Good morning!

There has been little change in the macro situation overnight: the FTSE is at 10,600, Brent crude is at $95, and US-Iran talks are set to happen over the next two days.

All the while, 800 vessels remain trapped in the Persian gulf, with the majority of them being oil tankers and other carriers of fuels.

Done for today, thanks for your patience! Spreadsheet accompanying this report: link.

Companies Reporting

| Name (Mkt Cap) | RNS | Summary | Our view (Author) |

|---|---|---|---|

AstraZeneca (LON:AZN) (£232bn | SR74) | Positive high-level results from a prespecified interim analysis of the I CAN Phase III trial showed that Ultomiris (ravulizumab) met its primary endpoint, demonstrating a statistically significant and clinically meaningful reduction of proteinuria. | ||

Rio Tinto (LON:RIO) (£120bn | SR85) | Q1 copper production +9%, iron ore production +12%, although weather disruption means shipments only rose by 2%. No change to 2026 guidance. | ||

Experian (LON:EXPN) (£26bn | SR44) | Adam Crozier to be Chair after AGM in July. Currently Chair of BT Group, previously Chair of Whitbread and ASOS. | ||

Associated British Foods (LON:ABF) (£13.3bn | SR73) | Outcome of its review of Group Structure & Interim Results Announcements | Has decided to proceed with a demerger of Primark and Foodco. Both Primark and Foodco to be listed. H1 results: revenue down 2%, adj. operating profit down 18%. Outlook: “Our full year outlook is currently unchanged, with the exception of Sugar where we now expect an adjusted operating loss in 2026.” Continues to expect H2 weighting. | |

British Land (LON:BLND) (£3.96bn | SR54) | FY26 Underlying EPS of 28.9p, ahead of guidance. Also upgrading FY27 Underlying EPS guidance to at least 30.5p (previously 30.2p). | ||

Integrafin Holdings (LON:IHP) (£1.13bn | SR51) | Total Group revenue is expected to be up 11% at c.£85.8m for H1 FY26. No change to cost guidance given in December 2025. | ||

Jupiter Fund Management (LON:JUP) (£807m | SR95) | AUM +27% since year-end driven by CCLA acquisition and positive net inflows (£1.5bn). | GREEN = (Graham) | |

XPS Pensions (LON:XPS) (£659m | SR52) | Strong revenue growth coupled with ongoing disciplined cost management and delivery of operating efficiencies means the Board is confident of achieving full year results in line with expectations. | ||

THG (LON:THG) (£654m | SR40) | Revenue +7% at constant currency. Full year guidance reiterated. | ||

Griffin Mining (LON:GFM) (£512m | SR53) | “Extremely pleased” to announce that the first production blast in Zone II was completed yesterday. | ||

Ibstock (LON:IBST) (£423m | SR31) | The new CFO joins from Mpac where he has been CFO since 2018. Expected to start in August. | ||

VAALCO Energy (LON:EGY) (£412m | SR61) | Positive operational updates in Gabon regarding the ongoing drilling program. Excellent initial flow rate of approximately 4,850 gross barrels of oil per day, 2,850 net to Vaalco. | ||

ACG Metals (LON:ACG) (£375m | SR48) | Total production of 12,168 oz AuEq in Q1 2026, down 22% year-on-year, as expected. C1 cash costs down 12%. AISC rose 49% due to higher royalties on higher gold and silver prices. It was “a strong start to the year for ACG”. | ||

Avacta (LON:AVCT) (£351m | SR31) | Giving two presentations today at the American Association for Cancer Research Annual Meeting 2026. “The data being presented at AACR underline the potential of our pre|CISION® technology and AVA6103 to make a considerable difference to cancer patients.” | ||

Nichols (LON:NICL) (£339m | SR73) | Q1 revenue +4.3%, in line with expectations. Net cash £59.8m. FY26 revenue and adjusted PBT expectations are unchanged. | ||

Capital (LON:CAPD) (£282m | SR99) | Q1 revenue +41.6% year-on-year as a mining contract commenced (£18m vs. £0.6m last year). The drilling business performed “well” (revenue +8.8%). Full year revenue guidance is reiterated. | AMBER/GREEN = (Roland) Today’s trading update shows good progress in a number of areas, although my feeling from executive chair Jamie Boynton’s commentary is that the company’s investment portfolio is not doing as well this year, after reporting strong (mostly unrealised) gains last year. Broker forecasts are unchanged today, suggesting Capital is performing in line with expectations rather than ahead of them. The valuation still looks reasonable to me here and I think a broadly positive view remains fair. | |

