Good morning!

Today's Agenda is complete. Spreadsheet accompanying this report: link.

Companies Reporting

| Name (Mkt Cap) | RNS | Summary | Our view (Author) |

|---|---|---|---|

Reckitt Benckiser (LON:RKT) (£39bn | SR70) | Sales ahead of expectations. Revenue up 5% LFL with adj operating profit up 2% to £3,543m. Growth driven by Core Reckitt including Dettol, now the largest brand by revenue. Outlook: expect Core Reckitt LFL revenue growth of 4% to 5%. Q1 revenue affected by weaker cold and flu season. | ||

Aviva (LON:AV.) (£20bn | SR64) | Operating profit up 25% to £2,203m, including £174m contribution from Direct Line. Operating earnings per share rose by 17% to 56p, with the dividend up 10% to 39.3p. £350m buyback. New three-year targets of 11% CAGR EPS growth, Return on Equity >20% and cash remittances of >£7bn. | AMBER/GREEN = (Roland - I hold) I don’t see too much to dislike in these results, with solid growth from the core insurance business and good cash generation. If return on equity can be sustained at last year’s high-teens level, then I think the current 6% dividend yield could still represent an attractive valuation. I’m leaving our previous broadly positive view unchanged today. | |

Associated British Foods (LON:ABF) (£13.7bn | SR81) | Appointment of Primark Chief Executive & ABF Chief Financial Officer | Joanna Edwards appointed as Group CFO, she has served as Interim CFO since March 2025 and was previously Group Financial Controller. Eoin Tonge appointed as Primark CEO having been interim CEO since March 2025. He was previously ABF Group CFO. | |

Rentokil Initial (LON:RTO) (£10.8bn | SR67) | Revenue up 4.4% to $6,908m, adj pre-tax profit up 4% to $876m. Adj EPS up 2.4% to 25.91c, leverage reduced to 2.6x EBITDA. On track to deliver NAm 2027 targets for $100m of cost savings and 20% margin. 2026 outlook: expect to deliver full-year results in line with market expectations. | ||

Admiral (LON:ADM) (£8.8bn | SR41) | “2025 was an exceptional year for Admiral”. Turnover -1% to £5.9bn, adj pre-tax profit up 16% to £957.9m, with adj EPS up 16% to 247.4p. Dividend per share up 7% to 205p. Return on equity -3% to 53%. | ||

Harbour Energy (LON:HBR) (£4.1bn | SR82) | “We delivered excellent operational performance while maintaining capital discipline and integrating new assets.” Production up 84% to 474kboepd, operating cost -22% to $12.8/boe. 2P reserves and 2C resources of 3.0bn boe (2024: 3.2bn boe). Adj pre-tax profit up 50% to $0.6bn, free cash flow of $1.1bn. Dividend of 8.05c in line with new policy (2024: 26.2c). Outlook: production to be 475-500kboepd w/ unit op costs of $14.5/boe and free cash flow of c.$0.6bn at $65/bbl Brent. | ||

Entain (LON:ENT) (£3.7bn | SR42) | NGR +7% inc BetMGM, with Entain +3% and BetMGM +33%. Adj pre-tax profit down 2% to £507.2m, with net loss of £(680.5)m. Outlook: “remain comfortable with market expectations for FY26 Group Underlying EBITDA”. Expect to mitigate about 25% of UK gaming tax increases, rising to 50% in FY27. | ||

