Good morning!

In the Middle East, President Trump has reportedly rejected a new peace proposal from Iran, describing it as “totally unacceptable”. Iranian media reported that Tehran also rejected Trump’s latest proposal.

Brent Crude oil rose by around 4% to $104 a barrel on the news, reversing some of last week’s decline.

At home, the fallout from Labour’s poor showing at last week’s local elections rumbled on over the weekend. The Prime Minister is now set to promise “urgent change” according to the FT, but the Guardian reports that various potential rivals are preparing for a leadership bid.

Finally, reports suggest airlines are cutting ticket prices for this summer to try and persuade holidaymakers to book trips despite concerns that jet fuel shortages could disrupt travel. We’ve seen evidence of this in the DSMR recently, with Jet2 warning on profits and reporting limited visibility on summer bookings.

Stock markets appear set for a fairly low-key start to the week

FTSE 100 to open up by 0.2% at 10,248

S&P 500 to open down 0.1% at 7,390

German DAX is expected to open down by 0.1% at 24,282

Brent Crude is up 3.7% at $103.70 a barrel

Gold is down 0.9% at $4,672/oz

I’m delighted to share that I am joined by Ed Sheldon CFA again for today’s report.

Today's report is now complete.

Spreadsheet accompanying this report: link.

Companies Reporting

| Name (Mkt Cap) | RNS | Summary | Our view (Author) |

|---|---|---|---|

| GSK (LON:GSK) (£75bn | SR92) | Collaboration with CTTQ for bepirovirsen | GSK enters exclusive collaboration with SBP Group, a market leader in hepatology in China, to accelerate bepirovirsen at launch. Agreement provides access to over 5,000 medical centres in China at launch. | |

Compass (LON:CPG) (£37bn | SR59) | Revenue up 11%, with operating profit up 9% to $1.6bn and adj EPS up 16% to 72.8c. Raising full-year guidance: now expect adj op profit growth of >11% (prev. 10%). | AMBER ↑ (Roland) This outsourced catering giant isn’t cheap, but I think it has some of the qualities of a long-term quality compounder, backed by a long track record of successful growth and sector consolidation. Even on a forward P/E of 19, I’m quite happy taking a neutral view. | |

Wise (LON:WISE) (£13.1bn | SR49) | Trading of Wise shares on Nasdaq will begin today. London-listed Wise plc shares will be replaced by new Wise Group plc shares from today. | ||

Renewables Infrastructure (LON:TRIG) (£1.6bn | SR81) | Reiterated dividend target of 7.55p for 2026, targeting £400m from disposals over the next 12 months. Prioritising buybacks, debt reduction and internal investments. Not currently pursuing any new third-party investments. | ||

Grainger (LON:GRI) (£1.2bn | SR66) | Has extended £540m of its core banking facilities to 2033 at lower margins, resulting in an annual saving of c.£1m in finance costs. The extension improves Grainger’s weighted average facility duration to 4.6 years. | ||

Renew Holdings (LON:RNWH) (£727m | SR89) | Acquired cable jointing services specialist PWR-X for £1.1m to enhance its offering in the high voltage power market. | ||

Victrex (LON:VCT) (£513m | SR71) | Revenue up 1%, volumes up 6%. Underlying pre-tax profit down 18% to £19m due to softer sales mix and competitive pricing, with adj EPS down 24% to 17.2p. Outlook: expect H2 weighting to profit, with FY26 adj pre-tax profit of £42-44m (previously £46.6m). | BLACK (AMBER/RED ↓) (Roland) Today we have another profit warning as Victrex highlights the adverse trends we’ve flagged previously; the company is selling more low-margin commodity PEEK and less high-margin value-added product. Competitive pressure and alternative choices for Medical customers appear to be the underlying causes of this malaise. However, newish CEO Dr James Routh believes the company’s core advantages remain and that poor commercial execution has been to blame. He is also cutting 10% of headcount and launching a portfolio simplification exercise to try and address the slump in profitability. I don’t know enough about the end market to judge whether this will work, but I do think a dividend cut is likely (and overdue) to prevent Victrex continually borrowing money to fund shareholder payouts. | |

