Trending Value - the strategy for opportunistic bargain hunters

Who would turn away from the idea of buying bargain stocks right at the moment they have turned the corner? Discovering a hidden gem with a catalyst can lead to transformational stock returns. Many of the biggest stock market winners in any year begin their journey with low valuations, where something changes to trigger a revaluation.

Most investors love the idea, but often don’t have the stomach or the time to hunt for these kinds of shares. But the principles of this approach are time-worn and can be easier than you think to implement.

Whether you are a lazy investor with a few hours available per year, or an active trader seeking to be ahead of the pack, this guide will help you understand the elements of implementing the Trending (or Turnaround) Value approach.

Is this right for you?

Let’s be clear, this strategy is not without risk. When fishing in the bargain bucket of the market, there’s always the chance of picking a false positive. Stocks are often “cheap for a reason”.

While this is not the bargain-basement of “Deep Value” stocks, the cheaper end of the market is full of out-of-favour sectors and troubled business models. While the stock market is fairly efficient at valuing stocks on average, it’s prone to over-react on individual stocks. It must be stressed that a proportion of these types of shares do continue their decline. But the base rates are clear - trending value stocks, benefiting from change, beat the market.

The approach is often attractive to:

Opportunistic, active traders who seek out bargains, but want to minimise the chance of buying Value Traps by ensuring there’s a new trend or catalyst in place.

Cautious value investors who have a good grounding in the history of the returns to value & momentum stocks.

To be clear, this approach to investing is a dynamic strategy. It requires either active rebalancing periodically, or active selling when valuations recover. Value stocks only rarely become long-term Compounding Quality shares that should be bought and held forever.

You’ll also have to become comfortable owning names that you may never have heard of. For many investors, who seek comfort in household names or popular stocks, that’s too much to bear. But remember, as Sir John Templeton once said:

Background to the power of buying “cheap and strong”

In James O’Shaughnessy’s opus study of “What Works on Wall Street” he found that the best performing strategy, on a risk-adjusted basis, over 45 years was what he called “Trending Value”. This was a simple approach that bought the 25 shares with the highest 6 month share price strength from the cheapest 10% of the market.

The Trending Value portfolio never had a five-year period in which it lost money, and it also had a significantly lower downside during all other holding periods.

The reasons why this approach works are simple. Cheap value stocks tend to see their valuations return to their average over time (mean reversion), while strong momentum stocks tend to continue to trend (trend continuation). The combination of these two powerful factors is a profound force, not just in stocks, but in almost every asset class in the world.

