Good morning! Let's see what the RNS has in store for us today.

Today's Agenda is complete. It's another very busy day for updates but amazingly, everything is either "in line" or "ahead" - so portfolios should be doing ok!

All done for today, thank you.

Companies Reporting

| Name (Mkt Cap) | RNS | Summary | Our view (Author) |

|---|---|---|---|

AstraZeneca (LON:AZN) (£159bn) | New US manufacturing facility for weight loss portfolio. Targeting 50% US revenue by 2030. | ||

Compass (LON:CPG) (£42.8bn) | Upgrading FY25 guidance. Now expect adj op profit +11% w/organic rev +8%. Acquiring Vermaat for €1.5bn. | ||

Centrica (LON:CNA) (£7.6bn) | Acquiring 15% equity stake for £1.3bn. Expect 10.8% allowed return on equity. | ||

Inchcape (LON:INCH) (£2.9bn) | Askja is Iceland’s leading automotive distributor with FY24 revenue of £150m. | ||

Petershill Partners (LON:PHLL) (£2.6bn) | AUM +4% to $351bn w/ fee-paying AUM +5% to $245bn. Realisation losses of $6bn in H1. | ||

MITIE (LON:MTO) (£1.73bn) | Rev +10% to £1,282m, contract wins/renewals of £1.2bn TCV. Avg daily net debt £238m. | ||

Greencore (LON:GNC) (£1.06bn) | SP +11% Rev +0/9% in Q3, +7.6% year-to-date. Upgrading FY profit guidance, adjusted operating profit to be £118-121m (previous range £114-117m). Profit conversion ahead of expectations due to strong volume momentum and cost management. Greencore is the world’s largest producer of fresh, pre-packaged sandwiches. Major transaction with Bakkavor to complete in early 2026 subject to regulatory approval including the UK’s CMA. | PINK (AMBER/GREEN) (Graham) [no section below] There’s a major ongoing M&A situation here with the anticipated takeover of Bakkavor for £1.2bn, in a combination of shares and cash that will see Bakkavor shareholders own 44% of the combined group. I’m therefore going to leave this on “PINK” as the successful outcome of this acquisition (really a merger?) is key to the investment case. There is no mention of balance sheet numbers in today’s trading update but Greencore's net debt did reduce by over £60m (to £136m) as of H1/March 2025. I think the cash element of the takeover will cost nearly £500m and so it’s important that Greencore’s finances are as healthy as possible in the run-up to this transaction. I’m happy to take a moderately positive stance given the positive trading update, the defensive nature of the sector, and seeing as GNC’s leverage multiple did fall below 1x as of the H1 results. Bakkavor’s net debt was 1.1x as of March 2025, so both companies are now modestly leveraged. | |

Kier (LON:KIE) (£941m) | FY24 to be in line with exps. Y/end order book c.£11bn, 88% secured for FY26. CEO retiring. | ||

ME International (LON:MEGP) (£820m) | Rev +2.3%, PBT +13.3% to £34m. Growth driven by laundry w/ rev +18%. FY25 outlook in line. | PINK (AMBER/GREEN) (Roland) [no section below] As usual, ME Group’s accounts are clean and reflect high margins and good cash generation. The company confirms its focus remains on the laundry (faster growth) and photobooth (cash cow) businesses. Today’s half-year results haven’t moved the market and seem comfortably free of surprises to me. I covered the main points from the half-year trading update in June and do not see anything in these accounts to change my positive view. The company officially remains up for sale and considering its options. | |

Apax Global Alpha (LON:APAX) (£786m) | Recommended Acquisition (y’day pm) | Cash offer from Apax Partners at €1.90 per share; 17.1% discount to Q2 NAV of €2.29 | PINK |

GB (LON:GBG) (£573m) | Q1 trading in line with exps, FY outlook unchanged. Expect growth to be H2 weighted. The majority of FX headwind based on current exchange rates is already priced into market expectations (implying a small downgrade might be necessary if rates stay where they are). £25m share buyback has been approved and necessary workstreams underway to support their proposed application to move from AIM to the Main Market. | AMBER/GREEN (Graham) [no section below] Roland covered GB’s full-year results in detail last month and the company is back again with an AGM statement. Earnings forecasts have been stable since April with the company offering relatively unimpressive numbers for a software group: very modest growth and limited returns on capital (ROCE only 1%). Forecasts in the market currently suggest that turnover will be flat this year (FY March 2026) and the company says its outlook remains consistent with these expectations. As today’s update is light on numbers for FY26, but in line with expectations, I can leave our existing stance unchanged. The earnings multiple is inexpensive at 12x and I think the sector (identity verification/fraud prevention) should provide plenty of opportunities for growth over the long-term, so on balance I do think there is more to like than to dislike. The proposed move to the Main Market could also widen the pool of potential investors, with a marginally positive impact on valuation. | |

