As the second half of the year begins, let’s check what has happened so far in 2026.

The FTSE is up 5.5% year-to-date.

The AIM All-Share Index has underperformed, up by only 0.3%. I no longer use this index as a major benchmark, as it doesn’t perform well over the long term. I’d rather use something like the FTSE SmallCap Index (up 5.1% year-to-date).

The S&P 500 is up 9.3% year-to-date. After a very slow Q1, it has roared higher in Q2.

Gold is down 7.1% year-to-date, measured in dollars. Bitcoin is down 30.5% year-to-date.

Brent crude oil is up 20% year to date, having been up c. 90% at the peak.

And finally the pound is down 1.6% against the dollar, with uncertainty over who the next chancellor might be.

It’s been a very eventful six months politically but overall, probably not a terrible one for most investors.

For what it’s worth, here’s the total return of the top five holdings in my personal portfolio: Volvere (26% of the PF): down 12%, Berkshire Hathaway (21%): down 1% in US dollars, IG Group (21%): up 10%, Next (11%): up 8%, British American Tobacco (5%): up 12%.

Overnight market movements:

The FTSE is down 0.2% at 10,490

S&P 500 is down 0.2% at 7,470

Brent crude (September) is up 0.2% at $73.05/bbl

Gold is down 0.7% at $3,980/oz

Bitcoin is up 0.7% at $59,100

Companies Reporting

| Name (Mkt Cap) | RNS | Summary | Our view (Author) |

|---|---|---|---|

Associated British Foods (LON:ABF) (£14bn | SR52) | Q3 revenue +3%, YTD +1%. Primark, Grocery and Ingredients are in line, Sugar profits will now be lower than previously expected due to higher gas prices as a result of the Middle East conflict. Apart from Sugar, the outlook is unchanged. | ||

South32 (LON:S32) (£10.0bn | SR68) | Final Approval of Sierra Gorda's 4th Grinding Line & Agreement to Sell Aluminium Assets to Alcoa | Sale of aluminium value chain assets to Alcoa for an Enterprise Value of US$5.6bn, including a $3.1bn upfront cash payment. Valuation implies a “through-the-cycle EBITDA multiple of ~6..8x”. Fourth grinding line at Sierra Gorda JV will increase processing capacity from ~48Mtpa to ~60Mtppa. First production expected FY30. | |

Primary Health Properties (LON:PHP) (£2.5bn | SR58) | Refinanced existing debt facilities with a new 3-5yr loan and RCF facility totalling £800m. This will allow the partial refinancing of the bridging facility put in place to finance the acquisition of Assura in 2025, reducing finance costs. Further initiatives are underway to complete the refinancing of this facility. | ||

Derwent London (LON:DLN) (£2.16bn | SR72) | Horseferry House: sold for £131.8m (6% net yield to purchaser and IRR of 8.4% over 21 years for DLN). 80-85 Tottenham Court Road: sold for £32.6m before costs, reflecting capital value of £755/sq ft. £279m of disposals agreed YTD towards £400m 2026 target. | ||

Greggs (LON:GRG) (£1.64bn | SR80) | CFO Richard Hutton will retire at the end of 2026 after 28 years with the company. He is replaced by Ben Waldron, who was previously at Bakkavor Group. | ||

Chemring (LON:CHG) (£1.39bn | SR36) | Awarded sole source Indefinite Delivery / Indefinite Quantity contract for the Joint Biological Tactical Detection System. Contract has a ceiling value of $48.8m and an initial value of $36.3m through to March 2028. | ||

CMC Markets (LON:CMCX) (£1.28bn | SR88) | Strong momentum continues. CMC now expects net operating income for FY2027 to be at least £550 million, materially ahead of previous guidance of £460 million to £480 million, with EBITDA guidance of £250 million. | GREEN ↑ (Graham)

Performance has been turbo-charged by B2B expansion - for example, did you know that CMC provides a huge amount of trading infrastructure for Revolut? It does the same for ASB Bank in New Zealand. These activities are massively expanding CMC’s reach, beyond its own customer base. We should have been GREEN on this already - I’ll put us GREEN on it today. For prior coverage, I would also recommend checking out Mark’s Stock Pitch in March. | |

Polar Capital Holdings (LON:POLR) (£890m | SR88) | AUM +43% to £30.6bn, with net inflows of £902m. Pre-tax profit +49% to £76.9m, adj EPS +10% to 57.8p. Post year-end AUM up to £44.7bn on 19 June, with net inflows of £2.3bn 1 Apr - 19 June. | GREEN = (Graham)

