Good morning!

The agenda is now complete.

Mello 2025: Ed, Mark and Graham will be at Mello in London this week (Tue/Wed) and are looking forward to meeting subscribers in person. If you'd like to go and haven't booked it yet, we can offer a discount code "STOCKOPEDIA50", which can be used at this link. See you there!

Update 14:20: today's report is now complete, see you tomorrow!

Companies Reporting

| Name (Mkt Cap) | RNS | Summary | Our view (Author) |

Greatland Gold (LON:GGP) (£1.9bn) | Reorganising to become ASX listed. Will remain on AIM. AUD50m retail offer & 20:1 share consolidation. | ||

Sirius Real Estate (LON:SRE) (£1.44bn) | PBT +75% to €201.6m inc. €81m valuation gain. Rent roll +6.3% to €205.6m, EPRA EPS -4.7% to 7.8c. | ||

Indivior (LON:INDV) (£1.2bn) | Will cancel secondary LSE listing and maintain US NASDAQ listing. Last day of UK dealing 24 Jul 25. | ||

ME International (LON:MEGP) (£808m) | Record H1 PBT, +14% due to laundry growth. Net cash £36m. FY25 profit exp to be in line (£76-80m) H1 laundry revenue +14%, photobooths -3.3% due to technical issue. | AMBER/GREEN (Roland) This solid H1 update highlights continued strong momentum in the self-service laundry business. While photobooth revenue was slightly lower than expected due to an isolated technical issue, this is now resolved. Performance has historically been weighted to H2, so I think there’s still scope for a strong finish to the year. In the meantime, the shares seem fairly priced to me and I’m happy to remain broadly positive. | |

Custodian Property Income Reit (LON:CREI) (£366m) | 28 units w/avg value £0.7m and £1.7m rent roll; 8.1% yield. Also £2.7m of new-build housing. | ||

Anglo-Eastern Plantations (LON:AEP) (£299m) | Final results (Friday pm) | Rev +0.5% to $372.3m, op profit +17% to $81.7m. FFB production -7.5% to 1,019.8mt. | AMBER/GREEN (Mark) |

Gulf Marine Services (LON:GMS) (£224m) | A shareholder has requested a GM to propose changes to the board and payment of a dividend. | AMBER/GREEN (Roland) [no section below] This looks like a shareholder is agitating for the company to focus more closely on shareholder returns. As we’ve discussed previously, GMS will eventually need to choose between upgrading its fleet and running the existing vessels for cash. Despite today’s reference to boardroom changes, there were very few votes against directors at last week’s AGM – the largest was 3.7% against exec chair Mansour Al Alami. One other factor to consider is that the outstanding Saudi tax issue could limit dividend payment capacity this year – postponing a dividend decision until this is finalised seems prudent to me. I’ll leave our moderately positive view unchanged for now. | |

Helios Underwriting (LON:HUW) (£178m) | NAVps +11% to 243p, total return on equity of 16.8%. Retained underwriting profit flat at £31.4m. Positive outlook. | ||

Duke Capital (LON:DUKE) (£151m) | Providing £2m to Tristone Healthcare at 13.5% yield. Total credit exposure now £21.2m. Also investing further £500k equity, taking shareholding to 28.4%. | ||

Eagle Eye Solutions (LON:EYE) (£105m) | Termination of a contract with an annual value of between £9m and £10m in revenue (c.20% of annual rev), from Neptune Retail Services. No meaningful impact to FY25, which remains in line with expectations. Net cash £12.5m. Shore Cap estimates: FY26E EPS -99% to 0.1p | AMBER/RED (Roland) Eagle Eye appears to have lost its largest and perhaps most profitable customer, which has effectively taken its work in house by acquiring a competitor. This may be an isolated issue but I think it’s worth noting that it’s the second time the company has cut its revenue guidance in six months. The £12.5m net cash pile should help to support a recovery, and provides evidence of cash-generative trading in the past. But with earnings forecasts cut to almost zero for FY26, I think it makes sense to remain cautious until there’s evidence of a recovery in momentum. | |