Crest Nicholson Holdings (LON:CRST) (£278m | SR45) | Taking a more cautious view on sales, reducing volume expectations to 1,400 to 1,500 units (previously 1,550 to 1,700 units). Also anticipating a reduced number of land sales, with expected revenue of c. £40m (previously £75m to £100m). New EBIT guidance £5m to £15m, new net debt guidance of £100-120m. | BLACK (RED ↓) (Roland) Today’s update flags up a 79% reduction in EBIT guidance and a very large increase in year-end debt forecasts. The company is now in talks to relax its lending covenants and appears to be accelerating efforts to liquidate existing inventory. I think it’s prudent to take a negative view ahead of the company’s interim results, when we should get more clarity on the order pipeline and balance sheet situation. | |

S&U (LON:SUS) (£244m | SR96) | Profit before tax £31.8m (2025: £24.0m). Net assets £249m. “The current recovery shows we are on the right track, but challenges and necessary improvements remain - alongside real opportunities for growth.” | GREEN = (Graham) [no section below] I’m a broken record on this stock. Today' s results aren’t going to change my tune, with PBT bouncing back strongly and I think slightly beating expectations. PBT has been higher than this historically, and the overall size of the business is bigger than ever, so there is plenty of room for PBT to continue on this upward trajectory for the next few years - especially considering that the regulatory uncertainty and interventions have now ended. In the company’s words: “Advantage (the motor finance division) has seen a significant recovery following the regulatory, legal and fiscal onslaught of the previous two years.” The market cap is trading close to NAV, which is fair enough, but given the quality of the track record and management here I’m happy to remain positive. This is a family business which is managed to last for the long run. | |

Cab Payments Holdings (LON:CABP) (£230m | SR47) | Total income for Q1 2026 grew c.35%. “Excluding a non-repeating dislocation in Q4 2025, as previously highlighted, sequential QoQ performance was broadly flat and ahead of plan.” Medium term guidance unchanged. | ||

Supreme (LON:SUP) (£178m | SR80) | Entered five-year licensing agreement with Carabao, an energy drink. Supreme will manufacture and distribute Carabao energy and isotonic drinks in the UK. Zeus upgrades FY26E adj EPS to 19.6p (prev. 18.0p) to reflect yesterday’s update. No change to FY27 estimates. | ||

Accsys Technologies (LON:AXS) (£163m | SR43) | Revenue up 12% to €153m, with sales volumes +6% to 60,384m3. Expects FY26 adj EBITDA to be in line with consensus of €21m. | ||

Activeops (LON:AOM) (£147m | SR38) | Revenue to be up 48% to £45m, ahead of expectations. Adj EBITDA to be £4.2m, “marginally ahead” of expectations. Outlook: strong end to FY26 provides “a healthy position” for further progress in FY27. | ||

MPAC (LON:MPAC) (£78m | SR26) | Revenue up 26%, adj pre-tax profit up 27% to £13.5m. Order book stabilised in H2 but was down 24% to £90m at the year end. Outlook: in line with expectations, with H2 weighting as in previous years. Current order book provides c.66% coverage of 2026 revenue. Some risk of disruption to client decisions due to the Middle East. | RED ↓ (Graham) | |

Likewise (LON:LIKE) (£58m | SR42) | Acquired freehold for a 2nd distribution centre in Leeds for £3m, using existing bank facilities. Q1 revenue up 15%, implying a significant increase in market share. Considering further growth investments. | ||

Billington Holdings (LON:BILN) (£54m | SR95) | Revenue down 15% to £96m, adjusted pre-tax profit down 62% to £4.1m. Dividend of 11p (2024: 25p). Expect improved 2026 result, in line with expectations. | ||

Intercede (LON:IGP) (£53m | SR37) | Further contract wins since 9 April include MyID CMS licence sales to UK and US government clients (total $3.7m) and a $0.1m renewal with a US Federal Agency. No change to Cavendish forecasts today. | AMBER/RED = (Roland) [no section below] Today’s market reaction seems a little over-egged to me, given that there are no changes to forecasts from Intercede’s house broker today. It’s also worth noting that the 9 April update referred to today wasn’t an upgrade either – the new orders and renewals reported were simply in line with expectations. Prior to that, forecasts were cut in March. As far as I can see, this is another example of a small cap reporting business-as-usual contract wins in a rather promotional way. With the stock trading on a FY26E P/E of 20 after today’s gains, I am going to maintain our moderately negative view on this business until there’s more tangible evidence profits have returned to growth. | |