The standout number for me is the latest AUM figure: £44.7bn. This is astounding: up 46% in less than three months. It almost feels like a typo. It’s 72% higher than the average AUM figure for FY March 2026. And it’s been achieved with only £2.3bn of net inflows since year-end. That’s an excellent net inflow number, but it only accounts for one sixth of the increase in AUM. The new earnings forecast published today by Equity Development is for EPS of 97.7p in FY27, up from their previous forecast of 61.8p. If that’s accurate, Polar is currently trading on only 9x earnings. | |

Bytes Technology (LON:BYIT) (£882m | SR61) | Chair will retire in September, new chair will be Gavin Rochussen, previously CEO of Polar Capital Holdings. | ||

ACG Metals (LON:ACG) (£397m | SR61) | A sustained improvement in gold recovery at the Gediktepe Mine, Türkiye has been achieved by introducing a new product to the metallurgical recovery process. Gold recovery has been increased to c.85% (prev. c.75%) with cyanide consumption reduced by c.45%. Patent protection secured in Turkey and progressing elsewhere. | ||

Asos (LON:ASC) (£345m | SR45) | Lease assigned to “a global consumer brand” with the associated automation assets sold to a member of the DHL Group. Disposal will generate net proceeds of c.£48m and annual cash cost savings of c.£6m. ASOS’s pro forma net debt is reduced to c.£180m. | ||

Ab Dynamics (LON:ABDP) (£244m | SR33) | Edward Haycock appointed Group CFO. He is being promoted internally and will assume his new role from 1 December 2026. | ||

Seeing Machines (LON:SEE) (£210m | SR20) | Seeing Machines is in advanced discussions with a number of potential lenders and has received multiple term sheets for the purpose of refinancing its Convertible Note ahead of the stated maturity date of 4 October 2026. The Company expects to complete the refinance process well in advance of the stated maturity date. | ||

Capricorn Energy (LON:CNE) (£208m | SR99) | Alamadiyaf al-Masiyyah continues to progress its funding arrangements and the deadline for a firm offer has been extended to 5pm on 29 July 2026. | TAKEOVER | |

Supreme (LON:SUP) (£183m | SR88) | Revenue +18%, adj pre-tax profit -14% to £27.5m with adj EPS -13% to 18.9p. Vaping revenues +15% YoY. FY27 outlook: current trading in line with market expectations. | AMBER/GREEN = (Roland) Although today’s results appear to have come in slightly below expectations, I am encouraged by progress with scaling up the Drinks & Wellness business, which now accounts for more than a quarter of gross profit. Early evidence the group is emerging as a net beneficiary of tighter vaping regulations is also positive, in my view. Supreme’s valuation may remain discounted for a while, given the exposure to vaping and falling margins. However, the group’s strong profitability suggests to me that the shares probably offer value on a single-digit P/E, so I’m maintaining my broadly positive view today. | |

Rainbow Rare Earths (LON:RBW) (£150m | SR26) | Pilot plant has operated successfully during H1 2026 with the data recovered feeding into the process design for the Definitive Feasibility Study. 75% of the flowsheet now in the engineering phase of DFS, final optimisation of the solvent extraction circuit underway. | ||

Amcomri (LON:AMCO) (£107m | SR75) | Premier Limpet sold to Dalpo Group UK for a minimum initial consideration of £10.1m. Net cash proceeds to date of c.£7m. Additional consideration will be payable based on FY26 profits. Premier Limpet was acquired for £4.1m in 2021. | ||

Distribution Finance Capital Holdings (LON:DFCH) (£106m | SR69) | Has entered into a new ENABLE Guarantee facility with the British Business Bank “on facility terms more closely aligned to its lending strategy”, with a pool size of up to £350m of loans. Commercial terms are unchanged. | ||

Home Reit (LON:HOME) (£76m | SR22) | A total of 39 properties were auctioned in May 2026, followed by 32 properties on 25 June 2026. 4 properties expected to be auctioned in July. £3m spent on opex, primarily legal fees against threatened litigation and in relation to the ongoing FCA investigation. | ||