Metals Exploration (LON:MTL) (£356m) | SP +7% Q2 revenue +46% to £70.5m, pre-tax free cash flow + 101% to $47.2m. Net cash $43.5m. Gold sales +26% to 23.0koz at an average price of $3,061/oz. All-In Sustaining Costs (AISC) were $1,098/oz, 15% below the same period last year. | AMBER/GREEN (Roland) [no section below] Today’s Q2 results look pretty strong to me and appear to be ahead of forecasts produced by advisory Hannam & Partners. The Runruno gold mine in the Philippines appears to be a cash cow at current gold prices. But it’s worth remembering this mine is the group’s sole source of production and is only expected to have a remaining life of “two/three years” (as per FY24 results). Work is underway to bring the La India deposit in Nicaragua into production and MTL has also identified exploration prospects close to Runruno with the potential to extend production from this region. As yet, however, there’s no other production – in my view, this means the company will need to shepherd its cash balance and explains the lack of any shareholder returns. Although the forward P/E of 5.5 is tempting in a high gold price environment, I think investors need to consider the risk that the gold price could fall and/or that future earnings may be delayed or run over budget. With the caveat that I view this as a speculative situation with a certain amount of cliff-edge risk, I’m going to maintain my previous moderately positive view on this NAPS portfolio stock. | |

Fuller Smith & Turner (LON:FSTA) (£311m) | LFL sales +5% in 16 weeks to 19 July. Chairman Turner retiring after 47 years. | ||

Marston's (LON:MARS) (£279m) | LFL sales +2.9% in 15 weeks to 12 July. FY25 PBT to be in line with exps. | ||

Big Technologies (LON:BIG) (£279m) | Revenue -6.4%, adj EBITDA -12.6% to £12.5m. Additional £4m FX loss. Net cash £94.9m. | ||

Evoke (LON:EVOK) (£277m) | Q2 rev +5% YoY, H1 +3%. Exp H1 adj EBITDA £163-167m with FY expectations unchanged. | RED (Graham holds) I'm leaving our RED stance unchanged given the weak balance sheet, although the company continues to work on a deleveraging plan before its debts come due. There are probably more entertaining ways to gamble money than investing in these shares. | |

Thor Explorations (LON:THX) (£270m) | Completed 3,000m of RC drilling. “Great start to our drilling activities in Cote d’Ivoire” | ||

Yu (LON:YU.) (£263m) | H1 rev +9% to £341m, avg monthly bookings -12%. FY25 EPS to be in line with exps. | AMBER/GREEN (Roland - I hold) Falling wholesale power prices are said to have increased competitive pressures and had a negative impact on revenue. Today’s trading update doesn’t split out the impact of volume and price changes, so we don’t have much insight on underlying market share growth. I think the broad picture here remains positive, but I can’t help feeling that growth rates may have slowed somewhat in H1. Until we learn more in September’s H1 results, I’ve opted to moderate our view slightly. | |

Luceco (LON:LUCE) (£225m) | H1 rev +15%, adj op profit +10%, exp to be £13.5-13.8m. 1.6x leverage. FY outlook unch.. | ||

Fonix (LON:FNX) (£214m) | SP -3% FY25 adj EBITDA +6.6% to £14.6m. New product launches & geographies. FY26: “confident”. Fonix is "a leading specialist in mobile operator payments, messaging and telephony", used by the likes of ITV, Comic Relief, and Children in Need. | AMBER/GREEN (Graham) [no section below] Thanks to sparkler in the comments for pointing out that the adj. EBITDA result for the financial year (£14.6m) is a slight miss against prior estimates at Cavendish (prior estimate: £14.8m). Gross profit is also a slight miss. Looking ahead, there is no change to the FY26 estimates, including adj. EBITDA of £16.2m. I'll moderate our stance on this by one notch seeing as this is on quite a high rating (P/E in the region of 20x) and today's update could be interpreted as minor profit warning. Quality metrics are excellent though - an interesting small-cap with blue-chip customers. | |

Netcall (LON:NET) (£188m) | Y25 results to be comfortably in line with exps. Rev +23%, adj EBITDA +17% to £9.8m. | ||

