Good morning!

Hopes of a Middle East deal continued to buoy markets overnight, with Japan’s Nikkei 225 index up 6%. Press reports suggest Iran is reviewing a US-backed proposal that might allow negotiations over Iran’s nuclear program to be pushed back to a later stage.

The suggestion is that President Trump is now keen to find a route out of the current conflict, which has seen average US gas prices rise above $4.50 per gallon and is becoming unpopular with US voters.

After solid gains for stock indices yesterday and a sharp move lower for oil, markets are expected to open broadly flat this morning:

The FTSE 100 to open up by 0.2% at 10,460

S&P 500 to open up by 0.1% at 7,369

Brent Crude at $101 a barrel

Gold at $4,705/oz

The market has flip-flopped a number of times during the conflict, making it hard for investors to know how to successfully position themselves. In a new article yesterday, Gareth looked at some ideas for companies that are poised to benefit from volatility and uncertainty itself, regardless of the eventual outcome. I’d recommend taking a look if you haven’t seen it.

Today's report is now complete, thanks for all your comments. We'll be back in the morning!

Spreadsheet accompanying this report: link.

Companies Reporting

| Name (Mkt Cap) | RNS | Summary | Our view (Author) |

|---|---|---|---|

Shell (LON:SHEL) (£180bn | SR89) | Q1 Unaudited Results & Commencement of a share buyback programme | Adjusted earnings rose by 24% to $6.92bn and were ahead of expectations for $6.05bn, according to Reuters. Growth driven by higher profits from trading, improved refining margins and higher commodity prices. Quarterly buyback reduced from $3.5bn to $3.0bn. | |

BAE Systems (LON:BA.) (£63bn | SR73) | On track to achieve full year guidance with increased defence spending “across all our key markets”. Expects adj EPS to be up by 9% to 11% in 2026. | AMBER/GREEN = (James) BAE reiterated full-year guidance of 7-9% sales growth and 9-11% EPS growth in today’s trading update, but the market has taken the stock down 3% as I write. It’s a sign that at the current elevated valuation - 24x forward earnings and a PEG ratio around 2.4 - that investors need more reassurance. Revenue has compounded consistently at 8-9% organically over the past five years, and there’s unlikely to be a considerable uptick on this. Its quality is undeniable and relative to defence peers, its valuation is not egregious, but a near-term re-rating looks unlikely. | |

Coca-Cola HBC AG (LON:CCH) (£16.1bn | SR86) | Revenue up 12%, driven by 9.6% volume growth (c.3.5% excluding additional selling days). Trading in line with expectations, full-year guidance unchanged. | ||

Intercontinental Hotels (LON:IHG) (£16.1bn | SR81) | Global RevPAR +4.4%, led by EMEAA and Greater China. Growth strongest in Groups (+7%) and Business (+6%) with Leisure weaker (+1%). Average daily rate +2% with occupancy +1.5%. Confident of achieving consensus forecasts. | ||

Flutter Entertainment (LON:FLTR) (£12.7bn | SR12) | Revenue up 17%, average monthly players down 3%. Q1 net income down 38% to $209m, with adj EPS down 23% to $1.22. Full year guidance downgraded: revenue to be $18.305bn with adj EBITDA of $2.865bn (midpoint). Previously $18.4bn and $2.97bn. | BLACK | |

Centrica (LON:CNA) (£9.7bn | SR58) | AGM Statement & Acquisition of the Severn CCGT for c.£370 million | Expect Retail EBITDA to be towards the lower end of guidance, reflecting weather, commodity pricing and bad debts. Guidance for Optimisation EBITDA is unchanged, while Infrastructure EBITDA is to be “above the top end of its guidance range”. Outlook remains subject to “usual uncertainties”. Acquiring Severn CCGT (gas power station) which is expected to contribute £30-60m of EBITDA from 2027. | |

M&G (LON:MNG) (£7.4bn | SR86) | £0.6bn net inflows from new business with AUM of £371bn at 31 March (FY25: £376bn). “... we are confident in our ability to deliver continued growth this year.” | ||

Hiscox (LON:HSX) (£5.0bn | SR52) | Premium income up 10.2% to $1.7bn, driven by growth in retail and big ticket. Loss experience during the quarter “within expectations”. Outlook for 2026 is “positive”. | ||

Lion Finance (LON:BGEO) (£4.8bn | SR65) | 1st Quarter Results & GEL 55 million share buyback extension | Adjusted net profit up 14% to GEL585m, with return on average equity of 27.4% (Q1 25: 28.7%). Loan book +23% YoY, with net asset value per share up 21.5% to GEL 207.82. | |

