Good morning- thanks to Roland and Mark for all their coverage last week while I visited Paultons Park/Peppa Pig World, near Southampton. A great spot, highly recommended if you have young kids! And I enjoyed the experience of being a reader rather than a writer for a week.

Today's Agenda is now complete.

Spreadsheet accompanying this report: link.

Companies Reporting

| Name (Mkt Cap) | RNS | Summary | Our view (Author) |

|---|---|---|---|

BP (LON:BP.) (£63bn) | Manifold was CEO of CRH from 2014-24 and has a strong record as an industrial leader. | ||

South32 (LON:S32) (£6.3bn) | 102% of FY25 prod guidance, FY25 op costs in line. $225m working capital inflow in Q4. | AMBER (Roland) [no section below] It looks like South32 had a strong year, with copper production up 20% and aluminium up 6%. Australia Manganese production in Q4 also successfully recovered from previous weather disruption. The $225m reduction in working capital in Q4 is encouraging and this company has a decent track record of returning surplus cash to shareholders. With the stock now trading below its Dec ‘24 book value, it’s tempting to think there could be value here, but I think some caution may be prudent. The CEO who has led the business since its separation from BHP in 2015 is retiring shortly. South32 also recently warned that it will include an impairment charge against its Mozal aluminium business in its FY25 result. The company is having difficulty negotiating a new electricity supply for Mozal to replace the current deal, which expires in early 2026. Mozal generated 13% of revenue and 5% of group profit in 1H25. I am going to mirror the StockRanks and take a neutral view at this time. | |

Assura (LON:AGR) (£1.63bn) | EPRA earnings +9% to £111.8m (EPS of 3.5p). NAVps +2.2% to 50.4p. Avg rent uplift 3.2%. | PINK | |

| Oxford Nanopore Technologies (LON:ONT) (£1.4bn) | HY Trading Update | Expect H1 revenue +28% (CC) to £105m, ahead of exps. FY guidance “remains on track”. | |

MONY (LON:MONY) (£1.16bn) | Rev +1% to £225.3m, net profit +3% to £45.6m. Outlook: FY25 adj EBITDA to be within consensus. | AMBER/GREEN (Roland) These H1 results highlight excellent quality metrics, but flag up weak growth and a mixed outlook. I can’t help being attracted by the quality and value on offer from this price comparison group, which has 25%+ operating margins and a 6% dividend yield. However, earnings forecasts have been trending lower and the language in today’s update suggests to me that there’s a risk profits will be at the lower end of expectations. I think an element of caution is sensible at this point, so I have downgraded our view by one notch today. | |

PRS Reit (LON:PRSR) (£588m) | Q4 Update & Update re. Strategic Review and Formal Sale Process | Portfolio complete at 5,478 homes, ERV of £72m. Rent collection 99%, LFL rent growth +9.6%. Remains in takeover discussions with Long Harbor re. 115pps proposal reported in June. | |

Hunting (LON:HTG) (£515m) | Order for titanium stress joints for use in deepwater gas project. First delivery exp Q1 2027. | GREEN (Roland) [no section below] This is a follow-on order for phase 3 of this Turkish project, following a c.$20m phase 2 order received in 2024 that’s due for completion in 2026. The company says its Subsea order book is now c.$125m, up from $72.5m at 31 Dec 24. I see this as encouraging evidence Hunting is successfully diversifying into longer-cycle offshore work, reducing its dependence on shorter-cycle onshore fracking (where order visibility is more limited). After a strong H1 update earlier in July, I remain positive ahead of August’s H1 results. | |

Allergy Therapeutics (LON:AGY) (£396m) | H2 rev -3%, FY25 rev £55m. Funding req’d from August, shareholder loans to be extended. | ||