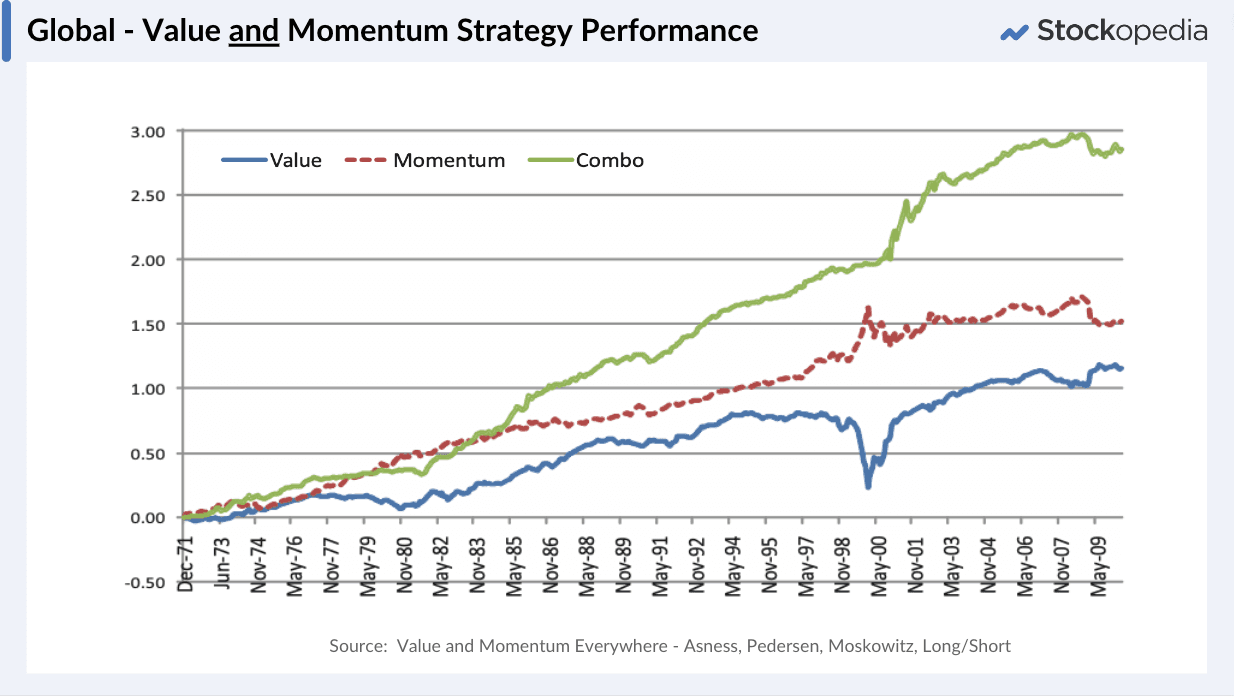

One of the greatest studies of these forces was by Asness, Moskowitz et al. in their paper “Value and Momentum Everywhere”. This extensive study by the team at hedge fund AQR showed that value and momentum drive returns in bonds, currencies, commodities, but especially stocks. The chart below from the paper illustrates that the combination of value and momentum is far more powerful than either on its own. Buying “cheap” and “strong” stocks works.

But it’s not just the quants that have all the fun with this strategy. One of my favourite books for active traders in this style is Jesse Stine’s “Insider Buy Superstocks”. Jesse famously turned $46,000 into $6.8m in 28 months by buying stocks under a P/E of 10 that broke into new uptrends on a catalyst. When cheap, forgotten stocks jump above their 30-week moving average with director buying and something new happening, there can be transformational stock returns. We’ll dig into his ideas on when to buy and sell a bit later.

Waiting for a catalyst

If you are a discretionary, stock picker or trader, you may run a more concentrated portfolio, in which case you absolutely must back up your picks with confirming qualitative research. It’s not unusual to find yourself investing in cyclical stocks at the bottom of their business cycle, asset backed stocks that have suffered from neglect, or former growth stocks that have suffered near fatal setbacks. As Jim Slater said in Chapter 11 of the Zulu Principle on cyclicals and recovery stocks:

Timing is of the utmost importance. You are looking for the first glimmer of change - the first hint of good news after the gloom.

Some things to look out for include:

Director Share Buying - when stocks get over-sold, company directors may think it’s ridiculous and buy more shares on the open market. As they’ve got more insight into the company’s operation than anyone else, this can be a highly valuable signal. Just remember, some directors do this as a PR exercise - so there can be false signals. (You can check recent Director’s Deals in the “Accounts > Directors Deals” tab on Stockopedia.)

Something New - perhaps there’s been a change in strategy, a change in management, a new product line, a shift into a new market segment, a restructuring. When something radical happens at a company, the business dynamics can be transformed and investors can think differently about it. Look for something new - it will accelerate the improvement in valuation.

Revenue or earnings jumps - due to the power of operational gearing, a company with low variable costs can see an enormous profit jump if revenues increase. If you can spot a news item, before it hits screening databases, where an out of favour stock is showing revenue improvements, you may be able to jump ahead of the crowd in entering an improving situation. Common terms to look out for in news statements are “ahead of expectations” or “significantly ahead of expectations”.

How to screen for “cheap, strong” stocks?

Let’s dig into the basic financial metrics you need to know to identify value and momentum stock winners.

1. Low valuation - cheap shares

Firstly, you’ve got to buy cheap. A stock can’t benefit from the power of its valuation returning to normal unless it starts from the lows. You want to find shares in the cheaper buckets of the market at the start of your hunt. Let’s keep things simple. You don’t need to use all these ratios, just using one from the following list can be effective as a starting point for screening.

Price to Earnings Ratio less than 8-10. Where to draw the cut-off depends on overall market conditions, but if a company has earnings, then a P/E of 8 implies an earnings yield of 12.5% - which is usually significantly above prevailing interest rates. Jesse Stine always used a P/E < 10 at the start of his hunt.

