The big overnight mover is the oil price which officially returned to pre-war levels. The spot price for Brent crude has fallen to $72.50.

Although talks between the US and Iran still have a long way to go, the reopening of Hormuz has massively increased supply. I think we’ll be able to refer to the Iran situation and the oil price much less frequently in these preambles from now on!

Overnight market movements:

The FTSE is set to open down 0.3% at 10,425

S&P 500 is up 0.6% at 7,405

Brent crude (August) is down 1.8% at $72.50/bbl

Gold is down 0.3% at $3,987/oz

Bitcoin is up 1.2% at $61,700

Roland Head joins me today.

The Agenda is complete.

Companies Reporting

| Name (Mkt Cap) | RNS | Summary | Our view (Author) |

|---|---|---|---|

3i (LON:III) (£23bn | SR54) | Action LFL sales growth was 3.3% year-to-date (21 June). New store openings of 105 are on track for 2026. The remainder of the PE portfolio “continues to demonstrate good momentum in line with our expectations”. | ||

Balfour Beatty (LON:BBY) (£4.2bn | SR73) | Two-year contract from SSEN to deliver the Netherton Hub in Aberdeenshire, Scotland. This is a facility to improve transmission of renewable energy nationwide. | ||

easyJet (LON:EZJ) (£4.1bn | SR42) | Rejection of Possible Offer for easyJet and Extension of PUSU | easyJet has rejected a further proposal from Castlelake of 650p per share but has decided to give Castlelake access to “limited commercial information” in the hope of producing “a more attractive proposal”. The PUSU deadline has been extended to 5pm on 5 July 2026. | TAKEOVER |

Serco (LON:SRP) (£2.3bn | SR83) | H1 revenue +3%, with adj operating profit of c.£155m delivering a margin above 6%. Over £2bn of contract awards and extensions, with order intake of over £500m in AsiaPac. FY26 guidance unchanged for revenue of c.£5bn and adj operating profit of c.£300m. | ||

Sirius Real Estate (LON:SRE) (£1.57bn | SR74) | Sale of two business parks near Sheffield for £5.3m, a 3% premium to book value. Also exchanged contracts to develop three self-storage locations in the UK, with a total cost of £12.6m. The balance will be funded by further planned UK disposals this year. | ||

Chemring (LON:CHG) (£1.32bn | SR35) | Signed agreement with US DoW to resume sustained manufacturing at the Alloy Surfaces business, which was previously classified as discontinued. Contract value of up to $300m over five years, with a minimum of $35m/yr for the first three years. No change to FY26 or FY27 guidance. | ||

Resolute Mining (LON:RSG) (£1.09bn | SR64) | Resolute will receive a payment of A$77 million (approximately US$54 million), representing full repayment of the outstanding principal and accrued interest under the Vendor Financing Promissory Note. | ||

Volex (LON:VLX) (£1.08bn | SR81) | Preliminary Group Results FY2026 & Update on Move to the Main Market | Revenue +14.4%, adj operating profit +19.9% to $127.3m. Adj EPS +19.8% to 43.5c, in line. Net debt reduced to $152m. Growth led by strong Complex Industrial division, including Data Centre demand “from a leading hyperscale customer”. FY27 outlook: trading in line with expectations. Move from AIM to Main Market scheduled for 24 July 2026. | |

Spire Healthcare (LON:SPI) (£894m | SR57) | Remains in talks with Toscafund. Deadline for a bid has now been extended to 5pm on 9 July 2026. | TAKEOVER | |

Moonpig (LON:MOON) (£677m | SR69) | Revenue +6.5%, adj pre-tax profit +13.4% to £76.5m. Adj EPS +19.5% to 18.0p. Order growth of 2.1%, average order value +5.7%. Plans £65m buyback in FY27. Outlook: trading in line with expectations. | ||

Advanced Medical Solutions (LON:AMS) (£529m | SR59) | Recommended cash offer of 285p per share (£715m) from H.B. Fuller. Represents a 34.8% premium to the undisturbed closing price on 20 May 2026. | TAKEOVER | |