Kenmare Resources (LON:KMR) (£343m) | This is the first step of a c.18 month process to start mining Nataka ore zone (9bnt resources) | ||

| Central Asia Metals (LON:CAML) (£257m) | Update on New World Resources acquisition | SP +7% NWR has received a superior bid from Kinterra. CAML has withdrawn and is due a break fee. There’s no mention of the value of the break fee in today’s update, but on 7 July CAML mentioned a possible break fee of A$2.3m – around £1.2m. | AMBER/GREEN (Roland) [no section below] Investors have welcomed the news that miner CAML has withdrawn from a bidding war to buy Australian-listed firm NWR, which owns a copper deposit in Arizona US. I see that CAML’s latest offer (previously recommended by NWR) was for A$240m (c. £116m). This would have been a fairly big deal relative to CAML’s market cap, with the majority of the payment funded through new debt. In addition to this, previous updates from the firm suggest CAML would have needed to fund around US$300m of capex to bring the acquired asset into production. I haven’t carried out any analysis on the potential returns from the NWR asset. But in general I would say that I share the market’s positive view of CAML’s withdrawal. Debt-funded acquisitions of pre-production mining assets are fraught with risk. The size of this project relative to CAML’s existing business would have made me nervous. With NWR out of the way, I am happy to maintain Mark’s moderately positive view from March, as I can see some potential value here, reflected in the StockRanks contrarian view. |

Midwich (LON:MIDW) (£216m) | H1 rev -4.3% to c.£620m, adj EBIT c.£15.4m. Leverage 2.6x. FY25 outlook in line with revised exps. | AMBER/RED (Roland) [no section below] It’s good that the company has not needed to downgrade its guidance again. But these figures look fairly weak to me. I’m also concerned by the H1 leverage multiple of 2.6x EBITDA. This has risen from 2.0x at the prior year end due to deferred acquisition payments and seasonal cash outflows. Leverage is expected to reduce to 2.2x by the year end, but this level of gearing still looks uncomfortably high to me for a low-margin distributor. A further concern is that today’s update also reiterates guidance for a stronger-than-usual H2 weighting this year, raising the risk of a further warning later this year. There may be recovery potential here, but the leverage involved means this situation also looks risky to me. I downgraded Midwich in May and am leaving this negative view unchanged today. | |

Public Policy Holding (LON:PPHC) (£208m) | Rev +24% to $87.9m, organic +8%. Adj EBITDA +21% to $21.2m. FY25 outlook in line. | ||

Avacta (LON:AVCT) (£126m) | Used recent £3.25m placing to settle quarterly payment on conv. bond. £22.95m remaining. | ||

Jubilee Metals (LON:JLP) (£107m) | FY production ahead of guidance. PGM production +6% to 38.6koz. FY26 PGM guidance 36-40koz. | ||

Aoti (LON:AOTI) (£96m) | Q2 weaker than anticipated. Outlook: mid-teens growth, low double digit EBITDA margin. | BLACK | |

Pebble (LON:PEBB) (£77m) | Return of capital of up to £6.5m by purchasing shares at 61p. | ||

Headlam (LON:HEAD) (£70m) | Sale and leaseback of distribution centre. Sale proceeds £21.75m. 153% premium to book value. | ||

Ondine Biomedical (LON:OBI) (£58m) | Canadian hospital completes 291-patient pilot study in ICU. | ||

Creo Medical (LON:CREO) (£52m) | “40% to 60% revenue growth… in-line with prior guidance”. Continued historical H2 weighting. | ||

Kromek (LON:KMK) (£36m) | Contract for procurement of radiological nuclear detection equipment and services. | ||

Manolete Partners (LON:MANO) (£35m) | £3.2m incoming. Costs were only £483k. But there will be an £836k fair value writedown on bal sheet. | ||

Metals One (LON:MET1) (£35m) | Price: $50k and 500k new shares. Strategic acquisition in Wyoming. Phase 1 Exploration underway. | ||

Riverstone Credit Opportunities Income (LON:RCOI) (£28m) | RCOI is in wind-down. A July 2023 investment of $9.9m has been realised at a 20% IRR. | ||