Taylor Wimpey (LON:TW.) (£3.6bn | SR73) | Revenue up 13% to £3.8bn, adj operating profit up 1.1% to £420.6m. Completions up 6% to 11,229 units. Adj EPS down 4.8% to 8.0p, dividend down 20% to 7.62p per share. Net cash of £342.6m (2024: £564.8m). £53m share buyback. 2026 Outlook: “Spring selling season has started well”, but affordability remains challenging. Expect completions of 10,600-11,00 with lower profit margins resulting in adj op profit “around” £400m. | BLACK? (AMBER=) (Roland) [no section below] I discuss housebuilders in more detail in a new article published today. These results from Taylor Wimpey appear to be broadly in line with expectations, but as I speculated could happen, the dividend has been cut to restore earnings cover in the face of a dwindling net cash balance. Looking ahead, I’d also note that management expects margins to remain under pressure this year, with a small decline in completions. There will also be a heavier H2 weighting than usual, with around 60% of completions expected in the second half. Arguably, this increases the risk of a cut to guidance later this year if conditions don’t improve. Today’s 2026 profit guidance is for adjusted operating profit to fall by c.5% to around £400m. I don’t have access to any broker forecasts, but my impression is that this might be slightly below previous consensus. Overall, I’m happy retaining my previous neutral view here given the c.15% discount to book value. However, as I discuss in today’s article, I think there could be better choices elsewhere in this sector currently. | |

3i Infrastructure (LON:3IN) (£3.2bn | SR91) | Selling 71% stake in TCR for c.€1,140m, a 22% uplift from 30 Sept 25 valuation. Buyer not specified. TCR is the largest independent lessor of airport ground support equipment. | ||

Serco (LON:SRP) (£3.0bn | SR87) | Revenue up 3% cc (+1% organic) to £4.9bn. Adj operating profit up 1% to £272m, adj EPS up 2% to 16.93p. 2025 order intake £5.5bn, with book-to-bill of 114%. Around two-thirds of new business in defence. Total order book up 9% to £14.5bn. Outlook: FY26 guidance unchanged for 3% organic revenue growth and adj op profit of c.£300m. | ||

ITV (LON:ITV) (£3.0bn | SR89) | “We remain in discussions with Sky regarding a possible sale of the M&E business”. Revenue up 1% to £3,511m, adj pre-tax profit down 5% to £448m. Adj EPS down 11% to 8.5p, total dividend held at 5p per share. 2026 Outlook: expect “good growth” in total revenue with EBITA margin at lower end of range. Expect H2 weighting to revenue and profit due to timing effects. | PINK | |

Drax (LON:DRX) (£2.9bn | SR97) | CFO Frank Lemmink is taking a six-month leave of absence to support his recovery from a health issue. Deputy CFO Daniel Peacock has been appointed interim CFO in his absence. | ||

| Osb (LON:OSB) (£2.0bn | SR84) | Preliminary Results | Net loan book up 3.2% to £24.9bn, with net interest income down slightly to £679.4m (NIM:2.28%). Pre-tax profit down 9% to £382.5m with TNAV per share up to 579p due to reduced share count. Total dividend of 35.3p (+5%) as per guidance. | |

Grafton (LON:GFTU) (£1.77bn | SR93) | FY adj op profit “ahead of expectations”, up 7.1% to £190.2m. This was driven by an acquisition in Spain. Improved gross margins supported an operating margin of 7.3% (FY24: 7.6%), reflecting cost pressures. 2026 outlook: Ireland and Spain are positive, but the exit rate of trading in the UK was weaker than expected. | ||

Coats (LON:COA) (£1.68bn | SR68) | Revenue up 2% to $1,465m, adj EBIT up 7% to $290m with EPS down 5% to 9.3c. Net debt up to $815m (2024: $449m). Gained market share in weak markets and exited non-core US Yarns business. Ortholite acquisition delivered FY profit in line with exps. Outlook: expect organic growth despite weak external conditions. Warn of potential impact of events in the Middle East. | ||

Lancashire Holdings (LON:LRE) (£1.56bn | SR86) | GWP up 5% to $2,259.3m with insurance revenue up 5.4% to $1,860.4m. Net profit down 9% to $293.4m, with return on equity of 20.9%. Additional special dividend of $0.50 per share, total dividend for year of $1.23 per share (c.91p). | ||

Senior (LON:SNR) (£1.26bn | SR63) | Senior confirms that, on 21 February 2026, it received a preliminary, non-binding all-cash offer from Arcline Investment Management. Discussions with Arcline and other potential offerors remain ongoing. | PINK | |

