Good morning! I'm joined by Roland today, who's come in to help with some backlog items from yesterday, thanks Roland!

Today's report is now finished. Have a lovely weekend!

Explanatory notes -

A quick reminder that we don’t recommend any stocks. We aim to review trading updates & results of the day and offer our opinions on them as possible candidates for further research if they interest you. Our opinions will sometimes turn out to be right, and sometimes wrong, because it's anybody's guess what direction market sentiment will take & nobody can predict the future with certainty. We are analysing the company fundamentals, not trying to predict market sentiment.

We stick to companies that have issued news on the day, with market caps up to about £700m. We avoid the smallest, and most speculative companies, and also avoid a few specialist sectors (e.g. natural resources, pharma/biotech).

A key assumption is that readers DYOR (do your own research), and make your own investment decisions. Reader comments are welcomed - please be civil, rational, and include the company name/ticker, otherwise people won't necessarily know what company you are referring to.

Agenda/Summaries

We managed to cover everything today!

Paul’s Section:

Watkin Jones (LON:WJG) (I hold)

110p (last night)

Market cap £281m

Graham reviewed the nasty profit warning here in Oct 2022, which clobbered the share price to an all-time low of 82p. It’s since bounced to c.110p, but remains well below the pandemic 2020 low point of 134p (in Nov 2020). Note that WJG has not diluted shareholders, with a share count almost static at c.256m shares, since it floated in 2016 - a common trait of family-owned/controlled companies, which tend to jealously guard themselves against dilution, and tend to also operate with a long-term focus, and sound balance sheets - which are good reasons as to why many value investors congregate in family/founder-run companies. They often out-perform, although that’s subjective, I don’t have any data to prove it (maybe we should do a study of this, if anyone has a few hundred hours of spare time?!)

Share price since it listed on AIM, plus there have been decent divis on top -

Anyway, I scraped up some cash, and bought a few near the recent low, and have since topped up to, so I’m declaring my interest because that’s bound to not be unconscious bias, but conscious bias - I think the company is good, and the shares good value, so that's why I put some of my own money in them recently.

On to the most recent news -

Results FY 9/2022 (announced 25 Jan 2023)

The profit warning in early Oct 2022 was due to the impact of higher interest rates making institutional clients more cautious, and political/economic turmoil causing the sale of 2 projects to be delayed. It also reported “some pricing and margin softness”. Guidance was revised from adj PBT of £55m, to £49m - hardly a disaster, and the share price plunge looks overdone.

WJG sold 8 developments last year, so this business model of big, lumpy projects, is always going to come with some risk of project delays around period ends, investors just have to accept that, and management need to maybe be more prudent in their assumptions at a time of increased uncertainty & higher interest rates (which have changed the economics of property investment projects for the institutional buyers).

WJG mainly builds student accommodation, but also build to rent (BTR) projects for wider occupation. These are pre-sold to institutional buyers, thus nicely lowering risk compared with many other construction companies.

Actual results now show £48.8m adj PBT, so that’s in line with expectations, near enough. Although note the statutory PBT figure is much lower, at £18.4m, due to a £30.4m exceptional charge for remedial work under the new Building Safety Act, which seems to particularly apply to tall, residential buildings (which is what WJG builds), in response to the Grenfell tragedy.

The worry for shareholders might be that further increased provisions might be needed - it seems to be the case that initial estimates for complex liabilities generally, are usually too low. That’s a bear point for this share. Notes 4 & 12 give more detail, and worry me considerably. An initial estimate of a liability arising from 30 years’ building projects, where the situation is complex and fluid - sounds like a can of worms to me. But the costs will be spread over probably many years, so I doubt this would prove an existential crisis, but might limit the future ability to pay generous divis, if the situation does deteriorate. Something to keep an eye on, for all builders that are impacted by the new law.

