Good morning!

To get started with we have a backlog section from Mark on James Cropper (LON:CRPR), which issued annual results yesterday.

It's a fairly quiet day for news today, so I'll aim to take a look at one or two backlog items from yesterday - including Ashtead Technology Holdings (LON:AT.).

Spreadsheet accompanying this report: link.

The agenda is now complete.

Report complete at 12.30: that's all we have time for today, enjoy your weekend.

Companies Reporting

Name (Mkt Cap) | RNS | Summary | Our view (Author) |

BHP (LON:BHP) (£98bn) | FY copper +8% to >2.0Mt, “record” iron ore prod. Jansen Stage 1 now exp $7-7.4bn vs $5.7bn prev. | ||

GSK (LON:GSK) (£58bn) | SP -5% The FDA’s Oncologic Drugs Advisory Committee (ODAC) has voted against proposed dosage of Blenrep for use to treat myeloma (a type of blood cancer). A final FDA decision on approval is due on 23 July 2025. | AMBER (Roland) [no section below] I don’t follow pharma stocks closely as I lack the knowledge to understand their products in any detail. But today’s announcement does look disappointing. An expert committee of the US FDA has recommended against approving Blenrep, a new blood cancer treatment. A final decision from the FDA is expected next week, which analysts expect to mirror the committee’s recommendation. GSK has previously said that Blenrep sales could reach over £3bn annually, which would be 9% of FY25E sales. So this was seen as a potentially important new blockbuster drug for the company. Applications to use Blenrep remain under review in most major markets, including the EU and China. I’m going to moderate our view to neutral, although I continue to think GSK as a whole is quite reasonably valued. | |

Reckitt Benckiser (LON:RKT) (£33.8bn) | Selling to Advent PE for $4.8bn (7.7x EBIT). Plans $2.2bn special divi + share consolidation. | ||

Burberry (LON:BRBY) (£4.5bn) | Retail rev -6% to £433m Outlook: no specific guidance, improvements expected in H2. | AMBER (Roland) Further revenue falls highlight the challenge that remains to rebuild customer desire, especially in the dominant Asian markets. I’m also concerned that the process of eliminating loss-making store space could be a costly and lengthy process. On the other hand, if CEO Joshua Schulman can reignite brand desire and resolve practical issues, I can see scope for a decent recovery. While my inclination is to be negative here, I think a fairer view might be to remain neutral until Schulman has had a little more time to deliver on his plans. | |

Bridgepoint (LON:BPT) (£2.9bn) | AUM +20% to $86.6bn at 30 June. Fee-paying AUM +2% to €37.5bn. Adj EBITDA -11.7% to £128.0m. | ||

Smarter Web (OFEX:SWC) (£797m) | Raised £17.5m at 295p through a placing to institutional investors. Admission due on 23 July 25. | ||

Senior (LON:SNR) (£788m) | SP +9% Selling for up to £200m (13.1x FY24 EBITDA) to a UK PE group. Initial consideration of £150m is expected to result in net cash proceeds of c.£100m. This will be used to fund a £40m buyback and for debt repayment. Transaction costs are expected to be £12m (!) and further contingent consideration of £50m is due in H1 2026, depending on FY25 EBITDA. | AMBER (Roland) [no section below] Aerospace and defence group Senior reported in March that the sale of its Aerostructures business was at an advanced stage, so today’s news should not be a complete surprise. | |

Rentguarantor Holdings (OFEX:RGG) (£327m) | Planning to move listing from AQSE to AIM, effective 15 August 2025. | ||

| Altyngold (LON:ALTN) (£156m) | H1 Operational Update | Gold poured +44% to 28.1koz, revenue +84% to $70.0m. On track for FY prod target of 50koz. | |

Crystal Amber Fund (LON:CRS) (£101m) | Rec’d final £18m relating to DLAR, total £40.7m. Main focus is now Morphic Medical reg. approvals. | ||

Metals One (LON:MET1) (£36m) | 10% interest in NovaCore Exploration, which holds 15,000 acres in Red Basin, New Mexico. | ||

Kavango Resources (LON:KAV) (£34m) | Made high-grade gold intercept at Bill’s Luck mine, Zimbabwe: 13.6g/t over 10.4m, 111.4m deep. | ||