Gear4music (HOLDINGS) (LON:G4M) (£51m | SR89) | FY26 performance ahead of recently upgraded expectations. Sales up 30% to £191m. FY26 pre-tax profit to be not less than £9.7m (previous Singer forecast: £9.3m). FY27 outlook: trading to date is in line with expectations. | GREEN = (Roland) Today’s update is the seventh consecutive upgrade to FY26 guidance from this founder-led online retailer. While there’s no change to FY27 forecasts (profit is expected to fall as the cost base expands to support a new warehouse), I think the recent share price pullback discounts much of this risk. I am also unwilling to bet against a business that appears to be executing well and has strong momentum. For these reasons, I’m leaving our positive view unchanged today. | |

System1 (LON:SYS1) (£38m | SR69) | Relationship Agreement with Brave Bison & Q4 and Full Year Trading Update | FY revenue steady at £37m, in line with previous guidance. Strong recovery in Platform revenue in H2. Adj EBITDA down 45% to £3.3m. FY27 outlook in line with market expectations. Brave Bison can appoint a board observer, reflecting its status as 27.85% shareholder. | AMBER/GREEN = (Graham)

We are moderately positive on the stock, and I see no reason to change stance today. However, I can understand why long-term shareholders might feel dissatisfied. It’s been stop-start here for years, with the company’s evolution leading to higher revenues but no sustained increase in profitability. Despite the company’s emphasis on automated marketing tools, it has been a long wait for these efforts to scale profitably. Perhaps a takeover by a larger group is becoming the most logical outcome? |

Everyman Media (LON:EMAN) (£31m | SR40) | Farah Golant CBE is appointed CEO with immediate effect, having been interim CEO since 1 January 2026. Results due on 28 April 2026. | ||

Windar Photonics (LON:WPHO) (£30m | SR10) | Appoints Andreas Berg Nielsen as CEO, effective 1 June 2025. He is currently a NED and has previous experience in the wind energy and industrial B2B sector. | ||

Checkit (LON:CKT) (£26m | SR41) | Adj EBITDA up 113% to £0.3m, ahead of previous guidance for breakeven. ARR up 1% to £14.3m, with £4m cost saving programme completed. Formal sale process ongoing. FY27: will retire a legacy product in order to free up resources needed to upgrade solutions. This “more than doubles our penetration potential”. | ||

Abingdon Health (LON:ABDX) (£26m | SR24) | Trading will begin today on the OTCQB Venture Market in the US under the ticker ABDXF. | ||

Genedrive (LON:GDR) (£16m | SR11) | NHS England has published a market engagement notice relating to the procurement strategy for rapid genetic MT-RNR1 testing in neonates to prevent antibiotic induced hearing loss. Genedrive’s products are already in use in some trusts and management believes it’s well positioned to compete for the tender. | ||

Ebiquity (LON:EBQ) (£16m | SR21) | Revenue down 4%, adj pre-tax profit down 82% to £1.1m. Good performance in UK & Ireland offset by “challenges in North America and Europe”. Q1 began “encouragingly”, expects Q2 to provide “greater visibility on the full year outturn”. | ||

IXICO (LON:IXI) (£16m | SR19) | H1 revenue to be up 23%, with gross margin to be 53% (H1 25: 50%). Order book of £18.1m, +38% vs 31 March 25. Trading in line with FY expectations. | ||

Facilities by ADF (LON:ADF) (£12m | SR35) | Revenue up 17%, adjusted EBITDA up 28% to £9.2m driven by acquisitions. Q1 2026 trading in line with expectations, FY26 to show similar H2 weighting to FY25, reflecting current production patterns. |

Graham's Section

Jupiter Fund Management (LON:JUP)

Up 3% at 156.8p (£828m) - Trading Update and Notice of Results - Graham - GREEN =

I’ve stayed positive on this one for momentum reasons (see here) with the original value thesis having already played out::

The positive momentum continues in the business.

Highlights from today’s update:

AUM up £14.4bn in the quarter, to £68.4bn

£15bn of additional AUM came in as the acquisition of CCLA completed

Positive net inflows of £1.5bn, including small net inflows during the turmoil in March (excluding CCLA).

CCLA itself saw small outflows during the quarter, and market movements were negative.

As a reminder, Jupiter has paid £100m for CCLA: a very cheap deal to my eyes, receiving £150 of AUM for every £1 they spent buying it.