Using the adjusted numbers, EPS is 14.8p, and the divis are 7.4p for FY 9/2022 (policy is 2x earning cover), so that’s a PER of 7.4, and yield of 6.7% - very attractive valuation metrics, but it stands to reason that we’re likely to see lower earnings/divis in the new year, and possibly in 2024 too? I’m generally assuming that peak earnings have passed for cyclical companies, and investments have to stack up on reduced earnings. Although it’s always worth remembering that we’re not just buying 2023 earnings, we’re buying all earnings forever. So a low PER, on low earnings, could be a long-term bargain, as the future earnings, and the multiple they're valued on both improve. That's what always happens in bull markets.

Balance sheet - looks really healthy to me.

NAV is £177m - down nearly £8m on LY, mainly due to the big increase of £21m in “Provisions” within non-current liabilities - this will be the bulk of the remedial work required by law, referred to above. There’s also a smaller element of this in current liabilities.

The only adjustment I would make to the balance sheet, is to remove £12.2m of intangible assets, which gives us NTAV of £165m. This includes net cash of £82.5m (cash: £110.8m, less £(28.3)m interest-bearing loans).

The market cap is £281m, so this means NTAV constitutes 59% of the market cap, which is decent tangible asset backing. Not as good as the housebuilders, but that’s fine because WJG has a different business model, which places less reliance on a big land bank, and its projects are forward-sold to institutions, rather than being sold piecemeal to the public.

Overall then, this is a very safe balance sheet, in my view.