Topps Tiles (LON:TPT) (£70m | SR71) | Revenue for Q3 down 1.8%, driven by challenging market conditions as well as store closures. Taking into account recent trading and given the ongoing market headwinds, we now expect Adjusted Profit Before Tax to be above £6.5 million. | BLACK (AMBER/RED =) (Roland) The company doesn’t share details of previous expectations in today’s update. But checking a recent broker forecast suggests to me that today’s revised adjusted PBT guidance equates to a c.30% cut to profit expectations. This follows another large profit warning in April. Topps’ self-help measures may start to deliver results over the next 12 months or so. But macro conditions seem unfavourable with housebuilding remaining subdued and “lower consumer spend”. I think it’s sensible to leave my previous moderately negative view unchanged today. | |

Clean Power Hydrogen (LON:CPH2) (£68m | SRn/a) | Firm placing, conditional placing, conditional subscription and retail offer. All at 1.5p per share. (price before suspension: 13.6p). CEO resigns. The current cash balance is sufficient for the Company to continue operating through to mid-July 2026. | Shares suspended since 29 May 2026. | |

Sanderson Design (LON:SDG) (£52m | SR98) | Momentum has been sustained with the Group delivering year-on-year growth year-to-date. Consequently, expectations for the full year are unchanged. | ||

Zanaga Iron Ore (LON:ZIOC) (£44m | SR25) | No revenues, operating loss $7.1m. “This was a transformational period… the Group strengthened Project economics, confirmed the ability to produce premium DRI-grade iron ore products, and advanced Zanaga's position as a strategically important future supplier to the low-carbon steel industry.” | Very late to publish 2025 results. | |

Time Out (LON:TMO) (£38m | SR20) | New 10-year franchise agreement with ITP Media Group covering Time Out's Media operations in Hong Kong and Singapore. | ||

Amigo Resources (LON:AMGO) (£32m | SR90) | Systematic geological mapping has identified multiple carbonatite lithologies distributed across the Project area. | ||

Atome (LON:ATOM) (£28m | SR0) | Discussions in Paraguay are still ongoing. Given the material impact of the Villeta Project on the presentation of the Financial Statements, the Board has decided to defer the finalisation of 2025 accounts. | Shares will now be suspended. | |

Goldplat (LON:GDP) (£27m | SR97) | “As a result of the continued high gold prices and strong volumes, and subject to a number of year-end adjustments, the Board expects that the Group's results for FY2026 will materially exceed prevailing market expectations.” | AMBER = (Roland) [no section below] Today’s update is brief in the extreme and there are no new broker forecasts available on Research Tree today. But use of the word “materially” suggests we could see a double-digit percentage increase to current forecasts for the year-ended 30 June. Checking back, Goldplat also upgraded its guidance “materially” in February, prompting a remarkable 61% upgrade to FY26 EPS estimates. I don’t expect such a big increase this time, but as Mark has commented in the past, broker estimates often lag commodity price movement for small producers. Given that the gold price has fallen by 10% in the last month alone, I think the more pertinent question is whether Goldplat’s FY26 profits will be sustainable in FY27. The company’s share price has been pretty resilient in the face of the recent declines in the price of gold, but with the shares now trading above book value, I’m not sure if this will continue. I have no idea on the likely outlook for gold over the coming year, so while I think Goldplay is performing well, I’m going to maintain my neutral view to reflect the speculative nature of this situation. | |

Carclo (LON:CAR) (£25m | SR57) | Revenue £114.2m (down 5.8%). Underlying operating profit £12.6m (up 28.1%). Market conditions across the Group are currently mixed… We anticipate demand strengthening as we move through the year… and accordingly expect trading to be weighted towards the second half and to deliver positive organic revenue growth for the full year. | ||

Medpal AI (LON:MPAL) (£18m | SR0) | Sarus Court will be the Company's largest pharmacy robotic distribution facility to date and is expected to provide approximately 23,000 sq ft of operational capacity when fully completed. | ||

Energypathways (LON:EPP) (£17m | SR10) | Following the award of a Gas Storage Licence for its MESH project, the Licence work programme has been launched, and a site survey is planned for Q3 2026. | ||

Rockfire Resources (LON:ROCK) (£12m | SR17) | Drilling update from Rockfire's 100%-owned Molaoi zinc deposit in Greece. High grade germanium up to 52.3g/t Ge continues to be encountered in drill core. | ||

DSW Capital (LON:DSW) (£11m | SR62) | Equity funding of £360,000 to support the acquisition of Integer Advisory Limited by DSW Business Planning. DSW BP is a licensee of DSW Capital. | ||

