Mid East tensions continue to rumble with Israel and Iran firing missiles at each overnight. In Iran, there have been explosions in Tehran, at various military targets across the country, and at a petrochemical complex in the city of Mahshahr. This comes despite reports that President Trump told Israeli PM Netanyahu to not respond to Iran’s missile strikes.

As a consequence, oil is back testing recent highs although it remains below the levels seen in early May.

In markets, AI-related shares fell sharply on Friday afternoon after another very strong US jobs report saw 172,000 job gains. The Nasdaq fell by over 4% as investors started to price in the potential for rate hikes rather than rate cuts later this year. This negative sentiment continued overnight in the Korean market, where the Kospi index fell by more than 8% at the open.

Overnight market movements:

The FTSE is set to open down 0.75% at 10,300

S&P 500 is up 0.3% at 7,380

Brent crude is up 5% at $97.35

Gold is down 0.75% at $4,300

Bitcoin is up 1.6% at $62,800

Wrapping it up there, thank you. Spreadsheet accompanying this report: link.

Companies Reporting

| Name (Mkt Cap) | RNS | Summary | Our view (Author) |

|---|---|---|---|

Balfour Beatty (LON:BBY) (£3.9bn | SR75) | The independent compliance monitorship of its U.S. subsidiary Balfour Beatty Communities, LLC required by the U.S. DoJ formally concluded on 6 June 2026. A number of improvements were made during the monitorship period. | ||

Tate & Lyle (LON:TATE) (£2.2bn | SR75) | Cash offer from Ingredion for up to 615p per share, comprising a payment of 595p per share, plus the right to dividends totalling up to 20p per share. This offer represents a 58.7% premium to the undisturbed closing price on 13 May 2026, or 64% including dividends. | TAKEOVER (Graham) | |

PPHE Hotel (LON:PPH) (£821m | SR41) | PPHE clarifies that the entity within the Fattal Hotel Group which is proposed to be the offeror for PPHE (should an offer be made) is Fattal Hotels Ltd. This entity is also the owner of 1.66m shares in PPHE. The MD of Fattal Hotel Group also owns 1,350 PPHE shares. | TAKEOVER (Graham) [no section below] The Managing Director of M&A at Fattal Hotels - who are hopefully going to buy PPH - was personally buying PPH shares on 14th November 2025, the same day that PPH's major shareholders announced that they were planning to hold meetings with a view to potentially selling their stakes. Although he only bought 49 shares that day (for less than £1,000!), this transaction changes the minimum lawful price at which the takeover of PPHE can take place. Thankfully, the deal can still go ahead at £22 per share. This MD is "a core member of the deal team in relation to the offer", and personally holds 1,350 shares, worth nearly £30k at the proposed takeover price. I don't think any of this affects the likelihood of the transaction going ahead, but I do find it interesting and surprising that someone so close to it could personally profit from it in this way. | |

Boohoo (LON:DEBS) (£328m | SR23) | New partnership to develop beauty and fragrance products across Debenhams Group brands. First collections will launch ahead of Christmas and will include ranges for PrettyLittleThing, Karen Millen and boohooMAN. | ||

Pensana (LON:PRE) (£320m | SR6) | $250m development of Longonjo is on target and on budget for commissioning in 2027 with a 20yr mine life and initial MREC production of 20kt. A “multi-partner offtake framework has been established”. | ||

On Beach group (LON:OTB) (£210m | SR38) | Commencing a buyback programme for up to £10m for completion by 31 Dec 26. Shares purchased will be cancelled. Equivalent to 4.8% of share capital at the current share price. | ||

