Good morning and welcome to today's report.

Spreadsheet accompanying this report: link.

12:50 - Report is complete.

Companies Reporting

Name (Mkt Cap) | RNS | Summary | Our view (Author) |

AstraZeneca (LON:AZN) (£163bn) | Trial did not achieve statistical significance for primary endpoint but did show some benefits. | ||

Rio Tinto (LON:RIO) (£71bn) | Copper production +13% YoY, iron ore +5% YoY. 2025 production and cost guidance unchanged. | ||

Antofagasta (LON:ANTO) (£18.3bn) | Copper production +10.6% YTD, gold +36% YTD. Net cash costs -32% YTD. FY guidance unch. | ||

Intermediate Capital (LON:ICG) (£5.75bn) | AUM +3% to $123bn vs prior qtr. Fee-earning AUM +4% to $82bn w/ $34bn dry powder. | ||

Zegona Communications (LON:ZEG) (£5.6bn) | Completed acquisition of Vodafone Spain. FY25 rev £3.6bn, EBITDaL £1.2bn. Net debt £3.7bn. | ||

TwentyFour Income Fund (LON:TFIF) (£867m) | NAV total return per share +13.6%, FY dividend 11.07p per share. NAV +3.7% to £843.8m. | ||

Craneware (LON:CRW) (£797m) | SP +12% FY25E EPS: $1.11 (prev. $1.08) FY26E EPS: $1.19 (unch) FY27E EPS: $1.35 (prev. $1.22) | AMBER/GREEN (Roland) [no section below] Today’s update from the US-focused healthcare software business reads well and notes an increase in net revenue retention (an analogy to contract renewals?) of 107% (FY24: 98%). This seems to support management’s claim of good momentum transitioning certain Trisus Platform revenues into recurring revenue streams. The company also comments that its partnership with Microsoft is helping to raise Craneware's profile with US hospital CIOs. The Board recently rejected a takeover proposal at £26.50. With the shares now trading at £25.20 without any bid premium, this seems to have been a solid decision by management. The strong valuation and somewhat average profitability mean there’s a risk of disappointment if momentum slows. But I’m quite comfortable taking a moderately positive view today. | |

Workspace (LON:WKP) (£763m) | LFL rent unch at £47.42, LFL occupancy -0.3% to 82.2%. Total rent roll -0.6% to £138.6m. | ||

Cohort (LON:CHRT) (£719m) | SP +14% Rev +33%, PBT +29% to £25.6m. Order book +19% to £616.4m. FY26 likely to be ahead of exps. | AMBER/GREEN (Roland) A strong set of results and upgraded outlook for the year ahead mean that I’m able to overlook the increasingly steep valuation here. This group of specialist defence companies appears to be in the right place at the right time and executing well. My moderately-positive view remains unchanged today. | |

Apax Global Alpha (LON:APAX) (£645m) | Investing €4.5m in Foods Connected, part of £22m Apax investment into HFG - see 15/7 | ||

Foresight Solar Fund (LON:FSFL) (£499m) | £50m buyback acquired 50m shares to date, adding 2.6pps to NAV. Adding £10m to buyback. | ||

Bloomsbury Publishing (LON:BMY) (£397m) | FY results to be in line with consensus exps for rev £335.9m and adj PBT of £41.6m. | AMBER (Roland) News that the company is trading in line with (reduced) consensus forecasts is reassuring, but the outlook remains that sales are expected to fall by c.7% this year. Strong paperback sales for bestseller Sarah J Maas are encouraging, but there’s no news on when a new book is due from Maas. Similarly, comments on a new AI content partnership do not include any guidance on value. I don’t see much reason to upgrade our view until there’s a little more evidence of improving momentum. | |

| Gulf Keystone Petroleum (LON:GKP) | Reports over the past two days of explosions at a number of oil fields in the vicinity of the Company’s Shaikan Field. As a safety precaution, temporarily shut-in production and has taken measures to protect staff. The Company’s assets have not been impacted. | ||