Croma Security Solutions (LON:CSSG) (£9m | SR59) | Receipt of £440,064 representing the final payment to complete the £6.5 million disposal of Vigilant Security Limited. | ||

Shearwater (LON:SWG) (£9m | SR47) | £12.5m of this £25m contract to be recognised in FY26, “which underpins the Board's confidence in achieving market expectations for FY26 EBITDA, with revenue expected to be slightly ahead of expectations.” |

Graham's Section

CMC Markets (LON:CMCX)

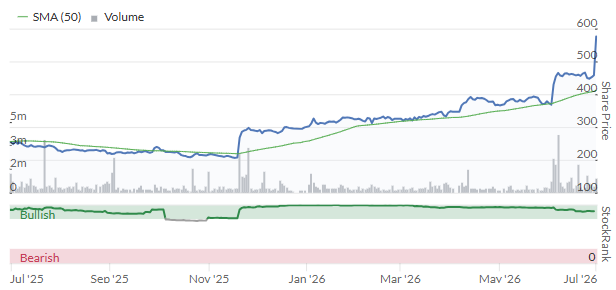

Up 29% at 591p (£1.65bn) - Trading Update and upgrade to FY2027 NOI guidance - Graham - GREEN ↑

What a chart this is:

I don’t get everything right (far from it!), but I’ve done well by sticking with a positive view on CMCX - I left it on my watchlist for 2026. I’ve also got a decent stake in its rival, IG group (LON:IGG).

Last November, IG said it was beating expectations for FY March 2026 (in the end, they may have slightly missed those upgraded expectations).

In June, they issued a large upgrade to FY March 2027 expectations.

Today they have upgraded expectations once again:

As outlined at our FY2026 results, the Group entered the new financial year with strong momentum driven by exponential and exceptional growth in our B2B business. That momentum has continued to build and scale.

As a result, CMC now expects net operating income for FY2027 to be at least £550 million, materially ahead of previous guidance of £460 million to £480 million, with EBITDA guidance of £250 million.

At the midpoint, that’s a 17% increase to revenue expectations.

And guidance for operating expenses is unchanged at £280m (this excludes bonuses, or “variable remuneration”). So the additional £80 million of net operating income should mostly trickle through to profits, depending on how much variable remuneration is paid.

Their B2B business is booming:

The strength of this performance reflects the scale of our B2B platforms driving operational gearing and delivering higher profit margins as income growth is delivered against a largely fixed cost base.

Our B2B platform business is well positioned to scale with several important milestones expected over the next 12 months and a continuous pipeline of new B2B opportunities.

Graham’s view

Performance has been turbo-charged by B2B expansion - for example, did you know that CMC provides a huge amount of trading infrastructure for Revolut? It does the same for ASB Bank in New Zealand. These activities are massively expanding CMC’s reach, beyond its own customer base.

We should have been GREEN on this already - I’ll put us GREEN on it today.

For prior coverage, I would also recommend checking out Mark’s Stock Pitch in March.

It’s the scale of the upgrade today that is so staggering - an additional £70m of net operating income, and achieved without any increase in adjusted operating expenses.

£70m of additional income equates to 26p per share, or perhaps 19p after tax. I would not assume that this converts cleanly into EPS: there will be higher bonuses and probably a few other miscellaneous costs that increase. But considering that the EPS forecast for the current year was sitting at just 36.5p, today’s upgrade will translate into an enormous increase in earnings guidance.

This stock is an old idea for me, and I don’t regret not owning it as I already own enough IGG. But it just goes to show that sometimes the old ideas are best!

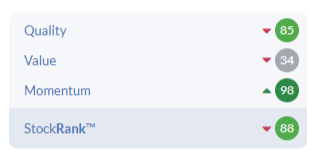

The StockRanks view it as a High Flyer, not a Super Stock, due to limited value. But the value is clearly much better than the existing forecasts implied:

It seems to me that EPS should be heading north of 50p this year, putting the shares on a P/E multiple of perhaps 11-12x while also carrying surplus cash.