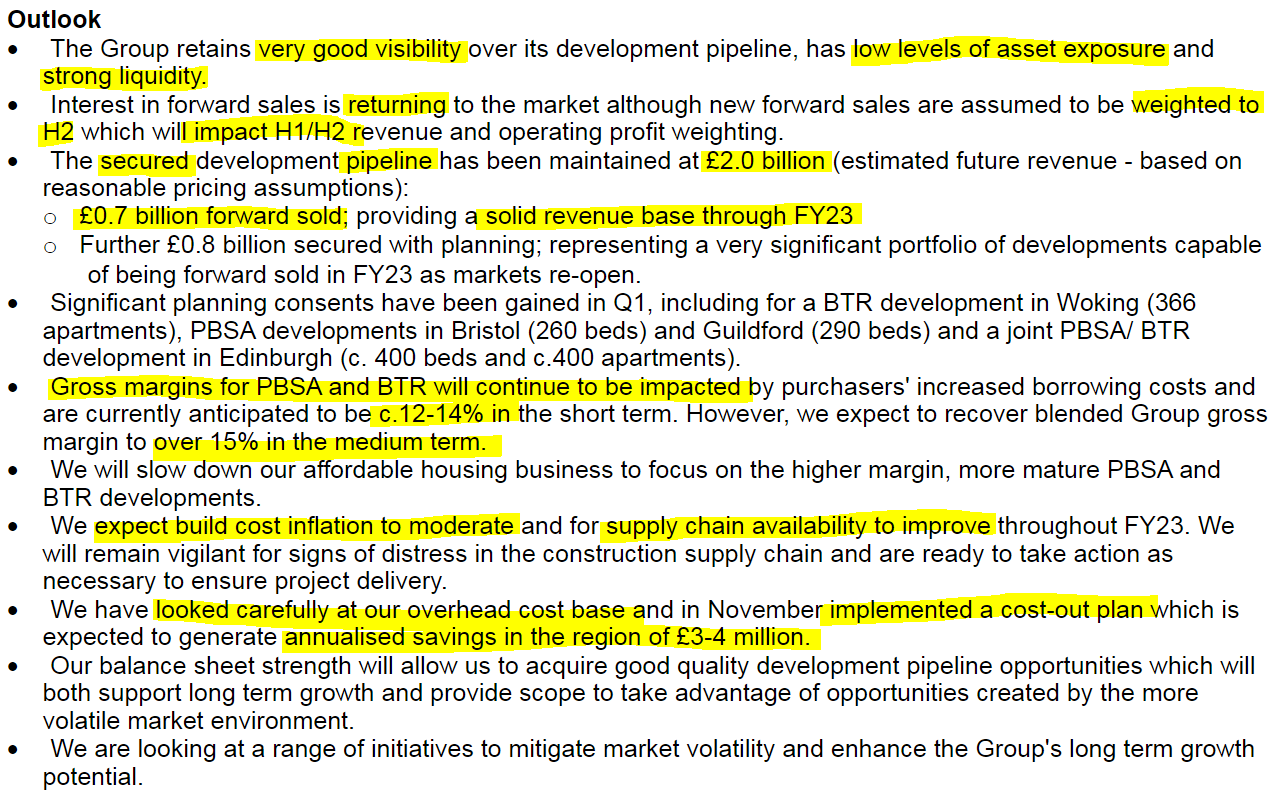

Outlook - there’s so much useful detail, I’ve taken a photo and made it more colourful -

Broker forecasts - nothing available on Research Tree unfortunately. Management needs to address this, as private investors need some help with research notes, and we’re the people who create the market liquidity, and hence set the share price.

EDIT: a new note from Progressive has just come through. Jolly good.

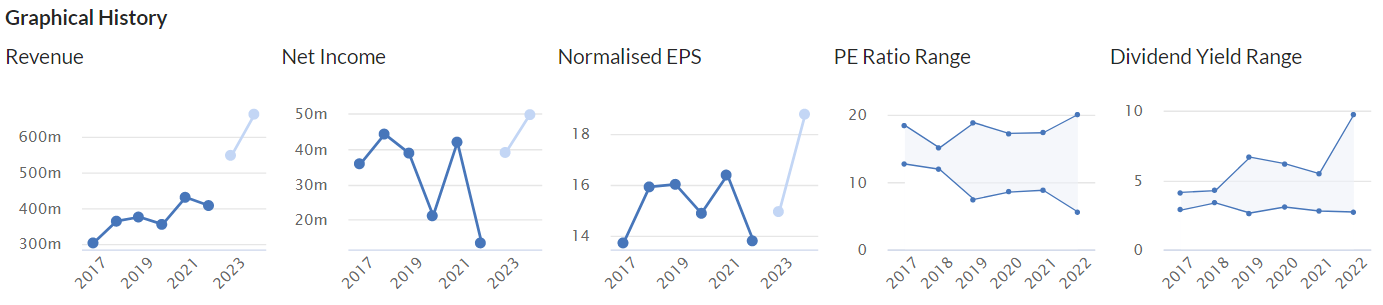

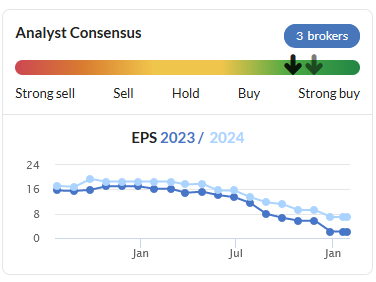

Stockopedia’s wonderful little graph shows us the trend below, with 5 brokers contributing -

I’ve sense-checked these forecasts, and I’m worried they’re possibly not cautious enough yet, given that historic EPS was 14-16p (based on the same number of shares, there’s not been dilution remember) see below -

There’s a recording of the video (with slides) results webcast here.

My opinion - I’ve bought some shares outright (am not using gearing any more for my main portfolio), hence am happy to just keep them for the duration - ie. several years. I think the current price looks attractive based on current fundamentals, taking a longer term view. The facts will change over time of course, as with everything. The period of zero interest rates would have undoubtedly stimulated demand, which might permanently reset at a lower level, thinking through the downside risk.

Also, I think it’s prudent to assume that legal provisions are more likely to increase, than decrease.

Overall though, I think the share price has already factored in so much downside, that it’s probably overshot too low. Hence there’s the chance of a shorter term recovery in price, plus a longer term re-rating once the economy is improving again. Plus there’s always going to be demand for this type of accommodation, due to the structural shortage of housing in the UK. I would like to see many more co-living spaces, for younger, and single people, which are much more social ways to live, eg in city centres. WJG has great experience & expertise, relationships with many institutional investors, etc, which give it a big advantage, and a barrier to entry for competitors.

Thumbs up from me, but it could be a bumpy ride, with another profit warning distinctly possible as 2023 develops.