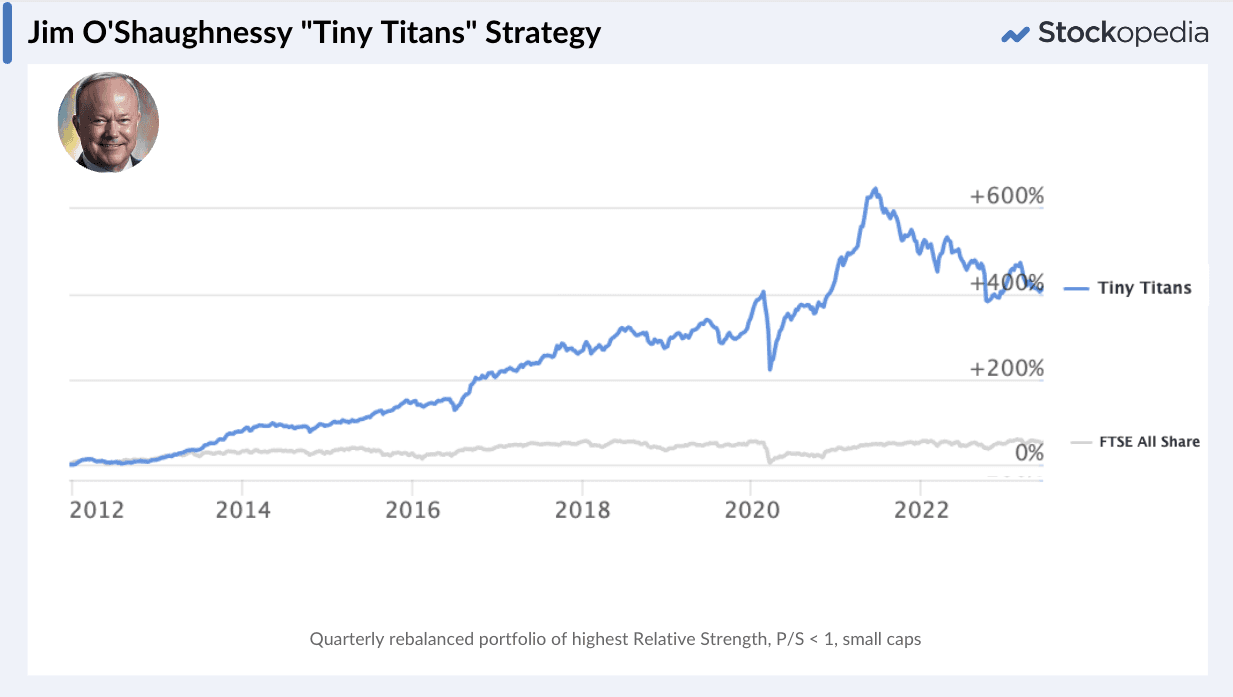

Price to Sales Ratio less than 1. Not all cheap stocks have earnings, so the P/E ratio may not always be available. When stocks are down and out, profits can slump, even into losses. But companies normally always generate sales. So using the Price to Sales ratio can include loss-makers that might rocket back once profits return. It’s out of scope for this article, but operational gearing is a powerful force where a small increase in sales can drive an enormous increase in profits. Using the P/S ratio brings some stocks into the fold that may benefit from this. P/S < 1 is the rule that O’Shaughnessy uses in his “Tiny Titans” screen - that at Stockopedia has been among the best performing screens of all time.

One of the most reliable ways to screen for cheap shares is to use a composite measure of Value. This is a combined measure of cheapness that brings together a range of different valuation ratios such as those above. At Stockopedia we have the “Value Rank” - which combines 6 valuation ratios into a score from zero (expensive) to 100 (cheapest). This makes screening for “cheap” stocks surprisingly easy.

Value Rank > 80. This would include all stocks in the cheapest 20% of the market across a range of six measures including P/E, P/S, Yield and a few others.

2. Strong price momentum or “earnings surprise”

I know this is counter-intuitive, but cheap shares really can have strong upwards trends. Too many make the mistake of trying to buy when shares are at new price lows - trying to buy a bargain - but this can be the equivalent of stock market seppuku. The trend tends to persist - so invest with the trend, not against it. You may miss out on the early part of the recovery, but it is lower risk.

We covered some signs of momentum in our Breakout Momentum piece, but in summary:

6 month Relative Price Strength - often used to sort for the highest gainers over a period, or to filter out losers. Buying winners is incredibly hard for value investors to do, as they prefer to buy out of favour stocks. Change the habit. Screen for Relative Strength 6m > 10%.