Harbour Energy (LON:HBR) (£4.4bn | SR98) | Q1 production up 1.2% to 506 kboepd with unit operating costs of $12.8/boe. Net debt increased to $6.3bn (31 Dec 25: $4.4bn) reflecting the LLOG acquisition. 2026 production guidance narrowed to 480-500 kboepd (prev. 475-500 kboepd) with free cash flow outlook increased to $1.4bn based on $80/bbl Brent and $13/mscf European gas (prev. $0.6bn). | AMBER = (Roland) [no section below] I’m happy to maintain my previous neutral view on Harbour Energy today, even though it’s slightly at odds with a StockRank of 98. There are a couple of reasons for this. The main highlight from today’s guidance is the upgraded free cash flow guidance, to $1.4bn (c.£1bn). When compared to a market cap of £4.4bn this looks cheap, but the size of the revision from earlier this year shows how volatile this figure can be: a $5 move in oil (like we saw yesterday) would impact 2026 free cash flow by c.$170m. While it’s probably fair to argue that there’s still a likelihood that oil prices will remain elevated, Harbour’s modest P/E doesn’t tell the whole story. The group’s latest acquisition has left net debt at $6.3bn, meaning debt reduction is likely to be prioritised over the (smaller) dividend this year. As a result, while the valuation looks attractive at current oil prices, it could quickly become less so in a weaker commodity price environment. Given the influence of commodity pricing on the valuation of oil (and gold) stocks, my general practice is to remain neutral during bull market conditions and leave it to sector experts to carry out more detailed valuation estimates. I would note that Harbour's long-time private equity backer, EIG, has been selling down this year. Our data also indicate chemical group BASF has been selling. | |

Balfour Beatty (LON:BBY) (4.2bn | SR84) | Trading well with no change to 2026 guidance. Continues to expect high single digit percentage growth in profit from earnings-based businesses. Forward order book at 31 March was in line with the year end position. | ||

Tritax Big Box REIT (LON:BBOX) (£4.1bn | SR43) | National vacancy reduced by 0.32% to 6.8% in Q1, with an additional 5.3m sq ft let during the period, with an average 13.3% increase in rent across lease events. A total of £10.8m of annual income added during the period. | ||

ROSEBANK INDUSTRIES (LON:ROSE) (£3.7bn | SR8) | ECI trading in line with expectations, completion of MW Components and CPM acquisitions are on track. Admitted to Main Market on 1 May 26, expect to join FTSE 250 in due course. | ||

JD Sports Fashion (LON:JD.) (£3.3bn | SR73) | FY26 revenue up 10.5%, adj pre-tax profit down 7.7% to £852m. Adj EPS down 5.5% to 11.71p. FY27 outlook: “providing a wider range of profit guidance” than previously. Now expects adj pre-tax profit of £750m to £850m (previous consensus c.£840m). | BLACK? (AMBER/GREEN =) (Roland) While headline growth remains slow and profit margins came under pressure last year, my impression is that JD is doing the right things and remains a good, cheap business at a fundamental level. Cash generation is impressive and the balance sheet looks relatively strong to me. While I see today’s FY27 guidance as a modest downgrade, I think the company’s cheap valuation and 10%+ free cash flow yield justify remaining broadly positive here. | |

Rathbones (LON:RAT) (£2.2bn | SR68) | Q1 operating income up 9.4% to £240.7m, with FUMA down slightly to £113.6bn at 31 March (31 Dec: £115.6bn). Q1 net outflows of £0.8bn. | ||

Helios Towers (LON:HTWS) (£2.1bn | SR48) | 2026 guidance upgraded for strengthened tenancy pipeline – 1,406 tenancy additions YTD, with 14% adj EBITDA growth to $127.2m. Now targeting FY26 adj EBITDA of $515m to $530m (prev. $510m to $525m). | AMBER (Roland) We’ve not covered this mobile tower company before, but today’s upgrade highlights strong momentum and – I think – supports the view that profits could rise quickly over coming years. While I’m impressed with operational progress and the growth potential of the company’s African/Middle East markets, I can’t help feeling that some of the good news is already priced in. To reflect this mix, I’ve initiated our coverage by adopting a neutral view today. | |

Great Portland Estates (LON:GPE) (£1.3bn | SR28) | Has let over 6,200 sq ft at 170 Piccadilly, W1. This Fully Managed development is now 73% let or under offer. | ||

Uniphar (LON:UPR) (£938m | SR59) | “2026 has started well, with performance in the first four months in line with the Board's expectations.” | ||