That’s about half of the price of Jupiter shares currently (you’d get £83 of AUM for every £1 spent on Jupiter shares today).

A quick note on market sentiment:

Market sentiment has clearly shifted materially in recent weeks in response to geopolitical events. It is too early to tell if this represents a sustained change in client appetite towards risk assets or whether it will be more short-term and transitory. Despite the external environment, Jupiter remains in a stronger position today than we have been for a number of years and, with a broader, more diversified set of investment capabilities, are well-placed to take advantage of the opportunities that lie ahead.

Graham’s view

I respect the momentum at work here, and will stay positive. There are a few fund management businesses on my GREEN list - and Jupiter is one of them.

Ever since Matthew Beesley was hired as CEO in 2022, I thought his plans were remarkably logical - primarily around cost control and simplification in a tough environment.

Patient shareholders have been rewarded with positive net inflows, a cheap acquisition significantly boosting AUM, and a recovery in the share price.

The StockRank is 95 and my view is consistent with what the algorithms are saying here:

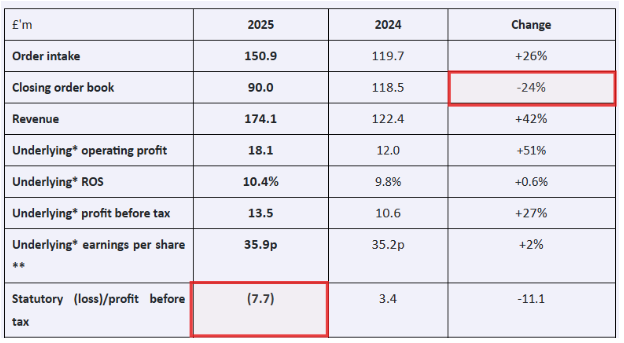

MPAC (LON:MPAC)

Down 10% at 234p (£70m) - Graham - Full Year Results and CFO Succession - Graham - RED ↓

Mpac Group plc, the global packaging and automation solutions Group, today announces its results for the 12 months to 31 December 2025 ("FY25").

We’ve been neutral on this one (see here), and our lack of excitement seems justified given the reaction to today’s results.

Today’s financial highlights don’t look too bad at first glance, but the order book has fallen 24% year-on-year, and the statutory result - i.e. the result without any adjustments - is poor.

Those two facts are highlighted in red below:

The list of adjustments (adding up to £21m) includes the usual categories, plus a few others.

A “customer dispute” cost £1.9m. “Reorganisation and site closures costs” were £3.4m.

If we want to ignore amortisation (£6m) and impairment (£8.4m), that’s fair enough, but in that case let’s not assume that the company’s intangible assets are worth anything.

If the intangibles are worthless, the balance sheet is left with net tangible assets of minus £33m, implying zero support for the share price coming from the balance sheet.

The net debt figure is £47.9m, which is now not all that far away from the company’s market cap (a signal I look out for).

Outlook

This isn’t terrible, but it is cautious, and sounds like the precursor to a downgrade:

The Group remains in line with full year market expectations, which as in previous years will be second half weighted, but, in the context of increasingly uncertain market conditions, it is difficult to predict the full impact of the Middle East conflict on the timing of customer capital investment decisions.

The combination of an H2 weighing and limited visibility implies a very high risk of a profit warning.

On the bright side, the company says that the order book stabilised in H2.

Estimates at ShoreCap are unchanged. Adj. PBT of £15.1m this year, then rising to £17.6m in 2027.

Graham’s view

What really irks me about these results is that the company doesn’t tell us plainly what the organic growth rates were.

For example, one of the acquired companies (CSi Palletising) generated €71.5m of revenues in 2023. That takeover completed in November 2024. So a comparison of 2025 vs. 2024 revenues for Mpac as a whole isn’t meaningful. Organic growth rates should be spelled out clearly.

Conclusion - normally, with a profit warning from a company we are neutral on, I’d take it down to AMBER/RED.

However, in this case, there’s a fragile balance sheet and a reporting style that I haven’t found helpful.

On top of that, a separate announcement today reveals that the CFO is leaving. He’s going to Ibstock (LON:IBST). The CFO jumping ship is a classic red flag.

I’m therefore taking our view on this all the way down to RED.

It might offer value at the current level - there is every chance I’ll take our view back to neutral in a few months. It could be worth investigating further. But today’s data points would steer me away from taking a chance on it for the time being.