Elementis (LON:ELM) (£917m | SR63) | Revenue down 1%, adj pre-tax profit up 11.2% to $107.5m. Personal care revenue up 2.4%, with coatings down 4.3%. Operational improvements delivered $18m cost savings and improved capacity utilisation. Outlook: expect “another year of progress”. | ||

Hunting (LON:HTG) (£788m | SR83) | Results for the year ended 31 December 2025 & Cost Reduction Plan & Update to Capital Allocation | Revenue down 3%, EBITDA up 7% to $135.7m. Adj EPS up 9% to 34.1 cents, with total dividend up 13% to 13.0 cents per share. 2026 guidance for EBITDA of $145-155m unchanged, with EBITDA-FCF conversion of at least 50%. Targeting additional c.$15m cost savings and new $40m buyback to be executed up to March 2028. | |

Spire Healthcare (LON:SPI) (£785m | SR34) | Revenue +4.5%. Adjusted operating profit £150.5m (2024: £149.4m). Statutory PBT £18.6m (2024: £38.3m). “We are targeting FY26 EBITDA broadly in line with FY25 EBITDA within our NHS planning scenarios… during FY26 Spire will focus on cash generation, private patient opportunities, delivering more efficiency and disciplined capital investment.” | PINK | |

WH Smith (LON:SMWH) (£766m | SR36) | Group revenue +5%, or +2% like-for-like. “The Group has delivered a solid first half performance and is on track to deliver Group guidance for the year.” | ||

Pagegroup (LON:PAGE) (£587m | SR43) | Revenue -7.4% (cc). PBT £16.2m (down 67%). Cost reduction programme to save c. £15m from 2026. ”Whilst the market outlook remains uncertain due to the unpredictable economic environment, we will continue to control the controllables.” | ||

Ibstock (LON:IBST) (£474m | SR37) | Revenue +2% (£372m), adjusted EBITDA £71m (2024: £79m), in line with revised guidance. After a weather impacted start to 2026, residential construction and RMI markets expected to remain challenging in H1. Events in the Middle East to introduce new uncertainty. Actively managing production volumes and inventory which will create a margin headwind for 2026 but benefit cash generation. | BLACK? | |

Funding Circle Holdings (LON:FCH) (£439m | SR36) | Credit extended £2,453m (2024: £1,899m). Revenue £204.3m (2024: £160.1m). Adjusted PBT £20.3m (2024: £3.4m). Upgrades guidance for FY26, including PBT of at least £35m, and sets new medium-term targets through to FY29. | ||

Bloomsbury Publishing (LON:BMY) (£388m | SR55) | Sarah J. Maas has announced the publication dates of the next two novels in her A Court of Thorns and Roses series which will be published on 27 October 2026 and 12 January 2027. FY 2025/26 in line, FY 2026/27 expected to be materially ahead of previous expectations for adjusted pre-tax profit of £44.5m. | AMBER/GREEN = (Roland) [no section below] Bloomsbury is in the hit business and the market is expecting – probably with good reason – that these long-awaited new books from best-selling fantasy author Sarah J Maas will deliver the goods. Maas hasn’t published anything since 2024, but was the highest-selling author in the US that year. She has been responsible for a growing proportion of Bloomsbury’s profits in recent years and is now ready to release two new books within three months, something the company describes as “almost unprecedented”. Guidance for FY27 to be “materially ahead” of consensus suggests to me that forecasts could rise by 15%-20% – a view reflected by this morning’s share price movement. Prior to today, profit forecasts for FY27 were flat on FY26 so this represents a welcome return to growth. I estimate a pro forma FY27E P/E of 12 following this morning’s news – at this level I’m happy to retain our broadly positive view and would guess that the eventual FY27 results could be ahead of these expectations. I’m not going completely positive today because Bloomsbury’s recent performance has highlighted the company’s dependence on a handful of hit authors – and there’s no guarantee Maas won’t take another long break after these have been published. | |

Foresight Solar Fund (LON:FSFL) (£350m | SR54) | NAV was £545.9m at 31 December 2025. NAV per share 99.2p. | ||