BRCK (LON:BRCK) (£160m | SR81) | Jacksons was founded in 1947 and supplies premium timber and steel fencing, gates and perimeter security systems. BRCK is acquiring the business for £15m plus £4.9m for freehold land and property and deferred consideration of up to £11m. Jacksons generated EBITDA of £4.2m in FY25 and had net assets of £26.1m. Cavendish forecasts cut: - FY27E adj EPS: 8.6p (prev. 9.6p) - FY28E adj EPS: 9.1p (prev. 10.0p) | BLACK (AMBER/GREEN ↓) (Roland) This acquisition seems reasonable to me, but I’m disappointed to see broker Cavendish has cut its FY27 and FY28 forecasts without the company making any mention of a change to expectations in today’s RNS. While BRCK shares still look potentially good value to me as a Contrarian buy, I think today’s revised guidance justifies a more cautious stance. I’m downgrading our view by one notch ahead of BRCK’s FY26 results, which I expect in July. | |

KEFI Gold and Copper (LON:KEFI) (£157m | SR19) | 2025 operating loss of $(6.7)m with year-end net cash of c.$8.5m. Confident in the development of the Tulu Kapi mine, which has arranged financing of more than $400m and is targeting production in mid-2028. Tulu Kapi is expected to generate annual EBITDA of $355-697m in its first three years of operation, based on gold at $3k-5k/oz. | ||

Pharos Energy (LON:PHAR) (£120m | SR92) | $12.6m received year-to-date, “clearing all receivables due in Egypt” including the collection of contingent consideration from its farm-out partner IPR. Returned to drilling in Egypt, with the first well spudded on 4 June. | ||

Beeks Financial Cloud (LON:BKS) (£111m | SR17) | “Beeks has signed a 5-year contract with a total value of $4.8m with one of the world's largest banks for deployment of the software in one area of its trading infrastructure. Revenue recognition is set to commence immediately, further supporting the Board's FY26 expectations.” | AMBER ↑ (Roland) Investors are evidently relieved that Beeks continues to expect to meet full-year expectations – as we identified in February, H1 performance suggested a revenue shortfall for the remainder of the year unless some new revenue was secured. I continue to have concerns about the profitability and capital intensity of this business and think our cautious view this year has been appropriate. However, I’m willing to move up one notch to neutral today to reflect Beeks’ reduced valuation and in-line guidance. | |

Audioboom (LON:BOOM) (£101m | SR26) | SP -14% Three non-binding offers were received for amounts over 540p per share. The board has concluded these all undervalued the company and has terminated discussions and concluded the strategic review. Trading: strong start to the year continued into Q2; expects to report H1 revenue of at least $45m, with adjusted EBITDA of at least $3m. | AMBER ↑ (Graham) [no section below] The market is disappointed today that no immediate takeover is happening at this podcast publisher, but I think it makes sense for us to upgrade our stance to neutral on the grounds that three separate parties were (apparently) willing to offer more than 540p. With a current share price of 480p, it would be churlish for us to remain negative on this share. That being said, I'm still quite cautious when it comes to Audioboom, due to repeated disappointment in the past. For the record, Cavendish are forecasting revenue of $94.5m and adj. EBITDA of $7.2m this year, converting to adj. PBT of $6.5m. Perhaps I'll need to be a little more open-minded in future about this, as I don't think the valuation is objectively extreme at this level. With 31 cents of adjusted EPS according to Cavendish, the adjusted P/E multiple for the current year falls to about 20x. Perhaps not so crazy, if the current growth trajectory continues? Q1 organic growth is estimated at c. 19%. | |

MPAC (LON:MPAC) (£79m | SR39) | Trading affected by delays in customer decision making, heightened pricing pressure and negative operating leverage from lower volumes. H1 margins are now expected to be lower than last year, with FY26 underlying pre-tax profit “substantially below current market expectations …”. Sale of Lambert subsidiary for initial consideration of £16m. - Shore Capital cuts FY26 EPS estimate by 44% to 21.0p. | BLACK (RED =) (Roland) This is a big profit warning that’s only made slightly more palatable by the sale of a loss-making subsidiary to reduce debt. Mpac is getting its money back on Lambert, having acquired it for £15m in 2019. But I estimate leverage will still be close to 2x EBITDA, while trading conditions and margins in the group’s core business remain under pressure. This is the second profit warning from Mpac in the last year – I think it makes sense to remain cautious until there’s more clarity on trading and the balance sheet. | |