System1 (LON:SYS1)

Down 2% at 292.56p (£37m) - Q4 & Full Year Trading Update - Graham - AMBER/GREEN =

Let’s check out the latest from this “marketing decision-making platform”:

Full-year revenue “steady” at £37m (prior year: £37.4m)

H2 was up 4% year-on-year

Adjusted PBT £2.1m (prior year: £5.2m), “in line with previous guidance”.

The year-end cash position £12.4m, and operating expenses are reduced by £1m per annum.

Outlook:

The strong level of new business wins secured throughout FY26 and particularly in the final quarter, provide confidence in delivering revenue and profit growth in FY27, in line with consensus market expectations.

Estimates from Singer, published earlier this month, suggest that adj. PBT can nearly double to £3.9m in FY27, with high operational gearing on increased revenues. Although that result still wouldn’t match what the company achieved in FY27.

CEO comment:

FY26 has seen the successful delivery on our plans to grow in the USA, revitalise our Innovation product offering and increase the number of the world's largest brands as customers. This progress against a challenging macro-economic environment delivered a resilient FY26 performance, a record H2 performance and places the business on an upwards trajectory into FY27.

Graham’s view

It’s been stop-start here for years, with the company’s evolution leading to higher revenues but no sustained increase in profitability.

We are moderately positive on the stock, and I see no reason to change stance today.

However, I can understand why long-term shareholders might feel dissatisfied.

Despite the company’s emphasis on automated marketing tools, it has been a long wait for these efforts to scale profitably.

Is there a larger marketing group that would make a more profitable home for the company’s technologies?

Brave Bison (LON:BBSN) are now the largest shareholder. If not them, then perhaps someone else might start digging around here for a complete takeover? The healthy cash position would help to fund any deal.

Here’s an example of the multiples involved: the adjusted EBITDA forecast for the current year is nearly £5m, while the enterprise value is only £25m. So EV/EBITDA is 5x. That’s the sort of multiple that makes takeovers happen.

As a standalone investment, however, I think we need more proof that the business is scaling on its own, before we get too enthusiastic.

Roland's Section

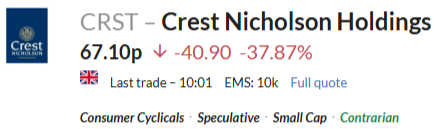

Crest Nicholson Holdings (LON:CRST)

Down 39% at 65.8p (£169m) - Title - Roland - BLACK (RED ↓)

Commiserations to shareholders here this morning – this is a big profit warning.

I estimate that this troubled housebuilder has cut 2026 profit forecasts by more than 75% today, while increasing its debt guidance. That’s not a good combination!

Management blames macro uncertainty:

Since the Group's AGM trading update on 25 March, macro-uncertainty has increased, with the ongoing conflict in the Middle East contributing to the prospect of a more prolonged higher interest rate environment, renewed cost pressures and a deterioration in consumer confidence.

Market conditions for housebuilders are certainly difficult, as I’ve discussed in these pages a number of times recently. However, I’m pretty sure that some of Crest’s issues are internal. As Graham noted in November, this business appears somewhat accident prone. Earnings forecasts have already seen multiple downgrades over the last 18 months:

Here are is the from today’s update, which covers the current financial year (since 1 Nov 25):

Home Sales: “Open market reservations have continued in line with the improved levels seen since mid-January.” Trading is positive in the Midlands, South-West and Eastern divisions, but softer in the South. Use of incentives and discounting has remained stable, but new enquiries have fallen.

Land Sales: Crest has completed one sale so far this year, but the market has softened and buyers are increasingly “reluctant to transact at market values”.

Outlook & Revised Guidance

As a result of softer market conditions, the company has now cut its guidance for both new home sales and land sales in FY26 (y/e 31 Oct):

Home sales: expected completions: 1,400 to 1,500 units (previously 1,550 to 1,700)

Current order book: 1,106

Land sales: now expected to total c.£40m (previously £70-100m). Management no longer expects to make any meaningful profit on land sales this year.

Unfortunately this operational slowdown means that profits are expected to be c.79% lower than previously expected, while borrowing levels are expected to be much higher:

FY26 EBIT (operating profit): now expected to be “around £5m to £15m” (my estimate: previously c.£47m)

FY26 interest costs: c.£15m (previously £10m to £12m)

Year-end net debt: £100 to £120m (previously £15m to £65m)

(The company’s previous guidance in January listed interest costs and pre-tax profit (not EBIT), so to get a comparable figure for today’s EBIT guidance I have simply added the mid-points of previous PBT and interest cost guidance.)