Portmeirion (LON:PMP) (£19m) | H1 sales +2.8% (cc), +10.8% ex USA. Outlook: modest growth. No reference to market expectations, perhaps because there aren’t any. The company’s Nomad Shore Capital has published a note this morning in which they decline to reinstate forecasts for PMP. | AMBER/RED (Graham) Leaving our moderately negative stance unchanged due to ongoing serious issues that the company is seeking to address, in particular US tariffs. I'm a little concerned that its debt position may become uncomfortable. While the company does have significant tangible net assets, these have been tied up in inventories, and the company's seasonal peak borrowing requirement is in October. Net debt rose to £14.8m as of June. Given the fragile balance sheet, I do not view this as a deep value opportunity. | |

Tekcapital (LON:TEK) (£18m) | Reebok athletic smartglasses available today on Reebok app. On Reebok.com on August 1st. | This is a Reach announcement, i.e. a non-regulatory press release. | |

Argentex (LON:AGFX) (£3.3m) (suspended) | With Argentex going into administration, IFX does not intend to go ahead with the acquisition (or at the very least is seeking to reserve the right not to go ahead with it). | RED (Graham) [no section below] Last week, we got the bad news that Argentex was in further difficulty, being unable to engage in any commercial activity at all after failing to meet a new liquidity requirement set by the FCA. Being unable to trade, it had little choice but to seek to enter administration, but this now means that the IFX takeover is in doubt. I would have to assume that zero is now the most likely outcome for shareholders, rather than the 2.49p per share takeover. |

Graham's Section

Portmeirion (LON:PMP)

Unch. at 134p (£19m) - H1 2025 Trading Update - Graham - AMBER/RED

Mark looked at PMP’s most recent annual results in some detail, in March.

Today we have a trading update which doesn’t read very well to me, but there aren’t any live earnings forecasts that need to be downgraded. The company’s brokers have chosen not to issue estimates in recent months, which itself must qualify as some sort of red flag?

Key points from the update:

H1 sales up 1.3% to £37.1m, or up 2.8% at constant currency.

Sales up 10.8% excluding USA (but note that USA is a key market).

North American sales are down 10.6% due to tariff disruption.

The response to tariffs involves a mixture of early deliveries, reduced volumes as they ditch certain low-margin retailers, and switching manufacturing back to the UK.

We have successfully managed our production schedules and shipments into the USA during the tariff disruption in H1, and our customers can expect to receive their orders significantly earlier than in prior years, ensuring our product is in-store and available for sale at the beginning of the peak Holiday and Christmas season.

In FY25 the product supplied by the Group into the USA market will be markedly down on a like-for-like basis by volume as we have cancelled certain orders sourced from Asia for the USA market which would be subject to higher tariffs. We are taking this opportunity to accelerate our Made in Stoke-on-Trent onshoring initiative which we outlined at the time of the Group's Annual Results on 31st March 2025, increasing the proportion of product supplied into the USA from the United Kingdom.

UK sales are up 3%, South Korea up 31.6% (a recovery situation after a Covid-related stock overhang), and other international sales are up 11.2%.

Net debt rises by £1m+ to £14.8m, due to the earlier USA shipments. Debt peaks seasonally in October.

Outlook:

We anticipate modest sales growth in H2, primarily due to short term caution on the US market. We anticipate the UK to be flat - low single digit growth driven by good Wax Lyrical performance, and continued improvement in South Korea and International markets.

Graham’s view

I’m still a little surprised that this homeware group has reached such a low valuation, but it has struggled with a variety of issues in recent years.

I covered its profit warning last December when it became apparent that the company had very little visibility on trading, and there has been zero improvement on that front since. Both brokers have declined to produce forward estimates in recent months, and that remains the case today, as far as I can tell - Shore Capital have published on PMP today, but again without publishing forecasts.

This isn’t normal and it says to me that there is deep uncertainty around the company’s transformation plans, its onshoring activities, and its ability to trade profitably in the USA.