Morgan Advanced Materials (LON:MGAM) (£629m | SR62) | Q1 trading in line with expectations, with revenue up 6.2%. Full-year guidance is unchanged. Not yet seen any material impact from the Middle East conflict and are increasing prices to offset inflation. | AMBER/GREEN ↑ (James) The business is in transformation - a simplification programme is delivering £27m in savings - and a roadmap to 12-14% margins beyond 2028 could lead to a re-rating. The Thermal Products division is under review, and disposal could see the company hit margin targets much sooner than planned. At 12.3x forward earnings and a 0.7 PEG, there’s scope for a re-rating if the transformation continues to deliver. | |

IP (LON:IPO) (£565m | SR53) | Michael Queen appointed as Chair Designate. He is a former CEO of 3i Group. | ||

Pollen Street (LON:POLN) (£511m | SR80) | Total AUM up £1.1bn to £8.2bn during the quarter, “reflecting strong fundraising in Private Credit IV”. Fee-paying AUM up by £0.2bn to £5.4bn. FY26 expectations for net investment return are unchanged. | ||

Johnson Service (LON:JSG) (£498m | SR79) | Q1 revenue up by 1.4%, with organic growth of 0.7%. Workwear rose by 3.9%, while HORECA was down by 0.6%, with “challenging” conditions for price increases and renewals. Remain on track to achieve our targeted adjusted operating margin of at least 14.0% in 2026. | ||

MHA (LON:MHA) (£440m | SR70) | FY26 revenue up 12% to £251m, in line. Adj EBITDA up 12% to £46m, ahead of expectations. Confident in prospects for the current year. | ||

Tharisa (LON:THS) (£356m | SR99) | Concluded a 5-year contract with Cementation Africa Proprietary for underground development works at the Tharisa Mine. The contract is on an open book, cost plus fee basis rather than rates-based, risk transfer model. | ||

S4 Capital (LON:SFOR) (£280m | SR96) | SP -10% Q1 net revenue fell 5% like-for-like to £149.2m, with technology clients - which account for roughly half of revenue - allocating more spend to AI buildout. The uncertainty of the Middle East conflict was also noted as a factor. 2026 like-for-like revenue is expected to be in line with current estimates, slightly below 2025. | AMBER ↑ (Roland) [no section below] Today’s quarterly net revenue figure of £150m suggests to me that a slightly stronger performance will be needed in the remaining nine months of the year to hit consensus forecasts of c.£650m. The company’s heavy exposure to a tech client base is once again flagged as an area of weakness, as clients spend money on AI instead of marketing. In accounting terms, the picture seems more positive. Net debt fell by £33m during the quarter and leverage looks manageable at 1.4x adjusted EBITDA. A further reduction in net debt is expected by the end of the year, together with an increase of at least 1% in the group’s EBITDA margin, albeit from a fairly low level. Graham upgraded our view to AMBER/RED in January. Given the continued reduction in debt and in line guidance today, I’m going to move up a further notch and turn neutral. | |

Petrotal (LON:PTAL) (£253m | SR90) | Adjusted EBITDA rose 90% quarter-on-quarter to $35.1m as stronger Brent prices lifted net realised prices to $51.07/bbl. Management raised full-year adjusted EBITDA guidance to $110-120m from the original $30-40m. | ||

Next 15 (LON:NFG) (£246m | SR70) | Revenue fell 6.3% to £448m as Next 15 cut its portfolio from 22 businesses to 11, and reduced headcount by 16%. Adjusted operation profit fell 8.6% to £67.6m. Management pointed to like-for-like revenue growth in line with market expectations. Auditors flagged uncertainty linked to ongoing Mach49 arbitration. | ||

| Genel Energy (LON:GENL) (£148m | SR38) | Trading and operations update Q1 2026 | Business reported that production at its Tawke licence in Kurdistan was suspended following US-Israeli air strikes against Iran in late February, cutting Q1 gross production to 52,800 bopd from 77,270 bopd in Q4 2025. Limited field operations only restarted on 9 April. The company ended Q1 with net cash of $131m and $88m still overdue from the KRG. | |

Strategic Minerals (LON:SML) (£146m | SR38) | Reanalysis of historical drill core at the Strategic Minerals’ Redmoor tungsten-tin project in Cornwall, using improved analytical methods, revealed previously unreported grades. This includes two new wide intersections of up to 10.85m at 0.33% tin that had not previously been identified. These findings, however, don’t materially impact estimates. | ||

Atlantic Lithium (LON:ALL) (£120m | SR26) | All cash offer for 18.8p per share, a 26.6% premium to last night’s closing price. | TAKEOVER | |

Personal group (LON:PGH) (£120m | SR78) | Reported strong momentum ahead of AGM, with the board expecting to deliver revenue of £54.4m and adjusted EBITDA of £14.1m in line with market expectations. CFO Sarah Mace steps down today after 12 years to be replaced by Matthew Cohen in the coming months. | ||