| Kenmare Resources (LON:KMR) | Q2 and H1 2025 Production Report | 25Q2 HMC production +5% on 24Q2 and +15% on 25Q due to improvement in grade. Shipments -23% on 24Q2 and -41% on 25Q1, due to poor weather and maintenance to transhipment vessels. “Kenmare no longer expects shipments to exceed production in 2025 and a further update will be provided in the H1 2025 Results.” | AMBER/BLACK (Mark) [no section below] Production here is doing well, increasing 15% on the previous quarter, mainly driven by higher grades. However, they seem unable to match that operational performance in their shipping of the products, struggling with their transhipment vessel uptime. This won’t be helped by one of the vessels entering drydock until August. I can’t see any updated research, but revenue will be booked on shipment so I have no doubt that this will impact reported profits. This is largely a timing issue. However, there is also a risk to pricing. Ilmenite is described as “stable”, but rutile and zircon saw declines. This is partly blamed for up to a $125m write-down that they will be taking to assets. This is non-cash and the company will still trade on a large discount to TBV, but the shipment delays come at a time when they have large capex commitments on the WCP A move. Net debt is now $83m and expected to rise in H2, before cash flow reduces this is FY26. This may put pressure on the company’s ability to pay its usually generous dividend. They say “the 2025 interim dividend is likely to be in the range of USc8-12/share”. Last year it was 15c. I think this remains undervalued compared to the long-term free cash flow generation. However, there is no doubt that the short-term is more uncertain than it has been recently. My view reflects that balance. |

Caledonia Mining (LON:CMCL) (£293m) | 25Q2 production 21,070oz exceeding expectations (24Q2: 20,773). Increases production guidance to 75.5 - 79.5 koz. | ||

McBride (LON:MCB) (£264m) | FY25 Adj Operating Profit in line with expectations. Revenue flat, volumes +4%. Net debt £105.2m (FY24 £131.5m). | AMBER (Mark) While I see nothing obvious in today’s update that should cause such a big drop in share price, it does highlight that the shares look fully valued at current EPS growth rates, even on the current modest rating. It may just be that shareholders who were attracted by the recent share price momentum have decided to take profits.That Momentum Rank looks likely to fall in the short term, and as such I think a neutral stance is best for the moment, at least until we get some indication that EPS can start growing again from here. | |

| Genel Energy (LON:GENL) | Production Temporarily Suspended at DNO Kurdistan Fields Following Explosions | Operator of Tawke field, DNO, suspending production following small explosion at storage tank and processing equipment. Expects to restart production once the damage assessment is completed | |

Corero Network Security (LON:CNS) (£75.5m) | PW: H1 2025 revenue will be below the prior period (at $10.9m vs $12.2m) as a result of the weaker macroeconomic environment and lower upfront capex license sales. H1 order intake $12.5m (24H1: $14.2m) below expectations. LBITDA $1.4m (24H1: EBITDA of $0.7m). Cash $3.1 (24H1: $7.9m). Discussing an overdraft. | RED/BLACK (Mark) [no section below] | |

Journeo (LON:JNEO) (£69m) | Minimum of £1.2m with Umove, Denmark's largest privately owned public transport operator. £0.8m engineering & installation this year, £0.4m software licenses over three years. | GREEN (Roland) [no section below] This small cap tech firm was one of the top performers in Ed’s NAPS portfolio in H1 and continues to look potentially attractive to me – a view supported by a high StockRank. This contract looks to me like good incremental business with an existing customer, with the potential for further work in the future. I don’t expect any change to forecasts, but I continue to think the stock looks reasonably priced on a cash-adjusted P/E of c.12. | |