On Beach group (LON:OTB)

190p (up 9% at 09:45)

Market cap £317m

We were discussing this online holidays company back in the autumn, with readers and I agreeing that it looked cheap at 95p. Here we are just a few months later, and it’s doubled, which is a considerable surprise! (well done to holders).

Holiday shares seem to be very strong at the moment, and I noticed that easyJet (LON:EZJ) recently announced strong trading too. Cruise operators have also been announcing strong bookings lately, helping to drive a strong recovery in share price at Saga (LON:SAGA)

OTB gives us an update for FY 9/2023 so far.

Key points -

Q1 (Oct-Dec 2022) - bookings up on prior year

Q2 so far - bookings “materially increased”

Overall bookings up 68% against last year - that is impressive, although I’m not sure how that would translate into revenues.

Higher costs (now known as “investment”) to drive sales growth.

Claims to have a strong balance sheet (checking the last one, it’s pretty good, with NTAV of £82.5m, and I like that client cash is held separately in a trust account).

The glaring gap in this announcement is obviously nothing said about what matters most (profitability). So investors are left scratching our heads, is this in line with expectations, or are they avoiding saying that for a reason? A badly written trading update then.

I can’t find any broker notes either.

Looking at consensus forecasts, they were reduced last autumn, so with bookings up so strongly, it looks as if the market might be expecting a beat against these forecasts below? -

My opinion - neutral, as I don’t have enough information.

Although given very strong bookings growth, it seems reasonable to assume EPS might end up nearer the 20p level that was being forecast before the cost of living crisis began. If that’s right, then 190p share price looks good value still, at 9.5

It might not get there in one go, but even if broker consensus of 12.2p is achieved for FY 9/2023, then the PER would be 15.6 - probably priced about right.

So valuation depends on whether you think it’s likely to meet, or beat forecasts. Either way, the doubling of share price in the last few months looks a fairly solid move, backed by fundamentals, although some people are bound to start banking their profits I imagine.

Superdry (LON:SDRY)

121p (down 19% at 12:02)

Market cap £99m

I need to get up to speed on Superdry, in time for the IMC webinar, which starts shortly at 13:00. Although what I have learned from previous webinars, is to take the permanently upbeat commentary with a pinch of salt. It seems to be more about what they want & hope is happening, rather than necessarily what is or will actually happen!

Superdry announces its Interim Results covering the 26-week period from 1 May 2022 to 29 October 2022 ("H1 23") and a trading update covering the 9-week period from 30 October 2022 to 31 December 2022.

H1 results look poor - some key numbers -

Revenue up 4% to £287m

Weaker gross margin, at 52.1% vs 55.2% LY. This seems low, but bear in mind that it’s a mix of retail (high margin) and wholesale (lower margin). Stores generated a good 68% margin in H1. Online was 58%, and wholesale 31% (down heavily from 38% LY).

Adj loss before tax was £(2.8)m in H1 LY, and worsened to £(13.6)m this year’s H1.

The statutory H1 loss was £(17.7)m.

Under-performance in H1 blamed “mainly” on wholesale (revenues down 18% YTD, and down 57% in the most recent 9 weeks). It’s strange to see product that’s selling well in the stores, not selling well to wholesale customers, so I’m perplexed by this. Although wholesale orders would be for the next season, so maybe that’s not resonating with customers - which could be an advance warning of softer retail sales in the spring of 2023 maybe?

Wholesale has proved more challenging with revenue down 18.0% year-to-date, in part driven by the impact of shipment timings, some of which will reverse in the second half. However, there is still a Covid-related confidence lag in Wholesale, which we expect to close as our partners see how successful our AW221 range has performed through our own channels, giving them confidence to buy for future seasons.

“Adjusted other gains and losses” stands out, at a large £23.4m overall gain, of which £17.2m is a forex gain. This seems to be telling us that excluding these gains (assumption being that they’re one-offs) would have meant an underlying trading loss of £37m in H1, which is rather alarming. Forex gains seem to have heavily cushioned a bad performance in H1.