Strix (LON:KETL) (£91m | SR88) | Reiterated full-year guidance of £150m revenue and adjusted pre-tax profit of £9.8m-£10.2m, and said trading volumes outside China were consistently ahead of the previous year. The company has completed a £10m tender offer at 43p as part of a broader capital returns programme. | ||

Journeo (LON:JNEO) (£72m | SR54) | Infotec subsidiary has secured a $1.2m order to supply display systems to Boston’s MBTA transit network, following earlier deployments in New York MTA. Work has already started and deliveries are expected to complete during 2026. | ||

hVIVO (LON:HVO) (£52m | SR36) | Signed a £6m contract to conduct an influenza human challenge trial for a clinical stage biopharmaceutical company testing a monoclonal antibody, with revenues to be recognised across 2026 and 2027. | ||

Ariana Resources (LON:AAU) (£49m | SR42) | Completes diamond drilling and metallurgical sampling and testwork agreement with Xinhai for 1.12Moz Dokwe gold project in Zimbabwe. Drilling is underway across three rigs as the company works towards an updated pre-feasibility study this quarter. | ||

Light Science Technologies Holdings (LON:LST) (£20m | SR3) | Signs new contract with healthcare client with an initial order worth £160,000 and potential revenues up to £650,000. Company continues to reposition towards higher margin sectors including defence and medical. | ||

NAHL (LON:NAH) (£16m | SR46) | Reported underlying pre-tax profit up 260% to £5m on revenues of £40m - up 3.2% over 12 months. Net debt was cut by 55% to £3.2m at year’s end and further to £2.2m at the end of Q1 2026. | ||

Alien Metals (LON:UFO) (£15.7m | SR17) | Phase 1 drilling at the Munni Munni platinum-palladium project in Western Australia returns of the highest grades seen at the site - new infill holes hitting up to 8.8g/t PGE. Alien Metals holds a 30% free-carried interest in the project alongside a 17.1% stake in operator GreenTech Metals. | ||

Mycelx Technologies (LON:MYX) (£11m | SR28) | Revenue more than doubled to $11.7m (2024: $4.9m), gross margin expanded to 48% from 27%, and the business swung to a pre-tax profit of $0.3m from a $2.6m loss. |

Roland's Section

JD Sports Fashion (LON:JD.)

Up 6% at 72p (£3.5bn) - Full Year Results 25/26 - Roland - BLACK? (AMBER/GREEN =)

This sportswear retailer has suffered a remarkable fall from grace, in some ways mirroring the problems at its key supplier Nike (NYQ:NKE):

I am not suggesting JD’s troubles are only due to Nike’s woes – but I suspect they've definitely been a factor, together with a broader slowdown in the athleisure boom.

Other issues have emerged too in recent years. CEO Regis Schulz inherited a company that had been built around founder Peter Cowgill and may have lacked the governance and management structures of a modern FTSE 100 business. There have also been more challenges resulting from some big acquisitions in the US.

The end result has been a string of profit warnings over the last 18 months:

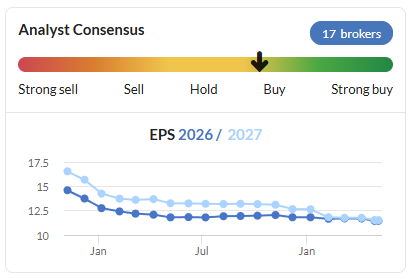

When we last looked at JD in November, Mark maintained our AMBER/GREEN rating despite the company issuing a profit warning on the day. His argument was that the shares were “very cheap” for a business of this quality, despite the downgrade to earnings.

JD’s share price has actually slipped lower since then and it’s possible that today’s guidance may also prompt a modest downgrade for FY27. Even so, I am inclined to agree with Mark’s view, especially as today’s results flag up strong cash generation and an increase in shareholder returns.

Today’s share price rise suggests the market is also optimistic. Let’s take a look.

FY26 results highlights

Today’s figures cover the year to 31 March 2026. The main headline numbers are not that encouraging but are in line with revised expectations following November’s downgrade:

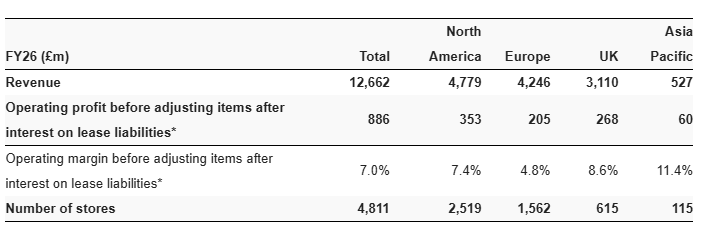

Revenue up 11.7% to £12,662m (constant FX)

Adjusted pre-tax profit down 6.4% to £852m (constant FX)

Adjusted earnings per share down 5.5% to 11.71p (Stockopedia consensus 11.5p)

Free cash flow up 36% to £462m

Dividend up 20% to 1.2p per share

Trading Summary: North America is the group’s largest region, generating nearly 40% of sales. Performance “improved sequentially” through last year, with a return to like-for-like sales growth in the fourth quarter.