Helix Exploration (LON:HEX) (£73m | SR16) | Agreed to acquire 100% of membership interests of Treasure State Drilling LLC for $600k through the issue of new shares. The main asset held by TED is the drilling rig which has drilled all of Helix’s existing Rudyard production wells, lowering future drilling costs. | ||

Cora Gold (LON:CORA) (£73m | SR28) | Now that Sanankoro is fully funded, CORA is focused on expanding the current JORC compliant mineral resource estimate, extending Reserve mine life beyond the current 10.2 years and supporting future production growth. | ||

MTI Wireless Edge (LON:MWE) (£61m | SR95) | The contract for the supply of communications infrastructure to the Israeli Ministry of Defence has doubled in value, increasing from US$2.2m to approximately US$4.5m. | ||

Revolution Beauty (LON:REVB) (£40m | SR38) | Debenhams and Revolution Beauty have agreed a new licensing partnership to develop beauty and fragrance products across Debenhams Group brands. It’s a related party transaction as Boohoo/Debenhams is the largest shareholder in REVB. | ||

Zenith Energy (LON:ZEN) (£32m | SR23) | Acquires an additional 5 MWp ground-mounted photovoltaic development project in Rome. Total consideration €440k. | ||

Skinbiotherapeutics (LON:SBTX) (£25m | SR n/a - suspended) | Investigation findings: “Accrued royalty revenue of £0.77m was inappropriately recognised [in FY25]...No other issues related to revenue were identified. Documentation provided as support for the FY25 accrued royalty revenue was identified by FRP as fabricated by the former CEO; no evidence has been identified to indicate that anyone else was involved or aware of the fabrication.” Trading on AIM restored today. Cash position £1.5m as of 31st May. | ||

Neo Energy Metals (LON:NEO) (£20m | SR20) | The Board has suspended the CFO while investigating potential misconduct. The misconduct allegation is not in respect to any financial mismanagement, impropriety or wrongdoing and the Company's financial position has not been impacted. | ||

Great Western Mining (LON:GWMO) (£19m | SR23) | GWMO’s shares have been approved to trade on the OTCQB Market in the US and will commence trading at the market open today under the ticker symbol "GWMOF". | ||

IXICO (LON:IXI) (£19m | SR12) | IXI has added three further experts to its Scientific Advisory Board. | ||

Aptamer (LON:APTA) (£18m | SR8) | New funded research programme with Imperial College London, supported by the Gates Foundation. | ||

Oriole Resources (LON:ORR) (£15m | SR27) | Total JORC Inferred Mineral Resource Estimate at the 50% owned Mbe orogenic gold project currently stands at 1.23 million oz contained gold. Results for holes MBDD043 and MBDD044 have returned 23 mineralised gold intersections. | ||

Total Graphite (LON:TGR) (£10m | SR6) | The Board has initiated a graphite portfolio optimisation programme to evaluate the options available to accelerate development and maximise value for all shareholders. |

Graham's Section

Tate & Lyle (LON:TATE)

Up 14% at 558.5p (£2.5bn) - Recommended cash acquisition of Tate & Lyle PLC - Graham - TAKEOVER

On 14th May, we learned that Ingredion were considering a takeover of Tate & Lyle for 615p: 595p plus 20p of dividends.

Today we learn that both Ingredion and the TATE Board are happy to go ahead with this, and we have the formal proposal.

Premium: It’s a 58.7% premium to the share price on 13th May, and an even higher premium when measured against the average price prior to that date.

Shareholder support: there are irrevocable undertakings to support the takeover from shareholders holding 17% of the company.

