A Style Classification for every stock

The Stockopedia StockRanks take a multi-factor QVM approach and rank every stock for their exposure to each driver. This process helps to simplify the goal of selecting good (quality), cheap (value), improving (momentum) stocks while avoiding the opposite.

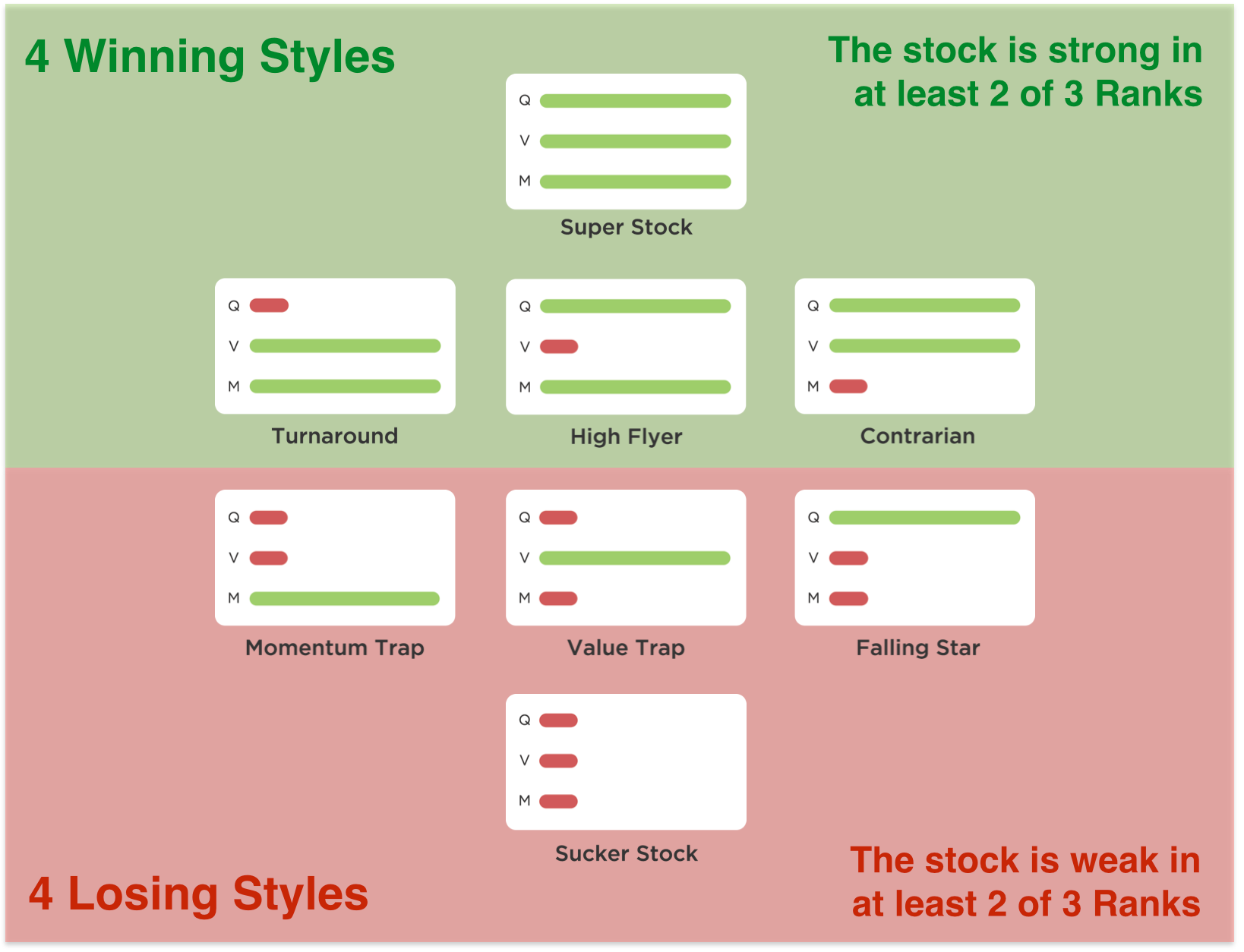

But a stock doesn’t need to be exposed to all three factors to have a good probability of success. There are actually eight different combinations of the QVM drivers which create a set of investment archetypes we call the StockRank Styles. Four are winning styles, while four are losing styles.