Caledonia Mining (LON:CMCL) (£339m | SR85) | Revenue up 18.3% with pre-tax profit up 69.4% to $18.9m. Gold production down by 30.9% to 14,767oz due to “constrained access to higher-grade areas”. As a result, AISC rose by 53.9% to $2,765/oz. Full-year production guidance of 72,000 to 76,500oz unchanged. | AMBER/GREEN = (Ed S) Today’s Q1 results show a strong rise in revenue, profits, and free cash flow. However, there were some operational issues during the quarter, with gold production falling. The company points to the ‘transformational investment opportunity’ associated with the Bilboes project. | |

| Serabi Gold (LON:SRB) (£261m | SR99) | Correction - Audited Results for the year ended 31 December 2025 | The Total AISC of production (per ounce) for the 3 months to 31 December 2025 in the table on page 2 has been corrected to US$1,818/oz. It was previously incorrectly stated as $2,158/oz in Serabi’s results on 1 May 26. | |

Asos (LON:ASC) (£261m | SR45) | Has sold Lichfield fulfilment centre to Marks & Spencer. The sale will generate net proceeds of “at least £66m” and cost savings of c.£6m. | RED = (Roland) Today’s disposal is good news, but Asos remains loss-making and indebted, with falling sales. Delivery of the group’s FY26 forecasts might prompt me to take a more positive view, but for now I think it’s prudent to remain (very) cautious on the equity here. | |

Galantas Gold (LON:GAL) (£173m | SR26) | Intends to raise up to $85m pursuant to a brokered private placement of up to 154,546,000 units of Galantas at a price of $0.55 per unit, where one unit includes one share plus a warrant equivalent to half a Galantas share. | ||

Aurrigo International (LON:AURR) (£60m | SR27) | Aurrigo receives £4.5m multi-year advanced engineering framework agreement for Automotive Division | Announces a three-year £4.5m framework agreement to supply new, innovative high performance electrical system sets for a next generation supercar programme. | |

80 Mile (LON:80M) (£47m | SR43) | Has received all exploration permits required to undertake the 2026 drilling programme at Disko and Nuussuaq. Represents a ‘significant milestone’ for the project. | ||

Poolbeg Pharma (LON:POLB) (£30m | SR24) | Has received formal notification of the grant for its POLB 001 cancer immunotherapy-induced Cytokine Release Syndrome (CRS) patent application from the Canadian patent office. | ||

Coppa Collective (LON:COPC) (£24m | SR78) | Coppa Club like-for-like (LFL) sales growth of 3.2%, ahead of the market. Group LFL sales growth of 1.8%. | ||

Shoe Zone (LON:SHOE) (£21m | SR65) | Revenue down 12% to £62.9m, loss before tax of £5.3m, no interim dividend proposed. Very challenging trading environment. | RED= (Ed S) | |

88 Energy (LON:88E) (£15m | SR20) | 88 Energy's 20% working interest in PEL93 fully secured, with no remaining earn-in funding or reassignment conditions. | ||

Cellbxhealth (LON:CLBX) (£12m | SR6) | Trading in Q1 reflected the company's focus on the necessary organisational restructuring required under the revised business strategy. 2026 annual cash operating costs reduced by more than £6.6m. | ||

Rockfire Resources (LON:ROCK) (£12m | SR12) | Drilling is ongoing with HMO-016 completed and HMO-017 in progress. Several narrow, but strong zones of mineralisation have been encountered in hole HMO-016 based on portable X-Ray Florescence ("pXRF") readings of drill core. |

Roland's Section

Victrex (LON:VCT)

Down 2% at 579p (£505m) - Half-Year Financial Report - Roland - BLACK (AMBER/RED ↓)

Specialist polymer producer Victrex left its full-year guidance unchanged in February, giving me hope that my decision to turn neutral in December might have been validated. Unfortunately that wasn’t to be – today’s half-year results include a profit warning:

Outlook: FY26 underlying pre-tax profit is now expected to be £42-44m (previous consensus £46.6m).

In essence, today’s interim results appear to show that the core problems facing the company are unchanged. Here’s what Graham said back in July last year:

“Destocking” can be written off as a short-term issue, but the availability of “alternative materials” cannot. If the medical industry has found cheaper or superior alternatives to Victrex’s polymers, this is not a problem that is just going to go away!

This situation doesn’t seem to have improved. Here’s what the company says today about its Medical business in H1 2026:

Medical revenues were down 9% impacted by order phasing, a weaker sales mix and some price impact within specific applications and geographies. Spine showed some signs of stabilisation.

Of course, Medical is only one part of the business – but it’s an area that’s expected to deliver higher-margin, valued-added opportunities for growth. That doesn’t seem to be happening.

Instead, Victrex is continuing to sell more lower-margin commoditised products in other markets, depressing profits even as volumes rise.