Price vs 52 week high > -10%. Stocks at or near their 52 week highest share prices have a tendency to keep on trucking, especially in the value stock basement of the market. This is a great signal when a stock has spent a long time consolidating in a base, and then pops its head up to begin a new trend.

Above the 200 day moving average - when shares trend, they trend above their longer term average price. The “moving average” is often used by active traders in chart packages (like the one at Stockopedia) to assess the right time to buy.

When things start going well in an out of favour stock, they tend to surprise to the upside. Analysts have low expectations in value stocks which makes estimates easy to beat. We’ve found that stocks surprising to the upside (both for sales and earnings) in the latest interim results period have a tendency to continue their trajectory.

Latest Sales Surprise (or Earnings Surprise) > 0 - this ensures that the company’s sales (and/or earnings) are beating estimates. Not all value stocks have estimates of course.

Momentum Rank > 90. One way of combining both price momentum with earnings momentum measures is using the Stockopedia Momentum Rank. This is a composite measure of price and earnings momentum which has been the most powerful predictor of future stock returns since the StockRanks were created.

Here are some example “Value and Momentum” Stock Screens to get you going:

The lazy investor’s guide to “trending value” investing

Kurt von Hammerstein-Equord was Commander-in-Chief of the Weimar Republic’s armed forces and an opponent of Hitler. He created a classification of officers:

I distinguish four types. There are clever, hardworking, stupid, and lazy officers. Usually two characteristics are combined. Some are clever and hardworking; their place is the General Staff. The next ones are stupid and lazy; they make up 90 percent of every army and are suited to routine duties. Anyone who is both clever and lazy is qualified for the highest leadership duties, because he possesses the mental clarity and strength of nerve necessary for difficult decisions. One must beware of anyone who is both stupid and hardworking; he must not be entrusted with any responsibility because he will always only cause damage.

The idea behind the smart, lazy approach is to understand that the forces of value and momentum drive stock returns, and put in place a reliable, repeatable process to capture them.