Polar Capital Holdings (LON:POLR)

Up 3% at 917p (£912m) - Group Audited Results for year ended 31 March 2026 - Graham - GREEN =

This is another watchlist stock that’s doing very well:

Today’s results are excellent:

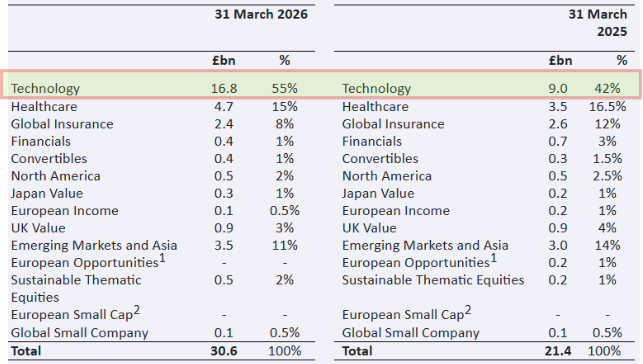

AUM up 43% to £30.6bn as of March 2026.

AUM has continued to rise and is now £44.7bn.

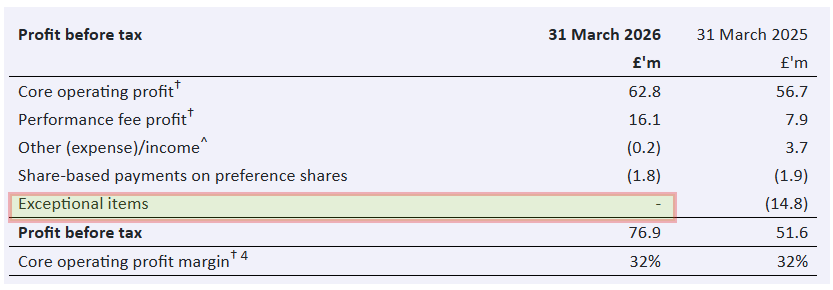

Core operating profit +11% to £62.8m.

Core operating profit only rose by 11% as average AUM only grew 14% during the year. Management fees consequently only grew by 10%, to £196.9m.

On the cost side of the equation, there was little net increase for the year (£152m vs. £157m the prior year), as higher staff compensation was offset by the absence of any exceptional items.

Therefore, while the profit figure has not grown very dramatically in FY26, I would expect a very significant uplift in revenues and profits AUM stays around current levels through FY March 2027.

FY26 was still very successful:

I always give full credit to companies who can keep exceptional items low, and it doesn’t get any better than a blank entry!

Surplus capital: a very healthy balance sheet with £72m of surplus capital above regulatory capital (£26m) and dividend commitment (£31m). There is a share buyback for £15m which is not particularly well-timed (given the high share price) but is also reassuringly small.

Outlook is very confident:

We have entered the new financial year with positive net inflow momentum, following the Group's strongest quarterly net flow figure in history in the final quarter of the financial year. Encouragingly, after a slight moderation in March 2026 as geopolitical uncertainty escalated, particularly in energy markets, that momentum has continued into the first quarter of the new financial year.

The structural headwinds facing active equity managers, such as passive substitution, fee compression, and client consolidation, have not abated. Yet we believe the environment is increasingly supportive of what Polar Capital offers. As markets broaden, as the pace of technological disruption accelerates and as investors seek genuine differentiation, the case for specialist active management becomes more, not less, compelling.

On the subject of passive substitution and fee compression, Polar are guiding for management fees to decrease by 1-2bps annually over the medium term. That’s just a fact of life in asset management: it’s getting cheaper and cheaper all the time.

Graham’s view

The standout number for me is the latest AUM figure: £44.7bn.

This is astounding: up 46% in less than three months. It almost feels like a typo.

It’s 72% higher than the average AUM figure for FY March 2026.

And it’s been achieved with only £2.3bn of net inflows since year-end. That’s an excellent net inflow number, but it only accounts for one sixth of the increase in AUM.

The focus on Technology is paying off: note how it jumped from 42% of AUM to 55% of AUM during FY26. I expect it’s a lot higher now:

So where do we go from here? Clearly there is a great deal of exposure to Tech and AI, and any cooling off in those sectors will have a great impact on Polar.

On the other hand, Polar is not a one-trick pony, even if most of its assets under management can be classified as “Tech”. There is some diversification to help cushion the company and shareholders, if we see a bust in the more speculative end of the market.

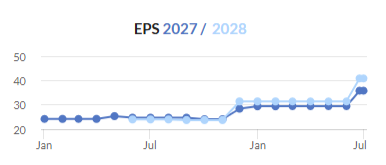

For me personally, I continue to think that the upside is likely to be more exciting than the downside risk. The £44.7bn AUM number is astonishing and if it can stay anywhere around this level, we are looking at a much bigger company than we’ve seen in the past - it has more than doubled in size over the past five years. And the FY27 results should be very exciting indeed.