IG Design (LON:IGR) (£83.6m) | Disposal of DG Americas (Friday pm) | Sale of DG Americas to SPV of Hilco Capital. Nominal cash payment of $1, IG Design to receive 75% any asset or business sale by Hilco, minus any working capital advanced by them. “By entering into a realisation agreement with the Buyer the Group has removed downside risk while retaining optionality on any value that may be realised.” | AMBER (Mark) |

| Frenkel Topping (LON:FEN) (£64m) | Harwood Pvt Equity - Possible Offer for Frenkel Topping | SP +15% to 49.4p Harwood and FEN are in discussions regarding a possible cash offer for FEN of 50p per share, or an alternative cash/loan/share offer also valued at 50p. This represents a 19.5% premium to Friday’s closing price of 43p and a 38% premium to the volume-weighted average price over the last three months. | PINK (Roland) [no section below] This offer represents a P/E of 12x FY25 forecast earnings. That may not seem especially generous, but this is a somewhat complex professional services business with a five-year average return on equity of just 6%. Forecast earnings growth is expected to be 8% in FY25 and just 5% in FY26. Harwood Capital is a longstanding shareholder with just under 30% of the stock, so can be presumed to know the business very well. On that basis, I think it’s safe to assume the bidders can see some value if they buy at 50p/share. However, Frenkel Topping’s record leaves me unsure as to whether the company is likely to deliver this for shareholders in its current form. The reality is also as a 30% shareholder, Harwood is in a strong position to push this through and could probably block any competing interest. On balance, I think this offer is not terrible, but could probably be a little more generous. |

MicroSalt (LON:SALT) (£32m) | Rev $0.75m (FY23: $0.57m). Net Loss $5.4m (FY23: $3.5m). Net debt $2.5m (FY23: $2.4m). | ||

Cyanconnode Holdings (LON:CYAN) (£27m) | Previously announced £70m contract for 750k smart meters is now signed. | AMBER/RED (Mark) [no section below] | |

Tekcapital (LON:TEK) (£20m) | £1.25m before expenses at 7p per share. 22% discount to 9p previous close. Proceeds to be used to support Guident investment and for general working capital purposes. | AMBER (Roland) [no section below] I commented last week on this company’s big discount and poor returns for shareholders. Today’s placing reinforces my view that TEK struggles to monetise its investments or generate satisfactory returns. The share count is up almost 4x since 2019, but NAVps has fallen. I’ll leave our neutral view unchanged to reflect the deep discount to book value, but personally I’m not convinced of the quality of the company’s investments - e.g. recently-listed MicroSalt (LON:SALT) , which reported a big loss today. | |

Facilities by ADF (LON:ADF) (£17m) | Trading remains in line with market expectations. H2-weighting. Cash in-line. Revised final dividend 0.5p (FY23 0.9p) | ||

Cordel (LON:CRDL) (£16m) | 5 year term contract with one of the US leading Class 1 freight railroads. Base contract US$3.7m over 5-years + US$3.8m for Cordel's latest PTC Asset Management SaaS launching in July. | ||

Light Science Technologies Holdings (LON:LST) (£12.1m) | Has been granted a patent for its environmental sensor, sensorGRO, covering its air and root zones measurement capabilities. Distribution Agreement Order for 400 lights, operational in 26Q1. | ||

Sunda Energy (LON:SNDA) (£12m) | LBT £2.0m (FY23 £1.7m), Cash £3.2m (FY23 £3.8m). | ||

Bigblu Broadband (LON:BBB) (£10.3m) | Rev. from continuing operations £0.7m +4% LFL, Adj. LBT £2.0m (FY23: LBT £0.7m). Net debt at 30 Nov £6.5m. Net cash of £1m, after disposal of Skymesh and £6.1m tender offer. |

Roland's section

Eagle Eye Solutions (LON:EYE)

Down 36% to 224p (£67m) - US Contract Update - Roland - AMBER/RED

Eagle Eye, a leading SaaS and AI technology company that creates digital connections enabling personalised, real-time marketing at scale, announces that the Company has been notified by Neptune Retail Solutions ("NRS") of the termination of a contract with an annual value of between £9m and £10m in revenue [...] with effect from 2 August 2025

Commiserations to holders of Eagle Eye today. This company specialises in providing retail customers with personalised loyalty deals, but has fallen sharply today after announcing the cancellation of a major contract equivalent to around 20% of annual revenue.