Rationale from the TATE Board:

The Tate & Lyle Board remains fully confident in the ongoing execution of its strategic plan and that its successful delivery through volume-led growth and strengthened financial performance will create value for the Tate & Lyle Shareholders over time. However, the financial performance in the 2026 financial year was disappointing and, while actions are being taken with urgency to return the business to top-line growth, the continuation of the current challenging market environment creates risks and uncertainties in the timing of delivery of Tate & Lyle's financial algorithm.

The so-called financial algorithm targets “4-6 per cent. organic revenue growth, Adjusted EBITDA growth ahead of Revenue, and Adjusted EPS growth ahead of Adjusted EBITDA”.

In FY March 2026, both revenue and adjusted EBITDA declined by 3% organically.

For FY March 2027, the company has guided for “modest revenue growth” and “broadly flat EBITDA” excluding a $20m charge.

It seems to me that the Board may have realised that they are unlikely to achieve the financial algorithm in the near-term.

We learn that Ingredion’s offer was unsolicited and that they initially proposed to pay 530p, with some of this being in the form of shares rather than cash. Negotiations led to four further proposals, culminating in the 615p cash offer.

This is 9x adjusted EBITDA for FY March 2026. As such, it’s “an attractive opportunity for Tate & Lyle Shareholders to realise a certain cash value… relative to the risks inherent in the execution of Tate & Lyle's strategy.”

Rationale for Ingredion is straightforward:

“Bolstering Ingredion's portfolio and creating significant strategic growth opportunities”

“Creating a complementary and differentiated portfolio for texture and sugar reduction”

Et cetera

Ingredion sees synergies of approximately $130m, at a one-off cost of $175m.

Graham’s view

It always leaves a bitter taste when a struggling company accepts a takeover offer - there is a sense of “what might have been”.

In the chart below, I’ve put a circle around the date when TATE announced that it was making the $1.8 billion acquisition of CP Kelco:

Just before they announced that, two years ago, their shares were trading at 670p, nearly 10% higher than today’s takeover offer.

The company’s leverage multiple had been a lowly 0.5x, following disposals. It moved up to 2.2x after buying CP Kelco

And in hindsight, what value did this acquisition create?

As for the bigger picture, I’m becoming rather wary of ingredients businesses. They’ve always felt a little inscrutable but it seems that the competition in the space might be particularly intense these days, with changing consumer tastes adding to their unpredictability.

And with low ROCE, firms in the space have turned to leverage to boost returns:

Ingredion (NYQ:INGR) has much higher ROCE numbers than Tate, but they too are moving up the risk spectrum: their leverage multiple will rise temporarily up to 3x in order to fund this deal.

Roland's Section

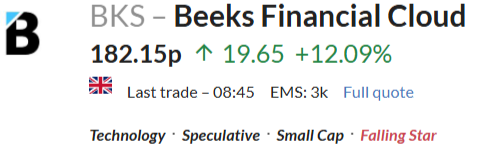

Beeks Financial Cloud (LON:BKS)

Up 16% at 188p (£128m) - First Market Edge Intelligence® customer - Roland - AMBER ↑

Beeks Financial Cloud Group plc (AIM: BKS), a cloud computing and connectivity provider for financial markets, is pleased to announce that it has secured its first contract for Market Edge Intelligence®, the analytics platform that brings AI-powered insight directly to the colocation edge.

Beeks has signed a five-year contract with a total value of $4.8m with “one of the world’s largest banks for deployment of the software in one area of its trading infrastructure”.

Importantly, revenue from this contract will help Beeks meet full-year forecasts for the current financial year, which ends on 30 June:

Revenue recognition is set to commence immediately, further supporting the Board's FY26 expectations.

In February and March I flagged up my estimate of a c.£4.5m shortfall in revenue visibility needed to meet full-year forecasts. The wording of the statement above doesn’t (quite) guarantee that full-year revenue estimates have been met, in my view, although it’s presumably very close.