Unsurprisingly, the company is now stepping up efforts to sell off its completed inventory, while tightening control on spending on current developments. In a soft market, I would speculate that this is likely to require additional discounting or incentives, adding pressure to margins.

Higher energy costs are also expected to result in higher build costs this year.

Balance sheet worries? This situation has added pressure to Crest Nicholson’s balance sheet. This was already looking a little tight in our view – the previous two sets of accounts have both included going concern warnings on interest cover.

Today we learn the company is in talks to relax its lending covenants. There’s no suggestion Crest Nicholson is likely to become financially distressed, but the fact it’s under discussion is a risk from an equity perspective.

Roland’s view

Last year’s decision to pivot to become a “leading player in the mid-premium housing market” does not seem to be delivering the hoped-for results.

I wonder if performance would have been better if the company had redoubled its focus on bulk and affordable housing. These categories accounted for 35% of units sold last year, but the intention was to phase these out starting in FY26 and there was no mention of either category in today’s update.

While it’s true that market conditions are difficult, I think the real issue here for equity investors is the level of debt in the business.

Many of Crest’s peers have gone into this slowdown with strong net cash positions. This is allowing them to maintain optionality over land purchases and development timings. It also means they aren’t under pressure from lenders to liquidate their inventories and generate cash – something I suspect Crest is now experiencing.

This morning’s share price drop has left Crest shares trading at a 75% discount to its last-reported net asset value of 279p per share.

While such a large discount may seem tempting, I am inclined to view it as a warning flag for equity investors, for two reasons:

The combination of lower sales and a higher net debt position this year is likely to mean that Crest’s book value falls when its interim results are published;

There could be a growing risk that the company will need an equity raise to reduce debt and allow it to trade its way out of the current slowdown.

Graham downgraded our view to AMBER/RED in November, based on our disciplined approach to balance sheet risk.

I am going to move down another notch to RED today ahead of the interim results. I would not consider investing here until there’s some evidence the company can trade its way out of this dip without needing refinancing.

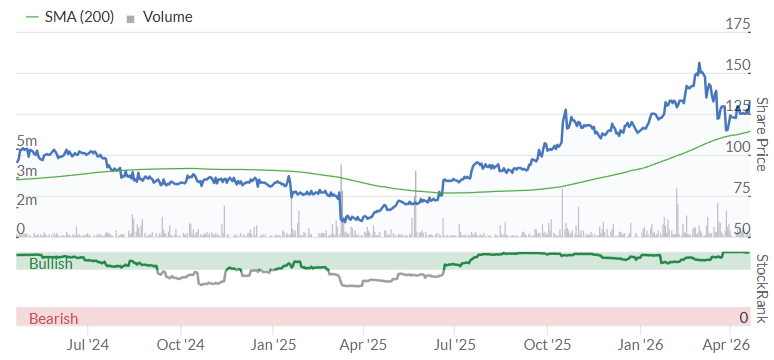

Gear4music (HOLDINGS) (LON:G4M)

Up 13% at 274p (£57.5m) - Trading Update - Roland - GREEN =

Musical equipment retailer Gear4Music has upgraded its profit guidance in each of its last seven trading updates, starting in June 2025.

The catch is that each of these upgrades has related to the FY26 financial year, which ended on 31 March. Brokers have been much more sparing in upgrading FY27 forecasts, with the result that profits are now expected to fall this year. Today’s update also leaves FY27 guidance unchanged:

What investors need to decide is whether the momentum displayed over the 12 months is likely to persist, potentially leading to FY27 upgrades.

Recent share price action suggests mixed views in the market (and perhaps some profit taking after a 100% gain in 12 months):

Let’s start with a closer look at today’s update.

Year-end trading update (y/e 31 Mar 26)

Gear4Music has clearly put in a stonking performance over the last year. Today’s guidance is ahead of forecasts, with pre-tax profit 4% higher than previous consensus:

Revenue up 30% to £190.7m, with UK +26% and Europe/ROW +36%;

Gross margin up 1.4% to 28.4%

Adjusted EBITDA to be up by “not less than” 81% to at least £18.1m

Pre-tax profit not less than £9.7m (FY25: £1.6m)

Net debt reduced to £5m (FY25: £6.4m), after £3.6m pre-payment on new warehouse

Previous consensus was for revenue of £186.4m and pre-tax profit of £9.3m, according to the company.