Synectics (LON:SNX) (£56m) | Awarded two gaming contracts for $2.5m & $0.6m. Delivered in current financial year. | AMBER/GREEN (Roland - I hold) [no section below] These are casino wins in Manila ($2.5m) and Oklahoma US ($0.6m). Both are for the company’s Synergy suite of surveillance tools. CEO Amanda Larnder says these “further underpin the Group’s revenue” for the current year. These appear to be business-as-usual wins that are already priced into forecasts, as there’s no change to broker estimates today. My view also remains unchanged – see our review of the recent H1 results for more detail. | |

Creightons (LON:CRL) (£29.4m) | Revenue +1.6% to £54.1m. EBITDA +57.9% to £5.1m. Adj EPS +131% to 3.29p, Net cash £3m. | AMBER (Mark) | |

M Winkworth (LON:WINK) (£27m) | Sales interest remained buoyant in Q2. However, lettings activity was more subdued, lettings revenue +3%. Opened three new offices & resold two franchises. PTP to 31 Dec expected to be £2.6m in line with market expectations. | AMBER (Mark) [no section below] | |

Vianet (LON:VNET) (£27m) | “The positive momentum reported across both divisions at the time of our Full Year results has continued, with the business making further progress in line with management's growth expectations.” | AMBER/RED (Mark) [no section below] | |

Wynnstay Properties (LON:WSP) (£20.5m) | Portfolio fully let, no material rent arrears, three properties re-leased at higher rents in the quarter. | ||

Itaconix (LON:ITX) (£17m) | “..a renewed global agreement with Croda in odour control, extending and expanding a successful supply collaboration that began in 2017 and was last renewed in 2022.” | RED (Mark) [no section below] | |

Cordel (LON:CRDL) (£15.7m) | Rev +8% to £4.79m, Cash £1.50m (FY24: £1.02). | RED (Mark) [no section below] |

Roland's Section

Bloomsbury Publishing (LON:BMY)

Up 3% to 503p (£410m) - AGM Trading Update - Roland - AMBER

Bloomsbury Publishing Plc (LSE: BMY), the leading independent publisher, provides the following trading update ahead of the Company's Annual General Meeting ("AGM") at 12.00pm today.

The Board expects to deliver full year results in line with consensus expectations.

Today’s AGM update from Harry Potter publisher Bloomsbury confirms that trading for the current financial year (y/e Feb 26) is in line with consensus forecasts, which were cut by 6.6% following the group’s recent results:

The company also uses today’s update to highlight some recent operational progress:

Consumer division: Romantasy author Sarah J Maas has “topped bestseller lists again in the UK and US” following the launch of paperback editions of two of her books in June. This is good news, but of course these aren’t new books and there still appears to be no comment on when the next new Maas book is due.

The company’s other big hitter in commercial terms is Harry Potter. Bloomsbury continues to work on ways of refreshing and repackaging these stories to stimulate sales and is launching a “Pocket Potters” series in August.

Non-Consumer Division: the integration of Rowman & Littlefield has continued post-acquisition and over 5,300 of its titles are now available in digital format through the Bloomsbury Digital Resources service.

The company has also signed its first “non-exclusive content partnership”, which a note this morning from h2Radnor indicates is with an AI company. There’s no indication of the commercials of this deal.

Roland’s view

Bloomsbury took a nasty fall in May when the company issued what – in our view – was a fairly cautious outlook statement for the year ahead.

Today’s AGM update doesn’t change this outlook and appears to confirm expectations that revenue will fall by 7% this year, while adjusted pre-tax profit will be broadly unchanged.

I’ve long had some concerns about the company’s dependence on a small number of authors for the majority of its profits. I'm also not yet convinced that the acquisitive non-consumer division is delivering much in the way of organic growth.

While past growth has been impressive, driven largely by JK Rowling and Sarah J Maas, profitability in this business is only slightly above average. I don’t see that the shares deserve a strong rating unless the top line is growing.

The current valuation on c.12x forward earnings and a 3.4% dividend yield looks reasonable to me.

Megan downgraded Bloomsbury to AMBER in May, reflecting a neutral view. While today’s update is encouraging as far as it goes, I don’t see any reason to change this view today.