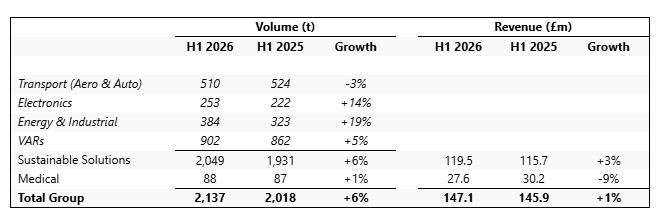

Here’s a summary of the main points from today’s H1 results:

Group sales volume up 6% to 2,137 tonnes

Group revenue up 1% to £147.1m

Gross margin down 2.4% to 41.7%

Underlying pre-tax profit down 18% to £19.0m

Adj earnings per share down 24% to 17.2p

Interim dividend unchanged at 13.42p per share

Net debt: £45.4m (H1 25: £40.7m)

Drilling into the underlying volume and revenue results shows a mixed performance across the business, with the low-margin VAR business continuing to dominate. (VAR = Value Added Resellers; this represents Victrex selling raw PEEK to other manufacturers for them to process):

Source: Victrex H1 2026 results

The Medical business only accounts for a small share of revenue but has very high profitability – today’s results show a gross margin of 75.7% (H1 25: 77.8%), versus 33.8% for the remainder of the business. This means that weakness in Medical sales has a disproportionate impact on group profit.

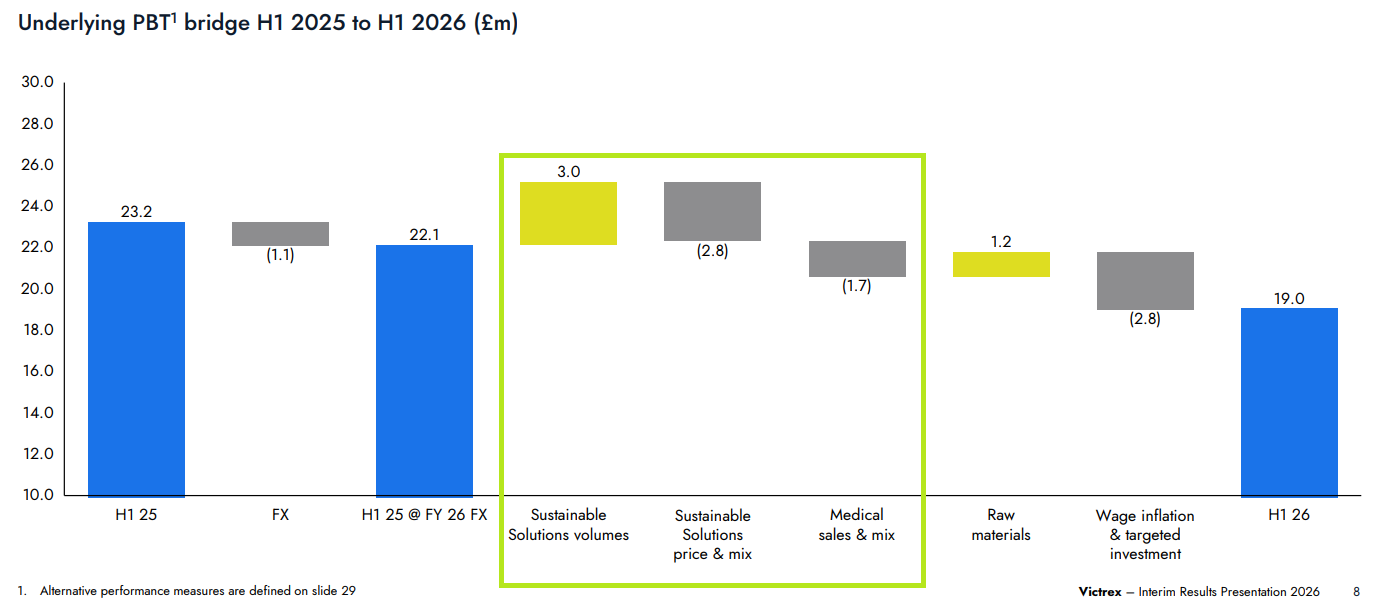

This slide from today’s analyst presentation shows how the adverse mix in Medical reduced underlying pre-tax profit by 7.7% in H1, after stripping out currency effects. In contrast, while the sales mix in Sustainable Solutions was unfavourable, this was fully offset by higher volumes:

Source: Victrex H1 2026 presentation

Taking a broader view, it’s clear that pricing power across the business was insufficient to address higher raw material and wage costs (see right-hand side). Victrex appears to be suffering the commoditisation of a product that historically carried much stronger pricing power.

