Good morning, it's Paul here.

I had a few technical problems getting yesterday's article to update, so have decided to start with a new article today, with the backlog from yesterday.

Timings for today - I'm not sure at the moment. In all likelihood the remaining backlog from yesterday might have to wait until this evening, or tomorrow morning.

Goodwin (GDWN)

Share price: 3480p (up 1.5% at close yesterday)

No. shares: 7.2m

Market cap: £250.6m

This is an engineering group. Several readers asked me to look at it yesterday. Unfortunately, the section I wrote yesterday disappeared when I updated the article, so am having to write it up again now.

Results for FY 04/2019 look solid:

- Revenue up 1.8% to £127m

- Pre-tax profit up 11% to £14.7m - note the decent profit margin of 11.6%

- Diluted EPS of 150p - giving a PER of 23.2 - that looks very pricey compared with Castings, which I looked at yesterday, on a PER of about half this level.

Outlook - this is the exciting bit. There's been a huge increase in the order book, with more in the pipeline:

Furthermore, I am also delighted to confirm that we have seen a significant rise in the level of sales order input within our Mechanical Engineering Division. Whilst some individual elements would not be notifiable the aggregation is significant for the Group. With this exceptional input, I am able to confirm that, at the time of writing, the Group order input since the start of the new financial year stands at £93 million and the total forward order book stands at a record £165 million (July 2018: £85 million), a 94% increase from this time last year, with yet more large long-term contracts, that we have been targeting over the past few years, still to be placed.

That sounds tremendously positive. I wonder what's driving it? At a guess, cheap sterling must be boosting things. Weak sterling is reported on the news as being something terrible, but of course it's positive for UK producers & exporters, making them more competitive.

Here are my notes from reviewing the results today;

- Very positive commentary & outlook

- Capex heavy

- Capitalised development spend of £1.5m - not very much

- High inventories - but £5m due to unwind. Still high though

- Balance sheet OK, but weaker than Castings (CGS)

- Big fall in cash generation compared with last year

- Reduced reliance on petrochemical industry

- Some debt on balance sheet, but looks OK relative to profits/cashflow

My opinion - I can see why readers like this, and asked me to review it - because the outlook comments, and large increase in order book, suggest that profits could rise strongly in future.

Which is better, Castings, or Goodwin? On balance, I'm more drawn to Castings, as it's much cheaper & has such a strong balance sheet. Although Goodwins seems to have much more exciting potential for growth - which is priced into the shares.

Weak sterling means that these UK businesses have quietly been getting a lot more competitive of late.

Eddie Stobart Logistics (ESL)

Share price: 71p at close yesterday - suspended from 07:30 today

No. shares: 379.3m

Market cap: £269.3m

Directorate change, company update & suspension

Eddie Stobart Logistics plc, a leading UK end-to-end supply chain, transport and logistics group...

EDIT: NB. please note that this announcement relates to ESL. There is another UK listed company called Stobart (STOB), which owns 11.78% of ESL, according to ESL's website here. So it's a bit confusing.

Sounds like very bad news. To summarise:

- CEO standing down with immediate effect

- Replacement CEO being promoted internally

- Accounting problems have emerged;

As part of the Group's review carried out in conjunction with the Group's auditors in relation to the interim results, the Board is applying a more prudent approach to revenue recognition, re-assessing the recoverability of certain receivables, as well as considering the appropriateness of certain provisions.

While revenue expectations for the first half are broadly in line with previous guidance, the full impact of these items on Adjusted EBIT is unclear, but it is likely to be significantly lower than anticipated at the time of the Half Year Trading Update on 9 July 2019.

As a result, the Board also intends to review the Group's current dividend policy.

Suspension - normally an announcement like this would probably hit the share price by perhaps 50-75%, in my experience. That's not possible in this case, as the shares are being suspended, pending clarification of the financial impact.

Accounts delayed - but not by much. Interims (6m to 31 May 2019) were due out on 29 Aug 2019. This will be delayed until "early September".

Outlook - management say they are confident:

The Board has full confidence in the ability of Eddie Stobart's management team to deliver an improved performance for the Group going forward, and remains confident in the strength of the underlying business.

My opinion - I've not looked at this share before. Looking back, its trading update on 9 July mentions accounting adjustments being required, but unrelated to what has been disclosed today.

I've had a quick look at the last reported accounts, and don't like what I see. The balance sheet is weak, with £312m intangible assets. Eliminate those, and NAV of £236m becomes NTAV of minus £76m.

Net debt was last reported at £154m, at 31 May 2019.

We've seen before (e.g. Staffline), how companies with stretched balance sheets (i.e. too much debt, and negative NTAV), which uncover accounting problems, may not have any safety margin to ride out the problems. That might trigger the bank losing confidence, possible breach of covenants, and an emergency fundraising being required.

This looks pretty grim to me. I hope none of our subscribers here hold this share.

