Good morning! As usual, Tuesday is a little busier than Monday.

1pm: thanks for your patience, the report is finished for now!

Companies Reporting

| Name (Mkt Cap) | RNS | Summary | Our view (Author) |

|---|---|---|---|

BP (LON:BP.) (£74.5bn) | Final Results | Q4 adj. profit $1.2bn, reported loss $2bn after impairments. 2025: upstream production to be lower. | AMBER/GREEN (Roland) [no section below] Today’s 2024 results show profits down 35% to $8.9bn, as expected, due to refining losses. The dividend is held. The real news will come on 26 Feb when BP unveils its plans to “fundamentally reset our strategy”. BP is under pressure to address its sector underperformance and respond to the challenge of activist investor Elliott – see our comments yesterday. |

Bellway (LON:BWY) (£3.1bn) | TU | On track for >8,500 homes (FY24: 7,654). ASP slightly higher £310k. Op. margin to approach 11%. | AMBER/GREEN (Roland) |

Dunelm (LON:DNLM) (£2.0bn) | Interim Results | In line. PBT expectations unch. and in line with consensus (£209m, range £204-214m). | |

PRS Reit (LON:PRSR) (£590m) | Strategic Review | Has received several acquisition proposals above current SP (109.2p), but below NAV (133.2p). | PINK |

RWS Holdings (LON:RWS) (£518m) | AGM Statement | In line with previous guidance, volume growth expected to more than offset price weakness. | |

Warehouse Reit (LON:WHR) (£341m) | TU | Another positive quarter of leasing activity. Transactions 32% ahead of previous contracted rent. | |

PZ Cussons (LON:PZC) (£340m) | Interim Results | Rev -10%, LFL rev +7.1% from pricing. PBT -24%. Adj op margin 10.8%. Trading to end Jan in line. | AMBER (Roland) |

MJ GLEESON (LON:GLE) (£287m) | Interim Results | Rev +4.2% to £157.9m but op profit -42% to £5.1m. ASP +4.8% to £193.9k. In line for FY exps. | GREEN (Graham) No major change here since the H1 trading update but it seems that demand continues to improve. Along with interest rate cuts, this sets GLE up well for a bounce in earnings over the next two years. Market cap fully supported by balance sheet strength. |

S&U (LON:SUS) (£195m) | TU | In motor finance, “we anticipate a recovery in profitability during the next financial year”. | AMBER/GREEN (Graham) |

Wynnstay (LON:WYN) (£65m) | Final Results | Gross profit -1% to £79.2m, PBT -53% to £4.1m. Net cash of £17.2m. Outlook improving. | GREEN (Roland - I hold) After a difficult period, it looks like trading conditions are improving. Good balance sheet, with new CEO keen to improve profitability. |

Time Finance (LON:TIME) (£55m) | Lending update | Hard Asset lending portfolio has topped £100m, delivering 21% YoY growth. | AMBER/GREEN (Graham) Continuing progress and I'm hopeful that we can see the quality of TIME's performance start improving, especially when it comes to ROE. Looking good so far to hit their medium-term strategic targets. |

Hercules Site Services (LON:HERC) (£40m) | Disposal | Loss-making Suction Excavator business sold for £2.4m cash (1.1x NAV), cutting leases/debt by £9m. | |

Checkit (LON:CKT) (£18m) | Merger with Crimson Tide (LON:TIDE) | Recommended all-share merger: 6 CKT shares for each TIDE share. Values TIDE at c.£6.5m, or 99pps. | PINK |

Graham's Section

S&U (LON:SUS)

Down 0.6% to £16.20 (£197m) - Trading Update - Graham - AMBER/GREEN

We’ve been waiting for the regulatory cloud hanging over S&U to clear, and it seems that day is finally approaching.

Today’s update covers the period from the last update (in mid-Dec) to the financial year-end (end of January).

Chairman Anthony Coombs tells us that there now is a positive outlook, thanks to “an easing of regulatory restrictions as the section 166 investigation (the "s166") of last year draws to a close”.

S166 refers to the FCA-ordered “skilled person review” which involves the heavy analysis of a financial firm’s operations.

S&U has long been one of my favourite financial stocks, but I turned neutral on it back in December 2023, when this investigation started.

I then upgraded it to “AMBER/GREEN” in October 2024, when there were initial indications that this business with the FCA might be reaching a conclusion.