The company gives a shout out to new technical tools that have launched recently and are said to be supporting growth. The impact of such initiatives is sometimes hard to measure, but I think it’s good to see the company continuing to invest in efficiency and digital marketing:

AI based inventory forecasting and purchasing platform

Digital promotions centre

Website AI chatbot

Management commentary: Executive Chairman and founder Andrew Wass is certainly motivated to build a sustainable recovery. The value of his shareholding has risen from £6.5m to more than £12m over the last 12 months.

Today, he strikes a fairly positive note about the outlook for the current year (my bold):

Whilst it remains early in the financial year and the Board has not yet made any changes to FY27 forecasts, it remains confident that the business will build on the substantial financial progress achieved in FY26. Trading in FY27 to date is in line with consensus market expectations.

FY27 outlook

The company says FY27 trading so far is in line with consensus expectations. Gear4Music helpfully includes its view of consensus within today’s update:

FY27E revenue: £200.2m

FY27E adj EBITDA: £16.0m

FY27E adj pre-tax profit: £6.0m

FY27E adj EPS: 33.0p (courtesy of Progressive Research, previously 31.6p)

These estimates are, respectively, 5% ahead, 11% below and 62% below today’s FY26 guidance.

The large fall in forecast pre-tax profit reflects two factors:

An increase in the company’s operating cost base as its new warehouse becomes operational and higher wage and energy costs are annualised;

A reduction in expected gross margin in FY27.

A new note from Progressive Research today – many thanks – gives us the following detail on these margin pressures:

FY27E operating costs are expected to rise by 10% to £39.7m;

FY27E gross margin is expected to fall by 0.6% to 27.8%.

Higher revenue is expected to cancel out the lower gross margin, resulting in a modest increase in gross profit.

But a much larger increase in revenue would be needed to offset the increase in operating costs, hence the expected fall in pre-tax profit this year.

Roland’s view

Graham upgraded Gear4Music to GREEN in January, noting the terrific series of upgrades to EPS forecasts; today’s updated Progressive FY26E estimate of 33p is more than three times the 9p consensus estimate from April 2025.

While I have some slight nervousness about FY27, I think the recent pullback in the share price means that much of the expected reduction in earnings this year is already priced in.

Gear4Music’s current valuation doesn’t seem unreasonable to me:

To my mind, today’s commentary leaves room for upgrades to FY27 forecasts if current trading conditions remain stable.

I’m going to leave our positive view unchanged today out of respect for the impressive momentum in this business currently.

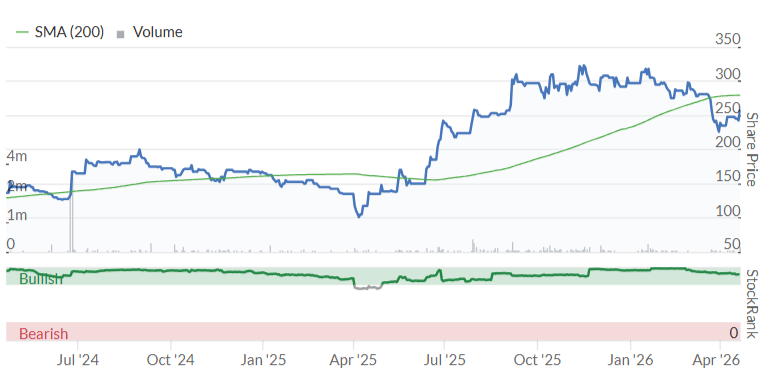

Capital (LON:CAPD)