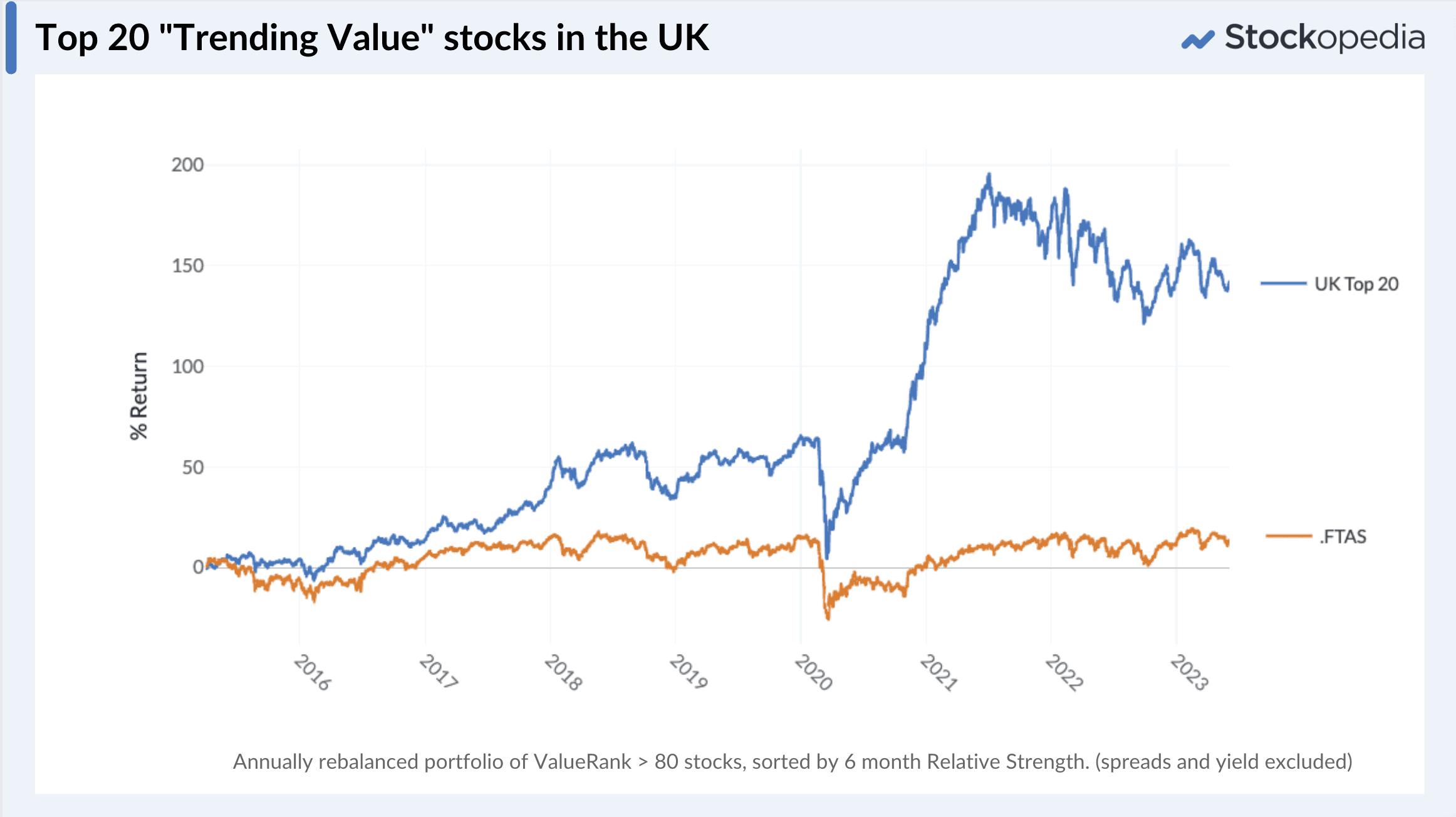

Here’s an approach inspired by James O’Shaughnessy’s Trending Value, from “What Works on Wall Street” but adapted for UK markets.

Screen the market for cheap stocks with ValueRank > 80. This means it’s in the 20% cheapest shares in the market. Also ensure the company size is greater than £20m capitalisation to weed out tiddlers.

Rank by descending 6 month Relative Price Strength to find the highest performers in that period.

Select the top 20 stocks, but ensure diversification of no more than 3 in any one sector. It’s important when building a portfolio to not put all your portfolio in 1 sector accidentally.

Buy the portfolio. Keep it simple - make all positions sizes equal (so for a £100k portfolio, buy £5k of each).

Once per year - repeat steps 1-4. If any of the names remain the same, just adjust that position back to the equal weight of the new portfolio size.

A portfolio of those rules has returned 11.3% annually in the UK market over the last 8 years.

The value shares typically in this portfolio are small to mid-cap (median £260m across the portfolios) but aren’t too hard to deal in. The average yield above was 4.7% which more than offsets the “spread” you pay to the market makers on buying and selling the shares.

Various combinations of a value filter and a momentum ranking can “work”. If you take a look at O’Shaughnessy’s “Tiny Titans” screen on Stockopedia it simply filters for P/S < 1 and sorts by price strength. These small-cap, cheap and strong shares have completely dominated the market. It’s worth being careful with these kinds of stocks, as they can be hard to deal in. O’Shaughnessy also found that the strategy had some occasionally harsh drawdowns.

The active trader’s guide to finding “breakout value” stocks

Let’s imagine you aren’t so lazy. You realise that there’s an opportunity to do even better by timing your buys and sells in value stocks. Taking this approach requires you to be a much more watchful and market monitoring individual. You are more likely to be “doing the work” - reading the news, watching market prices and staying abreast of changes in business fundamentals. You are the kind of investor who seeks to act when a catalyst appears.

Your routine would start with daily or weekly monitoring of similar stock screens to the Breakout Momentum approach but adding in a value screening filter. A good medium term trader will routinely check the charts of the candidate stocks, and monitor their news flow and company reports for catalysts.

Let’s have a deeper look at Jesse Stine’s approach to capitalising on breakout value from “Insider Buy Super Stocks”.

Fundamental Rules: the following fundamental rules are easily screenable.

Start with a P/E of less than 10. Stocks need to start cheap in this style.

Monitor small caps with low capitalisations. (Sub $100m cap). These are often the biggest movers. Stine prefers low analyst coverage.

Prefer stable earnings and revenues. Seek a jump in the latest interim or quarterly results, ideally with sequential improvement recently. Jesse likes a “blockbuster” earnings report as a catalyst that’s gone under the radar for most investors.

Ensure there’s a catalyst - has something changed or is something new? Is the stock now riding a potential super theme? Has there been significant open market buying by the company directors? Institutional buying is a solid confirming sign. (You can check these on the Ownership and Directors Dealings tabs on Stockopedia’s StockReports).