Regulatory investigations aren’t good for share prices:

But this morning’s update is one of the most positive I’ve read for some time. Mr Coombs doesn’t hold back when it comes to letting us know how he’s feeling about business prospects, and his mood can shift rapidly - the previous update, for example, was unusually gloomy.

But he seems to think the political climate has changed:

Recent shifts suggest a reassessment of previous consumer-focused measures, addressing concerns about potential constraints on economic growth.

Recent calls by the Prime Minister and the Chancellor for a deregulatory and growth-focused agenda, and their demands from every regulator for specific proposals for these, offer the prospect of a stable and pragmatic framework for financial services. The new zeitgeist is in fact exemplified in the current edition of The Economist magazine where the front cover splashes 'the revolt against regulation'.

He does highlight the Supreme Court’s upcoming review of the Court of Appeal, which we’ve talked about in this report before - do car dealers have a "fiduciary” duty to take care of their customers, and do they therefore need active consent from a customer to allow them to earn a commission for arranging a loan? The courts must decide again.

Rachel Reeves and the Treasury have recently made an intervention on this matter and Mr. Coombs is now sensing a “common-sense” approach:

My view is that even should the Supreme Court uphold the lower courts' decision in principle, any 'harm' found to have been suffered by consumers will be so marginal as to make demands for redress minimal.

Remember that S&U is not exposed to the FCA investigation into discretionary commissions car loans, where commissions might adjust relative to the interest rate charged to the customer.

However, it is exposed to the FCA’s new “Consumer Duty” standard (along with all other financial firms). I don’t believe that S&U will be found to have done anything wrong in terms of how it treats its customers, but that’s just my opinion.

S&U is also exposed to the Supreme Court/Court of Appeal’s judgement on fiduciary duty/active consent. Hopefully, Mr. Coombs is right and this particular risk will fizzle out before long.

With so much regulatory and legal activity going on around the car finance industry, it’s understandable that investors might want to stay away from this sector. However, if you get into the weeds and look at each particular regulatory and legal risk individually, I don’t think that any one of them is particularly dangerous for S&U. But of course it’s impossible to know for sure!

As far as S&U’s financial results for FY Jan 2025 are concerned, I don’t expect them to be good. The FCA put limits on S&U’s collections activities during the year and even with those limits now lifted, they will have made their mark on the company’s results. It will take some time to get collections back to normal.

Mr. Coombs says:

The continuing headwinds at Advantage will be reflected in its profits for the second half year (July 24-Jan 25), but as a result of the improving trends mentioned above in advances and collection rates, we anticipate a recovery in profitability during the next financial year.

Advantage Finance is S&U’s motor finance subsidiary, while Aspen is their property bridging subsidiary.

Aspen has been trading perfectly well, with no regulatory headwinds:

Aspen has enjoyed a record year on net receivables up c.17% on last year at c.£152m (2024: £130m). Collections are up 25% at £157m. Moreover, profits are likely to rise by a remarkable 50% on last year, testament to improving yield and transaction volumes alongside sensible cost control. With demand for residential properties up 13% on a year ago according to Zoopla and with interest rates falling slowly, the stage is set for another very good year.

Starting from zero, Aspen has grown rapidly into a solid business in its own right and has the potential to rival Advantage in its importance to S&U. Aspen’s receivable book is now more than half the size of the receivables book at Advantage (£152m vs. £283m).

Funding: in recent years, S&U has been more aggressive in the use of borrowings to fund growth. However, the need for external funding has eased more recently, and net borrowings have fallen from £206m in December to £192m. S&U’s facilities allow for borrowings of up to £280m.

Dividend: 30p is proposed for the second interim dividend (last year: 35p). There are normally three dividends each year, with the final dividend being the largest.

CFO: a new CFO is joining from Deloitte. The existing CFO retires after 25 years of service.

Graham’s view: I’m very content with my AMBER/GREEN stance on this. S&U is not totally in the clear yet but I believe that the regulatory risk is actually quite mild. I could be wrong about that; we shall see.

Net assets were last seen at £233m; I look forward to updating this figure when we get full-year results in April. So against a market cap of £197m, I think there could be a nice opportunity with this one.

Cheaper financial stocks are available in the market, but this is one of the better ones in my view. And when investors are feeling optimistic, it trades at a premium to NAV, not at a discount.