CEO Schultz says this was driven by “ranging, supply chain and omni-channel proposition”, suggesting investments in the nuts-and-bolts of retail are starting to deliver results in this region.

In Europe and the UK, there were improvements to the group’s supply chain and e-commerce platform, with a full rollout planned for later in 2026. However, the UK was the only region not to see any organic sales growth last year, with sales down by 3% to £3,110m (in part due to store closures).

Optimising the performance of the group’s store portfolio remains a key priority for the current year:

Driving store productivity & optimisation: accelerate Finish Line and City Gear conversions in the US; 'fewer, bigger, better' formats in the UK; significant steps underway to address under-performing stores in Central & Eastern Europe and North America

JD remains more heavily dependent on store sales than some omnichannel retailers – stores generated 78% of revenue last year, with online at 21%. The remaining 1% of revenue came from JD Gym memberships in the UK, a new area of growth.

This geographic report provides a nice summary of JD’s presence in different regions and the different profitability of each market:

Source: JD Sports Fashion FY26 results

Many of the group’s US stores were acquired through acquisitions and are presumably much smaller than in the UK, given the disparity in FY26 revenue per store:

North America: £1.9m

Europe: £2.7m

UK: £5.1m

Asia Pacific: £4.6m

Based on the size and profitability of the UK, I think it’s fair to suggest the North American business could still have significant growth potential if it can gain further share. The competitive landscape is presumably much tougher though – JD is a top sportswear retailer in the UK, but clearly doesn’t occupy that position throughout North America.

Dividend & Share Buybacks: today’s results contain an updated shareholder return policy that may explain this morning’s share price bump:

In line with our confidence in our cash generation and our medium-term trajectory, we are announcing today a 20% increase in the ordinary dividend with a clear intention to grow this progressively towards a more attractive dividend yield, and a rolling £200m annual share buyback as we deploy cash to drive improved returns for shareholders.

A 1.2p dividend still only gives a 1.7% yield, but it’s a step in the right direction and looks easily affordable to me, thanks to the group’s strong cash flow.

Free cash flow: cash generation is a key aspect of this group, which benefits from a relatively strong balance sheet when lease liabilities are excluded.

Today’s results report free cash flow of £462m for FY26. My own calculations match this almost exactly, giving me confidence in the company’s accounting metrics.

Based on today’s market cap of £3.4bn, this gives JD a FY26 free cash flow yield of c.13% – if it’s sustainable, then I’d argue that’s very cheap.

The company’s forward guidance certainly suggests cash generation is expected to remain strong:

FY27 guidance is for free cash flow of £460m to £520m;

New 3-year cumulative guidance is for free cash flow of >£1.4bn from FY26 to FY28.

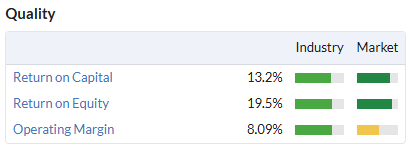

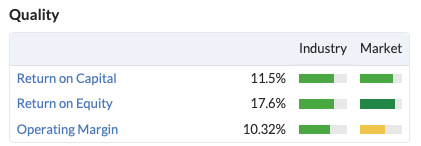

Profitability: in the past, JD has generated respectable double-digit returns on capital employed, driven by high single-digit operating margins.

I estimate an operating margin of 6.2% and ROCE of 10.3% from today's results, slightly below this level. However, this is partly due to some larger adjusting items last year (the Stocko calculations use reported figures, as do my own numbers). I think it’s probably fair to say the underlying profitability in the business was fairly stable last year.

Outlook & FY27 Guidance

Management expects “muted market growth in the near term”, which is said to be in line with previous guidance.

I don’t have access to updated broker forecasts for JD Sports today, but my impression when I looked at the results this morning is that today’s FY27 guidance probably represents a small cut to previous expectations:

FY27 guidance: reflecting the uncertainty, we are providing a wider range of profit guidance than we were previously planning for internally. Based on what we know today, we anticipate FY27 PBTAI of £750m to £850m, and free cash flow of £460m to £520m

Consensus earnings estimates on Stockopedia prior to today were for adjusted EPS to be flat at 11.5p in FY27.

However, since FY26 adjusted pre-tax profit was £852m, then achieving a flat result at a pre-tax level in FY27 would require a performance at the very top end of today’s guidance.