Panthera Resources (LON:PAT) (£32m) | Started Bido drilling (Burkina Faso); 1,740m drilling to test for continuity of earlier gold intercepts. | ||

GSTechnologies (LON:GST) (£30m) | GST considers that sellers of Semnet have breached non-complete [sic] undertakings. | ||

Atome (LON:ATOM) (£25m) | The EIB has agreed to support this green fertiliser project in Paraguay. FID now exp end September. | ||

Great Southern Copper (LON:GSCU) (£16m) | FY25: £4.2m net loss, £1m net cash. Outlook: planning drilling at Mostaza and Viuda Negra. | ||

CAP-XX (LON:CPX) (£14m) | Total pipeline “approaching” $2m. Achieved first design-win order. Focused on converting pipeline. | ||

Argentex (LON:AGFX) (£3.3m) (suspended) | Following yesterday’s news that the company has failed to secure interim funding, Argentex has agreed with FCA to cease all regulated activity. This includes not onboarding new customers, not opening any new FX trades and taking all reasonable steps to stop incoming payments from existing customers. | RED (Roland) [no section below] These new restrictions appear to amount to a near-total ban on any continuing operations for Argentex. As Mark highlighted yesterday, this situation looks terminal and remaining shareholders will likely be questioning whether the IFX takeover at 2.5p per share is still going to proceed. |

Backlog: James Cropper, Ashtead Technology Holdings

Roland's Section

Burberry (LON:BRBY)

Up 4% to 1,298p (£4.7bn) - First Quarter Trading Update - Roland - AMBER

As a former shareholder I have been following Burberry’s turnaround efforts with interest. Unfortunately today’s first-quarter update seems inconclusive, at best, to me.

Today’s update covers the 13 weeks to 28 June 2025 and shows a further drop in revenue, together with underperformance from both new and existing stores:

Retail revenue -6% to £433m (-2% at constant exchange rates)

Comparable (LFL) store sales: -1%

Contribution from space: -1%; I take this to mean that store closure(s) resulted in lost sales

This seems to be a geographic story, with falling sales in China and Asia Pacific cancelling out some signs of progress in Western and Middle East markets:

The main problem with these numbers is that Burberry generated 44% of its revenue in Asia Pacific last year (including Greater China) and only 21% in the Americas. So the positive and negative sales figures in the table above do not simply offset each other.

The Americas and EMEIA will have a lot of heavy lifting to do to offset the decline in sales in China/Asia.

CEO Joshua Schulman understandably takes a positive note today, flagging up progress with his Burberry Forward strategy to rejuvenate the brand:

“Distinctive monthly campaigns - High Summer, Highgrove and Festival” to appeal to different customer segments

Rebalanced Autumn 25 collection, focused on “fewer, bigger ideas”

Improved visual merchandising in stores, higher product density, “scarf bar pilot outperforming fleet”

Online momentum

“Outperformance in outerwear and scarves and improved conversion”

All of this seems positive and I am confident that Burberry probably can improve on its baseline desirability by focusing on its core brand identity and on products where it has a distinctive appeal.

However, I have concerns about the ultimate growth potential of the business and the size and cost of its store estate. This is a risk Megan highlighted when she reviewed the company’s results in May.

Burberry’s FY25 accounts included impairment charges relating to 18 stores and showed net lease liabilities of £214m. This effectively indicates the expected scale of future losses from the store estate, based on management assumptions about future trading at the end of March 2025.

Of course, this may change if trading improves; year-end accounts are by their nature a momentary snapshot.

However, the negative contribution from space in today’s update suggests to me that Burberry is starting to close stores or reduce retail space where it’s able to. That seems sensible, but I think there’s a risk this process could be a drag on performance for some time to come.

Outlook: today’s update did not include any comment on Burberry’s performance versus full-year expectations.

Instead, CEO Schulman reiterated his (sensible) strategy and guided for some improvement in performance in H2:

Our focus this year is to build on the early progress we have made in reigniting brand desire, as a key requisite to growing the topline. In the first half we are continuing to prioritise investment and expect to see the impact of our initiatives build as the year progresses. We will deliver margin improvement with a continued focus on simplification, productivity and cash flow.