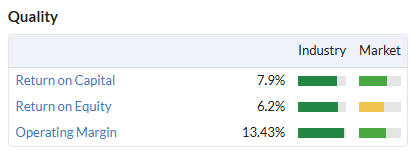

This is reflected in the company’s quality metrics, which had already declined sharply prior to today:

This business used to generate double-digit returns on equity and capital. Now it’s struggling to cover its cost of capital – unsurprisingly, the newish CEO has now launched a more significant restructuring plan.

Turnaround plan: Victrex will cut 10% of its headcount and target £10m of annualised cost savings from next year.

The company is also launching a “portfolio simplification” that will include a review of its mega-programmes. These are long-running industry-specific initiatives aiming to create value-added products for various markets to reduce the company’s exposure to commodity-type VAR sales.

Victrex has also used today’s results to report a £60.6m non-cash impairment charge relating to its jointly-owned Panjin factory in China. This facility has faced previously-reported operational challenges. A taskforce setup to address these issues has reached a disappointing conclusion:

Following a period of continuous running and production being increased during H1 2026, the Group concluded that part of the process technology in one of the final manufacturing stages at the plant is not capable of delivering the full intended nameplate capacity of 1,500 tonnes.

Victrex says it remains committed to the plant in China, which is the group’s fastest-growing market (10-year revenue CAGR of 17%). An appraisal is currently underway to understand the investment needed to increase capacity in China.

The risk for investors is that Victrex has simply lost its competitive advantages as the PEEK market has matured and evolved.

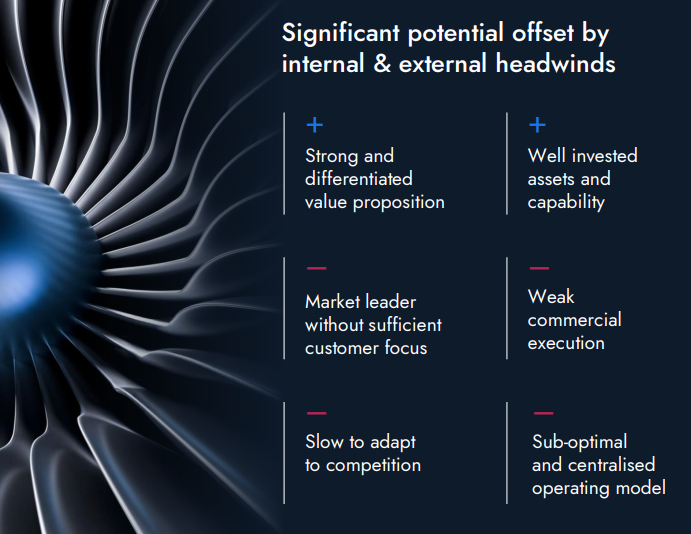

Naturally, the new CEO disagrees. Dr Routh believes that weak commercial execution and a lack of focus are the main issues:

Source: Victrex H1 2026 presentation

Roland’s view

I can’t be sure whether Victrex still enjoys the competitive advantages that drove its historic growth.

In my view, today's turnaround strategy appears to be much the same as the old strategy in product terms – improve differentiation and look for opportunities to create value-added products.

Perhaps the difference this time will be improved focus and strong commercial execution.

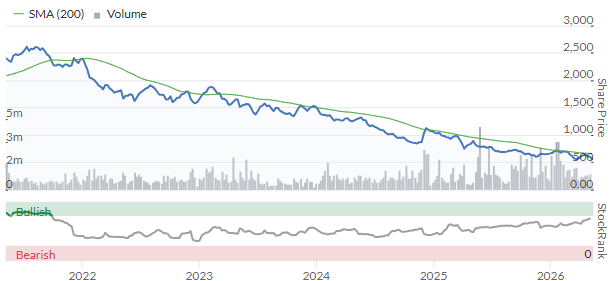

Shareholders will have to hope so. The shares have fallen by a further 15% so far this year and Victrex stock has now lost 75% of its value in five years:

Is this the bottom? Today’s cut to guidance equates to a 7.7% reduction at the mid-point and Victrex shares have fallen by less than this – the stock is down just 2% as I write.

This market reaction might support the view that the company’s fortunes are now bottoming out and that performance will now start to recover. Today’s results do have the feel of a kitchen sink update – a new boss using the opportunity to get all the bad news out in front so that he can establish a low baseline for a recovery.

However, I think it would be naive to ignore the risk of further profit warnings this year.

These results show Victrex delivered half its expected full-year volume in H1, but perhaps only 40% to 45% of full-year profit (adjusting for today’s downgrade).