What’s happened? Eagle Eye says that customer Neptune Retail Solutions (NRS) has terminated an annual contract valued at £9-10m for the provision of services to a major US supermarket. NRS appears to have been the company’s largest customer.

The underlying cause of the loss appears to be that NRS has purchased a competitor to Eagle Eye, Quotient Technology Inc, and will presumably be using Quotient’s services to replace those provided by Eagle Eye. This apparent substitution makes me wonder whether Eagle Eye’s services may not be highly differentiated – that could help explain the company’s historic low margins:

This termination takes place with effect from 2 August 2025 and is not expected to affect Eagle Eye’s results for the year ending 30 June 2025, which management say should be in line with expectations.

However, Eagle Eye warns that the lost contract was “high margin in nature” and says it’s now undertaking cost-cutting measures to mitigate the impact of this lost revenue.

My reading of this comment is that the NRS contract is likely to have contributed more than 20% of the group’s profits, a view confirmed by today’s updated broker forecasts (see below).

Outlook & Updated Estimates: Eagle Eye has provided some useful guidance and balance sheet information to try and reassure shareholders today:

FY26: impact “will be material” but management expect to maintain “double-digit adjusted EBITDA margin”

83% of revenue from remaining top 10 customers is under contract until at least FY27

Net cash of £12.5m at 30 April 2025 with £20m undrawn facilities

FY27: targeting return to double-digit growth and 20% adj EBITDA margin

Eagle Eye’s management have promised a further update on the outlook for FY26 with the company’s full-year update in July.

However, house broker Shore Capital has helpfully provided updated FY26 and FY27 forecasts today – many thanks for sharing this coverage.

Unfortunately, Shore’s analysts believe the loss of revenue will drop through to cause deep cuts to earnings over the next couple of years, with FY26 now expected to be broadly breakeven at a post-tax level:

FY26E EBITDA down 61% to £5.2m

FY26E EPS down 99% to 0.1p

FY27E EBITDA down 41% to £10.3m

FY27E EPS down 56% to 11.3p

Revenue guidance for the next two years is down 18-20%, suggesting that Shore has subtracted the NRS contract and left other assumptions unchanged.

A previously announced “transformational global OEM agreement” is said to be “progressing well”, so perhaps this may support upgrades to revenue guidance at some point over the next couple of years.

Roland’s view

I think it’s fair to say that this contract loss could be an isolated problem for Eagle Eye. April’s £12.5m net cash balance is also significant as it covers nearly 20% of the market cap after today’s slump.

However, there’s no escaping that this has been a painful story for shareholders in 2025:

It’s also worth remembering that this is now the second time Eagle Eye has cut revenue guidance this year. In January, Eagle Eye warned that revenue would be lower than expected for both FY25 and FY26, prompting a broker earnings downgrade.

I took a neutral view at the time, as the impression I got was that the revenue shortfall was only partly due to weaker trading, with the remaining part due to the businesses’ ongoing transition to a service-based model.

With hindsight I was too lenient in January, but March’s interim results appeared to be in line, so we left our neutral view unchanged.

With earnings forecasts cut to almost zero for FY26, it’s hard to value Eagle Eye on a P/E basis at the moment. However, today’s FY27 forecasts suggest the shares could be on a P/E of 20, which is broadly consistent with the stock’s valuation ahead of today’s warning.

Personally, I'd be wary about relying on forecasts and forward guidance at this stage. Eagle Eye may bounce back from here, but personally I think an extra measure of caution is justified at this time.

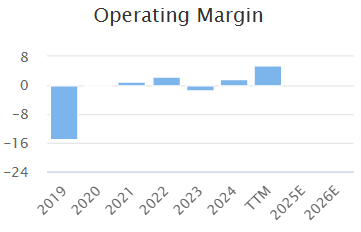

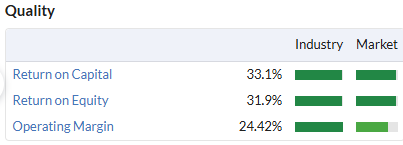

This company's historic quality metrics are fairly weak, perhaps suggesting that its competitive advantages and pricing power are limited:

I’m going to take an AMBER/RED view today due to Eagle Eye's strong net cash position. I’d expect this to provide sufficient headroom to allow the company to recover, assuming its broader competitive position remains unchanged. I also see the cash as evidence that this business has been cash generative in recent years.