Entertainment One (ETO)

This is getting ridiculous! Yet another takeover bid.

US-listed Hasbro is buying ETO for £3.3bn, or 560p per share. That's a 26% premium to last night's close.

With so many bids occurring, for decent-sized companies, it's difficult to avoid concluding that UK listed shares might be too cheap. Or at least some of them.

Stilo (STL)

This is de-listing after many years on the UK stock market.

It's absolutely tiny, both in terms of mkt cap (£1.65m), and revenues/profit. So a listing never made sense. It's looking at doing a tender offer for some shares are 1p.

It mentions lack of liquidity in the shares, and costs of "at least" £120k p.a. Clearly that is money wasted.

I think this is a good opportunity to review any micro caps which we might have languishing in our portfolios. Does it make sense for them to remain listed? If not, then a de-listing announcement could clobber the share price.

D4t4 Solutions

Share price: 230p

No. shares: 40.24m

Market cap: £92.6m

AGM Statement (trading update)

This update relates to trading for the year to date, FY 03/2020. I wish the company would explain its activities more clearly. As far as I can tell, it sells software & services relating to data management.

I last reported on D4T4 here in June, with a quick look at its results for FY 03/2019 (Financial Year ended 31 March 2019, for anyone not familiar with my abbreviations!). These figures were excellent, and I liked the share, concluding that it was good, and reasonably priced given the strong profit growth.

The update yesterday seems to be in line;

D4T4 entered the current financial year (ending March 2020) in robust shape, and I am pleased to say that the business is continuing to trade well and in line with our expectations ...

H2 weighting - a bit of a fly in the ointment here;

Reflecting the timing of anticipated contract wins, we are expecting some second half bias to the year overall though this is not expected to be as pronounced as that experienced in the year to 31 March 2018...

Taking a look back, this was how FY 03/2018 turned out;

H1: Rev £4.8m Adj PBT -£0.4m

H2: Rev £13.6m Adj PBT £4.5m

As you can see, that was a massive differential between H1 & H2 trading. Actually, I would have expected a considerably greater difference in H1/H2 profits, on that very weak revenue in H1, so I suspect the CFO might have done some smoothing of the numbers to be able to report only a small loss in H1.

Last year, the seasonality actually reversed, with H1 being the stronger half at £3.4m adj PBT, and H2 softer at £2.6m adj PBT.

Therefore, there does not appear to be a seasonal pattern, but a more random result dependent on what contracts they happen to win, and when. This makes it difficult to predict how future results might pan out, and therefore increases risk of an unexpected profit warning.

Healthy pipeline - this is reassuring;

However, with a growing and healthy pipeline of new business opportunities together with a range of opportunities with existing clients, the Board remains confident regarding progress during the rest of FY20 and beyond."...

"We continue to remain positive about the outlook and look forward to providing updates on contract wins and at the time of the interim results in late November."

Brexit/forex risk seems low, even favourable;

A large proportion (greater than 80 per cent.) of our business is dollar-derived and this gives us some protection from current Sterling weakness."

Surely it gives more than "some protection", but should be actively boosting margins, if revenues are in dollars, and costs in sterling?

My opinion - lumpy contract wins seem to be an unavoidable part of the business model with this company. Therefore the risk of missing forecasts because large contracts may not be signed by the year end, is just something shareholders have to live with.

On the upside, the problems in FY 03/2018 of a very weak H1, with management assurances that H2 would be much stronger, turned out to be fine. Therefore I feel that management gained credibility from that episode - i.e. by giving an accurate steer in the past, I'm now more prepared to rely on management assurances now & in the future.

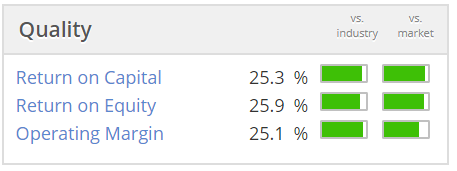

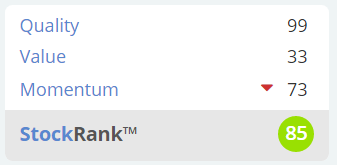

The quality scores look great;

The forward PER of 16 looks reasonable, especially considering that there's plenty of cash on the lovely balance sheet. Shareholders get a modest, but well-covered dividend too. I reckon there's plenty of scope for divis to be increased in future too. Or maybe some bolt on acquisitions using the surplus cash pile? There are lots of small companies in this space that might make a good fit.

Current forecasts are for only modest earnings growth, given last year's large increase. There's a 1-pager update note, available on Research Tree. That shows 14.2p EPS for this year - a PER of 16.2 .

Coincidentally, I went to a briefing last week on digital marketing. It really dawned on me that data is now incredibly important for companies, large and small. Therefore, I feel D4t4 operates in a sector that it makes a lot of sense for investors to have some exposure to. Therefore, whilst accepting there is some risk over the H2 weighting, this share gets a thumbs up from me as a potential long-term buy & hold - I'd categorise this share as QARP (quality at reasonable price).