Assuming a similar translation into EPS as in FY26, then my feeling is that we may see earnings forecasts edge lower in the coming days.

I’m going to stick my neck out and remain BLACK on JD today, albeit with a question mark added to indicate the lack of a definitive downgrade.

Roland’s view

JD Sports has obviously been through a difficult patch, but my impression is that the company is doing all the right things by laying the foundations for sustainable medium-term growth.

Underlying profitability remains respectable in my view and I’m impressed by the company’s strong cash generation.

I don’t have any insight into the likely path of consumer demand for JD’s products and I don’t fully understand the level of dependency on Nike brand sales.

However, at a fundamental level I think this looks like a good quality, cheap retail with sufficient scale to maximise its opportunities.

With the shares trading on a forward P/E of 6 and offering a 10%+ free cash flow yield, I’m going to leave Mark’s AMBER/GREEN view unchanged today.

Helios Towers (LON:HTWS)

Up 16% at 236p (£2.5bn) - Q1 2026 Results - Roland - AMBER

This mobile phone tower business is not a company we’ve covered before, but today’s upgraded 2026 guidance has triggered a 16% share price gain. That caught my eye, as recent share price performance seems remarkable for what’s essentially an infrastructure company.

Here are the main headlines from today’s update:

Helios owns a portfolio of nearly 15,000 mobile towers across Africa and the Middle East. The company’s business model is to rent out space on these towers to mobile network operators (tenants).

Hosting multiple tenants on one tower can provide a significant improvement in profitability. This is what has driven today’s upgrade:

Our tenancy pipeline this year is significant and we are upgrading our financial and operational FY 2026 guidance. We now target a record 3,000 to 3,500 tenancy additions for FY 2026, increasing by 1,000 compared to prior guidance, and all meeting our disciplined return thresholds.

CEO Tom Greenwood emphasises the strong macro trends underpinning demand for Helios towers. This is a contrast to the UK and Western Europe were mobile networks are more mature:

Demand for data and connectivity across Africa and the Middle East remains exceptionally strong, with our mobile operator customers accelerating investment, driving significantly increased demand for our infrastructure.

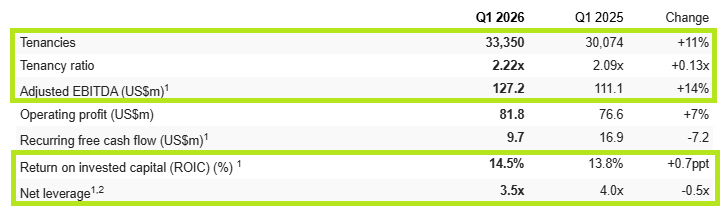

Today’s financial summary table highlights the key metrics the company uses to measure progress. Almost all of them improved in Q1 relative to the same period last year:

Source: Helios Towers Q1 2026 results

The reduction in recurring free cash flow is said to reflect the timing of customer payments and working capital movements. I don’t see it as an issue over such a short period, especially as cash flow guidance has been upgraded today.

2026 Outlook & Guidance

The Group has a strong site and tenancy pipeline from investment grade and blue-chip customers, underpinning an upgrade to FY 2026 guidance

There's a big increase to the expected rate of tenancy additions this year, with smaller revisions to financial metrics:

Tenancy additions: 3,000 to 3,500 (previously 2,000 to 2,500)

Adjusted EBITDA: $515m to $530m (previously $510m to $525m)

Recurring free cash flow: $215m to $230m (previously $210m to $225m)

Capital allocation guidance was also updated, with more spending planned to support the increase in tenancies:

Discretionary capex: $180m to $210m (previously $110m to $140m)

Share buyback: $51m (unchanged)

Dividend: $25m (unchanged)

At first I was puzzled by the small increase to EBITDA and FCF guidance, relative to the large increase in tenancies.

However, Helios’s capex guidance explains the contrast – clearly there is a significant cost in adding new tenancies. Once set up, I assume they become more profitable and cash generative.

Roland’s view

Today’s 15% share price rise appears to be at odds with the 1% increase in adjusted EBITDA guidance for the current year.

That’s especially true as Helios shares were not exactly cheap to start with:

My reading of this situation is that the market is pricing in the improved profitability that I’ve speculated on above – once the larger number of tenants has been established, future years should see a significant improvement in profits and cash flow.

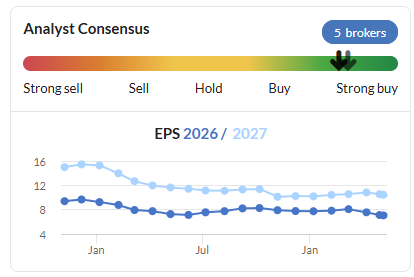

Broker forecasts suggest strong earnings growth was already pencilled in for 2027, even before today’s upgrade:

However, the consensus trend has drifted lower over the last year, so today’s upgrade represents a welcome change of direction:

Another big positive is the reduction in leverage flagged in today’s update. While 3.5x EBITDA is still quite high for a listed equity, it’s not so unusual for private infrastructure groups.