Outlook - guidance for FY 4/2023 is lowered to a small loss -

...we are mindful of the challenges facing the consumer as we head into 2023 and remain very cautious about the potential for a soft spring. s a management team we are taking action to seek costs savings initiatives to support our performance. When combined with current margin run-rates and the underperformance of our Wholesale division, we believe it appropriate to amend our adjusted profit before tax guidance to broadly breakeven (previously £10 – 20m).

Balance sheet - is burdened by a large deficit on IFRS 16 lease entries, suggesting that SDRY still has plenty of serious problems in its store estate, with loss-making sites. That could be a tailwind though, as those leases gradually disappear on expiry. But for now, it will be a nasty headwind on trading and cashflow.

Inventories & receivables have gone up, and look too high to me, but the balance sheet is at Oct 2022, which would be when inventories were high for seasonal peak trading season ahead..

Net debt was £38.0m at Oct 2022, but has since reduced to £9.8m at Dec 2022, the usual seasonal pattern.

SDRY came close to the edge when its existing bankers didn’t want to renew the facilities, but it managed to replace them with more expensive specialist debt providers. A close shave for sure, but at least that issue was resolved satisfactorily.

Accounting problems - as mentioned here in the past, SDRY’s Annual Reports are dripping with problems going back years re its accounting department, which seems to have been a complete shambles. To see what I mean, check the archive here, or have a look at the Annual Reports (which are full of useful info that most investors never look at!)

My opinion - there’s no sign of Dunkerton’s brand reset delivering tangible results in the numbers. There are red flags with SDRY, in particular - multi-year negative disclosures in the Annual Reports re sloppy accounting. Also the underlying H1 loss (excluding forex gains) seems to have been much worse than the headline loss. H2 guidance reduced to breakeven, but stripping out the forex gains, it’s actually a significant loss. Big deficit on the IFRS 16 lease entries, which indicates there are heavily loss-making stores in the estate.

Overall, I’m on the fence. This share could go either way - it wouldn’t completely surprise me if the business were to go under at some stage. It’s incredibly difficult to make any money in the mid-market fashion sector, unless you’re Next (LON:NXT)

If Dunkerton does pull off his brand reset, then this share could be a good riser. At £99m market cap currently, the upside could be a 2-3 bagger perhaps? The trouble is, today’s update doesn’t give me any confidence the upside case is likely to play out any time soon, but who knows - it all depends on the product - it’s fashion, so the fashions have to be right every season. I’m still scarred from Joules, which showed that a couple of bad seasons can bankrupt the company, even when it has only a little bank debt. Hence I don’t really want to get involved in any fashion businesses right now, unless there’s a bulletproof balance sheet with plenty of net cash.

It might be far less glamorous than SDRY, but little Quiz (LON:QUIZ) is performing better than SuperDry, and has half its own market cap on the balance sheet as net cash.

The only other small cap fashion retailer that strikes me as any good is Sosandar (LON:SOS)

In this sector, I’d be more inclined to go mid-cap, with JD Sports Fashion (LON:JD.) And Next (LON:NXT) standing out as particularly good, and reasonably priced. Frasers (LON:FRAS) is another one to consider.

EDIT: a very interesting webinar was held. Worth a watch.

Roland’s Section:

Strix (LON:KETL)

100p (+10% on Thursday)

Market cap: £218m

Shares in kettle control manufacturer Strix bounced 10% after yesterday’s trading update. This company makes the component that ensures kettles switch off automatically when the water reaches boiling temperature.

The shares have now risen by 25% since November’s profit warning (which Paul covered here), but on a one-year view the picture is still pretty bleak.

2022 results guidance: Management expects to report an adjusted after-tax profit of £23m for 2022. That’s in line with the guidance given in November, when Strix said that China lockdowns and wider geopolitical uncertainty had caused significant disruption to sales.

To put the scale of this drop in context, previous years’ profits were £31.4m (2021) and £29.5m (2020).

This week’s update implies a P/E ratio of around nine times 2022 earnings. That could offer value, if the company’s recovery proceeds as expected.