Monitor the charts. When you are an active trader, you are likely to monitor the charts for triggers, rather than using a broad approach of screening for momentum. Here’s Jesse’s approach:

Look for long, sideways trending chart patterns that have based. It adds a “layer of protection” as all the momentum traders have long since fled and downside is limited.

Wait for a price breakout above the 30-week moving average, and a high “angle of attack”. (Usually driven by the earnings change or other catalyst)

Ensure a high-volume expansion during the breakout. This shows new demand.

When to buy? Too many people buy the initial breakout only to see themselves “stopped out” during a post-breakout reversal. Jesse’s advice is to wait for the pullback, as it’s far lower risk.

Buy when the stock pulls back to its 10-week moving average (which he calls the “Magic Line”) - the “ultimate low-risk entry point”. This is often 2-3 weeks after the initial breakout.

Volume should ideally have contracted during this period as demand contracts.

If you buy a great stock, in an uptrend, after it has pulled back, your odds greatly improve.

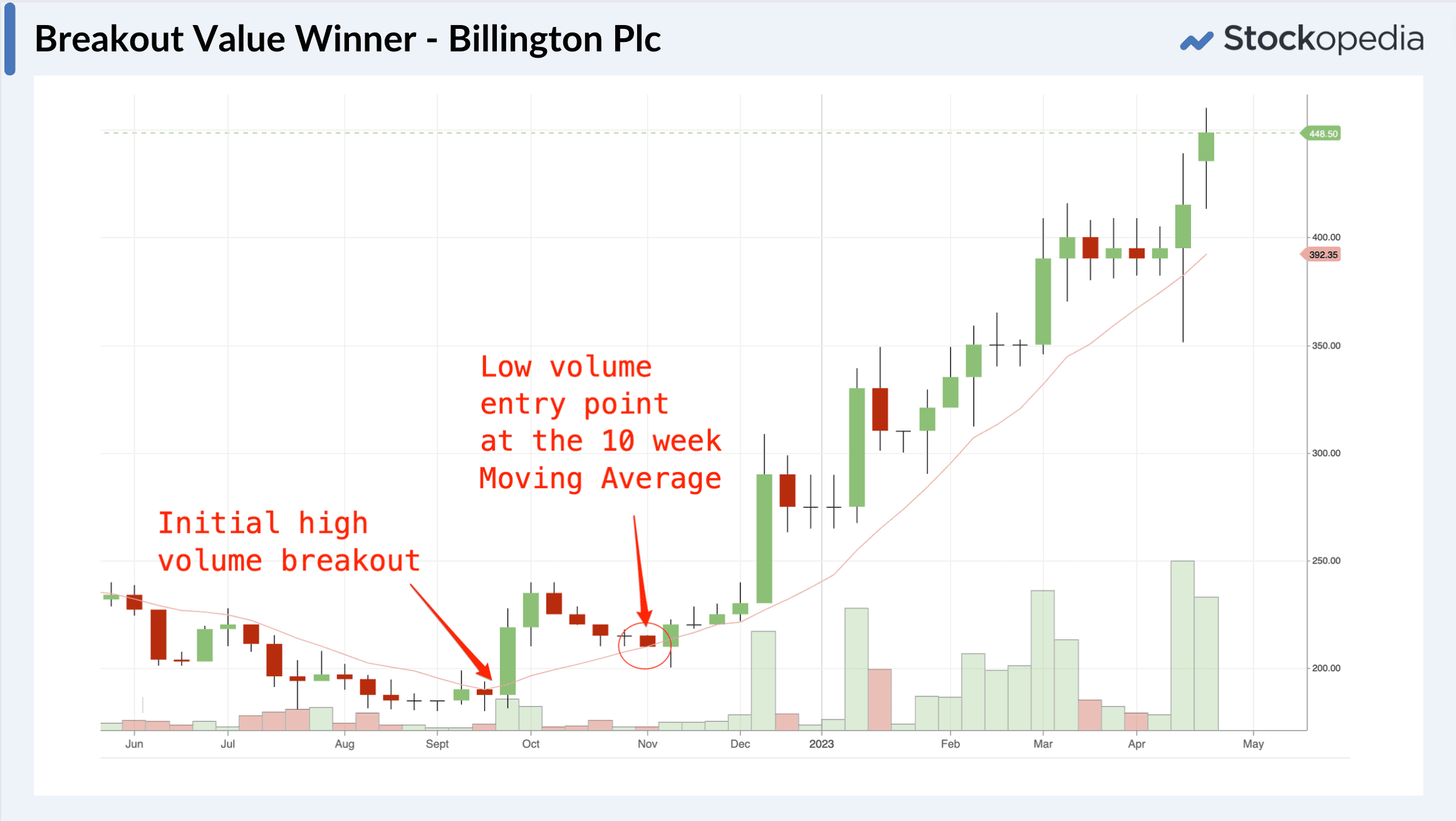

Below is an example from Billington Plc - a small-cap UK value stock on P/E ratio of 8 at the time of its initial breakout. The company announced an “ahead of expectations” trading update in September. After the initial flurry of buys, the stock sold off significantly. The low-risk entry point was at the “magic line”, before full-year results came through “significantly ahead” in December. The stock more than doubled in six months.

When to sell? Selling as a discretionary trader is an art, and there are no hard and fast rules. But to summarise some of Jesse Stine’s ideas:

Not dissimilar to Stan Weinstein’s approach as discussed in Breakout Momentum - sell after multiple surges off the 10-week moving average “magic line”, or when the chart flattens, or breaks its lower trend channel.

Sell 7-10 weeks after a surge off the magic line. The best stocks will revert back to their magic lines at least four times.

Sell parabolic blow off tops after a lengthy run, especially if there’s a large price range with high volatility.

Be extremely cautious when owning beyond the 9-month window.

Here’s an example Breakout Value Starting Screen that could be a good starting point for finding Jesse Stine Style shares. It includes a “Recent Volume Surge” rule to identify shares with higher than average recent volume. Don’t forget to check for a break above the 10-week moving average “magic line” on the charts & assess news for catalysts. This is the kind of screen that works best as part of a daily or weekly routine for active traders.

The Risks & Limitations of Trending Value

Every stock market strategy comes with its own share of risks. Trending Value is no exception. Let’s summarise some of the major concerns.