MJ GLEESON (LON:GLE)

up 1% to 498p (£291m) - Results for the half year - Graham - GREEN

We covered GLE’s H1 trading update last month, and today we have the publication of full H1 results.

I upgraded GLE on that trading update, as we had been AMBER/GREEN on it at higher levels in recent months (550-570p), and I didn’t see the justification for its continued share price weakness. Future rate cuts from the Bank of England were likely going to be delayed rather than cancelled, and so I thought that GLE could be a reasonable pick for patient investors.

Since then, we’ve had unexpectedly dovish commentary from the Bank of England which I think bodes well for GLE and the entire sector.

Today’s results show a “robust” performance.

Revenue at Gleeson Homes is up 10% while the land development division, Gleeson Land, had a quiet period with negligible revenue (£1m). Gleeson Land “is progressing a number of significant opportunities which we expect to complete in the second half”.

At Gleeson Homes, “there are early indications of an improving selling season with much stronger net reservation rates in the first four weeks”.

H1 operating profit has fallen sharply (from £9m to £5m) but this is impacted by the volatility of six-monthly performance at Gleeson Land. More importantly, the operating profit at the homebuilding division was reasonable at £9.1m (H1 last year: £10.2m).

Outlook: as noted above, there are signs of a recovery in demand. Net reservation rates are up, and the Board has “confidence in meeting current market expectations” at both divisions.

Consensus expectations are for PBT of £28m in the current year, with earnings per share of 35.2p.

Singers have published a note this morning with unchanged forecasts. They see adj. PBT rising to £32.8m next year (FY June 2026) and £39.9m the year after that.

Fire safety provisions: a huge issue for other builders, GLE has kept its provisions figure at £12.3m. Hopefully this figure won’t change much.

Graham’s view

I see no reason to change my stance. Homebuilders have benefited from the collapse in inflation (build cost inflation only 1% for GLE in H1) and at the same time they are set to benefit from rate cuts in the periods ahead.

As an affordable homebuilder, GLE strikes me as a lower-risk investment, with potentially more stable demand vs. builders of more expensive properties. The CEO notes that a couple with both earning the National Living Wage can afford to purchase a home in any one of GLE’s developments.

Balance sheet net assets are £297m, fully supporting the market cap.

I think it’s fine for me to keep a positive stance here, given the strength of the balance sheet and the potential for the company to grow its earnings. It’s ideal when there is more than one reason for a share to do well!

The shares are now trading around book value. I could see myself moderating my stance back to AMBER/GREEN if we saw them trading at a meaningful premium. But at this level, I’m fully positive on GLE.

Time Finance (LON:TIME)

Up 1% to 60.4p (£53m) - Lending Portfolio Update - Graham - AMBER/GREEN

Here’s yet another one that we saw already, in January.

Today’s update is about the company reaching a milestone: £100m in its “Hard Asset” lending portfolio.

Hard assets are its strategic focus - lending against vehicles, machinery and equipment. The idea is that loans against these assets are both larger (and therefore more cost-effective) and more secure than other loan types.

The other strategic focus is invoice financing. These two categories - hard assets and invoice financing - are now 80% of TIME’s overall lending portfolio, up from 50% back in May 2021.

CEO comment:

"Growing our lending book is one of the core pillars of our strategic plan and Hard Asset, alongside Invoice Finance, are the two key areas expected to drive this growth. To break through the £100m milestone in Hard Asset is an achievement we are very proud of, and it sets us on a firm footing to achieve our medium-term aim of growing the combined group lending book to £300m by the end of May 2028."

Graham’s view

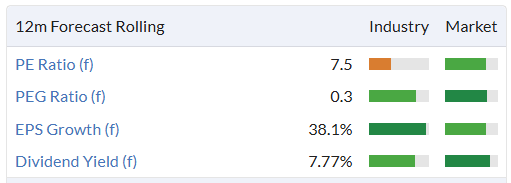

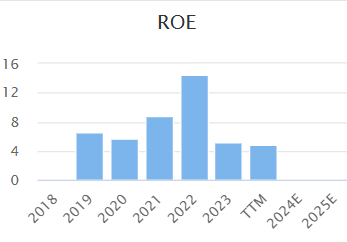

I’ve been AMBER/GREEN on this for a while now as I think that stretching (but realistic) portfolio growth targets could go hand-in-hand with rising profitability metrics in the next few years. ROE in particular has the potential to improve from 7% to the mid-teens - this is a strategic target for TIME and is a level that they achieved in the past.