This interpretation is supported by a new note today from house broker Canaccord Genuity. CG’s analysts estimate that today’s announcement and another recent win have unlocked £3-4m of additional revenue towards full-year forecasts. My reading of this is that they think Beeks is almost there, but perhaps not quite.

Investors are evidently more confident than previously that Beeks will meet FY26 forecasts.

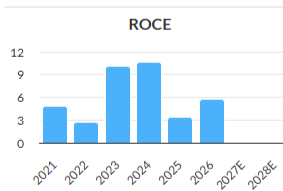

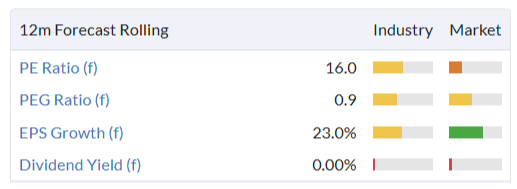

It’s too soon to know how large the addressable market for the company’s new Market Edge Intelligence service might be, but as an added-value software product, I would expect it to contribute higher-margin revenue than the group’s core infrastructure business.

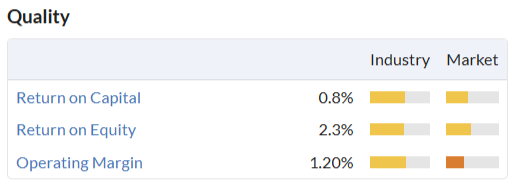

If I’m right (and uptake continues), this could help to improve Beeks’ rather average profitability metrics:

Roland’s view

Beeks’ share price is down by 20% this year and it seems to have been a tight race to meet FY26 forecasts. I think our cautious view this year has been appropriate.

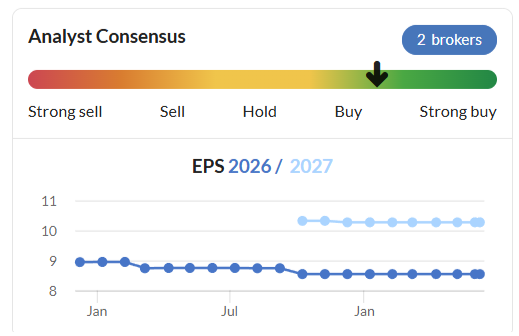

Interestingly, the StockRanks have reached a similarly cautious conclusion by a purely quantitative approach

Beeks’ StockRank of 17 is unusually low for a profitable, established business, and highlights weak value and momentum – a classic Falling Star profile. It will be interesting to see if this improves at all after today’s update:

Despite this, broker forecasts have remained stable this year and continue to suggest continued double-digit EPS growth over the year ahead:

A sub-1.0x PEG ratio also highlights the possible relative value on offer here from rapid earnings growth, despite the high-teens P/E:

I continue to have concerns about the profitability and capital intensity of this business.

But in the interests of balance, I am willing to move our view up by one notch to neutral today to reflect Beeks’ reduced valuation and in-line guidance. AMBER ↑

MPAC (LON:MPAC)

Down 12% at 231p (£70m) - Trading Update and sales of Mpac Lambert for up to £20m - Roland - BLACK (RED =)

In April, Graham concluded there was “a very high risk of a profit warning” from high-speed packaging specialist Mpac. He cut our view down to RED, citing a fragile balance sheet, unhelpful reporting style and departing CFO.

This decision has proved prescient – today we have a nasty profit warning that’s led the company’s house broker to cut its earnings forecasts for this year by 44%.

Mpac’s weak balance sheet and unhelpful reporting style are also on display; there’s no guidance in today’s RNS as to reduced profit expectations and the company is selling a subsidiary to help reduce debt.

Key points

Trading Update: in April Mpac warned of an H2 weighting, with “uncertain market conditions” and said the Middle East conflict was affecting the timing of customers’ capital investment decisions.

Lower order volumes and price competition were also said to be putting pressure on gross margins.