Profit margins: I’m concerned that Strix’s formerly strong profitability may have suffered a lasting hit. Using the firm’s past results and consensus forecasts, I’ve calculated Strix’s adjusted net profit margin from 2020 through to 2023:

2019: 29.8%

2020: 31%

2021: 26.3%

2022(fc): 20.7%

2023(fc): 17.2%

However, gross margins have remained fairly stable at around 40%, so my guess is that this falling trend reflects the expansion in the group’s cost base – probably due to acquisitions and the construction of a new factory.

Acquisitions: One problem with Strix’s core kettle control business is that with a global market share of over 50%, growth prospects are limited. To try and overcome this issue, Strix has been diversifying into areas such as hot water taps and water filtering.

What’s not yet clear to me is whether these acquisitions will be able to deliver the kind of steady profitability and cash generation that I’ve admired in the core kettle controls business. I’d like to see a bit more segmentation in the firm’s results so that we can understand this.

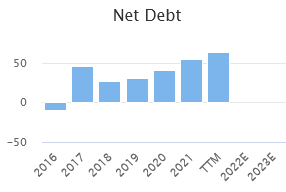

Net debt/leverage: This acquisition spree has taken place alongside the construction of a new factory in China. This combination has had a predictable result. Debt has risen and the dividend has no longer been covered by free cash flow.

Management say that net debt reached £87m at the end of December, up from £61.3m at the half-year mark. This means that net debt/EBITDA leverage has now risen above 2.0x.

This trend has been clear to see for some time now. Essentially, the dividend has been supported by borrowed cash – never a good thing:

Elevated inventories and receivables have also eaten into the group’s operating cash flow. With supply chain conditions now normalising, I’d hope to see this start to reverse. This could release a useful amount of cash for debt reduction.

Dividend: Back in November, Paul commented that the dividend could be at risk because of declining free cash flow.

The company now confirms this, saying that the final dividend payout is being reviewed in light of the need to prioritise debt reduction.

Outlook: Strix says that it will not be making any more acquisitions and will now focus on “returning to its core operating model of behind highly cash generative with no further M&A activity or investment into new factory builds”

Capex will be significantly reduced and the firm will work on reducing inventories to free up cash from working capital.

The firm’s latest acquisition, hot water tap firm Billi, is said to have a strong pipeline of orders and be “highly cash generative”.

My view: Strix’s core kettle controls business has a dominant market share and high profit margins. Given the safety-critical nature of the product, I think this position is fairly safe.

Before its 2017 flotation, this was a conservatively-run and very profitable business. If the current management can return to this mindset and achieve good results from the acquisitions of recent years, then I think Strix could be an attractive turnaround play at current levels.

However, given the level of debt involved and the apparent likelihood of a dividend cut, I’m still cautious here. My inclination would be to wait for the company’s full-year results in March before deciding whether to invest.

Provident Financial (LON:PFG)

233p (+9% on Thursday)

Market cap £596m

Q4 trading update & name change

This sub-prime lender has closed down its doorstep lending business and is now focused on credit cards, personal loans and motor finance for the “mid-cost and near-prime parts of the market”.

Last year’s half-year results showed significant progress versus 2021 and the company has now reported a solid end to the year, suggesting full-year results should be in line with expectations.

Trading update: the group saw “strong momentum” across its credit card, vehicle finance and personal loans businesses during the final quarter of the year.

Management are keen to emphasise the group’s strong capital position. No numbers were given, but Provident reported a Common Equity Tier 1 ratio (CET1) of 27.3% in its half-year results, which is nearly double that achieved by most mainstream UK banks. The balance sheet does appear to be quite healthy, in my view.

Asset quality is said to have “remained high”. Bad debt trends were said to be stable and consistent with the earlier part of the year.

The firm’s product lines include retail savings accounts under the Vanquis Bank brand. Access to this cheaper source of funding (versus wholesale markets) remains a key differentiator, according to management.

New product: a new second-charge mortgage product is being trialled. These loans are being bought in at the moment, but the company plans to start originating them if this pilot phase is successful.