Seraphim Space Investment Trust (LON:SSIT) (£339m | SR95) | NAV per share +20.1% (142.3p), due to private portfolio fair value gain (portfolio valuation +27.6%) less performance fee provision and costs. Measured according to fair value, 70% of portfolio companies are fully funded. 7% are funded for 12 months or more. | ||

FW Thorpe (LON:TFW) (£311m | SR73) | Revenue -2.4%. Adjusted operating profit -0.8% (£12.5m). PBT +3.1% (£11.6m). Special dividend due to absence of M&A. “...the outlook for growth for the second half remains a challenge, especially considering the strong second half achieved in 2024/25.” | ||

Hargreaves Services (LON:HSP) (£248m | SR98) | HSP has been appointed by Balfour Beatty and awarded an enabling earthworks subcontract at Lower Thames Crossing representing aggregate gross revenues of £10m. Thanks to contract awards and increased revenue visibility, they upgrade market expectations for Revenue and Profit before Tax for FY May 2027 by 4% each. | ||

Cab Payments Holdings (LON:CABP) (£223m | SR51) | Further response to firm offer announcement & Full Year 2025 Results | Offer from Helios Consortium “highly opportunistic and fundamentally undervalues CAB Payments”. 2025 total income +12%, adjusted EBITDA +14% to £35m. Reported profit after tax down 4% to £13.6m due to restructuring costs and higher tax. Expecting to face interest rate headwinds going into next year, as global interest rates fall. | PINK |

Vertu Motors (LON:VTU) (£187m | SR84) | The new car market remains challenging due to the Zero Emission Vehicle mandate impacting manufacturers and retailers alike. Full year FY26 adjusted profit before tax expected to be in line with market expectations. | ||

LBG Media (LON:LBG) (£138m | SR79) | The new CFO will take up his role on 9th March. His most recent role was as CFO at Inspired Thinking Group, a technology-enabled marketing services and software business. | ||

Foxtons (LON:FOXT) (£136m | SR57) | Revenue +5%, adjusted operating profit £22.2m (2024: £22.1m). 2026: letting to remain resilient, Renters’ Rights Act to create medium-term growth opportunities. The London sales market remains challenging with weak consumer confidence. | ||

RM (LON:RM.) (£101m | SR39) | Revenue -2.5%, PBT from continuing operations £3.2m (previous year: £12.1m loss). Adjusted net debt £50.6m. Trading in the first months of the year has been consistent with the Board’s expectations, with the full-year outlook remaining in line with expectations. | ||

Strategic Minerals (LON:SML) (£91m | SR33) | Assay results from drillhole CRD039, including ultra-high-grade intersections and long intersections of high-grade mineralisation from the Redmoor Tungsten-Tin-Copper Project in southeast Cornwall. | ||

Hansard Global (LON:HSD) (£70m | SR62) | Present value of new business premiums £49.2m (H1 2025: £49.1m). PBT £2.6m (H1 2025: £0.5m). Interim dividend unchanged at 1.8p. | ||

Rentguarantor Holdings (LON:RGG) (£42m | SR25) | Revenue +87% to £2.4m. Operating loss £1.38m. Year-end cash reserves £2.05m. The first two months of 2026 are showing further growth in revenues. | RED = (Graham) I’m staying RED on this due to the heavy cash burn in 2025, which I look into in greater detail in the section below. However, I am open to changing my mind on this stock if it becomes clear that it’s on track to break even, and if I can be convinced that it is fully funded through to profitability. It has the potential to be a really high-quality investment, in my view. But as it currently trades on 10x forecast sales, and the actual historic financials are poor, I think it’s right to stay sceptical. | |

Predator Oil & Gas Holdings (LON:PRD) (£26m | SR13) | Independent Technical Report by Scorpion Geoscience for the proposed Snowcap-3 well. 2P resources of 8.73 MM bls. Project economics based on US$60/bo. | ||

Inspiration Healthcare (LON:IHC) (£21m | SR46) | Has been re-appointed by the NHS supply chain as an approved supplier for its respiratory care units for newborns under a new four-year framework agreement covering England and Wales. | ||