Health warnings apply - we’ve seen plenty of mishaps with lenders and the smaller they are, the more careful we should be.

But I do like this one and I think it could be worth paying the 9x PER that the market is asking for it. So I’m keeping my moderately positive stance.

The StockRanks are even more enthusiastic than I am:

Roland's Section

Wynnstay (LON:WYN)

Up 9% to 310p (£72m) - Final Results - Roland (I hold) - GREEN

At the time of publication, Roland has a long position in WYN.

Trading in the new financial year is in line with management expectations, and we anticipate an improved performance over last year, helped by the actions we have already taken.

This agricultural supply and merchanting business has been in business for over 100 years. However, it’s exposed to commodity prices, government policy and adverse weather. Many of these factors have combined over the last years and today’s results show a sharp fall in profits.

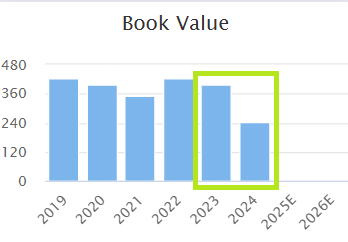

However, Wynnstay has net cash and its shares currently trade at a deep discount to their book value, which the company has reported as 583p per share this morning.

Let’s take a look.

2024 results summary: today’s results cover the year to 31 October 2024 and are the first to be reported under new CEO Alk Brand.

Brand took charge in October and appears to have plenty of experience in the UK food and agricultural sectors. He replaced long-serving CEO Gareth Davies, who had been on leave for a serious family matter since February.

Wynnstay’s business supplying feed, seed and fertiliser means it’s heavily exposed to commodity prices. This means revenue isn’t a primary performance indicator – gross profit is more useful in this regard, in my view:

2024 revenue down 16.7% to £613.1m

Commodity prices accounted for 96% of revenue fall

Gross profit down 1% to £79.2m

Adjusted pre-tax profit down 26% to £7.6m

Net cash exc. leases £32.8m (FY23: £23.7m)

Dividend up 1.4% to 17.5p per share

Trading conditions were difficult last year.

Feed and Grain (adj PBT -88% to £0.7m): wet spring and autumn planting periods led to “the UK’s second lowest harvest on record and reduced the [grain] volumes available for marketing”. Poultry feed volumes also fell.

Fertiliser and Seed (adj PBT +75% to £1.4m): following a difficult FY23, “results were off last year’s lows, but the expected recovery did not materialise”. Farmers are said to have delayed purchases due to weather conditions, while margins were below target levels due to raw material costs.

Depot merchandising (adj PBT +45% to £5.5m): price deflation saw revenue from the group’s retail division fall slightly, but footfall and volumes were in line with the previous year. Margins improvements offset higher energy and labour costs.

“Project Genesis” - restructuring: Mr Brand has lost no time in launching a three-year efficiency programme that the company has named Project Genesis.

It is a fundamental step, which will integrate and streamline operations and establish a lower cost, more efficient operating model. This will enhance profitability and significantly improve the Group's ability to drive future growth and value creation.

The current financial year is expected to see “some early gains” from these changes.

Profit adjustments: Wynnstay’s reported operating profit for the last year was £4.6m, versus an adjusted figure of £7.9m. Personally, I’d normally take a more inclusive view. But in fairness, the non-recurring items (£2.3m) do largely appear to be one-offs, relating to management changes, manufacturing restructuring and the sale of a mothballed feed plant below book value.

Balance sheet & NAV: Wynnstay’s year-end net cash position rose by 38% to £32.8m, excluding lease liabilities. The company reported a stable net asset value of £134.8m, or 583p per share (FY23: 589p).

The increase in year-end net cash was partly achieved as a result of a c.£7m favourable working capital movement. There may be some element of volume in this change, but to a large extent I think it represents the company’s exposure to various commodity and raw material prices. These are normalising after exceptional conditions in 2022 following the Russian invasion of Ukraine.