Outlook: 2022 results are expected to be in line with expectations. That prices the stock on six times forecast earnings, with a prospective dividend yield of 5.7%.

However, broker forecasts suggest earnings are expected to fall by around 35% in 2023, pricing the stock on 10x forward earnings. I assume this reflects the risk of increased bad debt levels during a recession, given the firm’s exposure to below-prime borrowers.

While this isn’t expected to impact dividend growth, I think it’s worth considering when valuing the shares:

Strategy update/name change: the company is aiming to move away from its sub-prime roots and reinvent itself as a near-prime lender.

The Provident brand was mainly linked to the doorstep lending operation, so the firm has opted to rebrand under its existing Vanquis Banking brand, which is already used for credit cards and loans.

New CEO: There’s a new chief executive to go with the new name. CEO Malcolm Le May is stepping down, having overseen the group’s turnaround since 2018.

The new boss will be Ian McLaughlin, who has a track record of senior positions in mainstream banks including Bank of Ireland, NatWest (I hold) and Lloyds.

Mr McLaughlin appears to be highly experienced, with past involvement in consumer and motor finance, SME finance and mortgages. His appointment seems logical, given the group’s intention of moving up the credit quality curve to near prime.

I’ll be interested to read his initial thoughts on the business after he takes charge this summer.

My view: It’s a little hard to believe that Provident Financial was once a FTSE 100 member with well over £1bn in annual revenue.

However, the business looks in decent shape to me today. The strategy of moving up the credit quality curve makes sense, given tougher regulation around high-cost lending and the problems suffered by the company in the recent past.

My main concern is that the firm’s client base are presumably more likely to suffer financial problems during a recession than those higher up the credit spectrum.

I think it’s possible that we’ll see bad debt losses spike over the next year. However, broker forecasts already appear to reflect this risk, pencilling a 35% fall in earnings.

I don’t think this is likely to be an existential issue for the firm, given the strength of the balance sheet.

Based on consensus forecasts, my sums suggest the group could achieve a return on equity of c.15% in 2022. That’s attractive, in my view, and suggests that the 5.7% dividend yield should be comfortably affordable.

While I’m not a massive fan of this sector, I think Provident shares could be a reasonable purchase at current levels.

Rank (LON:RNK)

92p (broadly unchanged on Thursday)

Market cap: £422m

This gaming group operates the Grosvenor Casino chain and Mecca Bingo, together with a number of online gambling properties. It’s delivered a string of profit warnings over the last year, as rising costs and weaker consumer spending have hit earnings.

For more background on these issues, I’d suggest a look at the SCVR updates from October and December.

This week’s half-year results suggests that performance may have stabilised – or at least that expectations have been cut to a more realistic level.

Trading: Underlying like-for-like net gaming revenue rose by 2% to £337.4m during the six months to 31 December. This was driven by a 9% increase in online revenue (£100.8m), offsetting a 1% fall in venue revenue (£236.6m).

Underlying operating profit for the half year was £4.2m, 83% below the £24.9m reported for the prior year.

At a statutory level, Rank reported a pre-tax loss of £107.1m for the half year, reflecting £95.4m of impairment charges. These primarily relate to soft trading at its Grosvenor and Mecca venues.

The dividend remains suspended.

Balance sheet: available cash and bank facilities stood at £148m at the end of December. Rank says net cash was £10.9m, excluding lease liabilities.

Including lease liabilities, statutory net debt was £158.3m at the end of the year, up from £142.7m one year earlier.

While I sometimes agree with the exclusion of lease liabilities from net debt, in this case I think there’s a case for including them. If the performance of UK venues doesn’t recover, then some of these leases could become onerous and need renegotiating.

More generally, the balance sheet doesn’t seem that strong to me. Tangible net asset value is negative and there is c.£78m of financial debt, in addition to £169m of lease liabilities.

I’d want to do further research into the group’s financial liabilities, before considering an investment.

Outlook: full-year operating profit guidance of between £10m and £20m is unchanged.

My view: Rank’s well-known brands and decent market share will probably support a recovery over the medium term. This business has generated double-digit returns on capital employed in the past. I’d imagine its hybrid mix of online/offline venues should continue to deliver results.