Roland’s view

Leaving aside the store estate, my main concern here is that demand from luxury buyers in Asia and China specifically will never return to the levels seen in the past.

The world has changed over the last decade and China’s domestic luxury market has matured and developed. From what I understand, there are now a growing number of coveted domestic luxury brands in China that offer an alternative to well-known western brands.

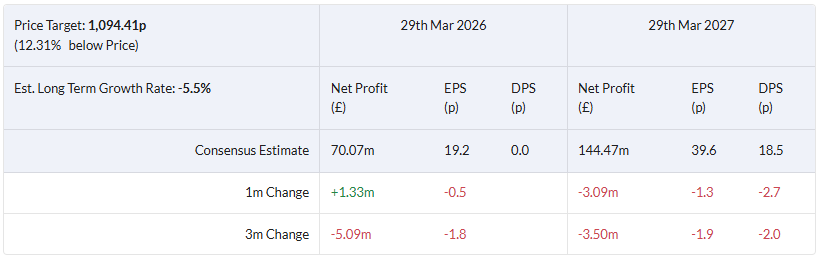

The other thing to consider is the valuation of this business. Historically, the shares tended to trade on a low-20s P/E ratio. Assuming a similar ratio in the future means that the current share price could imply earnings of 55-60p per share.

Forecasts for the next couple of years are much lower than this:

These forecasts put Burberry on a FY26E P/E of 65, falling to a P/E of 32 in FY27.

Valuation estimates I’ve attempted in the past suggest to me that this business could be close to fair value already at current levels. However, I recognise that if the brand can regain momentum, strong operating leverage could support a strong recovery in profits.

My inclination is to take a negative view here, but on balance I think a fairer view might be to remain neutral until Mr Schulman has had a little more time to deliver on his plans. AMBER

Ashtead Technology Holdings (LON:AT.) - backlog

Down 21% to 353p (y’day) (£268m) - Half Year Trading Update - Roland - AMBER/RED (BLACK)

Ashtead Technology Holdings plc (AIM: AT.), a leading provider of subsea technology solutions to the global offshore energy sector, provides an update on trading for the six months ended 30 June 2025.

Yesterday’s half-year trading update appears to have been a profit warning, at least using some measures of profit (my emphasis):

The Board's view is that full year Adjusted EBITA will be modestly below its previous expectations whilst its expectations for adjusted profit before tax remain unchanged.

Ashtead Technology is essentially an equipment hire provider to the offshore oil and gas sector. It floated on AIM in 2021 and initially did well, before seemingly coming unstuck:

This is a business where private investors seem to have been struggling for visibility over the last year or so. No broker notes are available on Research Tree. However, as Graham noted when he reviewed the interim results last September (when the shares fell sharply), there have not previously been any cuts to guidance.

As we can see from the consensus trend chart on the StockReport, this has remained true since then – right up until yesterday:

Half-year update

Yesterday’s update covers the six months to 30 June 2025 seems to contain a mix of positive and negative points.

Revenue rose by 23% to approximately £99m during the half year, but also fell by 6% on a pro-forma basis. I believe this reflects the acquisitions of Seatronics and J2 Subsea in October 2024; it looks like the addition of revenue from these companies has offset falls elsewhere in Ashtead’s business.

The company admits that H1 saw “lower revenues than initially expected” and blames a number of factors:

Geo-political factors, including “significant disruption in the US market”;

Focus on higher quality rental revenues, pro-actively reducing exposure to lower-margin activities

Profit margins for the half year are reported at c.27.3%, on an adjusted EBITA basis (H1 24: pro forma 26.1%). Management say this is consistent with the group’s medium-term target of “high 20%’s”.

However, this performance continues the sequential decline in EBITA margins seen since 2023:

FY21: 25%

FY22: 28%

FY23: 32.8%

FY24: 29.9%

HY25: c.27.3%

One positive is that cost savings from the integration of Seatronics and J2 have apparently been both higher and quicker to achieve than originally expected.

Leverage: cash generation was in line with expectations and pro forma net leverage is expected to have been 1.6x EBITDA at the end of June.

This level of gearing shouldn’t be problematic unless profits fall further than expected, when it might become a concern.