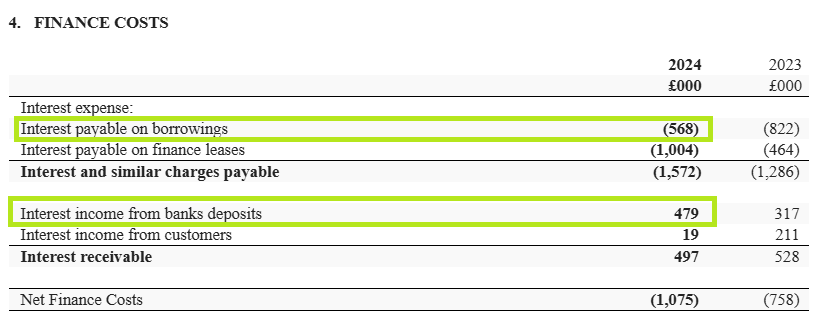

It’s not clear to me how much the cash position varies between the half-year reporting points, but we can see that interest received and interest paid on borrowings was broadly similar last year:

Interest income of £479k would be equivalent to 4% on c.£12m over a year. Wynnstay’s year-end cash balance was £38m. I suspect the reason for this is that the average cash balance during the year is much lower than at the year end, unless it’s getting a poor rate of interest on its bank deposits.

My point is that I don’t think Wynnstay’s net cash should be seen as surplus to requirements. Large working capital movements during the year appear fairly normal (e.g. to fund inventory builds). I believe the business needs a high level of liquidity.

Outlook: the company’s guidance today is positive but somewhat general:

Farmgate prices across most sectors are robust, which will support farmer sentiment despite continuing uncertainties around the transition in governmental support policies.

[The] Group is expected to deliver a stronger performance in FY25 than in FY24, helped by operational improvements already made.

Fortunately, we do have an update from house broker Shore Capital. Many thanks. Shore’s analysts have left their forecasts unchanged today, suggesting FY25 adjusted earnings of 26.9p per share, plus a 17.8p dividend.

These estimates are slightly ahead of the numbers in the StockReport and price Wynnstay on a FY25E P/E of 11.5x, with a 5.8% dividend yield.

Roland’s view

I bought shares in Wynnstay fairly recently, taking the position that there could be a cyclical recovery opportunity here, backed by a strong balance sheet and c.6% dividend yield.

I don’t see any reason to change that view following today’s results. I suspect that the company should also benefit from some external tailwinds over the coming year.

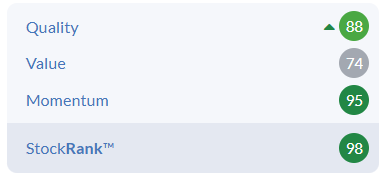

The StockRanks look favourable too:

The new CEO appears to have a commendable focus on improving the base-line profitability of the business. Achieving this could help to justify a higher valuation for the shares – Wynnstay’s recent profitability has been very average, arguably justifying a modest discount to book value:

Risks remain, both internally (due to the scale of change being undertaken) and externally. But Wynnstay’s discount to book value and improving outlook mean I’m comfortable taking a positive view here. GREEN.

Bellway (LON:BWY)

Down 4.9% to 2,438p (£2.9bn) - Trading Update - Roland - AMBER/GREEN

Bellway p.l.c. ('Bellway' or the 'Group') is today issuing a trading update for the six months ended 31 January 2025 (the 'period') ahead of its Interim Results announcement on Tuesday 25 March 2025.

Bellway operates at the mid-upper end of the market. In my view, it’s one of the better quality housebuilders on the London market.

Today’s update appears to be in line with previous guidance given in October’s full-year results:

Full-year completions of at least 8,500 homes

Average selling price of “around £310,000”

Operating margin to “approach 11.0%”

The company admits it didn’t experience the usual “seasonal step-up in reservations during the autumn”, but says that trading levels have improved relative to the weak comparatives seen last year:.

Housing revenue rose by 12% to “over £1.42bn”

Overall reservations up 14.3% to 160 per week (2024: 140)

Cancellation rate reduced to “a normalised level of 14%” (2024: 16%)

Pricing has remained “firm”

Order book at 31 Jan 25 was 4,726 homes (2024: 3,970 homes)

Land purchases: I tend to see land-buying activity among housebuilders as an indicator of sentiment and perceived value in the market.