This situation has continued and the company has taken steps to “align operational capacity with current demand levels, reduce overhead costs and to improve cash generation”.

The order book improved to £98.8m at the end of May (31 Dec 25: £90.0m).

Revised Outlook:

Accordingly, the Board now expects first half margins to be below the prior year, and FY 2026 underlying profit before tax to be substantially below current market expectations on a like-for-like basis.

While this is clearly a serious profit warning, the company’s commentary isn’t as clear as it could be.

Today’s RNS doesn’t include details of previous or revised expectations. Nor does Mpac explain the like-for-like basis, although I assume this relates to the disposal of Lambert.

Fortunately brokers Shore Capital and Panmure Liberum have both made updated forecasts available on Research Tree this morning – many thanks.

Here’s a summary of the Shore Capital estimates (Shore is Mpac’s Nomad):

FY26E adj EPS -44% to 21.0p (previously 37.5p)

FY27E adj EPS -35% to 28.2p (previously 43.3p)

Shore also splits out the impact of today’s disposal, providing like-for-like figures that compare revised expectations with prior performance ex-Lambert:

LFL FY26E adj EBIT £12.3m (-27% vs £16.8M previously)

Lambert Disposal & Balance Sheet: today’s update contains a clear warning that the balance sheet is under pressure:

The Group continues to focus on maintaining appropriate liquidity and covenant headroom. This position will be materially improved by the proceeds from the sale of Lambert.

To address this risk and further focus the group on packaging machinery solutions, Mpac has agreed the sale of its Lambert subsidiary. This business is based near York and specialises in bespoke product assembly processes.

£16m disposal: Lambert has been sold to Italian automation technologies firm Mech.i.Tronic S.p.A. for an initial cash consideration of £16.0m. A further £4m of earn-out consideration may become payable, although I note that Shore Capital has excluded these from its modelling.

Mpac purchased Lambert for £15.0m in 2019, so this investment appears to have largely wiped its face, although the business generated a pre-tax loss of £1.6m last year.

The main rationale for the sale seems clear:

The net proceeds from the sale will be used to significantly reduce Group net debt, which stood at £47.9m at 31 December 2025.

Roland’s view

Using today’s revised broker forecasts, I estimate that net debt of £48m would equate to a net debt/EBITDA leverage multiple of 2.8x. That’s higher than I’m comfortable with and may be higher than the company’s lenders want to see, too.

I would guess that the Lambert disposal will presumably reduce net debt to something closer to £30m, bringing the leverage multiple under 2.0x.

However, I’m not sure that’s enough to persuade me to take a positive view of Mpac. This stock is styled as a Value Trap by the StockRanks, a view I think is fair. It looks perennially cheap but appears to lack any major competitive advantages or pricing power.

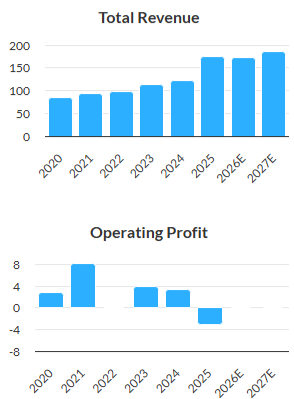

Expenditure on acquisitions has lifted revenue but so far failed to generate any additional profit – a situation worsened by today’s warning:

The picture may improve over the coming years, but this is the second profit warning in 12 months:

While the reduction in net debt from the sale of Lambert is helpfully, leverage remains relatively high and I am inclined to remain cautious. Checking the 2025 results, I see that the company mentions its compliance with banking covenants (often an indicator that cover is getting tight) and will need to renew its debt facility in 2027.

Additionally, the scale of today’s cut to forecasts means that Mpac’s forecast P/E has actually risen today to 11x FY26 earnings (previously 7x). In other words, the shares are more expensive than they were on Friday, based on current expectations.

I could probably justify moving our view up by one notch to AMBER/RED today on the basis of the reduction in leverage.