Outlook & Estimates: there is some seasonality to this business and results are normally weighted to the second half.

The company now expects to report “high single digit percentage” revenue growth in H2, relative to H1.

Applying this to the H1 revenue figure of £99m suggests to me that full-year revenue could be c.£208m.

This is 9% below the consensus figure of £228m shown on the StockReport on 15 July (click on the arrow by the print button to access past StockReports).

Applying the H1 adj EBITA margin of 27.3% to these two revenue figures gives profit expectations of c.£57m and £62m, respectively. So we might speculate that this measure of profit is now expected to be about 8% lower than previously expected, perhaps a little less if margins improve at all.

I’m not going to try and recalculate earnings forecasts as the company’s unchanged pre-tax profit guidance makes this difficult. This seems to suggest that either finance costs or amortisation will be lower than previously expected, offsetting some of the weakness in earnings.

Personally, I suspect we may see consensus earnings forecasts for 2025 and 2026 slip slightly lower over the coming weeks, as analysts' reworked forecasts feed through.

I note from the news feed that brokers Berenburg and Peel Hunt both cut their price targets for Ashtead Technology yesterday.

Roland’s view

I would view yesterday’s update as a profit warning, certainly in terms of trading performance.

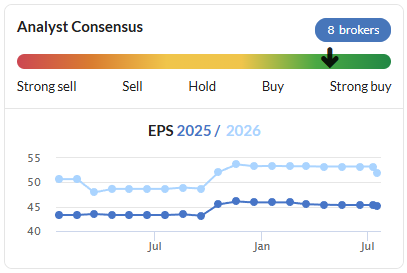

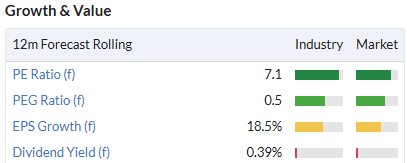

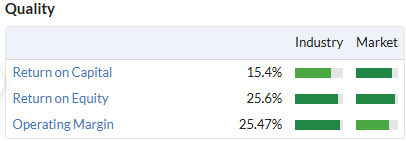

I’m tempted to take a neutral view here, as yesterday’s drop has left Ashtead trading on just seven times rolling 12-month forecast earnings:

A year ago, the stock was trading on a P/E of >20. At this level I think the business could be cheap, if past quality metrics can be maintained:

However, I’m a little concerned about the apparent speed at which trading conditions seem to have worsened.

In its AGM Update on 22 May, the company said trading for the first four months of the year had been in line with expectations and made several points which seem to be at odds with yesterday’s statement:

“Record key customer backlogs provide confidence in future demand”

“While the macro business environment remains fluid, the Group's mobile and fungible technology fleet provides operational flexibility and helps navigate regional geopolitical market fluctuations.”

“The Board’s performance expectations for the full year remain unchanged”

I recognise that geopolitical events have moved fast over the last couple of months. But I can’t help wondering if the revenue weakness seen since May suggests some cyclical weakness is emerging in this sector. Are the key customers mentioned above cutting back on their orders?

The other risk I can see here is more general, based on our knowledge that a longer period of weakness often follows an initial profit warning.

For both of these reasons, I am going to go AMBER/RED on Ashtead Technology despite the possible cheapness of the shares.

We’ll aim to revisit this situation when the half-year results are published in August to see if a more positive view can be justified.

Mark's Section

James Cropper (LON:CRPR) - backlog

Up 11% to 260p (y'day) - Full Year Results - Mark - AMBER

This year, James Cropper have appointed the well-regarded CEO, David Stirling, formerly of Zotefoams. My view of his tenure there is less favourable than many. While he seemed good at selling the Zotefoams story to investors, taking on debt to build manufacturing capacity in a capex-heavy industry ahead of demand didn’t look sensible to me. And the new management at Zotefoams cancelled many of the “blue-sky” projects that were developed while he led the business.

With James Cropper he has a different challenge. Existing debt levels mean that capital discipline is enforced, and the weak performing part of the business is the legacy Paper & Packaging BU. Perhaps old habits die hard, as the headline for the RNS “Robust performance with new strategic direction” doesn't seem to match the sales figures:

Group revenue of £99.3m (FY24: £103.0m):

- 3% growth in Advanced Materials

- 7% decline in Paper & Packaging due to a change in product mix.