My reading of this is that the company will need to deliver improved volumes or higher margins in H2 in order to meet even today’s reduced guidance.

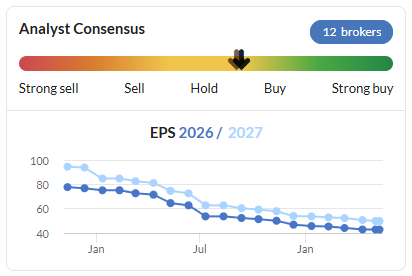

The track record of earnings forecasts is not encouraging:

I would also be wary about relying too heavily on Victrex’s 10% forecast dividend yield. The current payout isn’tcovered by earnings and today’s results confirm Victrex used its borrowing facility to fund last year’s final dividend.

The company’s current policy is to maintain the dividend as long as leverage remains below 1.0x EBITDA, but this makes no sense to me. I’d prefer to see the payout reset to a sustainable level and I suspect this could happen later this year unless there are signs of improved trading.

My optimism in turning neutral in December was obviously premature. I’m going to revert to our previous AMBER/RED view today.

Asos (LON:ASC)

Up 12% at 243p (£291m) - Disposal of Lichfield fulfilment centre - Roland - RED =

This former fast fashion giant has slumped to new lows in recent months, but the shares are up by around 14% this morning:

Today’s rise has been triggered by news that the company expects net proceeds of c.£66m from the sale of its Lichfield distribution centre to Marks and Spencer. This facility is deemed surplus to requirements and had already been mothballed.

While this disposal won’t have any direct impact on Asos’s sales performance, it may help to repair the group’s debt-laden balance sheet and perhaps lower its cost base.

Let’s see what the company has to say about this deal:

Net proceeds of at least £66m;

Annual cash savings of c.£6m relating to rent and other occupancy costs;

Will result in a one-off pre-tax profit of c.£85m, which will be recognised as an adjusting item in the results;

The net proceeds will add to the Group's cash position of £209.5m as at 1 March 2026, resulting in a pro forma net debt (excluding lease liabilities) position of c.£228m (1 Mar 26: £294.9m).

Asos also has a surplus warehouse property in Atlanta, USA. Perhaps this can also be sold?

Balance sheet: when Graham covered Asos’s interim results in April, he noted leverage of 1.8x and concluded he’d rather be a bondholder than a shareholder.

Today’s picture improves this view, at least slightly.

Based on the latest FY26E forecasts (24 April 26) from house broker Singer Capital, I estimate this disposal could reduce Asos’s leverage multiple to 1.6x EBITDA on a pro forma basis.

The absolute reduction in net debt should also help to reduce finance costs, perhaps aiding a return to positive free cash flow.

Roland’s view

There’s no update on trading today, so I assume that expectations remain unchanged from April. On this basis, Asos is expected to remain loss-making at least through to August 2028:

Graham was RED on Asos in April, citing the group’s declining sales, loss-making trading and weak balance sheet. While supporting the company’s ambition to become a multi-brand, "inspirational destination”, he was concerned about how long the business could continue going while remaining unprofitable.

The sale of the Lichfield warehouse should increase Asos’s financial runway. If a buyer can be found for the Atlanta property, that could also help.

However, retailers can’t shrink their way to greatness. Revenue fell by 14% in H1 and is not expected to return to growth until next year. This remains a loss-making and heavily-indebted business facing tough competition from China’s Shein and others.

Brokers are forecasting a return to adjusted operating profitability for FY26, excluding interest costs. If Asos delivers on this then I think it might be time to turn more positive. For now, I’m going to leave our negative view unchanged.

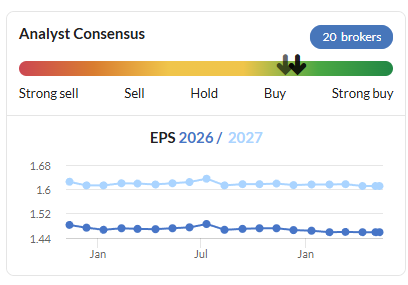

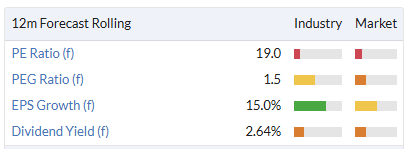

Compass (LON:CPG)

Up 2.5% at $30.23 (£37bn) - Half Year Results - Roland - AMBER ↑

This FTSE 100 catering group recently made the puzzling decision (in our view) to change the trading currency of its shares from sterling to US dollars.

As far as I can see, the choice has been made to align the group’s trading currency with its reporting currency of USD and the region where it generates most of its profit.