Zenith Energy (LON:ZEN) (£20m | SR42) | Acquisition of an additional photovoltaic development project in the Puglia region of Italy. Expected to reach Ready-to-Build status by February 2027. Total consideration €1.05m. | ||

Robinson (LON:RBN) (£20m | SR63) | Revenue down 0.4%. Underlying operating profit £3.6m (2024: £3.2m). Operating profit for the 2026 financial year to be in line with current market expectations, and PBT to benefit materially from property disposals. | ||

Vulcan Two (LON:VUL) (£15m | SR20) | Long-term lease agreement for a new 22,000 sq ft distribution centre in Leeds. | ||

Xeros Technology (LON:XSG) (£12m | SR11) | XSG’s manufacturing partner Donlim has received a Purchase Order from MediaMarkt, Europe's largest consumer electronics retailer for an initial production run of XF3 units. | ||

Cordel (LON:CRDL) (£11m | SR18) | The contract moves to a new Strategic LiDAR Program under a fixed monthly fee, Software as a Service (SaaS) model, moving away from a per-order approach. Delivering Cordel in excess of US$600k in 2026. |

Graham's Section

Rentguarantor Holdings (LON:RGG)

Unch. at 28.9p (£42m) - Full Year Results - Graham - RED =

RentGuarantor (AIM: RGG), a provider of rent guarantee services to prospective tenants across the socio-economic spectrum wishing to rent property in the UK private rental sector, is pleased to announce its audited financial results for the year ended 31 December 2025 ("FY2025").

This stock moved onto AIM last August, and I’ve been a keen follower since then. Despite its strong growth rates, I have struggled to understand the valuation it has achieved. I’ve also found the frequency at which it publishes RNS announcements rather offputting (there were five in February!).

But let’s try to keep an open mind as we review these full-year results.

Highlights:

Revenue +87% to £2.39m

Operating loss £1.38m (“or £817k excluding AIM Admission costs and accelerated marketing spend”)

Year-end cash reserves £2.05m

I can understand leaving out AIM admission costs from adjusted profit measures, but I’d have some difficulty when it comes to accepting the exclusion of marketing spend.

Additionally, the £2.05m cash balance should be considered in the context of the company raising £4m during the year. There has clearly been a significant cash drain, over and above the £1.38m operating loss, given that the company entered 2025 with a small net cash position.

Outlook

While there have been plenty of operational updates in the new year, the only financial guidance is that “the first two months of 2026 are showing further growth in revenues.”

We do also get an interesting note on the impact of the economy:

The current economic climate in the UK, combined with the Renters' Reform Act, presents a significant growth opportunity for RentGuarantor to scale its operations and establish itself as the leading provider in its sector. There has never been a more critical time for both landlords and tenants to protect their positions with a reliable rent guarantee solution. Landlords cannot afford sustained rental losses, and tenants benefit from avoiding the added stress and risk of potential possession proceedings…

With rental property likely to remain in limited supply, upward pressure on rents is expected to continue. At the same time, the private rental sector is undergoing substantial legal and digital transformation. RentGuarantor is well resourced, strategically positioned, and equipped with the expertise to capitalise on this shift and secure a valuable first-mover advantage.

CEO comment is pleased with the spending that was enabled by the fundraising efforts:

"FY2025 marked a pivotal year for RentGuarantor, with strong revenue growth, a strengthened balance sheet and meaningful strategic progress across the business. Revenues rose 87% to £2.39 million, and our improved cash position, underpinned by the total of c. £4 million raised in 2025, has enabled us to invest confidently in marketing, technology, product advancement and team expansion.