However, after two profit warnings in six months, I’d be inclined to wait for some signs of recovering momentum before taking a position here.

ME International (LON:MEGP)

Up 2% to 219p (£823m) - Trading Update - Roland - AMBER/GREEN

ME Group International plc (LON: MEGP), the instant-service equipment group, announces an update on the Group's trading for the six months ended 30 April 2025 ("H1 2025").

Today’s update from this distinctive business looks reassuring and suggests to me that the trends seen last year remain broadly unchanged.

Here are the key points I can see:

Revenue up 2% and pre-tax profit up 14% for H1 - using last year’s H1 results suggests the figures for this year could be approx. £153m and £34m respectively;

Wash.ME (self-service laundry) remains the group’s fastest growing division, with revenue up 13.3%. This is only slightly behind last year’s H1 growth rate of 16.7%;

Focus on laundry growth “at pace”: 590 net new machines installed in H1, on track for 1,200 in FY25;

Photobooth revenue down 3.3%: this is said to be slightly lower than expected, largely due to a technical issue with a new printer that resulted in a 2% drop in revenue. This is now resolved. On track to install 3,200 next-gen photobooths in FY25

Net cash up 69% to £36.2m

Outlook: Full-year expectations are unchanged. The company helpfully includes explicit guidance for pre-tax profit of £76-80m, reiterating its guidance from February.,

The equivalent figure for FY24 was £73.4m, so taking the mid-point of this year’s guidance suggests profit growth may slow slightly this year to c.6.5%, from just under 10% last year.

In fairness, these figures are affected by currency swings, which ME Group says formed a headwind in H1.

It’s also true that ME Group’s profits have historically been weighted to the second half of the year, so there may still be some scope for outperformance.

Roland’s view

This is a distinctive business that has no listed rivals in the UK, as far as I’m aware. The laundry business has been a standout success in recent years and appears to retain strong momentum.

I’d also argue that the company’s photobooth segment (where it has high market share) is a semi-legacy business that’s unlikely to attract new competitors – but could remain profitable for many more years.

While mobile phone cameras have been expected to displace photobooths, it’s not always easy to take suitable photos for passports etc on a phone, even when this is acceptable to the relevant authorities. Using a booth to get a guaranteed result makes sense for many people.

Share price growth has slowed over the last year and I think it’s fair to say that overall momentum may have moderated a little from previous highs:

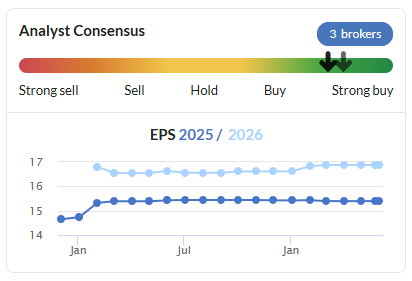

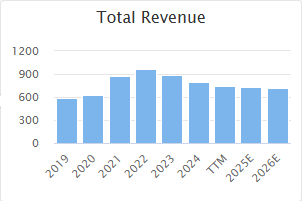

Forecasts have also been stable for most of the last year and seem likely to remain so today:

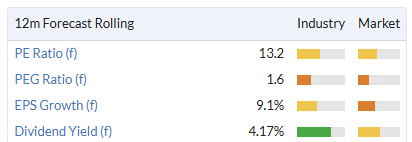

Viewed against this backdrop, I don’t think the shares are obviously cheap at current levels:

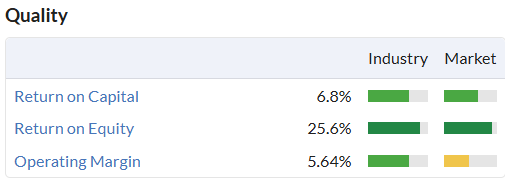

However, ME Group’s quality metrics are outstanding:

This profitability drive strong cash generation and has supported a number of special dividends in the past, in addition to a generous ordinary payout (perhaps a benefit of founder-management). Given the increase in cash, I wouldn’t be surprised to see a further special payout this year.

Based on current consensus, earnings growth is expected to be 8% in FY25 and almost 10% in FY26.

I think this could be enough to allow ME Group to maintain its High Flyer styling and am comfortable retaining our AMBER/GREEN view ahead of July’s half-year results date.