Up 5.5% at 132p (£294m) - Q1 2026 Trading Update - Roland - AMBER/GREEN =

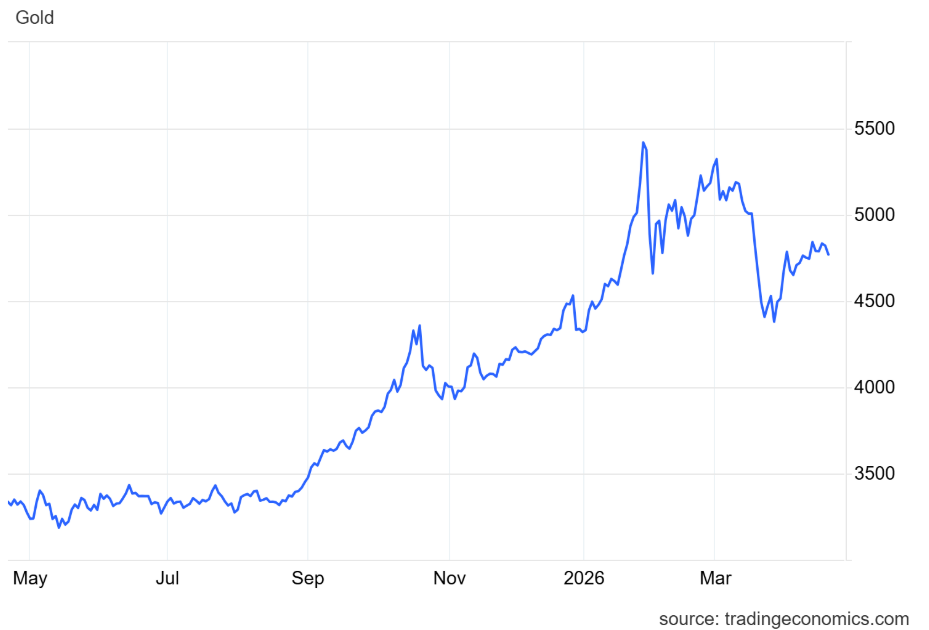

Investors who bought back into gold mining services specialist Capital when co-founder Jamie Boynton took control again in March 2025 have been well rewarded. The stock’s discount to book value has been erased and the share price has doubled.

Of course, this recovery may not just reflect Boynton’s leadership – this period has also corresponded with a remarkable period for the gold price:

When I last looked at Capital in October 2025, I upgraded our view to AMBER/GREEN, noting recent earnings upgrades.

Today’s update leaves 2026 guidance unchanged but does strike a fairly positive note:

Q1 revenue of $101.7m (+41.6% vs Q1 25 and +9.7% vs Q4 25);

Drilling and associated revenue up 4.3% to $62.8m vs Q4 25;

Mining revenue up 65.1% to $18m vs Q4 25;

MSALABS revenue down 3.2% to $20.9m vs Q4 25

Trading in line with 2026 revenue guidance of $410m to $440m;

Operationally, Capital reports solid progress during the quarter, albeit with a reduction in fleet utilisation:

Total fleet utilisation 70% (Q4 25: 74%)

Average monthly revenue per operating rig (ARPOR): up 7.5% to $201k vs Q4 25

Reko Diq mining contract is underway, with both fleets now being double shifted;

Re-commenced waste mining at Sukari under new contract;

MSALABS laboratory utilisation increased to 53% (Q1 25: 40%);

Newfoundland lab has started receiving samples, two further laboratories are under construction.

There are various new contract wins, including:

A 5-year deep hole mining contract at Sukari, in Egypt;

A 3-year drilling contract at the Kiniero Gold Project in Guyana.

Trading commentary: the company says it has not been directly affected by events in the Middle East, but has seen some impact on personnel and logistics. Capital’s investment portfolio (mostly gold miners) has also been hit “by a general slide in global equity markets”.

Full run rates are expected on Capital’s two mining contracts later this year, supporting revenue guidance.

Management also notes “strong tendering activity”, with good demand driven by record commodity prices and capital markets activity – in other words, gold is still booming.

Outlook - with thanks to Panmure Liberum, I can see that forecasts are unchanged today:

FY26E adj EPS: $0.15

FY27E adj EPS: $0.20

These estimates put Capital shares on a forward P/E of around 11, which seems fair to me.

Forecasts have been broadly stable for the last six months or so, suggesting the growth reported today is largely priced into existing forecasts:

Roland’s view

Capital’s reported profits can be skewed by unrealised movements in the value of its investment portfolio. This is one of the more unusual parts of this business – in addition to being a mining and drilling contractor, the company also invests in mining equity.

Presumably the company’s industry insight and connections leave it better positioned than most of us to invest profitably.

Last year Capital reported $66m of realised and unrealised investment gains (2024: $12m), but the cash flow statement only showed $4.7m of cash inflows from the sale of investments. If I’ve read this correctly, this meant the company was staying invested in the hope of further gains.

Today’s commentary from Boynton referring to a “general slide” in equity markets leaves me wondering if some of last year’s unrealised gains have now evaporated. If so, I’m a little surprised – my impression is that gold equity prices have remained pretty strong this year.

Time will tell. In the meantime, Capital’s improving operational performance and unchanged guidance mean I’m happy to leave our previous AMBER/GREEN view unchanged today.

See what our investor community has to say

Enjoying the free article? Unlock access to all subscriber comments and dive deeper into discussions from our experienced community of private investors. Don't miss out on valuable insights. Start your free trial today!

Start your free trialWe require a payment card to verify your account, but you can cancel anytime with a single click and won’t be charged.