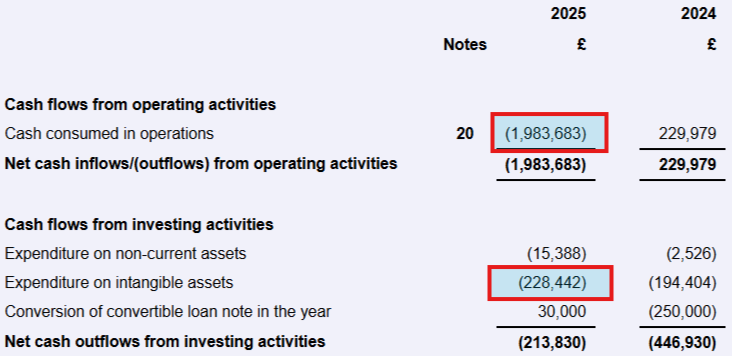

Cash flow analysis

As I try to get a greater understand of where the money has gone, here is the cash flow statement:

Checking footnote 20 (cash flow from operating activities), I see that over £700k left the company as it reduced outstanding payables.

Another footnote reveals that most of this (over £400k) was due to a reduction in “amounts due to related parties”. There is a long footnote explaining the related party transactions between the CEO and company itself.

To be clear, I’m not saying this to raise any suspicions - this is all fairly normal when studying smaller companies. I just think it’s worth understanding how the company managed to burn through over £2m when the operating loss was only £1.4m.

Graham’s view

You may wonder why I continue to study this company when I am so consistently negative about it.

The reasons are:

1. Very fast top-line growth. We don’t regularly get to study companies whose revenues are almost doubling year-on year.

The mission statement as expressed by RGG’s CEO is:

Unlike other property portals who have a subscription-based model with estate agents, Paul has a vision for RentGuarantor as being the premier online place to go for landlords and tenants.

It’s not easy, but I’m interested in finding quality businesses at an early stage in their development, before their quality is widely understood. RGG strikes me as something that has the potential to achieve this.

But I’m clearly not the only person who thinks this, as the shares apparently offer very little value. The ValueRank is only 13.

Given the lack of profitability, I think price to sales is the multiple we should be looking at: based on 2026 forecast sales of £4m, this is trading at 10x sales.

Even for a thriving, profitable SaaS business, that would be a demanding valuation.

Therefore, I am going to stay RED on this for the time being.

But I’ll be watching it closely. Forecasts suggest that it can turn a profit this year.

If RGG looks like it is on track to break even in 2026, and if I’m convinced that it’s fully funded through to profitability, my stance on this is likely to change very quickly. I could go straight to neutral at that point.

So I’m staying negative for now, but am very open to changing my mind - perhaps at the interim results this year.

Roland's Section

Aviva (LON:AV.)

Down 2% at 653p (£20.0bn) - 2025 Results - Roland - AMBER/GREEN =

(At the time of publication, Roland had a long position in AV.)

Today’s results from this FTSE 100 insurer have received an indifferent reception from the market, but look pretty healthy to me. As far as I can see, they suggest investors can remain confident in the medium-term outlook for the business (and the dividend).

2025 results summary

Headline numbers show a big rise in profit and improved profitability, with CEO Amanda Blanc reporting that the business has achieved its “2026 financial targets one year early”.

Operating profit up 25% to £2,203m, including £174m contribution from Direct Line

Operating profit rose by 15% excluding Direct Line

Cash remittances up 4% to £2,077m

Return on equity up 1.8% to 17.5%

Operating earnings per share up 17% to 56.0p

Full-year dividend up 10% to 39.3p per share

£350m share buyback

In a nutshell these figures show us that the group’s profits generated an attractive return on equity, reflecting the company’s capital-light strategy. Aviva says 68% of its profit is now from capital-light businesses.

Cash generation is another strength – broadly, the cash remittances figure above of £2,077m represents post-tax surplus cash returned to Aviva from its operating subsidiaries. This means that it’s a good proxy for the amount of cash available to support dividends and buybacks (as long as regulatory capital coverage ratios remain adequate, as they are here).

In this case, last year’s cash remittances comfortably cover the 2025 dividend of 39.3p (£1.2bn) and new £350m buyback.