Share Price Volatility - smaller cap, value stocks can be volatile. There’s often uncertainty over the future in these kinds of stocks, which leads to quite wide daily and monthly swings in share prices. The lazy portfolio approach is to own more than 20 shares across spread sectors, but the concentrated active trader may own far fewer. Managing risk through smart diversification is key.

Uncertain Quality - some value and momentum stocks, when they complete their turnarounds, can become highly profitable. But in the mix of these stocks can be persistent loss-makers or jam tomorrow asset plays. While profitability measures can be added into the mix (for a more blended approach) to help avoid loss makers, some potentially stellar winners will be screened out by the same process.

False breakouts - buying breakouts can often lead to reversals, which can be galling in small caps. Waiting for the reversals back to a 10-week average “magic line” can reduce the risk at entry points for active traders.

Periodic Underperformance - in some growth-oriented, bull market periods, value stocks can become deeply out of favour. In the dot-com boom of 1998-200, value stocks barely nosed ahead while growth stocks roared. Trending Value can become out-of-sync with the wider market during these periods. Mitigating this is hard in smaller portfolios, though larger portfolios may seek to run twin strategies, one more value oriented while another more quality/growth oriented.

While these risks can be galling during periods of underperformance, the underlying principles behind value and momentum seem to always hold true over multi-year periods. As James O’Shaughnessy said, there has never been a 5-year period where Trending Value underperformed the market.

Closing Thoughts

The Trending or Turnaround Value approach is a time-proven, evergreen stock market strategy. It’s driven by the powerful forces of value and momentum, which are universal across not just stocks, but all asset classes. These drivers of return are persistent and pervasive.

While not without risk, anyone can implement a value and momentum strategy using simple rules. I hope this guide is useful and triggers curiosity in you to learn more about these methods.

Safe Investing!

Resources & Further Reading

Value & Momentum Everywhere - 2012 - Moskowitz et al. (The classic research paper).

What Works on Wall Street - James O’Shaughnessy (p 583 - 4th Edition) - (Trending Value)

Predicting The Markets of Tomorrow - James O’Shaughnessy (Tiny Titans)

Insider Buy Super Stocks - Jesse Stine (Breakout Value Trading)

Beat the Market: Know what stocks to buy and what stocks to sell - Charles Kirkpatrick - (Value and Relative Strength)

The Zulu Principle (Chapter 11) - Jim Slater (Recovery Stocks)