Cohort (LON:CHRT)

Up 14% to 1,745p (£822m) - Final Results - Roland - AMBER/GREEN

Cohort has reported another record revenue and profit performance, with robust operating cash generation and a record closing order book stretching out into the mid-2030s.

Shares in this defence group have tripled over the last two years, as the business has returned to profit growth and benefited from a significant valuation re-rating. Cohort’s share price is remarkably up by 70% since February alone, when we last covered this company:

In fairness, my impression is that the growth of recent years has been due both to the obvious external factors and to internal progress, as problems have been addressed and the group’s subsidiaries have continued to develop.

There was also a substantial (£75m) acquisition in November of Australian firm EM Solutions.

Today’s results look strong to me and are further enhanced by guidance that results for the current 25/26 years are now expected to be ahead of previous expectations. Let’s take a look.

FY25 results

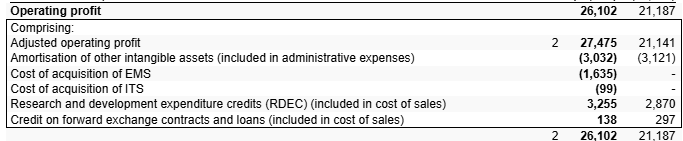

Today’s results cover the year ending 30 April 2025 and contain some very strong headline numbers:

Revenue up 33% to £270.0m

Adjusted operating profit up 30% to £27.5m

Adjusted operating margin: 10.2% (FY24: 10.4%)

Adjusted earnings up 27% to 54.4p per share

Net cash down 77% to £5.3m (due to acquisition)

Order intake down 27% to £284.7m

Closing order book up 19% to £616.4m

Dividend up 10% to 16.3p per share

At this high level, I think there are a few useful points to note:

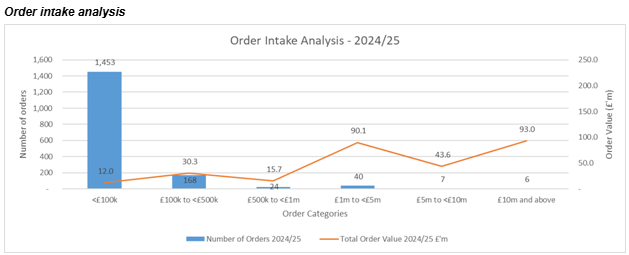

Order intake: this fell sharply last year, but the company says that the FY24 order intake included a long-term Royal Navy order worth £135m, without which order intake would have risen by 11% last year. Navy work is typically very long term, so is also inherently lumpy.

This is a contrast to the majority of the group’s orders, which are for relatively small amounts:

Order book: order book growth looks strong last year, but the closing order book included £80m acquired with EM Solutions.

Stripping this out shows organic growth in the order book of just 3.4% last year – again, this can partly attributed to the big Royal Navy order in FY24.

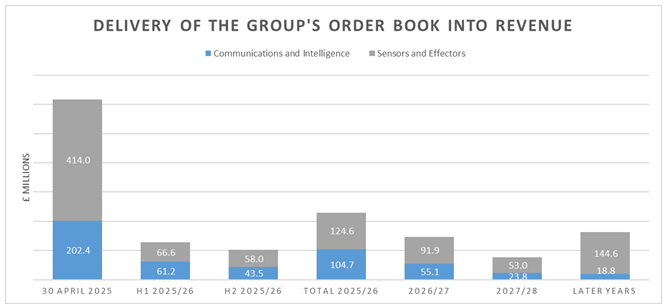

FY26 revenue coverage: the closing order book is equivalent to 2.3x FY25 revenue, but this includes deliveries stretching out to the mid-2030s. FY26 revenue cover was 79% (£230m) at the end of the year, although management say this has since risen to 85% – that seems pretty reassuring to me at this early stage.