Today’s half-year results tell us that 67% of H1 revenue and 83% of H1 profit came from North America. Pricing the stock in USD is likely to aid US investors’ understanding of its valuation. Perhaps a US listing will follow in due course?

H1 results summary

Half-year trading was certainly robust, allowing Compass to upgrade its full-year guidance today.

Here’s a brief summary of the key points:

Revenue up 11% to $25.0bn

Operating profit up 9% to $1,605m

Adjusted earnings per share up 12% to 72.8c

Free cash flow up 11% to $825m

Interim dividend up 13% to 25.5c

Compass reports organic growth of 7.2%, with new business wins up 14% to $4.1bn. Compass is something of a roll-up specialist and reports good progress with recent acquisitions.

On an adjusted basis, the group’s operating margin also improved by 0.2% to 7.4%.

The company also notes that it now operates Group Purchasing Organisations in five of its top 10 markets, following the recent acquisition of Pro Care Management in Germany for $270m. Pro Care is a procurement and software provider for large-scale kitchens and one of the largest independent food GPOs in Germany.

I would expect that managing the supply chain for its catering locations helps Compass to retain more of the margin in its operations. It should also provide some economies of scale and efficiency gains from greater vertical integration in areas such as logistics.

Outlook

Management continues to see “highly attractive structural growth opportunities” and reminds investors that the group’s addressable market has been growing at 5% per annum.

More specifically, FY26 profit guidance is upgraded:

For 2026, we now expect underlying operating profit growth above 11%, underpinned by organic revenue growth of around 7%, around 2% growth from M&A and ongoing margin progression.

Previous guidance was for underlying operating profit growth of 10%.

This isn’t a huge upgrade, but it’s a step in the right direction after a long period of flat forecasts:

The shares haven’t moved much today, perhaps unsurprisingly given the existing forward valuation:

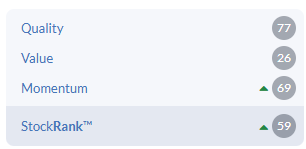

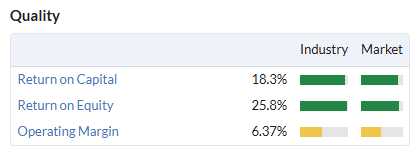

Roland’s view

Compass shares routinely looks quite pricey and are currently styled as a High Flyer - expensive but good, with positive momentum:

Quality metrics are indeed strong…

… and this business has a track record as a long-term compounder:

Rising food inflation and a possible global economic slowdown might cause some temporary softness in demand, but many of Compass’s clients are large public and private institutions where long-term demand is likely to remain resilient.

Compass operates in a highly attractive market, with sectors that are expected to benefit from continued structural growth. Our total addressable market has historically grown at around 5% per annum and could reach c.$600bn by 2035. Clients face increasing complexity, such as regulation, allergens and data-led insights, and these factors are driving demand for outsourcing across all sectors.

We last covered Compass’s trading in early 2025, when the market cap was £47bn. It’s since fallen to £37bn despite continued growth in profits and revenue.

I’d want to do more work before considering a positive view here, but I'm very comfortable taking a neutral view, so I’m upgrading our view by one notch today to AMBER.

Ed S's Section

Shoe Zone (LON:SHOE)

Down 11% at 40p (market cap of £18.5m) – Interim Results – Ed S – RED=

Shoe Zone has posted its interim results for the 26 weeks to 28 March 2026.

And they make for grim reading…

Financial highlights:

Revenue of £62.9m (2025 H1: £71.5m), down 12.0%

Store revenue £45.8m (2025 H1: £53.3m), down 14.1%

Digital revenue £17.1m (2025 H1: £18.2m), down 6.0%

Loss before tax of £5.3m (2025 H1: Loss £2.3m)

Adjusted loss before tax of £5.3m (2025 H1: Loss £2.6m)

Earnings per share of -11.5p (2025 H1: -4.9p)

No interim dividend proposed (2025 H1: Nil)

Net cash at the end of the period was £7.5m (2025 H1: £1.7m)

At 28 March, the company had:

259 stores (2025 FY: 269)

An average lease length of 2.3 years (2025 FY: 2.5 years)

Outlook:

As announced on 22 April 2026, the Company now expects an adjusted loss before tax for the full year of between £1.0m and £2.0m.

Management commentary:

Shoe Zone experienced a very challenging trading environment in the period against the continuing backdrop of weak consumer confidence and macro/global economic volatility.