Profitability is improved through lower segmental losses at Paper & Packaging, plus higher profits at Advanced Materials:

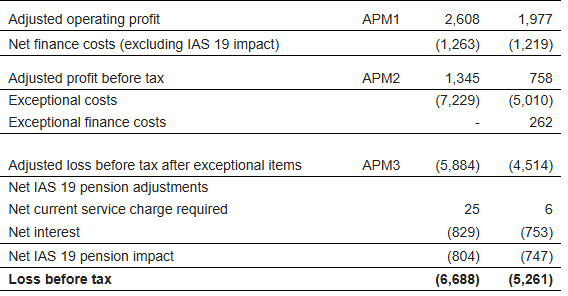

However, most of these gains seem to come from accounting for central costs differently. This confuses matters and makes it hard to determine where the improvement comes from, or how we should consider the business in a Sum of the Parts valuation (SOTP). There are also significant exceptional costs, although these are almost entirely non-cash impairments:

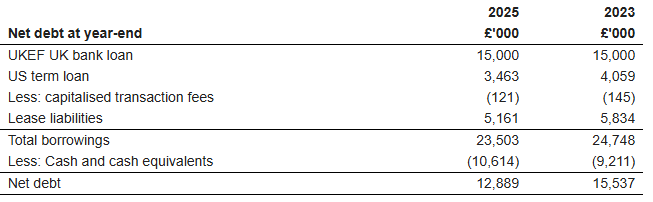

However, interest and pension deficit recovery payments are real cash payments. Net debt is down at the year end, but finance costs are up, suggesting this may not be a normal state of affairs:

Outlook:

Last week they issued a slightly confusing trading statement where they said that Paper & Packaging was trading ahead of expectations in the first quarter, but these expectations were for losses. They think they will reach break even in the final quarter of the year. Something they reiterate in these results:

Trading in the first quarter was ahead of the Board's expectations and at a similar level to the strong start recorded in FY25. Despite headwinds from the loss of business at a merchant customer, referenced above, expectations are for Paper & Packaging to deliver a significant improvement in Adjusted EBITDA against FY25, and to achieve run-rate Adjusted EBITDA breakeven in the final quarter. The Advanced Materials business is expected to report high single-digit revenue growth for full year FY26, with planned operational cost investments during the period focused on revenue growth beyond FY26.

Three things complicate matters. The first is the change in allocation of central costs mentioned above. The second is the use of adjusted EBITDA, the adjustments can often do the heavy lifting in these matters. The third is the loss of a customer. They wouldn't be the first company to try to get out of losses by raising prices and seeing customers leave. If this is the case here (and I don’t know this, I’m just speculating about how these things often play out), we may have further customer losses putting pressure on the recovery.

Valuation:

Given the current state of affairs I think the mid-case is that Paper & Packaging is worth nothing. However, Advanced Materials is clearly a valuable business. Even allocating most of the central costs and applying a relatively modest 10x operating profit, this is a valuation of around £70m. From this we have to take off £13m net debt. There is a £16m IAS19 pension deficit. However, in any corporate transaction the pension trustees will demand a much higher payment to protect pensioners, probably £10m or so. This gives a SOTP valuation of around £30m, perhaps more if we are less conservative about the multiple we apply to Advanced Materials, versus a market cap of £25m. So there is a possible upside here. However, it requires management to be willing to take the difficult decision to close or sell Paper & Packaging for a nominal fee. This is a business still with founding family shareholders and a history that dates back to the 19th Century. They may simply be unwilling to take the steps necessary to break the group up.

Mark’s view

If management can take the difficult steps here, there is a valuable business underneath. However, the risk is that the good part of the business continues to subsidise the poor part, giving poor returns for shareholders overall. I’m not sure I’m willing to bet that management will be able to convince family shareholders to let go of a century old business for a nominal sum. It’s an AMBER for me.

See what our investor community has to say

Enjoying the free article? Unlock access to all subscriber comments and dive deeper into discussions from our experienced community of private investors. Don't miss out on valuable insights. Start your free trial today!

Start your free trialWe require a payment card to verify your account, but you can cancel anytime with a single click and won’t be charged.