The company helpfully provides a chart showing the expected revenue delivery from the year-end order book:

Net cash was maintained despite the £75m acquisition of EM Solutions. This was made possible because Cohort raised £40m through a placing in addition to drawing down

Profit adjustments: statutory operating profit of £26.1m is very close to last year’s adjusted operating profit figure of £27.5m.

Sadly, this doesn’t mean there were no adjustments – only that the positive and negative numbers largely cancelled each other out:

Cash conversion: I’m inclined to take a relaxed view on these adjustments because cash conversion is generally good in this business.

After stripping out acquisitions and working capital movements from last year’s numbers, I estimate FY25 underlying free cash flow of £18.5m.

That represents a very respectable 94% conversion from net profit and is sufficient to have covered both the dividend and £4m of share buybacks last year, with room to spare.

However, using this measure of free cash flow for valuation gives the stock a free cash flow yield of just 2.5%. That’s equivalent to a P/FCF of 40 – not cheap at all.

Trading commentary

Cohort is a group of semi-autonomous businesses that benefit from central support. However, for reporting purposes the company categorises revenue into two core markets:

Communications & Intelligence up 51% to £124.9m (net margin: 16.9%)

Sensors and Effectors up 21% to £145.1m (net margin: 8.7%)

Geographically, Cohort generates more than half its revenue in the UK, with the remainder coming from exports and domestic sales for various overseas subsidiaries::

UK revenue up 36% to £147.9m

Non-UK domestic revenue up 36% to £28.4m

Export revenue up 24% to £87.3m

Last year saw stagnant performance in much of Europe, but strong growth in Australia, Portugal and the Americas.

The company comments that increased NATO spending plans in Europe are positive. CEO Andrew Thomis sounds particularly confident about the prospects for Naval orders and drone-related products.

Outlook & Estimates

FY26 adjusted earnings are now expected to be ahead of previous expectations – good news. But by how much?

I don’t have access to any updated broker notes today, but we do have some guidance from the company (my emphasis):

These factors together mean that adjusted EPS are likely to be ahead of our previous expectations. Our longer term prospects remain strong, with the potential for c.10% earnings growth in the following two financial years.

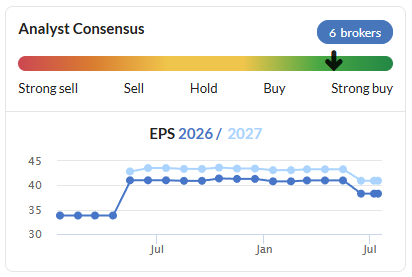

Checking Stockopedia’s consensus forecasts suggests that FY26 earnings were previously expected to be 56.8p, 4.4% above today’s FY25 adj EPS figure of 54.4p.

Adding 10% to FY25 earnings for the next two years gives me the following estimates:

FY26E EPS: 59.8p (prev. 56.8p)

FY27E EPS: 65.8p

It’s worth pointing out that the FY26 earnings upgrade implied by today’s commentary is only c.5%. However, the shares have risen by around 15% this morning, meaning that Cohort has just got more expensive (again).

At 1,746p, the stock is now trading on a FY26E P/E of 29, falling to 26x in FY27.

Roland’s view

Are Cohort shares becoming too expensive? The value investor in me wants to say yes. But in reality, I think it could still be too soon to call time on this rally.

Strong momentum often persists for longer than expected and today’s guidance appears quite clear. It’s not the first upgrade in the last 18 months, either:

Management also says that profit margins are expected to improve over the next couple of years, thanks to a changing mix and a margin-accretive contribution from recent acquisition EM Solutions. The company is targeting a net margin in the “low to mid-teens percent” within the next three to five years.

Higher margins could mean that profit growth outpaces revenue growth, supporting further share price and valuation gains – factors Ed highlighted in his multibagger article this week.

I can’t be fully positive at this valuation. But I am going to leave my AMBER/GREEN view unchanged today, out of respect for Cohort’s strong progress and improved outlook.