Note that the company provides a strategy update:

Our refit and relocation programme continues, albeit at a slower pace, and we now have 206 stores converted to our new, larger format. We expect to spend approximately £3.0m on capital projects this year, which is a similar level to the previous year, and we will continue to invest until all stores have been converted. Our long-term objective is to be trading out of approximately 260 stores in total, and the Board currently expects, subject to market conditions, to complete our relocation and refit programme by the end of 2027.

Ed S’s view:

Graham recently downgraded Shoe Zone to a RED rating and I don’t see anything in today’s interim report that makes me want to adjust this rating. This is a company that is really struggling right now.

As a reminder, back in January, the company was guiding to profit before tax of approximately £1.0m for the year ending 3 October 2026. However, on 22 April, it lowered its guidance to an expected adjusted loss before tax of between £1.0m and £2.0m for the year.

The company reiterates that guidance today. It says:

Trade continues to be negatively impacted by a further weakening in consumer confidence, following the Government's last two budget announcements, as well as the geo-political issues in the Middle East. These macroeconomic factors have increased customer caution, leading to lower footfall and less discretionary spend. The Middle East issues have also resulted in a higher cost of containers and general transportation costs.

Over the last 12 months we have seen more stability in the price of containers, and a strengthening of sterling against the dollar, but these conditions have recently reversed as fuel prices have increased and sterling has weakened, both of which are expected to negatively impact the second half of the year.

It’s worth noting that there are some positives in today’s results.

For example, net cash at the end of the period was £7.5m.

Meanwhile, the company has made moves to reduce costs and provide more operating flexibility:

It completed 19 lease renewals/re-gears in the period with an annualised saving of £44k, with an average reduction of 4.1%.

It reduced its average lease length to 2.3 years (2025 FY: 2.5 years), which gives it the opportunity and flexibility to respond to changes in any retail location at short notice (it notes that property supply continues to outstrip demand, and that it continues to take advantage of this and further improve its property portfolio).

It is in the process of reducing the size of its distribution centre. The whole site is made up of six leases, and it will exit three of these.

However, from an investment perspective, there are a lot of negatives here:

For a start, we have a retailer serving a demographic that is really struggling right now (the lower section of the ‘K-shaped economy’). And revenues are falling (note that the digital returns rate increased to 11.9% in H1 from 11.4% a year earlier).

Next, we have a lack of profitability (and a number of profit warnings recently). Broker forecasts point to further losses next financial year.

I’ll point out here that high oil prices are a problem for Shoe Zone because cheap shoes rely on synthetic, petroleum-based materials (approximately 70% of the materials used in a typical synthetic shoe have some level of exposure to oil price fluctuations). Transportation is also a major cost.

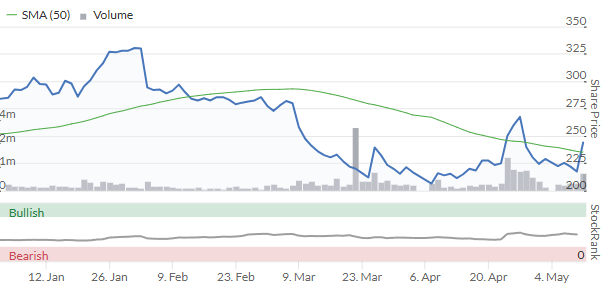

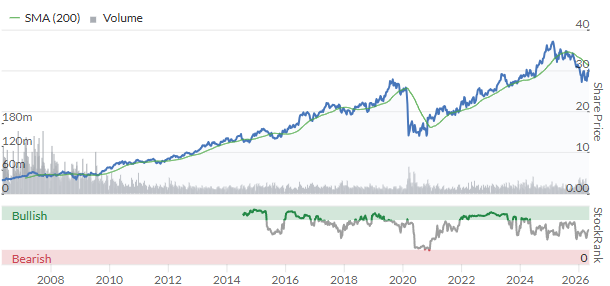

As for the chart, it doesn’t look good (the Stockopedia momentum rank is 3). It’s literally a ski slope:

Given all these negatives, I’m leaving Shoe Zone at RED.

Caledonia Mining (LON:CMCL)

Up 2% at 1,800p (market cap of £339m – 1st Quarter Results – Ed S – AMBER/GREEN=

Gold mining company Caledonia Mining – which operates in Zimbabwe – has posted its Q1 results today. And the headline numbers are strong, as you would expect them to be given the significant rise in the price of gold over the last year (gold is at $4,670 per ounce today versus around $3,250 an ounce a year ago). That said, there were some production issues during the quarter.

