. On some measures, they still are.

Here’s a summary of last year’s results and today’s new guidance:

FY26 revenue up 15% to c.£265m (previous consensus c.£245m);

FY26 adj EBITDA of £40.6m (previous consensus c.£37m).

FY25 actual: Revenue £231m, adj EBITDA £40.5m

As we can see, sales were indeed at record levels last year. However, I would struggle to describe a £100k increase on EBITDA of £40m (<1%) as a record result.

Updated Outlook & Forecasts: with thanks to Shore Capital, we can see that earnings are still expected to be lower than last year:

FY25 actual adj EPS: 21.6p

FY26E adj EPS: 19.6p (+15% versus 17.0p previously)

FY27E adj EPS: 18.7p (unchanged today)

Interestingly, Shore’s unchanged FY27 EPS estimate of 18.7p is well below that of Zeus (20.6p in Nov 25) and Equity Development (22.2p in Nov 25). This is reflected in the FY27 consensus figure of 20.5p shown in the StockReport:

I’m surprised by the wide range of estimates for FY27. My guess is that some analysts have discounted the planned introduction of a UK Vaping Tax in October this year more heavily than others, who may have adopted a wait-and-see approach.

Roland’s view

Supreme has good scale and distribution in the UK market and is well run, in my view, by family owner and CEO Sandy Chadha (54% shareholding).

Although the majority of Supreme’s profits still come from vaping, the business is gradually expanding into branded drinks (e.g. Tyhpoo tea, Clearly Drinks and various other areas such as Slimfast and sports nutrition.)

The group’s vaping exposure won’t suit everyone and does carry some regulatory risk. Following last year’s UK ban on disposable sales, the potential impact of this year’s vaping tax remains unclear.

I recognise these risks, but in my view they are most likely already priced into the shares:

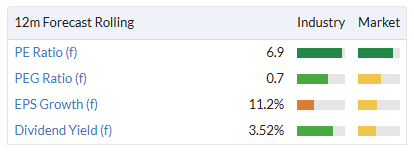

Although this isn’t a business for which I’d pay a high multiple of earnings, I do think the current valuation looks undemanding given Supreme’s strong profitability:

I was AMBER/GREEN on Supreme in September. The stock was also flagged up when I looked at Slater Investments’ holdings in February – Slater remains a significant shareholder, at c.4.7%.

Supreme also qualifies for one of my favourite Guru screens, Greenblatt’s Magic Formula.

The shares have been on a steady decline for most of the last year, but have perked up recently:

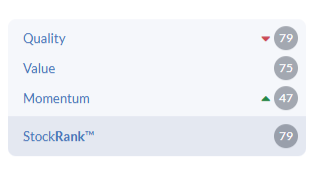

Given the combination of today’s upgrade and the declining trend in earnings from FY25-FY27, I am going to leave my moderately positive view unchanged today. This is also consistent with the StockRanks’ Neutral styling and high 70s score:

Renishaw (LON:RSW)

Up 6.5% at 4,450p (£3.2bn) - Trading Statement - Roland - AMBER/GREEN =

Today we have an upgrade to expectations for the year ending 30 June from this FTSE 250 specialist in high-precision measuring and manufacturing systems.

Trading commentary: today’s RNS is extremely short but highlights strength in a number of key customer sectors:

Since our H1 results announcement on 11 February, we have seen particularly strong demand from customers in the semiconductor and electronics manufacturing equipment, and aerospace & defence sectors, with a further substantial expansion of our order book.

Checking back to February’s half-year results, semiconductors, electronics and defence were all mentioned as areas where performance was strong. So perhaps we shouldn’t be too surprised by today’s upgrade, given the wider backdrop.

Renishaw’s management does acknowledge the wider macro challenges facing today’s market, but doesn’t sound too concerned by them:

We are actively managing the challenges and increasing costs imposed by ongoing economic and geopolitical uncertainties and supply chain pressures.

Outlook & Updated Guidance:

The StockReport shows nine brokers covering Renishaw, but none of them seem to make their coverage available on Research Tree.

Happily, the company has provided clear financial guidance today. By comparing this to the equivalent figures from February I’ve been able to gauge the scale of the upgrade:

FY26 revenue: £775m to £805m (previously £740m to £780m);

FY26 revenue: +4% midpoint upgrade

This is a fairly modest upgrade to revenue, as we might expect at this late stage in the year (y/e 30 June).

However, a larger upgrade to profit guidance suggests that full-year margins are now expected to be higher than previously anticipated – good news:

Adjusted pre-tax profit: £145m to £165m (previously £132m to £157m);

FY26 adj pre-tax profit +7% midpoint upgrade

Roland’s view

I see Renishaw as a good quality, differentiated business with valuable IP and engineering expertise.

Having admired the business for many years, I somehow failed to take advantage of the opportunity to buy the shares in the low £20s in April last year.

Fast-forward 12 months and the shares have doubled to £44:

Is there still an attractive opportunity here? Let’s take a look at the numbers.

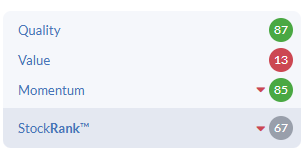

The StockRanks view Renishaw as a High Flyer. This is reflected in high Quality and Momentum scores and a (very) low ValueRank:

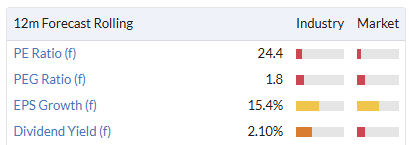

Renishaw’s share price has risen by around 6.5% today, mirroring the increase in pre-tax profit guidance. I think it’s fair to assume that the stock’s valuation metrics will remain broadly unchanged following this upgrade:

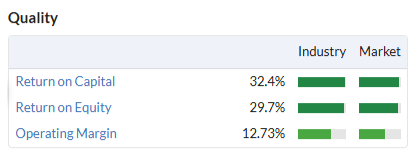

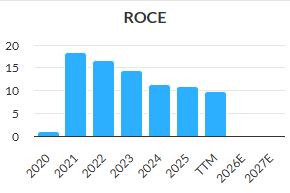

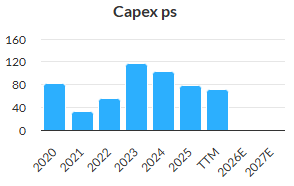

Although Renishaw’s profitability metrics have weakened in recent years, I think some of this reflects cyclical trends and renewed investment within the business – capex has peaked and is now falling:

Last year’s results flagged up an expected improvement in margins for FY26. If earnings momentum remains positive, as forecast, then I think it’s reasonable to expect Renishaw’s quality metrics to start recovering from FY26 onwards:

I upgraded our view on Renishaw to AMBER/GREEN in September following the group’s FY25 results.

While the shares certainly aren’t cheap on a near-term view, this business has an impressive long-term track record of growth and innovation. I don’t see any reason why that shouldn’t continue.

I think there’s also the possibility, at some stage, of a takeover bid.

On balance I think it’s fair to remain broadly positive, so I am leaving my view unchanged today.

See what our investor community has to say

Enjoying the free article? Unlock access to all subscriber comments and dive deeper into discussions from our experienced community of private investors. Don't miss out on valuable insights. Start your free trial today!

Start your free trialWe require a payment card to verify your account, but you can cancel anytime with a single click and won’t be charged.