Halfords (LON:HFD) (£394m | SR95) | Preliminary results for the 53-week period ended 3 April 2026 | Revenue +2.9% with LFL sales +4.8%. Adj pre-tax profit +4.1% to £50.0m with 53-week adj EPS of 17.4p. On a 52-week comparative basis, adj EPS is up 0.6% to 15.7p (FY25 restarted: 15.6p). Net cash of £19m. FY27 outlook: expect adj pre-tax profit to be towards the top end of the consensus range. | AMBER/GREEN = (Roland) Today’s results are flattered by a change to the group’s accounting policy that boosts its profit calculation. Even so, I think it’s a fairly solid performance in a difficult year, with good cash generation. Today’s outlook guidance suggests double-digit profit growth over the coming year, but this remains a low-margin business in a competitive market. On balance, I think our AMBER/GREEN view is a fair reflection of the risk/reward balance here. |

SDCL Efficiency Income Trust (LON:SEIT) (£364m | SR n/a) | NAV -14.1% to 77.8p per share. Portfolio valuation -10% to £1,078.4m. Total dividend paid 4.8p (FY25 6.32p), no fourth dividend to be paid. Intends to pursue a managed wind down or portfolio sale. | ||

Avacta (LON:AVCT) (£342m | SR8) | Platform-Validating Data with Faridoxorubicin & FDA Agreement on Pivotal Trial Design for AVA6000 | Seen robust tumor responses in patients with salivary gland cancer (SGC) for patients treated with faridoxorubicin. Has agreed the pivotal trial design for faridoxorubicin (AVA6000, pre|CISION-enabled doxorubicin) with the U.S. Food and Drug Administration (FDA) for a potential full regulatory approval. | |

Tharisa (LON:THS) (£333m | SR99) | Secured new ZAR750m (USD45.5m) revolving facility from Nedbank. Includes an option to increase the facility to ZAR1.25bn. Ensures underground mining fleet is now fully funded. | ||

B.P. Marsh & Partners (LON:BPM) (£252m | SR72) | Agreed $5.1m investment for a 17.9% interest in Autonomy, which is a newly formed investment vehicle. Autonomy has been established in partnership with XPT and will invest in US insurance distribution businesses, including XPT. BPM will receive a $12.1m payment from XPT for redemption of preferred units and debt as part of the transaction. | ||

Cornish Metals (LON:TIN) (£144m | SR19) | Has signed and concluded a new mineral lease in the mineral rights area at South Crofty. The Dudnance Lease is valid for 25 years. TIN owns 50% of the mineral rights and has agreed the lease with the family that owns the remaining 50%. | ||

Mercia Asset Management (LON:MERC) (£122m | SR52) | Warwick has completed an equity funding round of £6.4m, with additional funding of up to £1.1m anticipated. This will underpin the next phase of growth including the recent partnership with Jaguar Land Rover. Mercia has invested £0.7m from its balance sheet, with the remainder coming from a Mercia-managed fund and other co-investors. | ||

Aptitude Software (LON:APTD) (£112m | SR38) | New Fynapse contract win with a leading Canadian financial services group managing over C$100bn in assets. 3yr contract has a value of US$5.54m. | ||

Braemar (LON:BMS) (£76m | SR90) | Richard Heading appointed as CFO. He will join on 29 June 2026. He was most recently CFO at Record plc and was previously at IG Group. | ||

Clean Power Hydrogen (LON:CPH2) (£68m | SR n/a) | The parties have agreed to enter into definitive documentation relating to a Convertible Loan Note alongside a nine-month exclusivity period to negotiate and agree a Strategic Partnership and Manufacturing and Technology Development Agreement. “Hidrigin acknowledges the recent failure at final testing of the technology by CPH2 but continues to believe in the global potential for this new category of electrolyser and are investing to bring it to market.” | CPH2 shares have been suspended from trading since 29 May 2026. | |

Seascape Energy Asia (LON:SEA) (£62m | SR34) | Significant progress on Temaris field development with all key FEED (engineering) contracts awarded and well design completed. Initiated a process in Q1 to introduce a strategic partner into Temaris. Now broadening the scope to consider a wider range of participants and structures. | ||

Caspian Sunrise (LON:CASP) (£47m | SR32) | Deep Well 803 has been deepened to 3,927m. On the basis of the encouraging results to date at Deep Well 803 three further deep wells are to be drilled on the Yelemes Deep structure with Deep Wells 701 and 707 expected to be spudded in July 2026. | ||