Mark's Section:

IG Design (LON:IGR)

Up 12% to 95p - Disposal of DG Americas - Mark - AMBER

This fairly major news arrived late on Friday afternoon, and it is the complete disposal of their struggling Americas division, which made up about 2/3rd of their revenue. This had been plagued by weak consumer sentiment and the bankruptcy of a major customer, before tariffs made the business in its current form unviable. This is quite a climb down from a business that had big ambitions and was a much-loved growth company before COVID hit:

They made significant acquisitions in order to scale the business in North America with the aim of busting the $1bn revenue point. Something they never quite reached:

Instead, they almost went bust in 2022 as cost increases and extended working capital cycles stretched their balance sheet. A new management team was appointed and, until recent events, was doing a good job of turning the business around until a major profits warning in January saw FY25 adjusted profits slashed from $32m to close to zero.

The buyer is an SPV owned by restructuring specialist Hilco Capital. Here’s what they are paying for DG Americas:

(i) a nominal upfront cash payment of one US dollar; and (ii) 75 per cent of any proceeds (subject to applicable deductions agreed between IG Design Group plc and the Buyer) from the post Disposal sale or realisation of DGA or its assets by the Buyer, to the extent not utilised by the Buyer to provide working capital to DGA (the "Relevant Proceeds Consideration").

The good news is that this appears to be a clean break for IG Design, with no further obligations to the struggling business. Indeed they say

The Board has acted decisively and at pace to safeguard the wider Group from both further financial exposure at a crucial time in the Group's working capital cycle and also the escalating risks of prolonged underperformance.

There are huge capital swings in this business, and while things have been better more recently, the timing here is to prevent the company from having to go into debt to fund Christmas 2025 stock in America, which they don’t know if they can trade profitably:

So this is all about what value Hilco can extract from the trading or assets of DG Americas. The minimum received is zero, as they say:

There is no certainty that any Relevant Proceeds Consideration will be realised, and therefore it is possible that the total amount the Group will receive as a result of the Disposal would be limited to one US dollar. If the Buyer were to own and operate DGA in the long-term, without disposing or otherwise realising DGA or its assets, the Group will not receive any Relevant Proceeds Consideration.

I would imagine that dividends paid would count as a realisation, so while Hilco could just keep and trade the business, it seems unlikely that they would do so without wanting to extract capital or profits eventually. So there are two options, either Hilco turns around the business and IG Design receive 75% of the eventual sale proceeds. Or they sell the assets and return the net proceeds. Let’s look at those options:

Trading Business

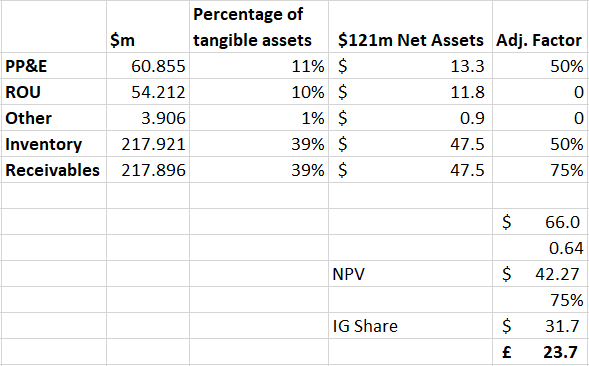

Prior to this year’s news, the company was targeting 4.5% operating margins. DG Americas 2024 revenue was $500.3m, but we know this has declined 13% in FY25. So this would be $19.6m operating profit. Apply a 10x multiple and this could be worth around $200m, of which IG Design would receive their 75% making this worth around £110m, more than the current market cap. There are two problems with taking this figure. The first is any cash Hilco put in to fund the turnaround will be taken off first. But more importantly, any sale of the turned around business will likely be 5 years or more away. If I assume a 20% discount factor to reflect the high risk involved, the NPV of this option is more like £36m based on these options.

Asset Sale

These are the details we get from the RNS:

As at 30 September 2024, DGA had un-audited net assets of $245.4 million, of which intangibles and deferred tax assets comprised $94.0 million.