Mark's Section

Creightons (LON:CRL)

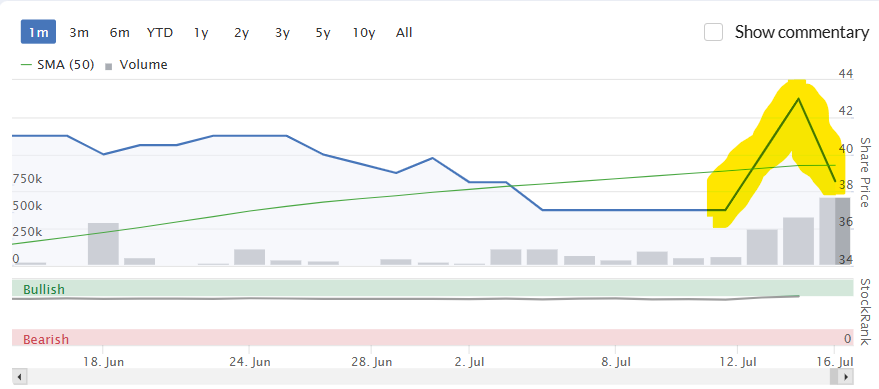

Down 10% to 38.5p - FY25 Audited Results - Mark - AMBER

Toiletries and fragrances manufacturer Creightons has a strong following amongst individual investors. Mainly because the share price did very well from 2018 to 2021, aided by their ability to supply alcohol hand gel to the COVID market (a strange misnomer from a wrong initial assumption that COVID was mainly transmitted by touch, and hence protected by hand-washing, rather than the largely airborne virus it proved to be!):

However, the company got hit by the inability to pass on cost inflation following the Ukraine invasion, and several management missteps. These included a move into more branded products via acquisition some of which were paid for by guaranteeing the then high share price as part of the deal. A change of management at the top, with the highly-regarded Pippa Clarke taking the helm has helped rebuild market confidence, helped by a return to profitability:

The shares price has done very well this year in a tricky market:

This has made it a popular stock again. However, with the share price reacting negatively to today’s results, has that exuberance proven misplaced?

Well, it is worth noting that excited investors had bid the share price up into these results, so it was likely to fall whatever they were:

With the results themselves, an initial look at the revenue figures leaves one a little underwhelmed:

Revenue increased by £0.9m (1.6%) to £54.1m (2024: £53.2m), driven by private label sales growth

o Private label £29.2m (2024: £23.8m)

o Branded products £18.2m (2024: £21.0m)

o Contract manufacturing £6.7m (2024: £8.4m)

Private label, where Creightons works with retailers to develop the retailers products and manufacture them has been the star of the show. Whereas their own brands and contract manufacturing (manufacturing existing products for other companies) have been weak.

They say they are in the “...process of reducing and repositioning the branded portfolio by phasing out underperforming brands and products” and that they are refocusing on their key brands of Emma Hardie, Feather & Down, TZone, The Curl Company and Creightons Haircare. Emma Hardie has continued to see sales decline but is profitable as a brand for the first time.

Given that their own branded products should be the highest margin part of the business, they have down well to increase gross margin and profit:

Gross profit increased by £1.3m (5.8%) with gross profit margin up 180 bps to 44.7% (2024: 42.9%)

The key to this has been an increased pursuit of operational excellence, with several initiatives intended to maximise “labour productivity at every stage of the process”. These include automated document management, implementing a warehousing management system, increasing automation and upskilling employees.

Efficiency has been the name of the game in all areas:

Distribution costs have decreased by 20.8% to £2.8m (2024: £3.5m) despite an increase in revenue. This reflects the ongoing benefits of actions implemented in the prior year, including the decision to bring the picking and packing of finished goods in-house and exit third-party logistics arrangements where possible…

Administrative expenses rose by £0.1m to £17.9m (2024: £17.8m), despite revenue increasing by £0.9m. This growth in revenue was achieved without a material increase in overheads, demonstrating a lean and efficient cost structure.