Capricorn Energy (LON:CNE) (£160m) | Collected $62m in Egypt in H1. Receivables $172m at 30 June. H1 WI production c.20kboepd. | ||

Arbuthnot Banking (LON:ARBB) (£156m) | H1 PBT -48% to £10.9m due to base rate cuts, NAV +4.7% to £16.49ps. Interim divi +10%. | ||

Motorpoint (LON:MOTR) (£152m) | Retail sales +10.6% in Q1, Board is confident will meet full year expectations. | ||

ASA International (LON:ASAI) (£128m) | Outstanding loan portfolio +16% from Q1, +37% year-on-year. Improved loan portfolio quality. | ||

Diaceutics (LON:DXRX) (£108m) | Rev +22% (cc). Order book £29.4m. 79% visibility on revenue forecast. Cash £10.4m | ||

Scancell Holdings (LON:SCLP) (£107m) | Phase 2 data shows strongly improved outcomes in Late-Stage Melanoma. | ||

Anexo (LON:ANX) (£81m) | Unconditional Recommended Contractual Offer & Proposed Tender Offer | Tender offer at 60p to return up to £12m. Separate unconditional offer: Bidco already owns >50%. Offer is 60p in loan notes. | PINK |

Headlam (LON:HEAD) (£70m) | In line outlook. Net debt £24m but subsequent sale and leaseback for £22m. | ||

hVIVO (LON:HVO) (£69m) | Outlook: revs £47m and low single digit LBITDA, improvement on previous guidance. | ||

Metals One (LON:MET1) (£47m) | £175k investment in Fulcrum Metals (LON:FMET). Participates in Fulcrum’s equity fundraise, gains 5.9% stake. | ||

Flowtech Fluidpower (LON:FLO) (£39m) | roject win: Narrow Water Bridge (€4.5m). Distribution agreements in fluid control and compressed air. | ||

Works co uk (LON:WRKS) (£37m) | Strong trading in first 11 weeks of FY26, in line. LfL sales +5%. Adj. EBITDA forecast £11m. | AMBER/GREEN (Roland) Rapid share price gains in recent months means a lot of the turnaround progress is now priced in. Rising employment costs are a concern this year and I don’t think the shares are as attractively valued as they were in May. Even so, I am impressed by recovering profitability at this retailer and encouraged by improved LFL sales performance so far in FY26. On balance, I think continued strong momentum is sufficient to allow me to leave our moderately positive view unchanged today. | |

Nexteq (LON:NXQ) (£37m) | Revenues expected in line. Market expectations: $85.5m rev, $6m adj. EBITDA, $3.6m adj. PBT. | ||

Solvonis Therapeutics (LON:SVNS) (£19m) | Initiation of key translational studies to support SVN-002 towards planned Phase 2b trial. | ||

Parkmead (LON:PMG) (£15m) | Successful conclusion of all post-completion tasks in sale of UK offshore petroleum licences. | ||

Eenergy (LON:EAAS) (£14m) | Outlook in line. Growing sales pipeline of c. £443m gross of which £138m is investment grade. | ||

B90 Holdings (LON:B90) (£13m) | In line. Priorities include continuing to scale & diversifying marketing channel mix. | ||

Surface Transforms (LON:SCE) (£12m) | Pivotal change in manf. yield and output. H1 rev +72%. Gross cash £1.2m. Cash constraints easing. | ||

IXICO (LON:IXI) (£10m) | Will pay in cash and analysis services for data usage rights. Directly accelerates R&D program. | ||

Mast Energy Developments (LON:MAST) (£10m) | Price is £50k, 50% cash and 50% new shares. Initial portfolio of 5 flexible generation projects. |

Graham's Section

Evoke (LON:EVOK)

Up 2% to 62.5p (£281m) - H1 2025 Post-Close Trading Update- Graham - RED

(At the time of publication, Graham has a long position in EVOK.)

An “in-line” trading update might not seem all that remarkable, but when you’re in a debt situation like Evoke is in, any bit of encouragement or reassurance is valuable.

evoke (LSE: EVOK), one of the world's leading betting and gaming companies with internationally renowned brands including William Hill, 888 and Mr Green, today announces a post-close trading update for the three and six months ending 30 June 2025 ("Q2" and "H1" respectively).

There is no change to FY25 expectations.

The company reiterates its confidence in achieving its targets of 5-9% revenue growth and adj. EBITDA margin of at least 20%.