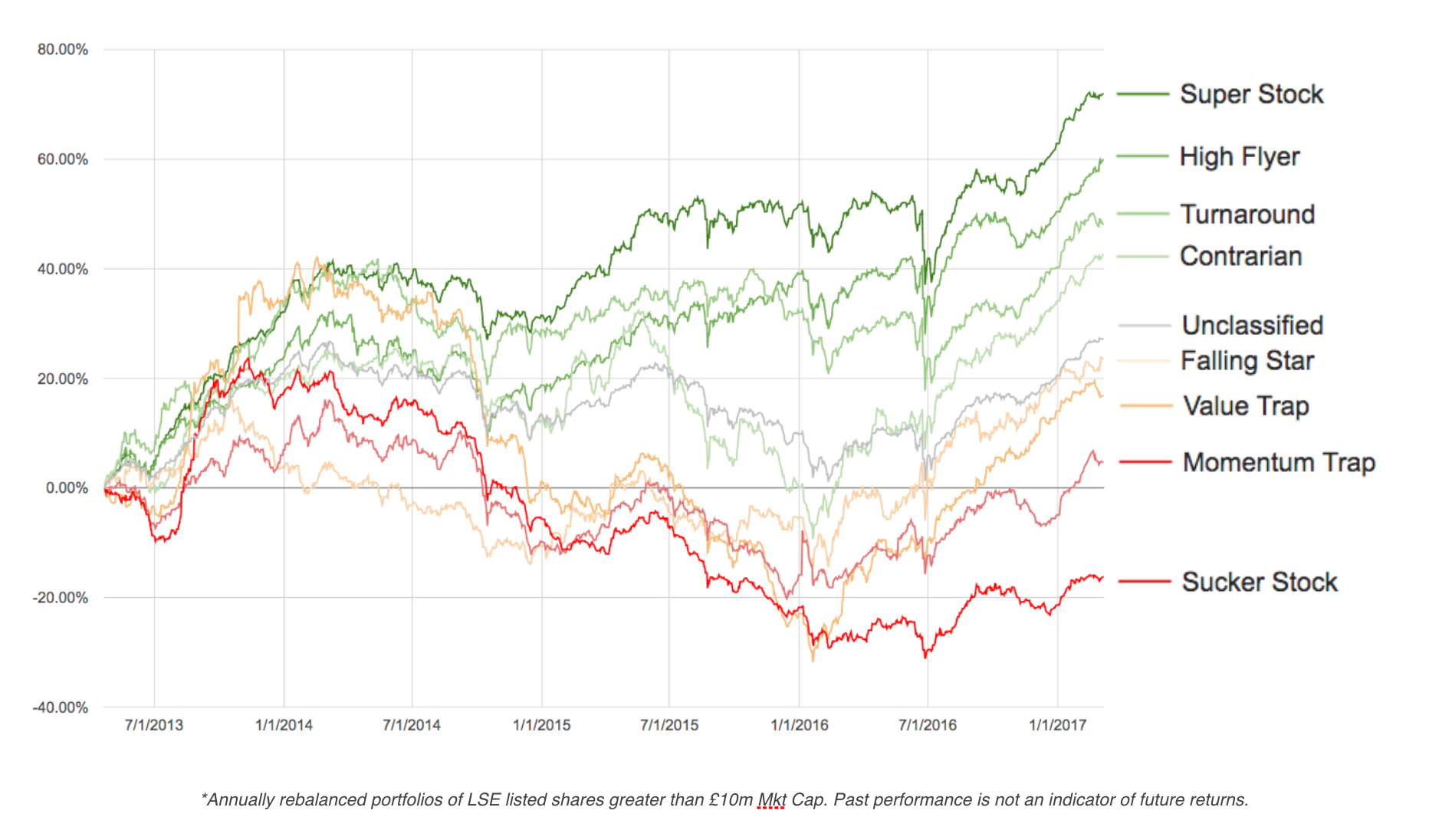

Performance Study of the StockRank Styles

We have conducted a performance study on each of the StockRank styles for the UK market where we have the most StockRanks history. It is clear from the below charts that the “Winning Styles” have historically outperformed the market, while the “Losing Styles” have historically underperformed. Unclassified stocks have tended to track or slightly underperform the market..