The result of increasing gross margins and flat administration costs is a big jump of operating profit from £1.5m to £3.5m, although this is part because the profit is the difference between several much larger numbers. EPS comes out at 3.29p. There are no forecasts in the market, but FWIW, this figure is slightly ahead of my own estimate.

Balance sheet:

This sounds good:

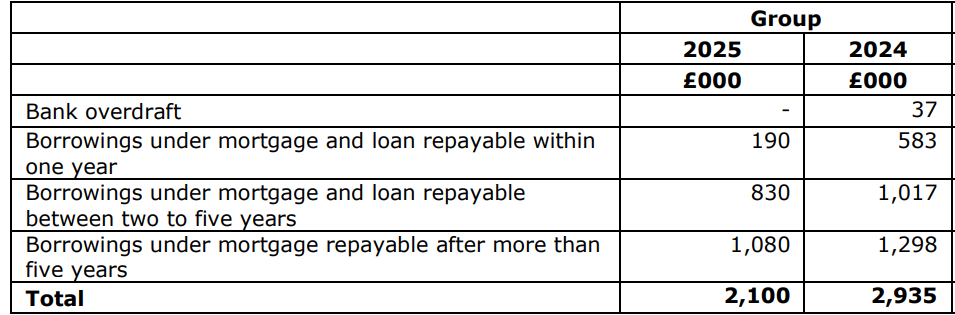

Net cash on hand is positive £3.0m (2024: positive £2.2m).

However, I don’t like their definition of net cash “on hand” as it excludes some of their debt. Here is the details from the Annual Report:

I can see why they have done this as the main debt is the mortgage they took out to buy the property they previously let in Peterborough. However, I prefer that companies are as conservative as possible with these things, as those reading just the headlines may assume that there is no debt, which is untrue.

The rest of the balance sheet looks strong with stable working capital and a reasonable current ratio. Net tangible assets are around £16.2m which is reasonable, but of course won’t provide any price support from current levels if the company were to face further issues.

Outlook:

With no forecasts yet in the market (this may change at some point) the outlook here is key to assessing the company and this is quite cautious:

The next year will not be without its challenges largely a result of factors outside the Group's control.

They go on to list credit risk for customers, which they do insure for where possible, but may impact which customers they are willing to sign, and secondary effects from US tariffs, such as increased supply to the UK from Asia. However, the major impact is:

Managing the impact of the increase in employers’ national insurance and the national minimum wage, together with associated pay increases to maintain pay differentials will cost the Group £0.9m. Our customers are facing similar challenges therefore, it is proving difficult to raise sales prices in the current market environment to offset these rising employment costs. The project to improve performance to alleviate the impact is ongoing.

Given that they have yet to fully mitigate these costs, and it appears cannot raise prices, there is a real risk that FY26 EPS is below that of FY25. Worryingly they don’t seem to give any concrete numbers for Q1 sales, which is a number they must surely now know from management accounts.

Strategy:

They say that this has been recently reviewed. They key part appears to be a break from the (failed?) strategy of the previous management to significantly grow the business through the acquisition of further brands. Instead it seems far more steady-as-she-goes:

Concentrate resources on developing existing business and will only consider acquisition opportunities if the opportunity offers significant immediate benefit to stakeholders.

They also seem to be jumping on the dupes trend:

Allocate additional resources to a team dedicated to developing the timely launch of 'fast follow' products and better capture market opportunities. This new multi-disciplinary team will develop and launch product at speed to meet fast-emerging market trends. The products could be sold under our own brands, as private label, or retailer specific brands. Existing revenue streams will remain fully resourced to ensure there is no negative impact on the remaining business.

Whether they have the skills or abilities to compete with more established players here remains to be seen. However, it doesn’t sound like they will be risking much by giving it a go.

Valuation:

With the shares around 40p they are trading at 12x historical EPS. This isn’t expensive, but if FY26 EPS falls on higher cost inflation the multiple may well look stretched. Historically, this has been a cheaply rated share, as the market has recognised that private label and contact manufacturing businesses are not typically high-quality ones.