Digging into the quarterly performance a little, I see that Q2 revenue growth was 5% year-on-year, an improvement from only 2% in Q1. I covered the Q1 update here. Online continues to outperform Retail (i.e. physically betting shops - William Hill).

This is an odd-numbered year, which means there is no boost from the World Cup or Euros.

Overall H1 revenue growth is 4% at constant currencies. That does leave a shortfall to cover in terms of the full-year growth target, but the company says “the anticipated growth in the second half is supported by product delivery, improved marketing returns, and further cost savings, with continued execution of the Group's strategy and value creation plan.”

H1 adjusted EBITDA is expected in the range of £163-167m, which takes last twelve months' EBITDA to >£360m, “representing significant year-over-year growth and delivering another period of strong deleveraging”.

CEO comment says “we continue to transform the Group's capabilities for the mid- and long-term”.

Graham’s view

At a market cap of less than 1x trailing EBITDA, this share is all about A) the balance sheet, and B) whether the company convert its adjusted EBITDA into real cash flow and profits.

The scale of adjustments has been awful here, a topic I’ve touched on before. See the last full-year results, when £230m of EBITDA became an actual after-tax loss of £191m.

And when I investigated the cash flow statement, I concluded that the company did not earn enough real cash flow to pay its interest bill last year.

Therefore, despite owning the share, I’ve been RED on it. (I invested in it when it had a strong balance sheet, prior to the William Hill acquisition, and have been stubbornly holding on since then.)

There is one very important metric that has started moving in the right direction, albeit not as quickly as anticipated: the leverage multiple (net debt to EBITDA).

This was 5.9x at the end of 2023.

It was 6.7x at H1 2024.

It was 5.7x at the end of 2024.

We’ve been promised that it will be below 5x by the end of 2025.

5x is still unacceptably high, but at least it's moving in the right direction.

They need to reduce this multiple as quickly as possible. Ideally they would get to 3x, but I don’t expect that to happen, in good time before their €582m note matures in July 2027.

As things stand, I am nervous of what the bond market might demand of the company in order to allow a refinancing.

If we are willing to use bond prices as a signal, there is some reassurance from the fact that the 2027 bond is trading around par:

There is also a £400m 2030 bond trading well:

Source: Börse Frankfurt

If bond investors were very nervous, they would be dumping Evoke’s notes at these prices. So I do take reassurance that this hasn’t happened yet - although it doesn’t prove that the equity is safe! Bond investors can be wrong, too.

At the ratings agency Fitch, there has been no change: the credit rating is still B+, outlook negative. Anything in the B category is considered to have “material default risk”, but “a limited margin of safety remains”. That’s a margin of safety for the bonds, not for the equity!

At Moody's, there was a downgrade in February this year, from B1 to B2.

I think I need to leave this at RED, due to the ongoing weakness of the balance sheet. Of course if the company pulls through, then I expect it to be a multi-bagger from the current level. But it could equally well turn out to be a zero. I do think that the risk:reward might be reasonably good, but there are probably more entertaining ways to gamble money than this. If I didn’t already own it, then I would be in no rush to buy it. But as it’s only worth 1% of my portfolio at this stage, I am not overly stressed about the outcome.

Roland's Section

Yu (LON:YU.).

Down 2% to 1,560p (£262m) - Trading Update & CFO Transition - Roland - AMBER/GREEN

(At the time of publication, Roland holds a long position in YU.)

Yü Group (AIM: YU.), the independent supplier of gas and electricity, meter asset owner, and installer of smart meters to the UK SME & corporate sector, is pleased to provide an update on trading for the six months ended 30 June 2025.

YU Group is a member of my rules-based SIF Portfolio and of Ed’s current NAPS portfolio. So we both have high hopes for further growth from the business this year!

As subscriber bohenie points out in the comments this morning, the shares have tended to be quite volatile – something that’s reflected in the stock’s Speculative RiskRating:

However, the general direction of travel has been positive in recent years and – personally – I am broadly positive on the founder-CEO’s high level of share ownership.

Today’s update is billed as an in line update, although my feeling is that there are some nuances to this that are worth noting.

Here’s a summary of the main highlights:

H1 25 revenue up c.9% to £341m

Average monthly bookings down 12% to £41.4m, reflecting lower wholesale power prices - sadly the company doesn’t provide a reading of volumes with price movements stripped out

Meter points +48% YoY to 107,000 with increased volumetric consumption

Yu Smart (the smart meter business) - meters owned +179% to 36,500

Forward annualised index-linked income from smart meters up 200% to £1.8m

Net cash £109.9m

CEO transition: long-serving CFO Paul Rawson is standing down as CFO and will become a non-exec. He is effusively thanked by CEO Bobby Kalar.