However, given the scale of today’s profit warning, I’d prefer to have more clarity on trading and the state of Mpac’s balance sheet before moderating our view. I’m going to stay RED for a little longer.

BRCK (LON:BRCK)

Down 0.2% at 49.5p (£159m) - Acquisition of H.S. Jackson & Son - Roland - BLACK (AMBER/GREEN ↓)

We’ve generally been positive on this construction materials distributor in recent months and my view remains broadly favourable.

Today’s acquisition looks like a sensible deal at a reasonable price, in my view.

However, updated coverage from the company’s house broker today also flags up a cut to earnings forecasts for FY27 and FY28. This has led me to the reluctant conclusion BRCK has pushed out a hidden profit warning through its broker.

Let’s take a look.

Acquisition

BRCK has acquired H.S. Jackson & Son (Fencing) Limited:

Jacksons designs, manufactures and installs premium timber and steel fencing and perimeter security systems. The company’s main markets appear to be upmarket housing and industrial/infrastructure applications.

The business generated revenue of £40.9m and £4.2m of EBITDA during the year ended 30 Sept 25.

Initial consideration: BRCK is making an upfront payment of £15m for the business, plus £4.9m for associated freehold land and property from which Jacksons operates.

Deferred consideration: up to £11m over three years, tested against target financial performance criteria and subject to a one-year extension in certain circumstances.

Total consideration of up to £30.9m

Valuation: we are told that Jacksons generated £4.2m of EBITDA in the year ending 30 Sept 25. That gives the acquisition a valuation range of 3.6x to 7.4x EBITDA, depending on whether you include the property purchase and/or deferred consideration.

For context, BRCK’s own shares trade on a trailing EV/EBITDA multiple of 5x, according to the StockReport.

Roland’s view: BRCK’s markets are cyclical and it looks like Jacksons is no exception. But on balance, this looks like a sensible acquisition which could expand BRCK’s access to a number of attractive end markets.

The valuation looks reasonable to me, assuming the deferred consideration criteria are suitably stretching.

Revised broker estimates: hidden profit warning?

We often complain that investors without access to broker notes don’t always get the full picture from RNS updates. Unfortunately, this appears to be the case here.

There’s no mention of trading or any change to FY27 expectations in today’s update from BRCK.

However, Cavendish estimates for FY27 and FY28 have been cut despite the addition of a contribution from Jacksons. (BRCK has a 31 March year end – Graham covered the FY26 y/e update here):

Here are the revised Cavendish estimates:

FY26E adj EPS: 8.6p (unch)

FY27E adj EPS: 8.6p (-10% vs 9.6p previously)

FY28E adj EPS: 9.1p (-9% vs 10.0p previously)

I’m not surprised to see a cut to forecasts for a construction materials company – relevant peers such as Ibstock and Travis Perkins have both seen downgrades in recent months. The sector is known to be under pressure from subdued demand and cost inflation.

What is disappointing is to see BRCK relying on its broker to slip out a downgrade, without mentioning it in the relevant RNS. I can’t help wondering if the share price reaction to today’s news would have been different if the RNS had included this information.

Roland’s view

Today’s revised forecasts leave BRCK trading on a FY27E P/E of 5.8x with a possible dividend yield of c.7%.

My view that the business could be attractively priced is (mostly) unchanged and I think the StockRanks’ Contrarian styling is apt:

However, I think the size and manner of today’s cut to broker forecasts justifies a more cautious view, so I’m cutting Graham’s previous GREEN view to AMBER/GREEN today.

With FY26 results likely in July, hopefully all investors will be given a clearer view of trading and expectations next month.

See what our investor community has to say

Enjoying the free article? Unlock access to all subscriber comments and dive deeper into discussions from our experienced community of private investors. Don't miss out on valuable insights. Start your free trial today!

Start your free trialWe require a payment card to verify your account, but you can cancel anytime with a single click and won’t be charged.