Time Finance (LON:TIME) (£46m | SR76) | Gross lending book +15% to £250.9m. Adjusted PBT +8% to £8.5m. Statutory PBT £8.4m. Net arrears and net bad debt write-offs are both “relatively stable”. “We have a proven, simple model that continues to deliver and the Board is confident that the Group remains appropriately positioned on its growth strategy…” | ||

Zambeef Products (LON:ZAM) (£29m | SR81) | Revenue +2.3% (measured in Zambian Kwacha), +29.2% (measured in USD). Material appreciation of the Kwacha during the period. Kwacha PBT +58%, USD PBT +99% to $3.8m. “Looking ahead to the second half of the financial year, the completion of the summer crop harvest in June is expected to materially improve the Cropping division's contribution and provide a favourable internal raw material base for Stockfeed and Milling.” | ||

Rome Resources (LON:RMR) (£27m | SR25) | Raised £1.6m in H1 2026. 2026 has seen the completion of a further 3,250m drilling programme at the Bisie North Project. Broader Kalayi intercepts from 2026 drilling have verified the geological model. Material uncertainty re: going concern. | Slow to publish FY25 results. | |

Petro Matad (LON:MATD) (£21m | SR17) | Mid-2026 Update: Production from Heron-1 has continued as forecast and production from Gazelle-1 has exceeded expectations post the period end. Average production year to date is 233 bopd. Block XX farm-out discussions are continuing, and with the significant rise in the oil price, an uptick in interest has been shown by a number of potentially interested parties. | Slow to publish FY25 results. | |

First Property (LON:FPO) (£20m | SR65) | PBT +12% to £3.4m. Cash £6.95m. Total AUM £189m (FY25: £220m). "The economy and markets remain challenging, but we are identifying some interesting deals and taking the opportunity to buy them where possible.” Positive outlook. | ||

Cleantech Lithium (LON:CTL) (£19m | SR21) | CTL had expected ratification of the CEOL to take place in Q2 2026, however, the administrative process with the Comptroller General's Office is taking longer than anticipated as it works through all the CEOL decrees put forward by the previous Government. CFO’s consulting agreement extended to September. | ||

Aptamer (LON:APTA) (£18m | SR8) | Aptamer has initiated its AI development programme, representing a significant step towards building an AI-enabled Optimer® discovery engine. Capital expenditure has been deployed to purchase new automation equipment, and the company has made significant progress across its internal therapeutic development pipeline: | ||

NAHL (LON:NAH) (£18m | SR76) | “...the positive trading momentum recorded in the first quarter of 2026 has continued into the second quarter of 2026. As a result, the Board remains confident in delivering a full year outturn in line with management's expectations.” | ||

Manolete Partners (LON:MANO) (£15m | SR63) | Realised revenue £27.9m in line with expectations. Adjusted realised PBT £0.1m. Two debtors did not pay when anticipated… the total net exposure to these debtors is £4.7m. The adjusted realised PBT figure is after taking a £1.8m provision against these debtors. Outlook: a positive start to FY27. Case signings and completions ahead of the prior year. | ||

Block Energy (LON:BLOE) (£14m | SR15) | The 3D seismic programme, covering the highly prospective Martkopi Terrace prospect within the XIQ PSC area (Project IV), is scheduled to commence in July. | ||

Ingenta (LON:ING) (£13m | SR97) | “...the Company is expecting to deliver increased revenues in 2026 compared with 2025… additional costs being incurred by the Company will result in EBITDA for the current year being a little lower than in 2025, despite the increased revenues.” | AMBER ↓ (Graham) | |

Orchard Funding (LON:ORCH) (£12m | SR92) | Final results for 18-month period. PBT £6.59m. Borrowings £33.6m. "...a strong set of results for an 18-month period that has reshaped our business. We have continued to grow our lending in our core market of insurance premium finance while carefully managing our costs and margins.” | ||

Mind Gym (LON:MIND) (£10m | SR21) | Revenue -23%, like-for-like revenue -7%. Adjusted EBITDA £0.6m, pre-tax loss £5.2m. Outlook: “...in FY27 we anticipate a return to modest revenue growth alongside positive EBITDA and a strengthened cash position.” Going concern warning. |

Graham's Section

Ingenta (LON:ING)

Down 17% at 69.98p (£10m) - AGM Statement - Graham - AMBER ↓

This is a “leading provider of software and services to the publishing and media industries.”