The company has guided for “modest sales growth”, so you would think that a revenue forecast would be possible. But costs and margins won’t be pretty, considering higher NICs, NMW, utility prices, US tariffs, and higher-margin UK manufacturing (all mentioned in today’s update). With all of those cost pressures, perhaps a realistic profit estimate would be difficult for investors to stomach.

I don’t blame management in particular for the poor trading, as many of the issues appear to be outside of their control. US tariffs on Asian imports are not something that management asked for or are responsible for.

But from an investment point of view, the issues are very serious, not the least of which is the inability of the company to provide forecasts for the past several months.

And it probably is reasonable to blame management for some forecasting errors in the lead-up to the December profit warning.

Personally, I don’t see how I can change our AMBER/RED stance. I don’t doubt that the company is working hard to address the challenges. But it’s still very much a work in progress.

For deep value investors, there are plenty of tangible assets on sale here: £45m as of Dec 2024. But a large portion of this (£38m) was inventories, funded by debt.

As noted by the company today, their seasonal peak for debt is actually around October. At year-end 2024, their cash and borrowing headroom was less than £10m. So I would conclude that their headroom was significantly less than £10m in October 2024, and that it could be lower again in October 2025.

In summary: this is not what I’d consider to be a comfortable balance sheet, and therefore I do not view this share as a deep value opportunity.

I’m therefore going to leave our AMBER/RED unchanged.

Roland's Section

MONY (LON:MONY)

Down 7% to 206p (£1.1bn) - Interim Results - Roland - AMBER/GREEN

We’ve previously been positive on the owner of the Moneysupermarket comparison business due to its exceptional quality credentials and modest valuation. In May, Graham suggested that “low top-line growth is perhaps the major challenge” standing in the way of a higher valuation.

Unfortunately, today’s interim results appear to emphasise this concern and flag up the risk of some weakness in earnings this year. The market has reacted with a mild sell-off this morning:

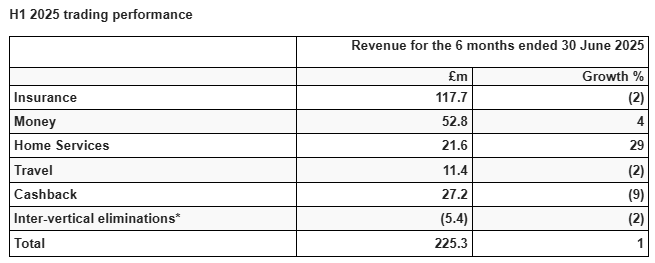

H1 results summary: Today’s half-year numbers cover the six months to 30 June 2025. They show another flat top-line performance, with only very modest profit growth:

Revenue up 1% to £225.3m

Pre-tax profit up 3% to £45.6m

Adjusted earnings up 4% to 9.3p per share

Net debt reduced to £18.4m (H1 24: £25.1m)

Interim dividend up 1% to 3.3p

Loyalty bonus: the group’s loyalty scheme is continuing to expand. SuperSaveClub membership rose by more than 50% (500,000) to over 1.5m during the first half of this year. Remarkably, the club now covers more than 95% of MoneySuperMarket’s products sold by volume – although this only translates to 14% of group revenue.

It’s not hard to see why membership is growing during a cost-of-living crisis – members get a cash reward of up to £20 for each purchase, a best price guarantee and a simplified application process, with much of their data stored by MONY.

Of course, this loyalty and information sharing is also of value to the company, providing the ability to offer “selected cashback and retailer discounts which encourages further engagement”.

Indeed, management says that when compared with “a baseline traditional” user, members are 3x more likely to renew and 3x more likely to make a second purchase. If this momentum can be continued, it could be a powerful tool for gaining market share – essential in such a mature market.

Headwinds in some markets

CEO Peter Duffy is keen to put a positive spin on today’s results, suggesting that a 1% improvement in revenue is “resilient” against “a strong prior period”. But H1 revenue growth last year was only 5%, which doesn’t seem a particularly strong comparator to me against a backdrop of low-single digit UK inflation.