Finding the StockRank Styles

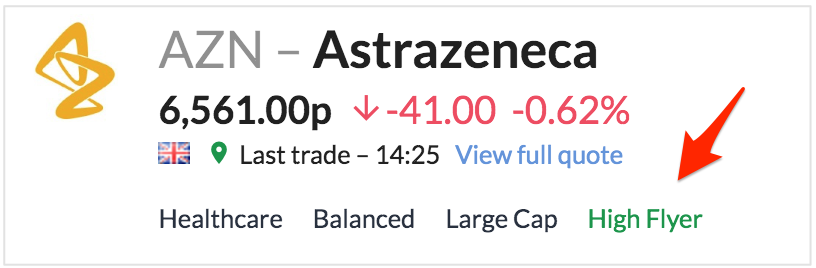

We label every stock in the market with its StockRank style in the header of every StockReport, alongside our own RiskRatings and Size Groups.

The Styles are also available in the StockRanks portal and the Stock Screener as different filter rules.

Winning Profiles

The following four combinations are classic successful investment styles, practiced by some of the greats of investing. They have also posted strong results in Stockopedia’s performance studies. A simple rule of thumb is to never consider a share that isn’t exposed to at least two of the three QVM drivers.

Super Stocks

Q: high, V: high, M: high (good, cheap, improving)

Q: high, V: high, M: high (good, cheap, improving)

The term "Super Stock" was first used by the late, great Professor Robert Haugen in " The Inefficient Stock Market". Haugen was the first to show that good, cheap, improving shares have a tendency to beat the market and we honour the great man by borrowing the phrase here. It can often go against one's instincts buying these kinds of shares as cheap stocks have problems, good stocks are boring, and stocks at highs are scary - this may be why they so often exceed expectations.

Learn More: Super Stocks - why multi-factor stock selection offers higher returns at lower risk.

Contrarian

Q: high, V: high, M: low (good & cheap, but declining)

Q: high, V: high, M: low (good & cheap, but declining)

This is the domain of the classic Value Investing style so favoured by investors like Neil Woodford, Warren Buffett and Joseph Piotroski. Warren Buffett summed it up best by saying "I like buying quality merchandise when it's been marked down". Joel Greenblatt popularised this strategy of buying good, cheap stocks in his excellent " The Little Book that Beats the Market".

Learn More: Contrarian stocks - how going against the crowd can put you ahead

High Flyers

Q: high, V: low, M: high (good & improving, but expensive)

Q: high, V: low, M: high (good & improving, but expensive)

These are the stock market stars, the ones that all fund managers want to be able to say they own. They tend to be very high quality growing stocks with a history of beating estimates, just don't expect this kind of stock to come cheap. Bill O'Neil's classic " How to Make Money in Stocks" is one of my favourite books - he shows that if you want to own the really big winners in the market you'd better be willing to pay a premium P/E ratio. Amongst this category of stocks may lie some of the great multi-year compounders - just watch out, when the momentum finally turns these can easily turn into falling stars (see below).

Learn More: High Flyers - how to beat the market in expensive and highly priced shares

Turnarounds

Q: low, V: high, M: high (cheap & improving, but low quality)

Q: low, V: high, M: high (cheap & improving, but low quality)

There's nothing better than picking up a seemingly broken stock in the bargain basement and watching it multi-bag, like Paul Scott did with Trinity Mirror in 2013. Value and Momentum are widely regarded as the two strongest factors driving asset returns. Even if a stock is currently losing money, the first indicator of recovery is often an improving share price - so buying cheap stocks on the rise can be hugely effective. James O'Shaughnessy in his classic " What Works on Wall Street" found that "Trending Value is the best performing strategy since 1963".