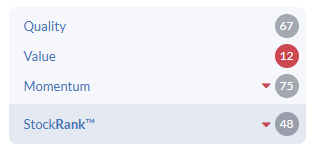

I can’t help feeling that the best buying opportunities may have passed here, a view that’s perhaps supported by the low StockRank and High Flyer styling:

Personally, I’m also discouraged by the low dividend yield. I see infrastructure as a buy-and-hold asset class and would rather Helios scrapped its buyback programme and used the cash to enhance its meagre dividend. Combining this year’s $51m buyback with the $25m dividend would provide a more meaningful c.2.5% yield, rather than the sub-1% yield on offer at the moment.

This is the first time we’ve looked at Helios and while I’m impressed by operational progress, I can’t help feeling much of the good news is already in the price.

To reflect this mix, I’m going to adopt a neutral view today.

James's Section

BAE Systems (LON:BA.)

-3% at 2,023p - Trading Statement - James - AMBER/GREEN =

I was checking back through our coverage of BAE Systems, and I was delighted to see Roland had it at AMBER/GREEN for our last coverage - I didn’t know that was an option. It’s a useful distinction for this high-quality, but increasingly expensive stock - the market has established a premium, but whether this premium can be justified and whether another re-rating is possible, remains the central question for any potential investor.

As we can see from the market’s reaction this morning, investors were looking for more than just a reiteration of guidance. And that makes a lot of sense when we dive deeper into the valuation.

There wasn’t much that was new in today’s trading statement. Management pointed to a strong operational performance and increased defence spending across all key markets - we could have anticipated this given the broader macroeconomic and geopolitical environment.

Around the world, security threats continue to grow, leading governments to increase defence spending. Across our markets, sustained investment and deliberate positioning have resulted in a proven portfolio of capabilities that aligns with customer priorities and evolving future challenges.

The business suggested its market positioning coupled with a supportive backdrop would support growth over the medium term. Once again, nothing new there, but also I like to hear things like confidence in the medium-term growth forecasts.

Guidance/forecast versus the valuation

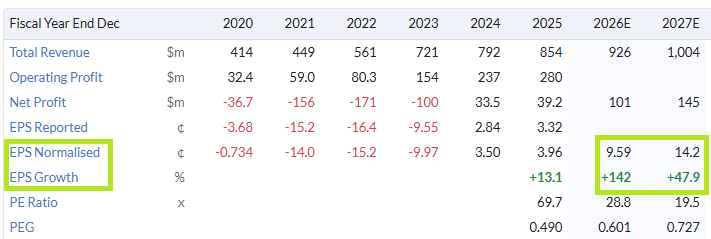

This is an ever-present consideration with quality stocks. BAE has compounded revenue at 8% annually from £19.3bn in 2020 to £28.3bn in 2025. Strip out the Ball Aerospace acquisition, which inflated 2024 growth to 14%, and the organic run rate has been remarkably consistent around that 8-9% mark throughout. For FY2026, guidance is 7-9% on a constant currency basis - essentially identical. For FY2027, analysts are forecasting 8.4%.

The business has guided towards 9-11% underlying EPS growth for FY2026. Also very positive, but not groundbreaking.

So, growth is not slowing from its underlying pace, but the pace of growth is unlikely to increase substantially from here - this is a business that benefits from long-term defence partnerships and not one-off orders for on-shelf inventory.

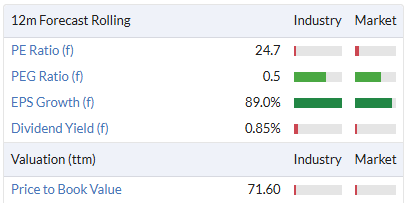

This is where investors need to ask themselves whether this very consistent business - which also has a backlog worth £83.6bn, equivalent to 2.7 years of annual sales - is worthy of trading around 24x forward earnings.

Being generous, the underlying medium/long-term earnings growth rate is around 10%, in turn, leading to a PEG ratio of 2.4. That doesn’t scream value. What’s more, the net debt position of £5.3bn and the dividend yield of 1.88% (covered 2.1x by net income) doesn’t vastly alter that equation in a positive way.

Quality is undeniable

BAE is undeniably a quality business. The aforementioned backlog of orders, long-term defence contracts, huge economic moats protected by sky-high barriers to entry, coupled with the below profitability metrics make for a very compelling prospect. What’s more, AI isn’t going to undermine the business, especially on the hardware side.