Bellway appears to have stepped up activity this year, acquiring 5,246 plots across 32 sites during the first half of the year. That is more than the company acquired in the whole of FY24 (4,621) or FY23 (4,715).

Net debt was £8m at the end of January and gearing including land creditors (deferred payments on land purchases) was 4.7%. These figures look fine to me.

Outlook: while Bellway’s full-year guidance appears to remain unchanged, CEO Jason Honeyman does sound a note of caution about market conditions:

While we have been encouraged by a seasonal pick-up in customer enquiries and reservation rates in the early weeks of the current spring selling season, we remain mindful of the sensitivity of customer demand to mortgage affordability and the evolving economic backdrop.

However, Honeyman also takes a more positive tone about changes to the planning system:

The long-term fundamentals of the UK housebuilding industry remain positive, and we welcome the Government's reforms to the planning system to drive a marked increase in the supply of new homes across the country.

There was no comment about fire safety remediation in today’s update. Hopefully this implies that no additional provisions have been required so far this year. Bellway has made £655.5m of provisions since 2017, with £509m remaining at 31 July 2024.

Roland’s view

Investors have reacted unfavourably to today’s figures, but I don’t see anything to suggest this is not an in-line update.

I tend to value housebuilders primarily based on asset values. Bellway reported a net asset value of 2,913p per share with its FY24 results. Assuming this figure remains broadly unchanged, the stock currently trades at a discount of around 16% to NAV.

The shares also offer a forecast dividend yield of 2.5% that’s expected to rise significantly in FY26 if trading improves as expected.

On balance, I think Bellway looks reasonable value at current levels, albeit not extremely cheap. I also wonder if continued spending on fire safety remediation will place a drag on free cash flow, compared to historic performance.

However, given the prospect of lower interest rates and continued volume growth, I think I can justify taking a moderately positive view. AMBER/GREEN.

PZ Cussons (LON:PZC)

Up 10% to 87p (£372m) - Interim Results - Roland - AMBER

Trading has been in line with expectations during the first half of our financial year and, together, three of our priority markets - the UK, Indonesia and ANZ - have delivered solid overall like for like revenue growth of 2%.

This consumer goods group mainly operates in the UK, Australia, Indonesia and Nigeria. It owns a number of well-known brands including PZ Cussons, Imperial Leather and Sanctuary Spa.

I am a former shareholder here but no longer hold the stock, having been scarred by the terrific destruction of value resulting from the devaluation of the Nigerian Naira in FY24. I estimate this has cost the business more than £120m. Unfortunately, PZC was caught with a lot of cash trapped in Nigeria, which was subsequently devalued before it could be repatriated.

This problem is continuing to hold back the group’s performance, judging from today’s interim results covering the six months to 30 November 2024.

Revenue down 10% to £249.3m due to Naira devaluation

Pre-tax profit down 24% to £19.8m

Earnings down 10% to 3.89p per share

Interim dividend held at 1.5p

Trading commentary: outside Africa, PZ Cussons’ turnaround efforts do seem to be making some progress.

Europe & Americas (c.80% UK): revenue up 3.9% to £101m with adjusted operating profit up 67% to £20.7m (20.5% margin). Sanctuary Spa was a key growth driver, with increased distribution and a strong performance over Christmas.

Asia Pacific: revenue down 1.1% to £87.7m with adjusted operating profit down 16.6% to £13.3m (14.9% margin). Indonesia grew strongly with Cussons Baby but was affected by currency depreciation. ANZ was affected by softer markets and industrial action, but Morning Fresh, Radiant and Rafferty’s Garden are said to have taken market share.

Africa: revenue down 33.3% to £60.6m due to Naira devaluation and translation into GBP. LFL revenue growth was 28% despite double-digit volume declines (!), reflecting pricing action to offset high inflation. Adjusted operating profit fell by 36.5% to £8.7m (14.4% margin).

Disposals: management says work remains underway to consider strategic options for the African business and a possible sale of the St Tropez brand. These plans were first mentioned in April 2024.

Profitability: these half-year results show a slight fall in operating margin to 10% (HY24: 11.0%) on an adjusted basis. On a statutory basis, H1 operating margin was just 5.4%.

Balance sheet: more positively, PZ Cussons’ net debt fell to £106.1m (FY24: £115.4m).