It looked cheap to me in April, but unfortunately it has only gotten cheaper since then, with the market cap falling from £15m to £10m since then:

A quick summary of this AGM statement:

Over £2m of new business wins this year (context: historic annual revenues of c. £10m).

Encouraging pipeline of further opportunities across core markets.

The £2m figure relates to a 3-year period, so this is really just £700k p.a.

New guidance is not great in terms of profitability:

As a result of this new business momentum, the Company is expecting to deliver increased revenues in 2026 compared with 2025. The management team is continuing with previously announced plans to invest in building our sales and marketing resources, and the additional costs being incurred by the Company will result in EBITDA for the current year being a little lower than in 2025, despite the increased revenues.

Adjusted EBITDA last year was £1.6m.

Estimates: I am going to record today’s news as “BLACK” for profit warning, as the market is clearly disappointed by the news that 2026 EBITDA will be lower than the prior year.

However, for completeness, I should note that there were no 2026 forecasts for Ingenta as of yesterday. So it could be argued that it’s not a real profit warning, as there were no official consensus estimates.

That changes today with the release of forecasts from Cavendish:

2026 revenue £10.6m (up £0.3m)

2026 Adj. PBT £1.4m (down £0.2m)

2026 adj. EPS 8.8p (down 1.4p)

Further ahead, there aren’t any 2027 estimates and the company included the following paragraph in today’s statement:

Looking beyond the current year, as previously noted, there is ongoing attrition of some longer-term customers currently on our legacy platforms who have been seeking to move to global whole-enterprise software platform providers. Some of the larger customers in this group have requested to move to shorter term contracts, which reduces our visibility over future revenue streams, and introduces a greater risk level to 2027 revenues and beyond. As a result, we are prepared for the new business wins described above to be subject to an offsetting impact from reduction in revenues from these customers in 2027, although some degree of mitigation will be achieved in future years by reducing costs related to the servicing of these customers.

Graham’s view

I have to downgrade our stance on this for a few reasons today.

Firstly, the news that profits will be lower this year than last year has clearly disappointed the market.

The Cavendish forecasts are helpful but in P/E terms the stock is now trading at 8x 2026 earnings, which is a little higher than the StockReport’s trailing 7x figure.

Also, the note that there’s less visibility and a higher risk level around 2027 revenues leads to the conclusion that we can’t expect growth here in the short-term.

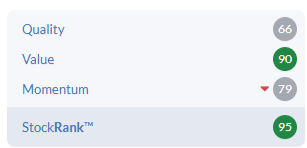

Ingenta is considered a Super Stock by the computers but I think that a neutral stance is the right call for me today, downgrading just one notch from my previous view.

Software companies at this small scale are vulnerable to lumpy, contract-driven revenues and management here has explicitly warned us that they can’t predict their 2027 results with much certainty. It says something that Cavendish waited until now to give us 2026 estimates.

All of that being said, I still think that deep value arguments could be made here. The cash balance at December 2025 was £5m. Cavendish are forecasting that the closing net cash figure for 2026 will be £4.9m.

So my position is as follows: I am neutral on Ingenta due to the lack of visibility and the downward pressure on its earnings.

At the same time, I think that it would easily be worth more than its current market cap if it was acquired in its current condition, due to the cash balance. But I can't guess at the likelihood of this happening.

I am therefore AMBER on it today, reflecting the pressures it is likely to face in the short- and medium-term.

Roland's Section

Halfords (LON:HFD)

Up 16% at 209p (£458m) - Preliminary results for the 53-week period ended 3 April 2026 - Roland - AMBER/GREEN =

Some headlines this morning have suggested that Halfords has beat FY26 profit forecasts, but I don’t think this is correct. In my view these results are in line with FY26 expectations; I will explain why below.

What is true is that the company has nudged its FY27 guidance higher this morning, triggering a round of euphoria from investors:

We now expect FY27 underlying PBT to be around the top end of the consensus range, with performance weighted towards the first half of the year.

Shares in this motoring and cycling products and services group have now risen by 50% this year, thanks to rising forecasts and growing investor confidence:

However, the stock remains a long way below its historic highs – 10 years ago, the share price was 342p.

Can CEO Henry Birch engineer a durable renaissance for this business? Let’s take a look at today’s results.