James’ View

I like to hunt around for stocks with PEG ratios under 1 – that’s an old benchmark for unappreciated value. But it’s absolutely necessary to recognise that valuations are relative, and that relativity is typically set by the sector.

Defence primes are not cheap. As a snapshot, I’ve got Lockheed at 17x, RTX (Raytheon) at 25x, Northrop at 20x. The forward PEG ratios sit at 0.9, 2.5 and 2.1 respectively. And the aerospace sector isn’t cheap either. Rolls-Royce sits at 32.5x forward earnings and GE at 38.5x.

In this broader context, BAE isn’t bad value. To establish a better idea of relative valuation a deeper dive is needed, but my interpretation of the above is that a re-rating is unlikely in the near term.

N.B. I also believe, if you look deeper, you can find better value defence and defence-related companies that may have been missed. In November/December, I picked up Innovative Solutions and Support (NSQ:ISSC) for around $9 - it’s now at $22.

Morgan Advanced Materials (LON:MGAM)

Up 1.3% at 230p - Trading Update, CFO Intention to Retire - James - AMBER/GREEN

Six months ago, Graham had Morgan Advanced Materials firmly in the RED following a run of profit warnings and margin deterioration. I believe a lot has changed since then, and following a run-up since mid-March (when I thought it was clearly overlooked), I’m going to utilise this AMBER/GREEN rating again.

Today’s trading update isn’t dramatic - management confirmed Q1 organic constant currency revenue growth of 6.2%, noted that the weak prior year comparator had a role in that number, and reiterated full-year guidance. In the context of where the business has been, this is exactly what the market needed to hear.

The business also reported no material impact from the conflict in the Middle East - I think also companies feel compelled to comment on this now - and that they were responding to inflationary pressure through pricing.

Our Q1 trading was in line with our expectations and today we reconfirm our full year guidance for 2026. We are making good progress against our strategic priorities, including the strategic review of Thermal Products, and continue to focus on executing at pace against the strategy set out at our December 2025 Capital Markets Day.

A business in transformation

The real story here is not Q1 revenue growth, welcome as it is. It is what the business is becoming. FY2025 results were ugly on the surface - revenue of £1,030m, adjusted operating profit down sharply to £99.1m, margins contracting from 11.7% to 9.6% - but beneath that, a strategic transformation is taking shape.

The disposal of Molten Metal Systems is done. A business simplification programme is on track to deliver £27m of cumulative savings by the end of 2026. And most significantly, management has initiated a formal strategic review of the Thermal Products division, which accounts for around a third of group revenue but delivered a margin of just 6.7% in 2025, down from 9.9% the year before.

The last point - the strategic review of the Thermal Products division - is where the investment case gets interesting. Strip the division out of the company, and what remains are the Performance Carbon and Technical Ceramics businesses. These two divisions have more obvious structural tailwinds in aerospace and defence, and have a blended margin above the group’s 2028 margin target of 12%.

CEO Damien Caby’s roadmap points to 10-12% margins by 2028 and 12-14% beyond that. Stripping out the Thermal Products division would be a shortcut to achieving that, while using the proceeds to reduce net debt, which stands at £234m, or 1.8x EBITDA.

CFO to retire

The update also confirmed that CFO Richard Armitage intends to retire in the first half of 2027, with a successor search now underway. The long lead time should allow for an orderly handover, though a CFO departure during an ongoing strategic transformation is always worth monitoring.

He has helped position the organisation for margin enhancing growth and led several transformation programmes. His contribution has been essential to designing our new strategy: 'Unlocking our Potential', and in leading its implementation.

James’ View

This is a business that has frustrated investors for years, and it would be wrong to pretend that the transformation is complete or that execution risk has disappeared. The Thermal Products review could go any number of ways, and the dividend cover leaves limited room for further earnings disappointment.

But the risk/reward equation is shaped by the valuation - and it’s not expensive.

The stock trades around 12.3x forward earnings. That doesn’t strike me as particularly expensive, but it’s a business that has been treading water for a decade now. However, analysts' forecasts point towards double-digit earnings growth over FY2026 and FY2027, resulting in a PEG ratio of 0.7. Factor in net debt and a 5.2% dividend yield (admittedly rather poorly covered by earnings - 1.5x) the equation looks quite compelling.

I think there’s scope for a re-rating if the business delivers a material improvement in margins. It’s worth watching in my view.

See what our investor community has to say

Enjoying the free article? Unlock access to all subscriber comments and dive deeper into discussions from our experienced community of private investors. Don't miss out on valuable insights. Start your free trial today!

Start your free trialWe require a payment card to verify your account, but you can cancel anytime with a single click and won’t be charged.