I think the real issue here is relatively weak performance in several of the group’s market segments during H1:

Insurance: car insurance premium inflation is said to have eased, resulting in a 9% fall in premiums in H1 (although this is not my personal recent experience!). To compensate, the company has switched focus to insurance categories such as home, life and travel.

Money: “strong activity” in borrowing was driven by credit cards, with some improvement in personal loans. Savings account activity remained strong but current accounts switching was lower.

Home Services: this division includes utility switching. Opportunities for energy switching have been minimal in recent years as we’ve all been paying (largely) the same government-capped prices. Widespread failures among smaller energy suppliers have further reduced opportunities for switching.

However, there are signs this market may now be recovering:

Home Services grew 29%, albeit from a low base, with both energy and broadband delivering significant growth over the period, as the energy market continues to gradually recover.

The Home Services segment generated £68m of revenue in 2021 and £103m of revenue in 2020. So trading remains very subdued in a historic context.

Personally, I think the market opportunity for energy price comparison is likely to remain smaller than in the past. There are now fewer, larger energy suppliers in the UK and none of them are offering the kind of unsustainably cheap fixed-price deals that previously drove a lot of switching activity.

Cashback: down 9% as a result of the weaker retail environment and the knock-on effects of a weaker car insurance market, which also affected the Quidco compare service.

Travel: tough competition on car hire, but stronger on package holidays.

Quality still shines through

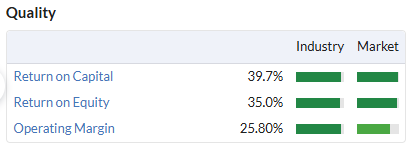

One factor that hasn’t changed is the exceptional quality of MONY’s accounts.

Today’s results show an operating margin of 27.2% (HY24: 27.0%) and return on capital employed of 36.3%. Both figures are excellent and are consistent with last year’s performance:

Cash conversion is strong too. I estimate underlying free cash flow of £52.9m, excluding working capital movements. This represents 116% of net profit for the period, a very respectable performance.

Outlook

I suspect this statement was the trigger for today’s share price weakness:

Our recent trading performance, coupled with momentum in our strategic execution gives the Board confidence that we will deliver Adjusted EBITDA for 2025 within our current published consensus.

My reading of this comment suggests adjusted EBITDA (a very subjective number) is only expected to be within the range of consensus, so might be below the consensus average.

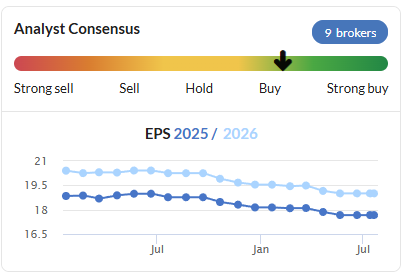

Helpfully, consensus expectations are given as an average of £143.7m, with a range of £137m to £150m.

We can see from the StockReport that consensus earnings estimates for 2025 have already been cut by 6% over the last 12 months. The general trend seems to be negative and I would not be surprised to see a further reduction in the coming days:

Roland’s view

With an EBIT/EV yield of around 10%, investors buying MONY shares today are getting a lot of high-quality business for their money. The 6% dividend yield looks safe enough to me and management are supplementing this with a modest ongoing £30m buyback.

However, growth remains challenging and I am not sure how easily this will change. While the performance of the SuperSaveClub loyalty scheme seems encouraging, my understanding is that MoneySupermarket remains in a distant second place to CompareTheMarket in the lucrative car insurance segment.

This might account for the apparent disparity between club members buying 95% of products on MoneySuperMarket, but only generating 14% of group revenue.

I can’t help but remain positive here, but I think that an added note of caution is sensible given the tone and content of today’s update. I’m going to downgrade our view by one notch to AMBER/GREEN.

See what our investor community has to say

Enjoying the free article? Unlock access to all subscriber comments and dive deeper into discussions from our experienced community of private investors. Don't miss out on valuable insights. Start your free trial today!

Start your free trialWe require a payment card to verify your account, but you can cancel anytime with a single click and won’t be charged.