FY26 highlights

Warning - confusing accounts: the year-on-year percentage change figures I use below reflect 52-week comparative figures provided by the company, but the financial figures I’ve quoted are for the 53-week year reported today, unless I specify otherwise.

In addition, FY25 profits have been restated today to reflect a new accounting policy, so they do not map onto last year’s results.

Rising employment costs and subdued consumer spending form a tough backdrop for consumer-facing businesses such as Halfords. Sales growth remained relatively weak last year:

Revenue of £1,801.7m (+2.9% YoY)

Retail revenue: £1,062m (+3.4% YoY)

Autocentres revenue: £739.7m (+2.1% YoY)

Gross margin: 52.9% (FY25: 50.7%)

Underlying pre-tax profit: £50.0m (+4.1% YoY)

Underlying EPS: 17.4p (the 52-week EPS figure is 15.7p, which is +0.6% higher than the restated figure FY25 figure of 15.6p)

Dividend per share: +2.3% to 9.0p

Have earnings beat forecasts? Consensus forecasts for FY26 were for adjusted EPS of 13.9p. At first glance today’s results suggest a strong earnings beat, but I don’t think this is correct.

The new accounting policy introduced with these results now excludes the amortisation of acquired intangible assets from the calculation of underlying profit. Although I’m not always a fan of this approach, it is quite a common approach and has its merits.

However, in this case the impact is quite significant, as Halfords has made a number of mid-sized acquisitions in recent years:

Applying the new policy transforms FY25 adj EPS from 13.8p to 15.6p.

FY26 52-week adj EPS provided today of 15.7p is only a 0.6% increase from 15.6p.

Adding 0.6% to 13.8p gives me a figure of 13.9p – in line with FY26 consensus expectations.

When companies change their accounting policies I think it’s always worth asking why – and what would have happened if they hadn’t.

In this case the revised policy has the effect of lifting the headline measure of profit, making Halfords shares look cheaper on the most commonly used metric of adjusted P/E.

When brokers incorporate the new accounting policy into their models, this change will also feed through to a nice bump in FY27 forecasts. Happy Days!

While I can see the appeal of this change for Halfords management, I don’t think it offers much benefit for shareholders. This revised view of earnings does not reflect any underlying improvement in the performance of the business.

Trading commentary: sales growth was minimal last year and was offset by a 7.6% increase in operating costs, reflecting higher labour costs and cost inflation.

What drove the increase in underlying pre-tax profit last year was a 2.1% increase in the group’s gross margin, to 52.8%. Management says this reflects a number of factors:

This very strong performance reflected the continued success of our Better Buying programme, improvements in pricing and promotional effectiveness, and an FX tailwind as movements in the US dollar rate over the last 18 months benefitted the hedged rate coming through in cost of goods sold. Changes to our contractual arrangements with suppliers also resulted in a 30bps YoY increase in Group gross margin with a corresponding increase in operating expenses.

It would have been nice to see the improvements in gross margin split out so we could see, for example, the contribution made by FX. But it’s good progress all the same.

Looking across the group’s two divisions, performance seems to have been stronger in the Autocentres division than in retail:

Retail: revenue rose by 4.1% to £1,039m, with motoring sales +2.9% and cycling sales +6.4%. But the increase in gross margin was much smaller than in the Autocentres business and was not enough to offset a 7.6% increase in operating costs. Retail underlying operating profit fell by 3.8% to £37.5m.

Autocentres: revenue rose by 5.8% to £725m, while underlying operating profit rose by 20.1% to £18.9m. Gross margin improved by a full 3% to 55.6%, driving a £30m increase in gross profit – sufficient to offset the £27m increase in operating costs.

As far as I can see, both sides of the business are delivering some incremental improvements in difficult market conditions. However, while retail will always face tough online competition, that’s less true for Autocentres. There’s no online substitute for a physical workshop and trained mechanic. Perhaps this side of the business has a more durable future?

Profitability: these improvements translated to a modest increase in margins for the group as a whole:

Underlying operating margin +0.2% to 3.4%

Reported operating margin: 3.1% (FY25: n/a - statutory loss)

The returns being generated by the business also improved:

Company-reported return on capital employed (ROCE) up 1.6% to 14.2%

Cost of capital: Halfords says its cost of capital last year was 10.6%. It’s very rare for companies to report this figure in my experience. For anyone building a DCF model for Halfords, it would make sense to use 10.6% as the required rate of return. A figure of 10% might also be a good estimate for many other small/mid caps.