On that point, the new earnings forecast published today by Equity Development is for EPS of 97.7p in FY27, up from their previous forecast of 61.8p. If that’s accurate, Polar is currently trading on only 9x earnings.

This stock can be interpreted as a bet on continued momentum in the tech space. Readers will know that I do fear that there is some extreme overvaluation in this sector. Personally, I won’t be chasing this higher and adding it to my portfolio at this stage - but I have to stay GREEN on it, as it’s performing exceptionally well and is still not obviously overvalued.

The StockRanks also say that this is a High Flyer, before taking into account the earnings upgrades that have just been realised and that will greatly increase the Value on offer.

Roland's Section

Topps Tiles (LON:TPT)

Down 6.5% at 33.5p (£65m) - Q3 Trading Update - Roland - BLACK / AMBER/RED =

This is the second profit warning this year from tile supplier Topps. The last came in April, when research provider Edison cut its FY26 EPS forecasts by 20%.

Although I don’t have access to any updated broker notes this morning, today’s warning appears to suggest another big reduction in profit guidance.

Let’s take a look.

Q3 trading

This update covers the approximate period April-June (Topps has a 52-week financial year). Trading has been lacklustre to date, although there are some signs of progress:

Group revenue -1.8% to £75.6m, including the CTD stores.

Core Topps Tiles revenue was +0.6% to £69.4m, or flat on a like-for-like basis.

On track to deliver self-help initiatives, including network optimisation, flexible labour model and head office role consolidation.

Online sales generated 23.3% revenue in Q3, an increase of 2.3% vs H1.

Sales of the new “hard surface” product category (e.g. acoustic panels, shower panels) rose by 10.9% in Q3.

Falling revenue against a backdrop of general inflation is always likely to put pressure on profits.

The weather has also caused problems, presumably contributing to today’s profit warning:

… recent periods of extreme heatwave conditions led to temporary work stoppages among housebuilders and traders, further affecting activity levels. Whilst there is likely to be a catch up over a six-month period, this is unlikely to come back fully in our financial year which ends in September.

Outlook

Whilst significant progress is being made, as set out above, the macro-economic environment has continued to be challenging, with lower consumer spend and commercial areas such as housebuilding coming under further pressure.

Topps Tiles helpfully provides explicit guidance on its revised profit expectations:

“we now expect Adjusted Profit Before Tax to be above £6.5 million”

Unfortunately, management hasn’t seen fit to include details of consensus expectations in its RNS updates to aid private investors. This makes it hard to compare this guidance to previous expectations.

Fortunately, I do have access through Research Tree to a recent broker note from Zeus that was published following the group’s H1 results in May.

Zeus’s estimates appear to be closely aligned with consensus and should be a good guide to corporate expectations prior to today’s downgrade.

The news isn’t good:

Zeus was previously forecasting FY26E adjusted pre-tax profit of £9.3m;

That means today’s guidance implies a 30% cut to FY26 PBT expectations.

Some back-of-the-envelope estimates suggest to me that pre-tax profit of £6.5m could imply adjusted earnings of c.2.4p per share.

If I’m correct, that would mean FY26 earnings forecasts had halved over the last year:

Roland’s view

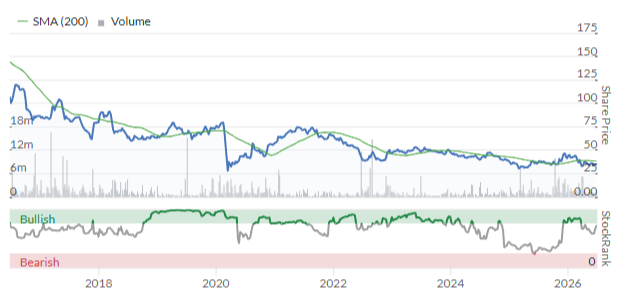

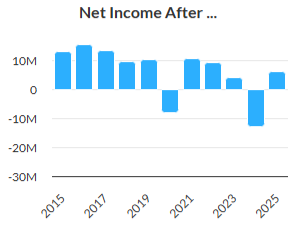

It’s been a painful decade for shareholders: Topp’s share price has been in decline more or less continuously since 2016:

The trend for profits has been slightly better, but not much:

It’s probably fair to say investors are already cautious about this business. Even so, I’m a little surprised Topps’ shares haven’t fallen further today given the apparent scale of today’s cut to guidance.