However, net debt looks high to me and I think trading could remain tough in 2023, given the macro backdrop. Regulatory risks are always a concern in this sector, too.

Rank shares have already staged a substantial recovery from their October lows.

On balance, I would be inclined to wait for another market dip before considering a purchase, given the risks involved.

Hargreaves Services (LON:HSP)

Share price: 430p

Market cap: £144m

This industrial services group operates land development and earthmoving businesses in the UK, together with a coal-focused commodity business in Germany.

Results from the six months to 30 November seem encouraging. Revenue rose by 53% to £116.5m, while pre-tax profit for the half year rose by 80% to £18.7m.

Hargreaves reported net cash of £18.1m (excluding leases) and a net asset value of 603p per share, up from 462p one year earlier. This increase appears to reflect a rise in the value of certain joint ventures and investments.

Earnings per share rose by 68% to 52.2p per share, while the interim dividend has been increased by 7% to 3p per share.

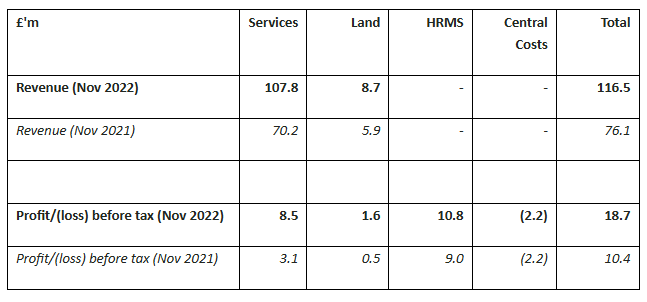

Segment performance: Revenue growth has been driven by contract work on the HS2 high-speed rail project. However, the largest profit contributor remains the group’s HRMS trading business, which is based in Germany.

Here’s how the different parts of the business contributed in H1 2022 (“Services” represents earthmoving/construction):

Outlook: the first half of the year included some one-off benefits. Management warns that this year’s results are likely to be weighted to the first half. In other words, second-half profits are likely to be lower.

This already seems to be reflected in consensus forecasts, which suggest full-year earnings per share of 71.7p, versus H1 eps of 52p.

The board is confident full-year results will be in line with market expectations, suggesting the shares remain reasonably valued at a 20% discount to book value, with a useful dividend yield:

My view: I’ve always had an interest in this business, but it’s been a complex investment over the years.

One attraction for me is that long-time CEO Gordon Banham is an 8% shareholder, so has a strong motivation to maximise the value generated by the group’s assets and protect against dilution.

I’ve only had a quick look at these half-year results, but they look fairly reassuring to me. However, I can see some risks on the horizon that could impact performance over the next 12 months.

Visibility on profits from the German HRMS business is poor, as much of this division’s income comes from commodity trading. However, the company has warned that its steel recycling business will generate less profit than expected this year due to higher maintenance and energy costs.

The UK-based earthwork and construction services business appears to be performing well, but this is a lower-margin and fairly capital-intensive operation (lots of leased equipment).

Hargreaves’ land bank remains a valuable asset. The firm has made good progress selling permitted building plots for residential developments in recent years. However, most major housebuilders appear to be cutting back on land purchases at the moment. I think it’s prudent to expect Hargreaves’ land sales to slow, also.

I think this business remains interesting and could be attractively valued, at a discount to book value. However, I’d need to do more research to understand the valuation of each segment of the group, plus the likely impact of macro conditions over the coming year.

Broker forecasts suggest some caution might be warranted, guiding for a 12% fall in earnings in the 2023/24 financial year:

On balance, however, my view is positive.

SCVR Summary spreadsheet - I'm updating this every day - please don't share this link, it's for Stockopedia subscribers only please!

See what our investor community has to say

Enjoying the free article? Unlock access to all subscriber comments and dive deeper into discussions from our experienced community of private investors. Don't miss out on valuable insights. Start your free trial today!

Start your free trialWe require a payment card to verify your account, but you can cancel anytime with a single click and won’t be charged.