Q1 financial highlights:

Revenue increased by 18.3% to $66.43 million, driven primarily by a significantly higher average realised gold price

Gross profit increased by 19.2% to $32.10 million

Profit after tax increased by 69.4% to $18.91 million

Net cash generated from operating activities increased by 41.5% to $18.87 million

Free cash flow increased to $12.28 million, compared with $4.86 million in Q1 2025

Basic earnings per share increased by 77.8% to $0.80 (Q1 2025: $0.45)

Quarterly dividend: The Board approved a dividend of 14 cents per share which will be paid on 5 June, 2026

Cash on hand at the end of quarter: $170m

Gold production, sales, and costs:

The Blanket Mine produced 14,767 ounces of gold in Q1 2026 (versus 18,671 in Q1 2025) and sold 13,372 oz, with 3,656 oz of gold bullion on hand at quarter end

Consolidated gold sales were 13,784 oz, compared to 19,388 oz in the comparative quarter

Consolidated on-mine cost averaged $1,740/oz sold which was higher due to the lower production volumes

AISC averaged $2,765/oz sold, based on 13,784 oz sold

Operational updates:

Bilboes Gold Project: Following the publication of the Feasibility Study in November 2025 and the successful completion of the $150 million convertible senior notes offering in January 2026, progress continues on advancing the financing of the Bilboes project, including both the interim facility and the broader project finance facility, in line with the Group's previously disclosed financing strategy.

Blanket exploration: As announced by the Company on 7 April, encouraging deep‑level drilling results continued to demonstrate the continuity and quality of the Blanket, Eroica and Lima orebodies at depth, supporting confidence in the long‑term sustainability of Blanket.

Management commentary:

We continue to trade in line with market expectations and with a strong gold price environment, improving operational performance at Blanket and continued progress towards developing Bilboes, we remain confident in our strategy and our ability to deliver long‑term value for shareholders.

As previously advised, we expect production to be weighted towards the second half of the year and we reiterate our full‑year production guidance at Blanket of 72,000 to 76,500 ounces.

Measures to improve the grade have already been implemented: the grade has improved month-on-month during the quarter, and the improvement has continued into April.

Some commentary on the Middle East situation:

The recent geopolitical developments in the Middle East have had no impact on the Group's operations to date. Diesel, of which the group consumes approximately two million litres per annum, represents less than 3% of operating costs, and the group has secured supplies of over one million litres, providing substantial buffer and supply certainty.

At present the Group is selling its exported portion of gold through South Africa (rather than the Middle East), ensuring uninterrupted revenue flows for that portion.

Some commentary on the Bilboes project:

Bilboes represents a transformational investment opportunity for Caledonia. The publication of the Feasibility Study in November 2025 indicates a 10.8 year life of mine with average annual production of 150 thousand ounces and a forecast AISC of $1,061/oz.

Once in full production, based on the Feasibility Study, Bilboes' average annual contribution is expected to result in an approximate fourfold increase in the Group's attributable gold production and at significantly lower operating costs than current operating costs.

Ed S’s view:

Like most gold producers, Caledonia is making a lot of money at the moment. With gold prices well above its all-in sustaining costs ($2,765/oz in Q1), it’s very profitable.

Having said that, the Q1 update gives us a glimpse of some of the operational issues that gold miners can face. For the quarter, gold production was 14,767 ounces versus 18,671 ounces in Q1 2025.

Production in the quarter was lower than anticipated, primarily due to lower mined grades. This reflected the mining sequence and constrained access to higher grade, higher volume areas. Performance during the quarter was also impacted by equipment availability issues and challenging ground conditions in certain areas, which temporarily limited access to some planned ore sources.

Ultimately, a lot can go wrong from an operational perspective. In this industry, setbacks are very common.

The other big risk to be aware of from an investment perspective is that gold miners are at the mercy of gold prices. Obviously, gold prices are high at present so this is not an issue today, but what if they were to fall?

Given these issues, it’s hard to accurately value these companies. Earnings forecasts suggest that the stock is cheap on a forward-looking P/E ratio of 6.44, but realistically, these forecasts could be way off the mark.

Despite all these risks, I’m happy to leave this stock on an AMBER/GREEN rating, given the level of profitability today and the scope for growth potential due to the Bilboes project. If one is bullish on gold, and looking for a leveraged play on the precious metal, this stock could be worthy of further research.

The StockRank is a healthy 85.

See what our investor community has to say

Enjoying the free article? Unlock access to all subscriber comments and dive deeper into discussions from our experienced community of private investors. Don't miss out on valuable insights. Start your free trial today!

Start your free trialWe require a payment card to verify your account, but you can cancel anytime with a single click and won’t be charged.