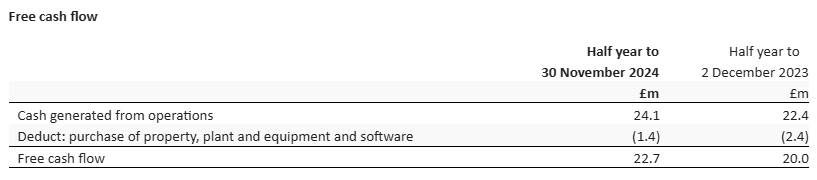

Cash generation: the company reports free cash flow of £22.7m for the half year, but this appears to exclude interest, tax and lease costs.

I don’t agree with this version of the calculation. Using the cash flow statement, I calculate free cash flow to equity of £11.3m (H1 24: £10.8m).

Annualising this prices PZC on around 15 times free cash flow. That seems fair, but not cheap, to me.

Outlook: performance from the end of November to the end of January is said to have been in line with expectations.

However, PZ Cussons has updated its guidance for adjusted operating profit today:

Old guidance: £47-53m

New guidance: £52-58m

Unfortunately, this isn’t due to improved trading. Instead, it’s the result of a change in the way the company accounts for expected foreign exchange losses on intercompany loans in Africa.

In September 2024 we provided FY25 guidance for adjusted operating profit of £47-53 million. This included an estimate, based upon prevailing foreign exchange rates, of approximately £5 million of costs related to FX losses on intercompany loans. These costs, which relate to our Nigerian business and are non-cash, are now treated as an adjusting item.

I am not sure if I agree with the characterisation of these FX losses as non-cash items. Presumably they reflect the decreasing expected cash value of intercompany loans.

However, as a general rule I am not enthusiastic about companies increasing their adjusted profits by simply excluding more costs, cash or otherwise.

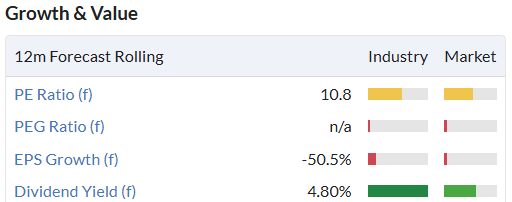

Consensus forecasts on Stockopedia have stabilised recently and suggest adjusted earnings of 7p per share for FY25, putting the stock on a P/E of 12.4:

Roland’s view

If PZ Cussons can manage to scale back its African operations without any further loss of value, I can see that the remaining business could be attractive. The company has some decent brands with double-digit operating margins in markets where it has good scale.

However, the lack of progress with both Africa and the St Tropez sale after nearly a year suggest to me buyers are not queuing up to take these assets out of PZ Cussons’ hands.

In the meantime, I think FX issues and weak trading conditions in Nigeria remain a significant risk, given that Nigeria accounts for nearly a fifth of sales (previously much more).

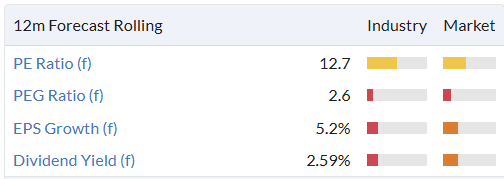

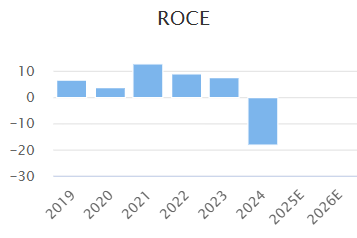

PZ Cussons’ overall profitability has been depressed for a long time:

I can see that this could remain an interesting turnaround situation. But I think I’d need to do some more in-depth work to get a clearer idea of how much more value might be on offer here.

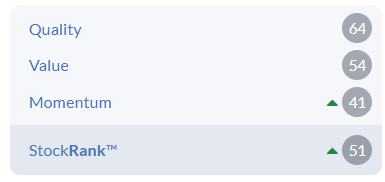

The StockRanks also reflect a neutral view:

Today’s results appear to be in line and some progress is being made. But given the outstanding issues, I can’t get higher than AMBER.

See what our investor community has to say

Enjoying the free article? Unlock access to all subscriber comments and dive deeper into discussions from our experienced community of private investors. Don't miss out on valuable insights. Start your free trial today!

Start your free trialWe require a payment card to verify your account, but you can cancel anytime with a single click and won’t be charged.