Rawson is being replaced by Andy Simpson, who joined in February 2025 as Group Finance Director and will assume the CFO role on 1 September.

Simpson appears to have no board-level plc experience, but was previously a senior manager at BT Openreach overseeing a £1bn revenue service business. He seems to have plenty of relevant experience in telecoms and billing – as I’ve commented previously, managing bad debt successfully is a key element of Yu’s profitability.

Outlook & Estimates: full-year earnings expectations are unchanged, although Yu warns that falling wholesale prices have created a more competitive market environment.

We also have an updated note today from house broker Panmure Liberum – many thanks.

PanLib’s analysts have left their EPS estimates unchanged today despite cutting revenue forecasts by 4.7% for FY25-FY27:

FY25E EPS: 213.6p (unch)

FY26E EPS: 228.1p (unch)

FY27E EPS: 240p (unch)

Perhaps it’s worth noting that achieving these unchanged EPS estimates on lower revenue forecasts required some changes to margin assumptions (improved) and bad estimates (worsened). I assume these changes reflect the broker’s dialogue with management.

More broadly, it’s worth noting that in a business with commodity price exposure, revenue forecasts are always somewhat volatile and unpredictable. I wouldn’t be surprised to see further changes to these estimates over the next 6-12 months.

Roland’s view

The main frustration I have with today’s update is that the company has chosen not to split out the impact of changing power prices on revenue. This means investors are not able to understand the underlying growth rate in supply volumes and customer numbers for the core energy supply business.

Having said that, I’m encouraged by the continued strong growth in the number of meter points supplied. I also continue to view the smart meter business as an attractive longer-term source of higher-margin revenue, even though the current contribution is minimal.

Net cash of £110m at the end of June sounds deeply impressive and I certainly think the balance sheet is strong here for a £262m market cap business. However, I think it’s worth remembering that this business needs a certain level of liquidity to ensure it can handle fluctuating commodity prices and forward power purchases.

I think this view is supported by the company’s policy of targeting 3x dividend cover by earnings – clearly management believes it’s important to retain a significant portion of earnings for reinvestment or liquidity.

Having said that, I do think this cash should help to give Yu the flexibility it needs to be able to continue investing in medium-term growth.

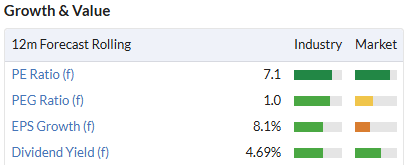

The valuation continues to look modest on around seven times forecast earnings and the dividend looks well supported to me:

CEO Bobby Kalar comments on the share price today, suggesting that he thinks the valuation is too low:

While I'm personally disappointed investor appetite remains restrictive, prolonged cash outflows from the UK continue to severely hinder our valuation.

I have to admit that CEOs complaining that their company’s share price is too low is a pet hate of mine. I think they should focus on running the business and accurately reporting progress to shareholders.

For example, I’d argue that greater clarity on underlying volume and customer growth might have supported a more positive reaction to today’s update. Or perhaps not – I can’t help feeling that the tone of today’s update suggests a slight weakening of growth rates so far this year.

The H1 results on 23 September should provide more insight on operational metrics.

For now, I am going to moderate our view to AMBER/GREEN. While I think fair value is somewhere above the current share price, I don’t see this as a business for which I’d want to pay a very high earnings multiple.

Works co uk (LON:WRKS)

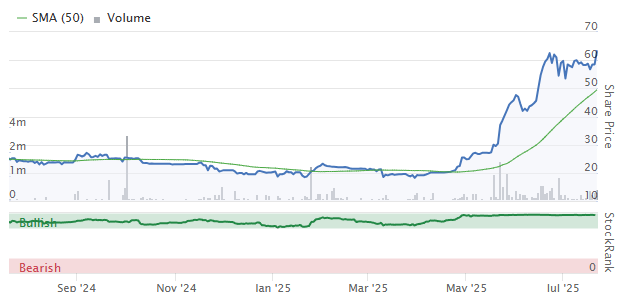

Up 9% to 64p (£40m) - Full Year Results - Roland - AMBER/GREEN

TheWorks.co.uk plc, the retailer of affordable, screen-free activities for the whole family, announces its preliminary results for the 52 weeks ended 4 May 2025 (the "period" or "FY25").