A more charitable interpretation of today’s slide may be that the market believes some weakness is already priced in. The group’s H1 adjusted EPS of 0.83p meant that an unusually heavy H2 weighting would have been needed to get anywhere near previous consensus estimates of 3.4p per share.

It’s possible that Topps Tiles’ performance will start to recover over the coming year as self-help measures take effect and – hopefully – construction market conditions stabilise.

However, our research at Stockopedia suggests that when companies warn on profits, it often marks the start of a longer period of weakness.

With two profit warnings so far this year and no sign of a more positive macro environment, I’m not tempted to call the bottom yet. I’m also discouraged by Topps’ lack of transparency when it comes to publishing consensus expectations – many companies now do this routinely and there’s no reason for others not to.

I’m going to leave my previous AMBER/RED view unchanged today.

Supreme (LON:SUP)

Down 5% at 148p (£174m) - Final Results - Roland - AMBER/GREEN =

The big question for investors in the vapes and consumer goods group is whether Supreme’s acquisition-led diversification into Drinks & Wellness can successfully reduce its dependence on vaping – and whether it even needs to do so.

This uncertainty has been reflected in the group's share price performance over the last year, although I’m encouraged by the recent increase in StockRank, which looks a bit like a jump to me:

Today’s somewhat mixed results appear to be slightly below expectations, but I think they do answer at least one of the questions above.

FY26 results summary

Revenue up 17% to £270.2m

Gross profit up 7% to £78.9m

Gross margin down 3% to 29%

Adj pre-tax profit down 9% to £27.5m

Adj EPS down 13% to 18.9p

Net cash excluding leases of £7.5m (FY25: £1.2m)

Total dividend up 4% to 5.4p per share

Earnings miss? Consensus forecasts on the StockReport show revenue of £266m and adjusted EPS of 19.6p. Two out of three new broker notes on Research Tree this morning confirm the view that today’s FY26 earnings are slightly below expectations.

Trading commentary

A look at Supreme’s three product groups individually adds some context to this situation and is broadly reassuring, in my view.

Vaping: this business obviously carries some ESG baggage and is not universally popular with investors. However, there’s no doubting Supreme’s strong presence in this sector in the UK. This was emphasised last year, with an increase in both sales and profits despite the introduction of a UK ban on single-use vapes:

Revenue up 15% to £148.1m

Gross profit up 0.3% to £47.0m

Gross margin: 32% (FY25: 36%)

While gross margin fell, Supreme says it has negotiated the switch to reusable vapes successfully, adding new brands to its distribution portfolio and maintaining its leading role as a manufacturer and distributor:

Our ability to retain every major retail customer and guide them through the transition from disposable vapes to pod systems - following our guidance on range and SKU count - highlights our position as a leader in the UK vaping market.

A further tightening of the rules is due later this year, when a new vaping duty regime is due to be introduced. Detail planning is well progressed and once again, the company expects to have an advantage over smaller competitors in this more complex environment:

We have spent a significant portion of the second half of FY26 preparing for its introduction: adapting our manufacturing processes to accommodate digitised tax stamps, reviewing packaging requirements, applying for duty suspension arrangements and reconfiguring certain warehousing operations. The operational implications are complex, but we are well-resourced and well-prepared.

This situation is consistent with what we often see in regulated industries. Tighter regulations generally favour larger incumbents – I don’t see any reason to doubt that outcome here, even if gross margins do settle at a lower level than in the past.

Drinks & Wellness: this area has been a major focus of the group’s acquisition activity over the last couple of years. The impact on division results last year was pretty notable:

Revenue up 60% to £69.3m

Gross profit up 62% to £21.5m

Gross margin: 31% (FY25: 31%)

Notable deals include Typhoo Tea and more recently, Slimfast.

The group’s new black tea manufacturing facility (‘The Plant’) produced c.380m tea bags last year and is expected to “more than double output in FY27 on an almost identical cost base”. Supreme says it has stabilised retail listings and permanent pricing for Typhoo, replacing “an inconsistent, price-led approach”.

Slimfast was acquired for £20.6m in October 2025 and is said to have been immediately earnings enhancing, but will require some investment, having been “somewhat under-invested prior to our acquisition”.

Of the group’s in-house brands, Sports Nutrition offering Sci-MX is growing strongly and was the “UK’s feast-growing vegan powder on the market” last year.