Mark’s view

There is a lot to like here. The accounts have very few adjustments (and none this year), directors are paid modestly and they have done well to recover the business following previous management missteps. If they can grow sales again, particularly on the branded side, then we may see sustainable growth in EPS which will make them look good value. However, in the short-term there looks a real risk to me that FY26 EPS will be below FY25 levels, making them look expensive on forward earnings multiples, especially for this type of business. The well-regarded management have the ability to grow the branded side of the business which may justify a higher rating. However, this will be steady progress as they are culling unprofitable brands and focussing on key ones. The appetite for adding brands via acquisition also seems low. Overall, I think an AMBER rating best sums up the balance between these risks and opportunities.

McBride (LON:MCB)

Down 12% to 133p - Full Year Trading Update - Mark - AMBER

This update is in line on adjusted operating profit. However, it looks to be a miss on revenue (at least compared to what Stockopedia's data provider Refinitiv give us):

Group revenue was 0.7% higher than the prior year period on a constant currency basis. The Group continues to make progress in its strategic markets and geographies, driven by strengthening customer partnerships. Total volumes were up 4.3% relative to the prior year period with private label volumes up 1.4% and contract manufacturing volumes up 48.9%, driven by the full-year impacts of significant new long-term contracts.

+0.7% on £935m is £942m, slightly below the £952m consensus in Stockopedia:

Volumes were up, so pricing pressure appears to be the reason that the revenue growth isn’t stronger:

Whilst demand for private label products remains strong, there are signs that private label market share has stabilised at current levels. In light of continuing inflationary pressures, many retailers are seeking value to support their consumer proposition with an increased requirement for cost out actions to support lower market pricing.

Plus it seems that currency is also an issue as broker Zeus are actually forecasting reported revenue to decline to £933.3m. Zeus’ figures for EPS are slightly below FY24 actuals, presumably due to different adjustments. However, the outcome is the same, flat EPS all through the forecast window:

There is good news on the debt:

The Group continued its focus on net debt reduction resulting in net debt closing at £105.2m, a £26.3m reduction versus the prior year end (30 June 2024: £131.5m), representing a net debt cover level of 1.2x.

And they now feel comfortable enough to reinstate dividends. However, this is unlikely to be particularly impressive at a forecast yield of around 2%. Even at reduced levels the debt remains a significant part of the capital structure for a £250m market cap company.

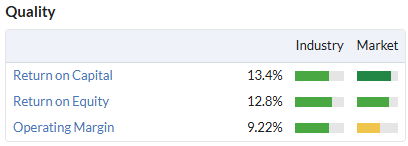

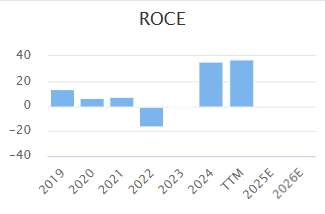

The company has a decent ROCE (at least on 2024 reported EBIT):

Giving a strong Quality Rank:

However, this does shareholders no good if the company can’t deploy incremental capital at these rates to grow earnings. The flat earnings forecast through to at least 2027 make the P/E of around 7 look about right, especially if we adjust for the debt levels.

Mark’s view

While I see nothing obvious in today’s update that should cause such a big drop in share price, it does highlight that the shares look fully valued at current EPS growth rates, even on the current modest rating. It may just be that shareholders who were attracted by the recent share price momentum have decided to take profits.That Momentum Rank looks likely to fall in the short term, and as such I think a neutral stance is best for the moment, at least until we get some indication that EPS can start growing again from here. AMBER

See what our investor community has to say

Enjoying the free article? Unlock access to all subscriber comments and dive deeper into discussions from our experienced community of private investors. Don't miss out on valuable insights. Start your free trial today!

Start your free trialWe require a payment card to verify your account, but you can cancel anytime with a single click and won’t be charged.