This retailer appears to be enjoying an impressive turnaround and has triple-bagged since April – congratulations to subscribers who spotted this opportunity earlier in the year:

The share price really gained momentum after the company upgraded its full-year guidance in May.

Today’s results are in line with those upgraded estimates and also reiterate guidance for FY26, which is the period ending 30 April 2026.

FY25 results highlights

Strong profit growth last year was driven by improved profitability rather than sales growth, perhaps highlighting the pressures on retailers at the moment:

Revenue down 2% to £277m (+0.8% LFL)

Reported pre-tax profit up 20% to £8.3m

Adjusted pre-tax profit up 44% to £4.6m

Adjusted operating margin: 3.4% (FY24: 2.7%)

Adjusted earnings up 69% to 7.1p per share

Net cash: £4.1m (FY24: £1.6m)

A few points jump out at me from these figures.

Revenue: first of all, the 2% fall in revenue is attributed to an extra trading week last year. Like-for-like sales growth was only marginally positive, suggesting that volumes and/or pricing power remained very constrained last year.

Pre-tax profit vs adjusted PBT: we are used to seeing adjusted profits that are higher than reported profits. Here we have the opposite situation!

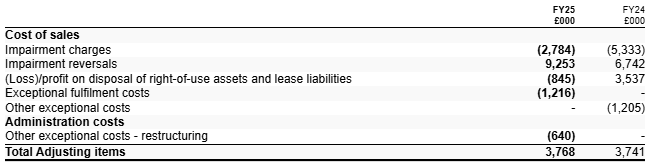

The explanation turns out to be quite simple. Due to improved trading and profitability, the company has been able to reverse some previous impairment charges against its store leases. This is the second consecutive year this has happened.

This resulted in a net impairment credit of £6.5m to the P&L in H1, offsetting various other costs and resulting in an overall £3.8m credit that was deducted to give adjusted pre-tax profit:

As shown above, it’s worth noting there were also new impairment charges last year:

FY25 impairment charges of £2.6m against 87 stores

FY25 impairment reversal of £8.6m against 253 stores

FY25 impairment reversal of £0.5m against the company’s website

Managing the store network to improve profitability is a key challenge here, especially given the increase in employment costs that will affect this year’s results.

Cash flow: today’s results report an increase in net cash, but the cash flow statement also shows £579k of interest paid on borrowings last year. So I think it’s reasonable to assume the £4.1m net cash figure is likely to be an annual peak.

Even so, cash generation was positive last year and showed fairly strong cash conversion from profits.

My sums suggest The Works generated free cash flow of £3.5m last year, representing 79% of adjusted net profit of £4.1m.

Outlook

The company reports a fairly strong start to the year, with like-for-like sales up by 5% in the first 11 weeks of FY26. It’s nice to see this figure running ahead of inflation.

Performance so far is said to be in line with expectations and ahead of the wider non-food retail market.

However, rising employment costs this year are expected to result in “significant cost headwinds in FY26”. Further cost savings are planned, but at this point management is leaving FY26 guidance unchanged, in line with forecasts introduced in May:

the Board expects to deliver pre-IFRS 16 Adjusted EBITDA in line with recently upgraded external forecasts of £11.0m.

Assuming this drops down to unchanged EPS forecasts for the year ahead, this leaves The Works trading on a FY26E P/E of 9.5 after this morning’s gains.

Roland’s view

I am impressed by the turnaround here and encouraged by the evidence of improving quality in the accounts. Margins rose last year and cash conversion was good, in my opinion.

The reversal of another big chunk of store impairment charges also seems like good news, as it implies The Works is improving the profitability of many of its stores.

However, the balance sheet still shows net lease liabilities of £13.1m, presumably implying that a number of stores remain loss making.

Today’s in-line guidance also suggests that earnings growth will slow sharply this year, unless forecasts are upgraded at some point:

I don’t think these shares offer the compelling value that was available a few months ago. After all, this is a low-margin retailer with a large store estate, potentially still including some loss-making stores.

However, I am impressed with progress. I’d argue that there could be some scope for further upgrades later this year, if LFL sales growth can be maintained and there is no repeat of last year’s logistics problems.

I’m going to leave our previous AMBER/GREEN view unchanged today, reflecting strong momentum and the potential for further improvements in profitability.

See what our investor community has to say

Enjoying the free article? Unlock access to all subscriber comments and dive deeper into discussions from our experienced community of private investors. Don't miss out on valuable insights. Start your free trial today!

Start your free trialWe require a payment card to verify your account, but you can cancel anytime with a single click and won’t be charged.