Soft Drinks are another area of growth, with sales up 41% to £26.3m last year. This includes Clearly Drinks (another previous acquisition) and various cross-sold third party brands produced in the company’s manufacturing plant. Two energy drink licence agreements were also signed post-period end in May.

Electrics and Household: this is the oldest part of the business, which started life as a battery distributor. Unfortunately this division was also the weakest performer last year, accounting for much of the drag on profitability.

Revenue down 10% to £52.8m

Gross profit down 26% to £9.0m

Gross margin: 17% (FY25: 21%)

This decline was mainly due to two changes outside the company’s control:

Panasonic withdrew from the UK battery market, a move described by Supreme as “swift and unexpected”. Lost volume has been replaced by alternative brands, but this took time and led to a temporary drop in revenue.

Amazon moved to a direct supply model with battery suppliers, cutting out the reseller channel through which Supreme had previously distributed. This appears to be another example of Amazon founder Jeff Bezos’ reported mantra that “your margin is my opportunity”.

More positively, the 1001 cleaning brand acquired last year is said to have “performed solidly” and contributed £2m of revenue last year. It is “beginning to demonstrate the cross-sell potential we envisaged at the time of acquisition”.

Profitability & Balance Sheet

Last year’s double-digit fall in an adjusted earnings tells us that the group’s profitability came under pressure last year:

Gross profit up 7% to £78.9m

Administrative expenses up 14% to £50.4m

Operating profit down 12% to £28.5m

Operating margin: 11% (FY25: 14%)

Return on capital employed: 27% (FY25: 36%)

To be honest, I don’t think this is a particularly bad outcome. Aside from the likely increases in labour and energy costs, Supreme invested heavily in upgraded production facilities to support recent acquisitions and growth plans. A 14% rise in overheads seems reasonable to me in this context.

To its credit, the company’s finance costs remained stable and the group ended the year with an improved net cash balance of £7.5m.

Cash generation was also strong. My sums show free cash flow of nearly £12m from a net profit of £18.4m. Given that capex rose to c.£18m last year against a normal run-rate of c.£5m, I think this is a good result that highlights the cash-generative qualities of the business.

Outlook

Supreme has had a positive start to FY27, supported by solid customer traction for existing and new products with current trading in line with market expectation.

The consensus EPS estimate for FY27 is shown as 19.8p on the StockReport, but updated forecasts from three brokers covering Supreme suggest a slight reduction to this is likely:

Zeus FY27E adj EPS: 20.4p (-1% vs 20.6p previously)

Shore Capital FY27E adj EPS: 18.6p (-1% vs 18.7p previously)

Edison FY27E adj EPS: 19.1p (-5% vs 20.0p previously)

Averaging these three forecasts gives me a new FY27 consensus EPS estimate of 19.4p.

Achieving this would represent modest 3% growth from the 18.9p figure reported for FY26 today. However, with revenue expected to rise by c. 13% in FY27, these earnings forecasts suggest the decline in margins seen last year may continue for a little longer.

Roland’s view

Supreme’s Drinks & Wellness division appears to be scaling up nicely. Over time, I think it’s fair to conclude that this should reduce the group’s dependency on vaping profits – probably a positive change, overall.

Based on today’s results and outlook, I think the shares look reasonably priced. However, the fact that margins are expected to continue declining in FY27 could make it hard to justify a much stronger valuation in the short term. Less profitable businesses are often less valuable, regardless of revenue growth:

The sin sector discount applied to the vaping business could also continue to keep a lid on the stock’s valuation. Leaving aside personal preferences, there is always the risk that future governments could apply more draconian restrictions to the sale of vaping devices, for example by making them available through pharmacies only (as in Australia).

Some investors see CEO Sandy Chadha’s 54% holding in Supreme as a negative, due to the control it gives him. Personally, I think the alignment it provides with shareholders is more valuable than any risk he might decide to take the company private at a bargain valuation.

In my view, Supreme has a decent record of generating attractive returns on its assets and building value. With the stock trading on a single-digit P/E despite generating double-digit returns on equity, I’m happy to maintain my previous AMBER/GREEN view today.

See what our investor community has to say

Enjoying the free article? Unlock access to all subscriber comments and dive deeper into discussions from our experienced community of private investors. Don't miss out on valuable insights. Start your free trial today!

Start your free trialWe require a payment card to verify your account, but you can cancel anytime with a single click and won’t be charged.