It's the sort of share that I could see rising maybe 10-25% once we have some clarity on Brexit.

Sopheon (SPE)

Share price: 815p

No. shares: 10.16m

Market cap: £82.8m

Sopheon plc, the international provider of software and services for Enterprise Innovation Management solutions, announces its unaudited half-yearly financial report for the six months ended 30 June 2019 together with a business review and outlook statement for the second half of the year.

Background - Sopheon issued a profit warning, which I covered here on 24 July 2019 here. Delayed contract wins meant that H1 figures were anticipated being down 14% on H1 LY, at $13.7m revenues, and EBITDA roughly halving on H1 LY to $2m. (note the Sopheon reports in US dollars).

The reason for the anticipated poor H1, was down to contract delays. The outlook comments were very positive for the full year.

H1 results - revenue is indeed $13.7m, and EBITDA has come in better than expected at $2.5m.

Outlook comments - the latest commentary remains very upbeat;

The underlying market and commercial momentum is increasing. Expanded sales resources have contributed to a 48 percent growth in sales pipeline value between January and June, expected to drive a strong second half weighted revenue profile.

Both the volume of deals and the number of larger deals in the pipeline have risen to all-time highs.

Revenue visibility - is still down on last year, but this should rise as more contracts are won in H2;

The proportion of SaaS business in the expanded pipeline has risen sharply, potentially accelerating our desired transition to a higher recurring revenue model and greater lifetime customer revenue.

Revenue visibility2 for full-year 2019 is now at $25.4m (2018: $27.2m).

This is the same quandary that many software companies are experiencing now. SaaS, recurring revenues are great longer term, but the transition is painful in that it suppresses short term revenues & profits compared with licence deals (that are all up-front profit, but one-off in nature).

Outlook comments remain very upbeat;

Sopheon's Chairman, Barry Mence said:

"The future prospects of the business have never been brighter, and we do not believe this first half pause in the impressive financial performance of the past several years has a bearing on Sopheon's unique potential and growth opportunity.

The business remains profitable and cash generative, and our balance sheet is stronger than ever.

With unprecedented activity and higher value in our sales funnel, we continue to anticipate rising deal flow and traction through the balance of the year.

We see the shift to SaaS as reflective of a change in procurement behavior, and not a change in commercial momentum, which is rising.

The Board believes that this development will drive shareholder value and remains confident that Sopheon is well positioned to build on its leadership position in the new and exciting space of Strategy Execution management."

Balance sheet - very good, including $18.7m in cash. No issues at all, this looks a soundly-financed business.

Valuation - current forecast for FY 12/2019 is EPS of 42.7 US cents per share, which is a big all on last year's 61.2 cents. Converting the 2019 forecast into sterling (at $1.23 = £1) gives 34.7p EPS, for a PER of 23.5.

Why would we rate a share on a high PER of 23.5, when earnings are forecast to fall by 30% against last year? Clearly the reason is that investors believe that the 2019 forecast is a blip, and that earnings should rise strongly in future.

Forecast for FY 2020 is for strong recovery in EPS to 59.6 US cents. that's 48.5p, for a 2020 PER of 16.8 - much more reasonable.

My opinion - I remain neutral on this share.

I'm impressed with the company's performance in recent years, and on the balance of probabilities, the weak H1 this year does sound like a blip, rather than a more permanent downturn. So I completely understand why a lot of shareholders are happy to give the company the benefit of the doubt - which is what the current share price is saying. It would be a lot lower if investors thought the company had a more serious problem.

The balance sheet is very secure, so there's no solvency risk.

Recovery already looks priced-in, therefore I don't personally want to take a position here. If H2 goes well, and the strong pipeline delivers good contract wins, then the share price would probably be back up into 4 digits (over 1000p). If H2 disappoints, then I think it could be going back down to 400p. A recovery in H2 looks more likely than a further deterioration, therefore the market is probably pricing risk:reward here about right, at 815p per share.

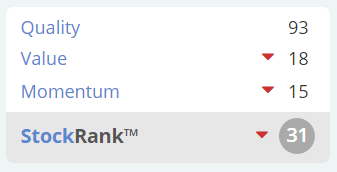

The Stockopedia StockRank system is warning us to be careful;

To finish off, here are some brief comments on the 2 remaining stocks outstanding from last week;

Macfarlane (LON:MACF) -

(I'll do this later on Saturday, or possibly Sunday. Markets are shut anyway, so there's no rush)

See what our investor community has to say

Enjoying the free article? Unlock access to all subscriber comments and dive deeper into discussions from our experienced community of private investors. Don't miss out on valuable insights. Start your free trial today!

Start your free trialWe require a payment card to verify your account, but you can cancel anytime with a single click and won’t be charged.