Learn More: Turnarounds - how to find value shares that are bouncing back

Losing Profiles

The four losing styles are common traps for investors. Shares exposed to only a single QVM Driver or worse may be alluring to the novice, but studies have shown average performance to be poor. These kinds of story stocks often come with hopes of jam tomorrow, blue-sky promise or eventual recovery.

Falling Stars

Q: high, V: low, M: low (good, expensive, deteriorating)

Q: high, V: low, M: low (good, expensive, deteriorating)

Oh, you don't want to be on the wrong side of a High Flyer when it turns. When brokers start aggressively cutting their estimates on high quality, premium shares look out below. This is the classic profile of stocks like ASOS when they start to drop. Falling Stars are the bane of fund managers around the world.

Learn More: Falling Stars - how to handle glamour shares that fall from grace

Value Traps

Q: low, V: high, M: low (junk, cheap, deteriorating)

Q: low, V: high, M: low (junk, cheap, deteriorating)

The great modern value investor, Seth Klarman, has warned "Value Traps are a dagger through the heart of value investing". This is the domain of broken business models, sectors in decline and generally one of the worst places to be in the market. The key lesson to learn is to give loss making, out of favour, cheap shares a wide berth unless they start to show confirming factors. Learn more about avoiding value traps here.

Learn More: Value Traps - how to avoid bargain stocks that might never recover

Momentum Traps

Q: low, V: low, M: high (junk, expensive, improving)

Q: low, V: low, M: high (junk, expensive, improving)

These stocks may be currently in vogue with strong share prices & sentiment, but deteriorating fundamentals and high valuations can't continue to contradict. The valuation has to fall, or the fundamentals have to improve… either way something has to change and the risks are to the downside.

Learn More: Momentum Traps - how to avoid the siren song of overhyped stocks

Sucker Stocks

Q: low, V: low, M: low (junk, expensive, deteriorating)

Q: low, V: low, M: low (junk, expensive, deteriorating)

Why on earth anybody would want to own stocks that have literally nothing going for them is completely beyond me - but many thousands do! These tend to be small cap, loss-making, jam-tomorrow, story stocks that are in the process of losing the market's faith. You can be pretty sure that a stock like this comes with a really promising idea … and an emergency fund raising just around the corner. Give these a wide berth… or use a bargepole.

Learn More: Sucker Stocks - why do we love to own the worst prospects in the market?

Statistics beat stories

What we've found in our StockRanks research is that the returns in the global stock markets have favoured the winning profiles, while stocks with losing profiles have on average underperformed. The key and critical lesson is to avoid buying a stock that is displaying less than two of the three QVM payoffs (i.e. one of the losing profiles). One should try to avoid buying a value stock unless it's either good or improving, avoid momentum stocks unless they are good or cheap, and shun expensive glamour stocks as soon as they accelerate into declines.

Playing the changes

Watching for the turning points between categories becomes much easier with a sound framework and a real world case study illustrates this well. While most investors think of housebuilders as housebuilders, their run of the last few years is quite instructive - in my mind they've moved through several of the categories listed above.

Back in 2011 the UK housebuilders were in deep value territory.... they had been terrible 'Value Traps' from 2008 to 2011, losing buckets of money while the share prices collapsed. But in late 2011, the shares initially started gaining, exhibiting the classic value & momentum 'Turnaround' signs. As the companies returned to profitability they displayed the whole spread of attributes - good, cheap, improving - pushing them into 'Super Stock' territory - the share prices soared.

Of course as prices rise, valuations often do too and now stocks like Barratt Developmentsare moving towards a premium valuation. These stocks are perhaps becoming 'High Flyers' - certainly they are at a premium valuation for their cyclical nature. What happens next is anyone's guess… but given the above framework, I know what I'll be looking for as a first indicator of trouble.

Webinar

For a more in depth review of the StockRank styles please do view the following Webinar.

Sticking to your own rules

Everyone should be warned that the stock market is a den of thieves. Unless you have steel, discipline and the capability to say no to 'opportunities' and the ability to admit when you have got it wrong you can be at the mercy of your own whims. It's absolutely crucial to build an investment process that fits with your own psychology… don't bother with momentum strategies if they freak you out… stick to good, cheap stocks and a contrarian approach. Most importantly of all, write down your own rules and stick to them.