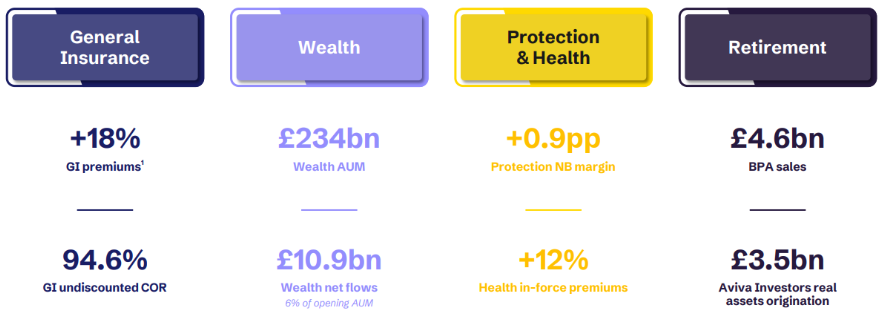

Divisional trading: Growth was positive across all four of Aviva’s operating segments, as this slide from today’s presentation illustrates:

General Insurance (UK & Ireland): volume and profitability improved, with gross written premium up 27% to £9,787m and operating profit up 52% to £708m. The discounted combined operating ratio for the year was 89.7% (2024: 90.9%). A figure under 100% represents profitable underwriting.

Canada General Insurance: Aviva is Canada’s second largest Property and Casualty insurer, with a c.9% market share and 2.6m customers.

In 2025, gross written premiums rose by 2% to £4,358m, while operating profit climbed 49% to £408m. Combined operating ratio improved by 2.9% to 95.6%.

Insurance, Wealth & Retirement: this business offers individual retirement products such as annuities,, wealth management and bulk annuities. Aviva has a c.25% share of the UK life insurance market and a large share of the personal annuity market, which has really strengthened since interest rates returned to more normal levels, improving annuity rates.

Last year saw bulk annuity sales fall by 41% to £4.6bn, “reflecting a more typical year”. I think this has also become quite a crowded market, perhaps explaining the slowdown.

However, overall IW&R results were boosted by strong demand for products such as Health Insurance (especially from corporate customers) and wealth management. Operating profit from these two segments rose by 53% to £204m and by +36% to £175m, respectively.

Net inflows into the Wealth business rose by 6% to £10.9bn, representing 6% of opening AUM.

Aviva Investors: this is the group’s conventional asset management business. It’s relatively small and largely serves the group’s own requirements – year-end AUM was £262bn, of which £221bn was being managed for Aviva Group businesses.

Net inflows were £1.4bn last year, but AUM rose by 10% to £262bn over the year. This suggests market performance/investment gains of perhaps 9% for the full year.

Learning more: there’s a lot more detail in the results about each division and the detailed financial mechanics of the insurance business. For anyone wanting to get an accessible overview I’d suggest starting with today’s results presentation before drilling down further if desired. While company results presentations inevitably put a positive spin on results, for complex businesses like Aviva they are also a good way to get an overall understanding of the business.

Outlook & updated financial targets

Aviva updated its three-year targets for the business in November. These are:

Operating EPS growth of 11% CAGR from 2025-2028;

Return on Equity of >20% by 2028;

Cash remittances of >£7bn cumulatively from 2026 to 2028.

Management says the group is “comfortably on track” to achieve its previous cash remittance target for >£5.8bn from 2024-26. Based on £4.1bn achieved to date, this suggests a 2026 figure of at least £1.7bn. That should provide continued support for the dividend, as a minimum.

Consensus forecasts have moved higher over the last year overall, despite recent dip:

Based on these FY26 estimates, Aviva shares are trading on a forecast P/E of 11, with a potential 6% dividend yield.

Roland’s view

I admire what CEO Amanda Blanc has achieved since taking charge at Aviva and today’s results don’t change that. If the company can maintain return on equity at the high-teens level achieved last year, then I think the current 6% dividend yield could still be a reasonably attractive valuation, despite the stock’s strong performance over the last few years:

I think Aviva remains an attractive choice for income at current levels and don’t see any reason to change our previous broadly positive view today.

See what our investor community has to say

Enjoying the free article? Unlock access to all subscriber comments and dive deeper into discussions from our experienced community of private investors. Don't miss out on valuable insights. Start your free trial today!

Start your free trialWe require a payment card to verify your account, but you can cancel anytime with a single click and won’t be charged.