In such a scenario, intangibles are likely to be worthless. So that is $151.4m of net tangible assets. From this, we know that a customer went into Chapter 11 owing $15m, so that should be taken off. We also know the adjusted operating profit for the group as a whole in H1 was $14.7m and that for the full year, they are guiding break-even even which means a loss in H2, which I think can largely be attributed to DG Americas and will impact net tangible assets. So I would take off another $15m or so for this. So we are down to an estimate of $121m of net tangible assets in DG Americas. The breakdown of this matters.

I can’t see subsidiary balance sheets, but here was the breakdown for the group:

Assuming the assets are in proportion to that of the whole group we can get an estimate of the NPV of the returns from those asset sales, based on some discount factors based on what can usually be realised in a fire sale of assets:

Again, I’ve assumed a 20% discount factor and that the returns will complete in two years, this time. There are a huge number of assumptions in here, and others will assume different figures, but the exercise is still worthwhile.

If I assume a 50/50 chance between these scenarios, my mid-case estimate of the NPV returns to IG Design from DG Americas is around £30m.

DG International

The remaining part of the puzzle is what DG international is worth. In FY24 international made $32.4m adjusted operating profit , which has reduced by 13% in FY25. The outlook for this in FY26 is unclear, but I would assume further worsening of trading conditions in the short term. I’ve also never really liked the adjustments here. Still if we assume $25m and apply a modest 5x operating profit we get around £93m.

The Group

On a simplistic view adding these figures together gets a NPV of £123m which is around £1.25 per share. There is net cash on top of this, but even with DG Americas gone I’m not convinced this won’t be needed to fund DG International’s working capital. There will almost certainly need to be significant cash costs reducing the $8 or so annual central costs. If these can’t be reduced significantly, they will certainly impact the valuation we should ascribe to the remaining business.

The thing that first attracted me to IG Design was the big discount to Tangible Book Value. This sort of situation doesn’t tend to last forever, assets are either made more productive again or end up in the hands of someone who can make them so. The remaining part of the business will have an NTAV of $115.4m or £86.1m, by my calculations or £116m if we assume a NPV £30m for DG Americas is received. This is 118p/share. Note that this will include any cash balances in the asset valuation. The company now trades on 0.81xTBV by my estimates.

Mark’s view

This was one of my 12 stocks of Christmas, which went wrong almost as soon as I wrote about it. A huge profits warning in January wiped out all the forecast earnings that made the stock look reasonable value. The subsequent big sell-off took the stock down to a third of its tangible book value. Doing the maths on the remaining business following this deal shows that this level was simply too cheap, and I can see why the share price has rallied strongly following this announcement. However, there is still a huge amount of uncertainty here. The big questions are how much they will ever get out of the now ring-fenced DG America, and how soon they will receive it. Plus, how much cost they can take out and how well DG International will trade in difficult near-term conditions. While, on balance of probabilities, there is probably a bit of further upside to come here, I have taken the opportunity of today’s rise to exit my position. The reason I invested here was the big discount to TBV, and I’m not convinced that the pro-forma balance sheet has that much of a discount anymore. AMBER is probably about right, until the dust settles and we get a clearer view on DG International trading and group costs.

Anglo-Eastern Plantations (LON:AEP)

Suspended - Final results - Mark - GREEN/AMBER

We’ve not really looked at this on the DSMR recently, although it has appeared on some of my Value screens (or similar companies have), and hence I have written about it a few times. They are an Indonesian palm Oil producer.

The shares are currently suspended due to the results being late:

As a result, the Company expects that its shares will be temporarily suspended from listing and trading from 1 May 2025 until the audit is completed and the 2024 annual report and accounts are published.

This initially confused me, as I’m used to AIM companies having six months to produce audited final results. However, this company is fully listed, which means they only had four months to produce their accounts. Having now released these after hours on Friday, I expect the listing to be restored shortly.