The figures provided by the company suggest Halfords is generating returns in excess of its cost of capital.

However, the more standardised and statutory approach that I prefer (and which is used in the StockReport) suggests the situation is more borderline:

Return on capital employed: 7.7%

Return on equity: 6.4%

One key difference between the two approaches is that Halfords excludes goodwill from its ROCE calculation. The issue I have with this is that goodwill reflects capital allocated to past acquisitions. In my view, it’s important to gauge whether companies are generating attractive returns on acquisition spend. I think the evidence here is mixed, so far.

Cash flow & Balance Sheet: Halfords ended the year with £19m of net cash, excluding lease liabilities. That’s a strong result, although it’s worth noting that this figure received an £8m boost from the 53rd week, due to timing effects. On a 52-week basis, net cash was £11.2m (FY25: £10.1m).

With so many profit adjustments floating around, I’m keen to see how much cash the business generated last year:

Free cash flow: £33.3m (FY25: £43m)

The company says that the decrease last year “was due in part” to the payment of performance incentives for FY25 in early FY26, but doesn’t provide any detail on this.

On the assumption that performance incentives might be due in the future, too, I am inclined to see the £33m figure as a fair representation of last year’s performance.

Applying this to today’s increased market cap of £458m gives me a free cash flow yield of 7.3% – potentially decent value.

Outlook

The company says it has not yet seen any changes to customer behaviour due to the situation in the Middle East, but believe there’s still a risk this could happen in the second half of 2026.

FY27 guidance: Halfords has restated its FY27 profit guidance to reflect the change in accounting policy:

The change in accounting policy outlined above will increase company-compiled consensus for underlying PBT in FY27 from £45.3m (with a range from £42.0m to £48.6m) to c.£49.0m (with a range from £45.7m to £52.3m). There will be a similar increase in FY28 and FY29.

FY27 underlying pre-tax profit is now expected to be “around the top end of the consensus range”, with a weighting towards H1.

I don’t have access to any broker notes today to see how analysts are addressing the 52/53-week issue. But assuming this guidance is for comparable 52-week years, then this suggests Halfords underlying PBT could rise by c.14% this year, to perhaps £52m.

Prior to today, consensus forecasts suggested a 12% rise in earnings for FY27, so this seems like a relatively modest upgrade – not necessarily enough to justify today’s 15% share price gain.

Roland’s view

Based on today’s guidance, I estimate Halfords could be trading on <12x FY27 forecast earnings.

However, without the change to accounting policies, I estimate this would be >13x.

I can’t help feeling some of today’s share price bounce may have been driven by the market revaluing the stock based on its revised formula for earnings.

Despite this, I think the current valuation could be reasonable if Halfords can continue to improve profitability and deliver above-inflation sales growth.

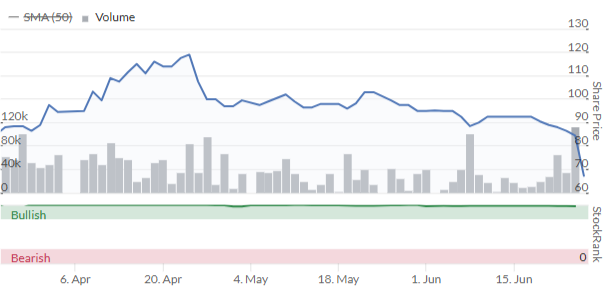

However, I wouldn’t personally want to pay much more than this. After all, this remains a slow-growing, low-margin business whose longer-term chart suggests continued structural pressure:

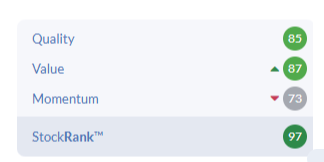

The StockRanks are fairly positive here and view Halfords as a Super Stock:

On balance, I think it’s fair to leave our previous moderately-positive view unchanged today. AMBER/GREEN

See what our investor community has to say

Enjoying the free article? Unlock access to all subscriber comments and dive deeper into discussions from our experienced community of private investors. Don't miss out on valuable insights. Start your free trial today!

Start your free trialWe require a payment card to verify your account, but you can cancel anytime with a single click and won’t be charged.