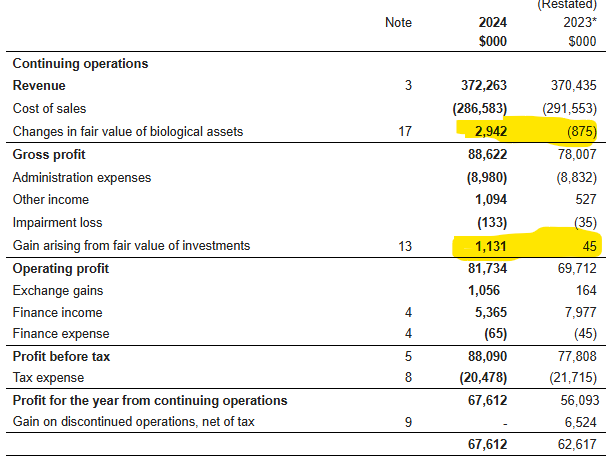

The results themselves are not bad for a company releasing after hours on a Friday! A decline in production was already known via their operations update. However, this has been more than offset by pricing and operational efficiencies, so that EPS has risen by 37%:

There are no forecasts in the market:

Although the YTD share price performance suggests that some investors may have anticipated these strong results:

This may be partly due to the stronger Palm Oil price towards the end of 2024:

Although it is worth noting that this has since retraced.

The 2024 EPS puts them on a historical P/E of 6 on the pre-suspension price, compared to the more popular MP Evans on a historical P/E of around 9. One of the issues has been that Anglo-Eastern have tended to sit on a large cash pile, appearing to do nothing with it. However, these results show an increased commitment to shareholder returns:

Considering the results achieved in the year, the Board has declared a first and final dividend of 51.0 cents per share (2023: 30.0 cents (interim and final)), in line with our reporting currency, in respect of the year up to 31 December 2024. This represents approximately 30% of the retained profits attributable to our Group for the year. The ex-dividend date is set for 19 June 2025.

This works out to be around a 5% yield on the pre-suspension price, slightly ahead of MP Evans at current prices.

It is quite refreshing to see a set of accounts where the management makes no attempt to present adjusted figures. However, in this case, there are a couple of items where investors may want to calculate their own adjustments:

In this case, around $4.9m of the $11.5m increase in PAT from continuing operations was due to factors I would consider one-off.

Cash and investments are up and represent around half the market cap

With no debt, this makes the balance sheet look incredibly strong.

There is little in the way of an outlook. However, this should provide a medium-term tailwind:

To ensure the improvement of yields, our Company has intensified its replanting efforts in recent years. In 2024 alone, approximately 1.7 thousand hectares ("ha") of aged, low-yielding palms were replanted. Looking ahead, AEP aims to replant around 10 thousand ha as part of its 2025-2030 programme, with 2.6 thousand ha identified for replanting in 2025. This initiative, involving the use of higher-yielding and disease-resistant palm varieties, is expected to significantly boost productivity and deliver improved and sustainable returns.

The weaker palm oil price means that any short term increase in profits will be modest, at best.

They are also having a minor rebrand:

In remaining steadfast to evolve and innovate in our future undertakings, we recognise the need for our brand to reflect our evolving presence and inclusivity for diverse stakeholders. To enhance accessibility beyond our English-speaking market, we are rebranding to AEP Plantations Plc, a refined name that reflects our forward-looking vision. Our new name preserves our legacy, values, and identity while reinforcing our dedication to excellence, sustainability, and responsible growth.

It seems that the Anglo-Eastern name is no longer as well-received, and if so, this move looks sensible. However, assuming AEP stands for the original Anglo-Eastern Plantations, then the new name is Anglo-Eastern Plantations Plantations. Perhaps we should be calling it AEP-squared!

Mark’s View

This is a company on a cheap rating, even more so when adjusting for around half the market cap in net cash, and pays a 5% yield (assuming no significant moves on re-listing). The balance sheet is incredibly strong, reflecting a conservative long-term approach by management. However, I can’t help feeling that some of this conservatism is because they have to be to operate a commodity producer in a challenging geographic area. The lack of forecasts and the (until now) reluctance to return cash to shareholders leaves one wondering how interested in shareholder interests the management team actually are. This means that they probably deserve to trade at a discount to their larger listed peer, MP Evans, just not as large a one as they currently do. Roland rated MP Evans GREEN earlier this year on strong broker forecasts, so at least an AMBER/GREEN would make sense here.

See what our investor community has to say

Enjoying the free article? Unlock access to all subscriber comments and dive deeper into discussions from our experienced community of private investors. Don't miss out on valuable insights. Start your free trial today!

Start your free trialWe require a payment card to verify your account, but you can cancel anytime with a single click and won’t be charged.